17. To calculate the nominal cash flows, we increase each item in the income statement by the inflation

rate, except for depreciation. Depreciation is a nominal cash flow, so it does not need to be adjusted

for inflation in nominal cash flow analysis. Since the resale value is given in nominal terms as of the

end of Year 5, it does not need to be adjusted for inflation. Also, no inflation adjustment is needed

for net working capital since it is already expressed in nominal terms. Note that an increase in

required net working capital is a negative cash flow whereas a decrease in required net working

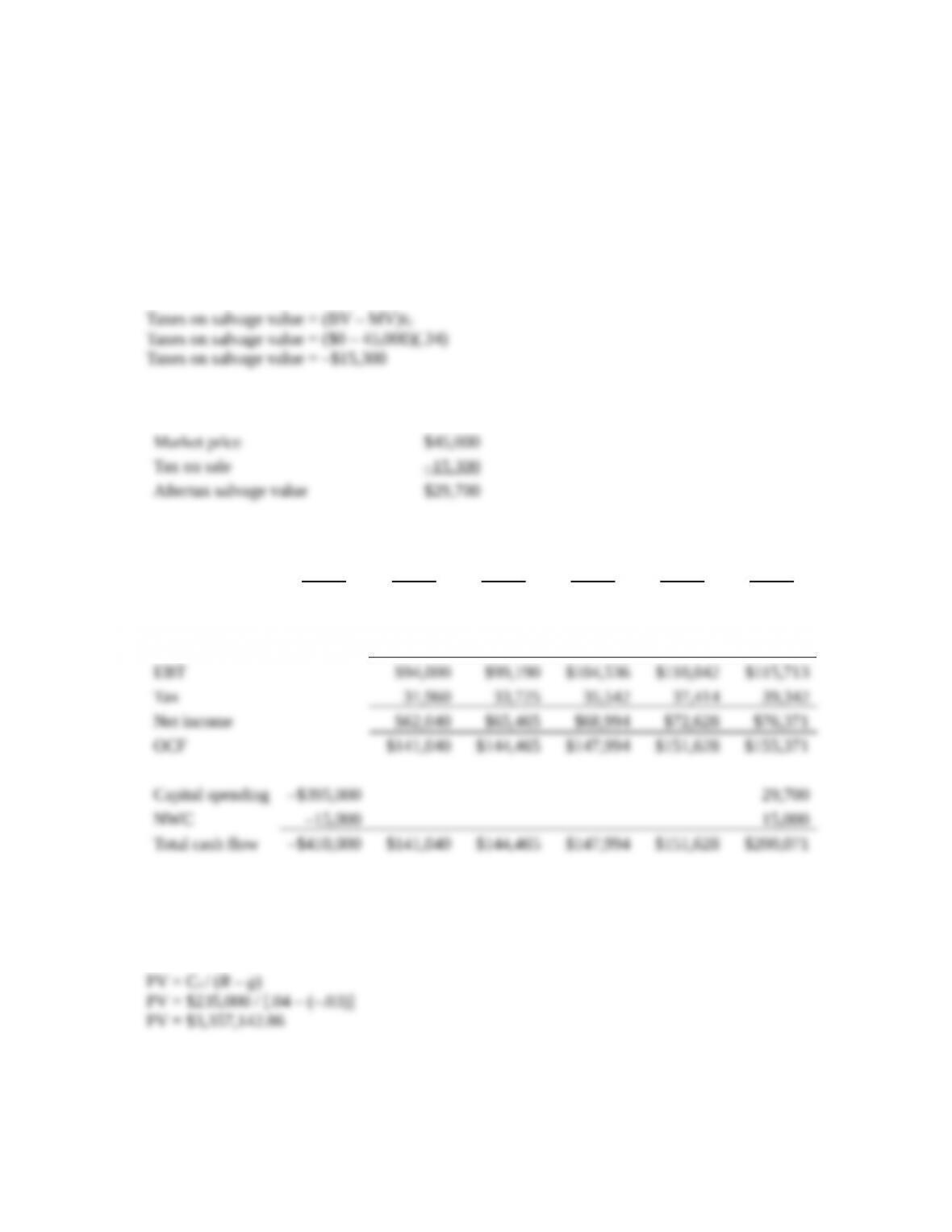

capital is a positive cash flow. We first need to calculate the taxes on the salvage value. Remember,

to calculate the taxes paid (or tax credit) on the salvage value, we take the book value minus the

market value, times the tax rate, which, in this case, would be:

So, the nominal aftertax salvage value is:

Now we can find the nominal cash flows each year using the income statement. Doing so, we find:

Year 0 Year 1 Year 2 Year 3 Year 4 Year 5

Sales $255,000 $262,650 $270,530 $278,645 $287,005

Expenses 82,000 84,460 86,994 89,604 92,292

Depreciation 79,000 79,000 79,000 79,000 79,000

18. The present value of the company is the present value of the future cash flows generated by the

company. Here we have real cash flows, a real interest rate, and a real growth rate. The cash flows

are a growing perpetuity, with a negative growth rate. Using the growing perpetuity equation, the

present value of the cash flows is:

19. To find the EAC, we first need to calculate the NPV of the incremental cash flows. We will begin

with the aftertax salvage value, which is:

Now we can find the operating cash flows. Using the tax shield approach, the operating cash flow

each year will be:

OCF = –$8,300(1 – .34) + .34($64,000 / 3)

OCF = $1,775.33

So, the NPV of the cost of the decision to buy is:

20. We will calculate the aftertax salvage value first. The aftertax salvage value of the equipment will be:

Taxes on salvage value = (BV – MV)tC

Taxes on salvage value = ($0 – 50,000)(.34)

Taxes on salvage value = –$17,000

Next, we will calculate the initial cash outlay, that is, the cash flow at Time 0. To undertake the

project, we will have to purchase the equipment. The new project will decrease the net working

capital, so this is a cash inflow at the beginning of the project. So, the cash outlay today for the

project will be:

Now we can calculate the operating cash flow each year for the project. Using the bottom up

approach, the operating cash flow will be:

Saved salaries $120,000

21. Replacement decision analysis is the same as the analysis of two competing projects, in this case,

keep the current equipment, or purchase the new equipment. We will consider the purchase of the

new machine first.

Purchase new machine:

The initial cash outlay for the new machine is the cost of the new machine, plus the increased net

working capital. So, the initial cash outlay will be:

Next, we can calculate the operating cash flow created if the company purchases the new machine.

The saved operating expense is an incremental cash flow. Additionally, the reduced operating

expense is a cash inflow, so it should be treated as such in the income statement. The pro forma

income statement, and adding depreciation to net income, the annual operating cash flow created by

purchasing the new machine, will be:

So, the NPV of purchasing the new machine, including the recovery of the net working capital, is:

And the IRR is:

Now we can calculate the decision to keep the old machine:

Keep old machine:

The initial cash outlay for the old machine is the market value of the old machine, including any

potential tax consequence. The decision to keep the old machine has an opportunity cost, namely, the

company could sell the old machine. Also, if the company sells the old machine at its current value,

it will receive a tax benefit. Both of these cash flows need to be included in the analysis. So, the

initial cash flow of keeping the old machine will be:

Next, we can calculate the operating cash flow created if the company keeps the old machine. There

are no incremental cash flows from keeping the old machine, but we need to account for the cash

flow effects of depreciation. The income statement, adding depreciation to net income to calculate

the operating cash flow, will be:

And the IRR is:

There is another way to analyze a replacement decision that is often used. It is an incremental cash

flow analysis of the change in cash flows from the existing machine to the new machine, assuming

the new machine is purchased. In this type of analysis, the initial cash outlay would be the cost of the

new machine, the increased NWC, and the cash inflow (including any applicable taxes) of selling the

old machine. In this case, the initial cash flow under this method would be:

The cash flows from purchasing the new machine would be the saved operating expenses. We would

also need to include the change in depreciation. The old machine has a depreciation of $1.35 million

per year, and the new machine has depreciation of $3.9 million per year, so the increased

depreciation will be $2.55 million per year. The pro forma income statement and operating cash flow

under this approach will be:

The NPV under this method is:

Using a spreadsheet or financial calculator, we find the IRR is:

IRR = 26.40%

So, this analysis still tells us the company should purchase the new machine. This is really the same

type of analysis we originally did. Consider this: Subtract the NPV of the decision to keep the old

machine from the NPV of the decision to purchase the new machine. You will get:

22. We can find the NPV of a project using nominal cash flows or real cash flows. Either method will

result in the same NPV. For this problem, we will calculate the NPV using both nominal and real

cash flows. The initial investment in either case is $750,000 since it will be spent today. We will

begin with the nominal cash flows. The revenues and production costs increase at different rates, so

we must be careful to increase each at the appropriate growth rate. The nominal cash flows for each

year will be:

Year 0 Year 1 Year 2 Year 3

$666,750.0

Capital spending –$750,000

Total cash flow –$750,000 $194,828.57

$205,355.5

7 $216,513.20

Year 4 Year 5 Year 6 Year 7

Revenues $735,091.88 $771,846.47 $810,438.79 $850,960.73

Capital spending

Now that we have the nominal cash flows, we can find the NPV. We must use the nominal required

return with nominal cash flows. Using the Fisher equation to find the nominal required return, we

get:

(1 + R) = (1 + r)(1 + h)

(1 + R) = (1 + .07)(1 + .05)

R = .1235, or 12.35%

So, the NPV of the project using nominal cash flows is:

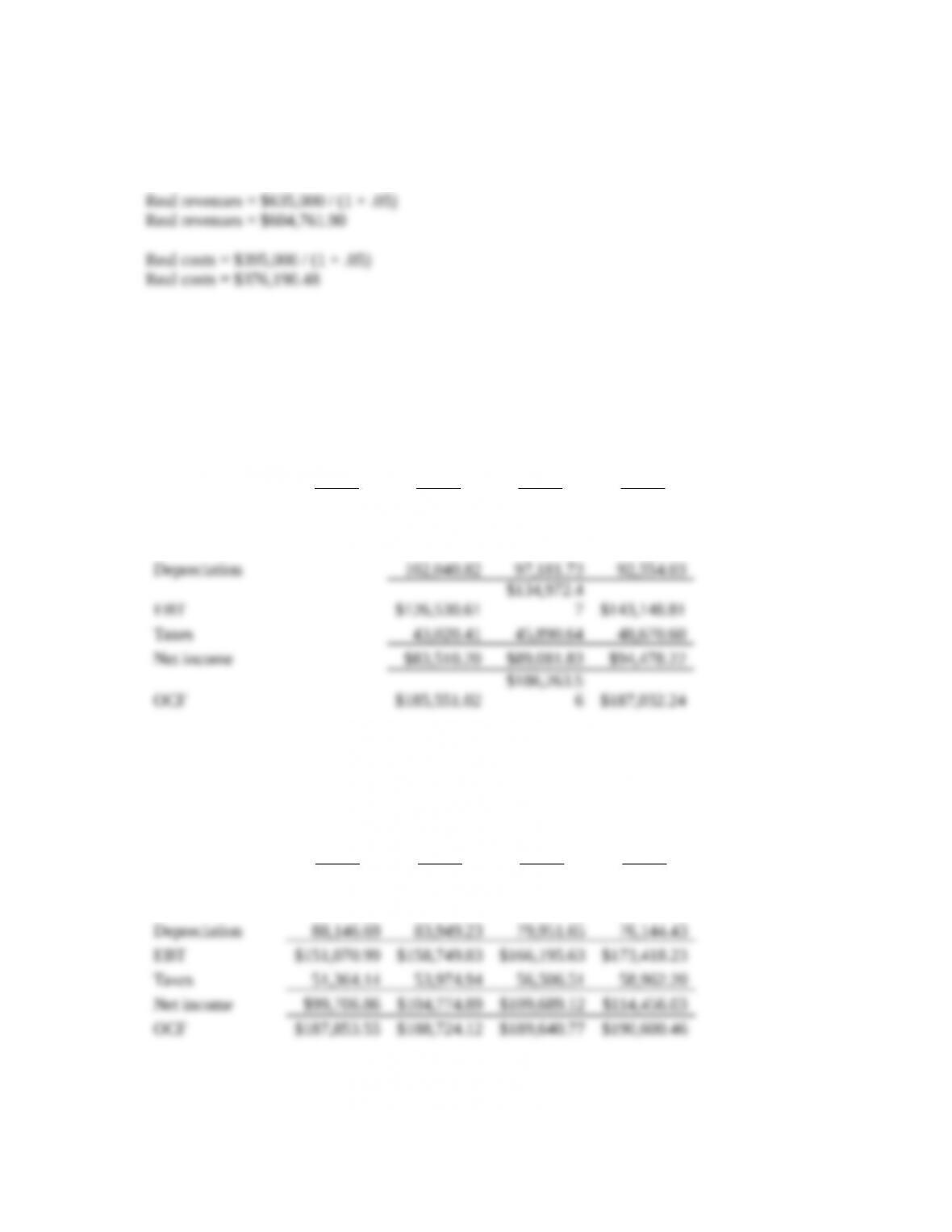

We can also find the NPV using real cash flows. Since the revenues and costs are given in nominal

terms, we must find the real value for each by discounting at the inflation rate. So:

Also, we must note that the costs are increasing at a different rate than the general inflation rate. As a

result, we must find the real cost increase, which is:

Real cost increase = [(1 + .04) / (1 + .05)] – 1

Real cost increase = –.0095, or –.95%

In real terms, the cost will actually decrease by .95 percent per year. So, the real cash flows will be:

Year 0 Year 1 Year 2 Year 3

Revenues $604,761.90

$604,761.9

0 $604,761.90

Costs $376,190.48 372,607.71 369,059.06

Capital spending –$750,000

Total cash flow –$750,000 $185,551.02

$186,263.5

6 $187,032.24

Year 4 Year 5 Year 6 Year 7

Revenues $604,761.90 $604,761.90 $604,761.90 $604,761.90

Costs 365,544.22 362,062.84 358,614.63 355,199.25

Capital spending

Total cash flow $187,853.55 $188,724.12 $189,640.77 $190,600.46

So, the NPV of the project using real cash flows is:

We can also find the NPV using real cash flows and the nominal required return. This will allow us

to find the operating cash flow using the tax shield approach. Both the revenues and expenses are

growing annuities, but growing at different rates. This means we must find the present value of each

separately. We also need to account for the effect of taxes, so we will multiply by one minus the tax

rate. So, the present value of the aftertax revenues using the growing annuity equation is:

And the present value of the aftertax costs will be:

PV of aftertax costs = C {[1 / (r – g)] – [1 / (r – g)] × [(1 + g) / (1 + r)]t}(1 – tC)

Now we need to find the present value of the depreciation tax shield. The depreciation amount in the

first year is a nominal value, so we can find the present value of the depreciation tax shield as an

ordinary annuity using the nominal required return. So, the present value of the depreciation tax

shield will be:

Notice, the NPV using nominal cash flows or real cash flows is identical, which is what we would

expect.

23. Here we have a project in which the quantity sold each year increases. First, we need to calculate the

quantity sold each year by increasing the current year’s quantity by the growth rate. So, the quantity

sold each year will be:

Now we can calculate the sales revenue and variable costs each year. The pro forma income

statements and operating cash flow each year will be:

Year 0 Year 1 Year 2 Year 3 Year 4 Year 5

Revenues $503,500.00 $543,780.00 $587,282.40 $634,264.99 $685,006.19

Fixed costs 115,000.00 115,000.00 115,000.00 115,000.00 115,000.00

Capital spending –$190,000

NWC –45,000 45,000

We could also calculate the cash flows using the tax shield approach, with growing annuities and

ordinary annuities. The sales and variable costs increase at the same rate as sales, so both are

growing annuities. The fixed costs and depreciation are both ordinary annuities. Using the growing

annuity equation, the present value of the revenues is:

And the present value of the variable costs will be:

PV of variable costs = C {[1 / (r – g)] – [1 / (r – g)] × [(1 + g) / (1 + r)]t}

The fixed costs and depreciation are both ordinary annuities. The present value of each is:

PV of fixed costs = C({1 – [1 / (1 + r)]t } / r )

PV of fixed costs = $115,000(PVIFA18%,5)

Now, we can use the depreciation tax shield approach to find the NPV of the project, which is:

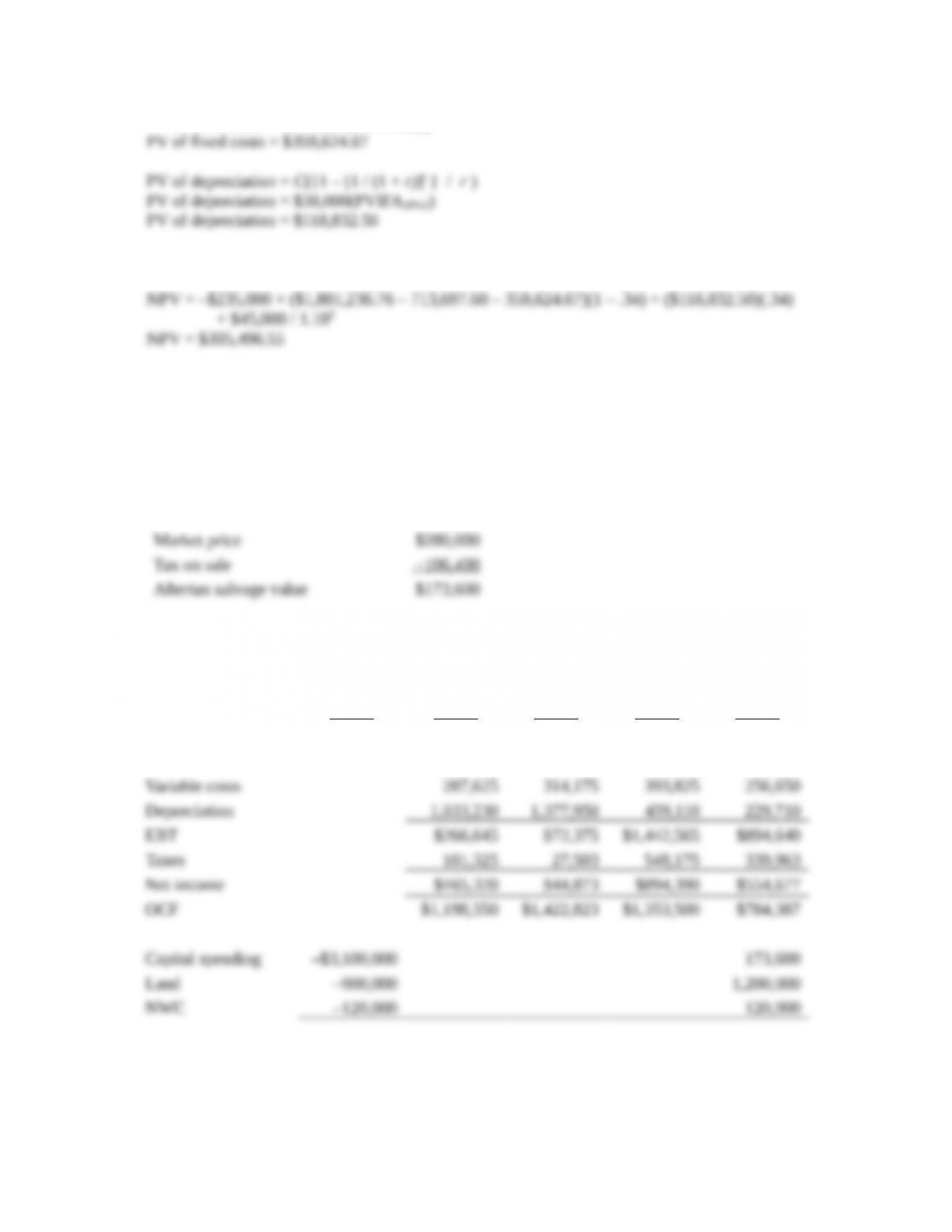

24. We will begin by calculating the aftertax salvage value of the equipment at the end of the project’s

life. The aftertax salvage value is the market value of the equipment minus any taxes paid (or

refunded), so the aftertax salvage value in four years will be:

Taxes on salvage value = (BV – MV)tC

Taxes on salvage value = ($0 – 280,000)(.38)

Taxes on salvage value = –$106,400

Now we need to calculate the operating cash flow each year. Note, we assume that the net working

capital cash flow occurs immediately. Using the bottom up approach to calculating operating cash

flow, we find:

Year 0 Year 1 Year 2 Year 3 Year 4

Revenues $1,917,500 $2,094,500 $2,625,500 $1,711,000

Fixed costs 330,000 330,000 330,000 330,000

Total cash flow –$4,120,000 $1,198,550 $1,422,823 $1,353,500 $2,277,987

Notice the calculation of the cash flow at Time 0. The capital spending on equipment and investment

in net working capital are cash outflows. The aftertax selling price of the land is also a cash outflow.

Even though no cash is actually spent on the land because the company already owns it, the aftertax

cash flow from selling the land is an opportunity cost, so we need to include it in the analysis. With

all the project cash flows, we can calculate the NPV, which is:

The company should accept the new product line.