CHAPTER 26 –

CHAPTER 26

SHORT-TERM FINANCE AND PLANNING

Answers to Concepts Review and Critical Thinking Questions

1. These are firms with relatively long inventory periods and/or relatively long receivables periods.

2. These are firms that have a relatively long time between the time that purchased inventory is paid for

3. a. Use: The cash balance declined by $200 to pay the dividend.

b. Source: The cash balance increased by $500, assuming the goods bought on payables credit

were sold for cash.

4. Carrying costs will decrease because they are not holding goods in inventory. Shortage costs will

5. Since the cash cycle equals the operating cycle minus the accounts payable period, it is not possible

for the cash cycle to be longer than the operating cycle if the accounts payable is positive. Moreover,

6. Shortage costs are those costs incurred by a firm when its investment in current assets is low. There

are two basic types of shortage costs. 1) Trading or order costs. Order costs are the costs of placing

7. A long-term growth trend in sales will require some permanent investment in current assets. Thus, in

1

CHAPTER 26 –

10. It is sometimes argued that large firms “take advantage of” smaller firms by threatening to take their

11. They would like to! The payables period is a subject of much negotiation, and it is one aspect of the

price a firm pays its suppliers. A firm will generally negotiate the best possible combination of

12. BlueSky will need less financing because it is essentially borrowing more from its suppliers. Among

Solutions to Questions and Problems

NOTE: All end-of-chapter problems were solved using a spreadsheet. Many problems require multiple

steps. Due to space and readability constraints, when these intermediate steps are included in this

solutions manual, rounding may appear to have occurred. However, the final answer for each problem is

found without rounding during any step in the problem.

Basic

1. a. No change. A dividend paid for by the sale of debt will not change cash since the cash raised

b. No change. The real estate is paid for by the cash raised from the debt, so this will not change

f. Decrease. The preferred stock will be repurchased with cash.

h. Decrease. The interest is paid with cash, which will reduce the cash balance.

i. Increase. When payments for previous sales, or accounts receivable, are paid off, the cash

k. Decrease. Here the dividend payments are made with cash, which is generally the case. This is

2

CHAPTER 26 –

2. The total liabilities and equity of the company are the book value of equity, plus current liabilities

and long-term debt, so:

We have NWC other than cash. Since NWC is current assets minus current liabilities, NWC other

than cash is:

NWC other than cash = Accounts receivable + Inventory – Current liabilities

Since total assets must equal total liabilities and equity, we can solve for cash as:

Cash = Total assets – Fixed assets – (Accounts receivable + Inventory)

So, the current assets are:

3. a. Increase. If receivables go up, the time to collect the receivables would increase, which

b. Increase. If credit repayment times are increased, customers will take longer to pay their bills,

f. No change. Payments to suppliers affect the accounts payable period, which is part of the cash

4. a. Increase; Increase. If the terms of the cash discount are made less favorable to customers, the

3

CHAPTER 26 –

b. Increase; No change. This will shorten the accounts payable period, which will increase the

c. Decrease; Decrease. If more customers pay in cash, the accounts receivable period will

d. Decrease; Decrease. Assume the accounts payable period and inventory period do not change.

e. Decrease; No change. If more raw materials are purchased on credit, the accounts payable

period will tend to increase, which would decrease the cash cycle. We should say that this may

not be the case. The accounts payable period is a decision made by the company’s management.

f. Increase; Increase. If more goods are produced for inventory, the inventory period will increase.

5. a. A 45-day collection period implies all receivables outstanding from the previous quarter are

Q1 Q2 Q3 Q4

Beginning receivables $335.00 $370.00 $420.00 $455.00

b. A 60-day collection period implies all receivables outstanding from the previous quarter are

collected in the current quarter, and:

(90 – 60)/90 = 1/3 of current sales are collected. So:

Q1 Q2 Q3 Q4

Beginning receivables $335.00 $493.33 $560.00 $606.67

c. A 30-day collection period implies all receivables outstanding from the previous quarter are

collected in the current quarter, and:

(90 – 30)/90 = 2/3 of current sales are collected. So:

4

CHAPTER 26 –

Q1 Q2 Q3 Q4

Beginning receivables $335.00 $246.67 $280.00 $303.33

6. The operating cycle is the inventory period plus the receivables period. The inventory turnover and

inventory period are:

Inventory turnover = COGS / Average inventory

Inventory period = 365 days / Inventory turnover

And the receivables turnover and receivables period are:

Receivables turnover = Credit sales / Average receivables

Receivables period = 365 days / Receivables turnover

So, the operating cycle is:

The cash cycle is the operating cycle minus the payables period. The payables turnover and payables

period are:

Payables turnover = COGS / Average payables

Payables period = 365 days / Payables turnover

So, the cash cycle is:

The firm is receiving cash on average 27.78 days after it pays its bills.

5

CHAPTER 26 –

7. a. The payables period is zero since the company pays immediately. Sales in the year following

this one are projected to be 15 percent greater in each quarter. Therefore, Q1 sales for the next

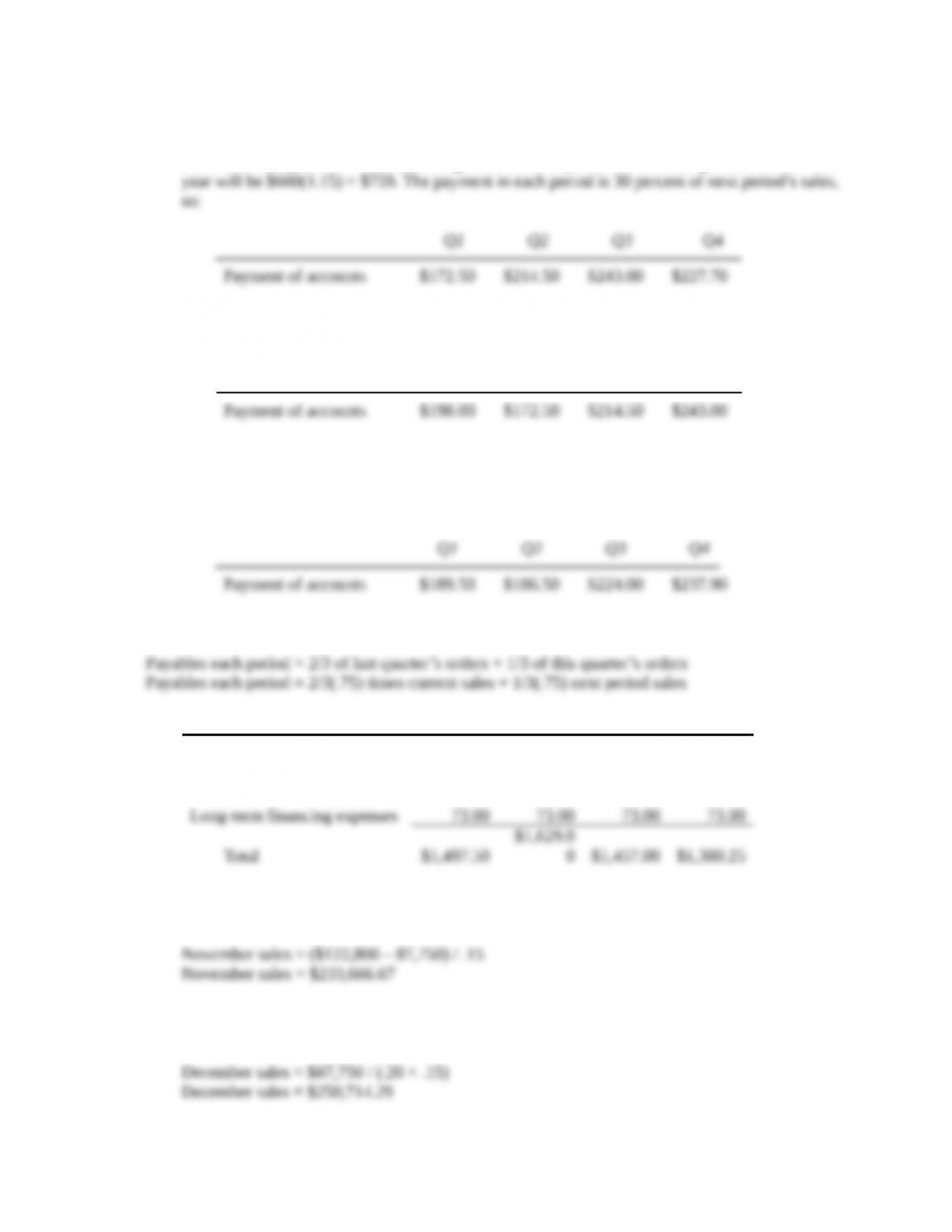

b. Since the payables period is 90 days, the payment in each period is 30 percent of the current

period sales, so:

Q1 Q2 Q3 Q4

c. Since the payables period is 60 days, the payment in each period is 2/3 of last quarter’s orders,

plus 1/3 of this quarter’s orders, or:

Quarterly payments = 2/3(.30) times current sales + 1/3(.30) next period sales

8. Since the payables period is 60 days, the payables in each period will be:

Q1 Q2 Q3 Q4

Payment of accounts $1,137.50

$1,220.0

0 $1,080.00 $1,051.25

Wages, taxes, other expenses 287.00 336.00 304.00 256.00

9. a. The November sales must have been the total uncollected sales minus the uncollected sales

from December, divided by the collection rate two months after the sale, so:

b. The December sales are the uncollected sales from December divided by the collection rate of

the previous months’ sales, so:

6

CHAPTER 26 –

c. The collections each month for this company are:

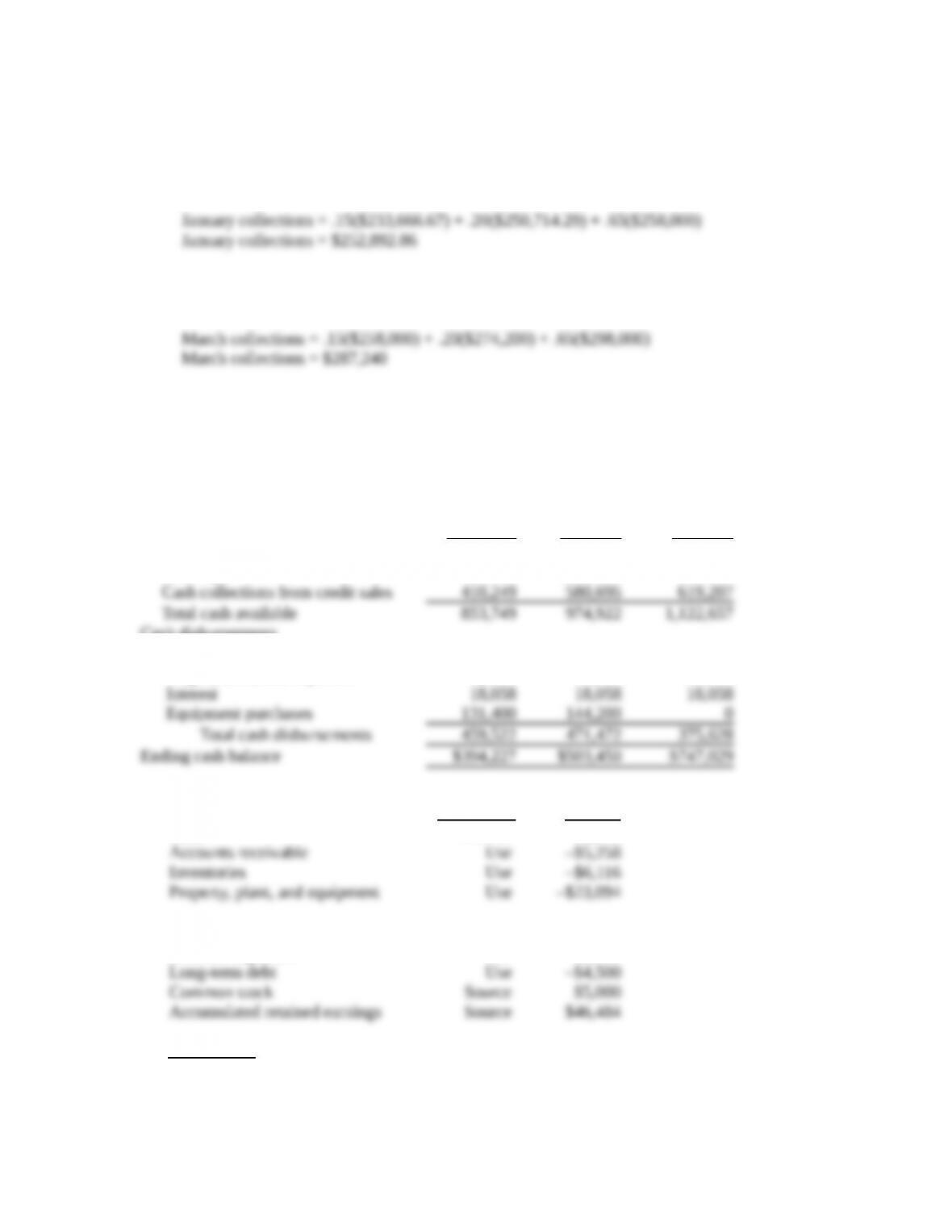

Collections = .15(Sales from 2 months ago) + .20(Last month’s sales) + .65(Current sales)

February collections = .15($250,714.29) + .20($258,000) + .65($274,200)

February collections = $267,437.14

10. The sales collections each month will be:

Sales collections = .35(current month sales) + .60(previous month sales)

Given this collection, the cash budget will be:

April May June

Beginning cash balance $443,500 $394,227 $503,450

Cash receipts

Cash disbursements

Purchases 247,100 232,850 277,900

Wages, taxes, and expenses 62,964 76,364 79,670

11. Item Source/Use Amount

Cash Source $2,365

Accounts payable Use –$22,126

Accrued expenses Use –$1,140

Intermediate

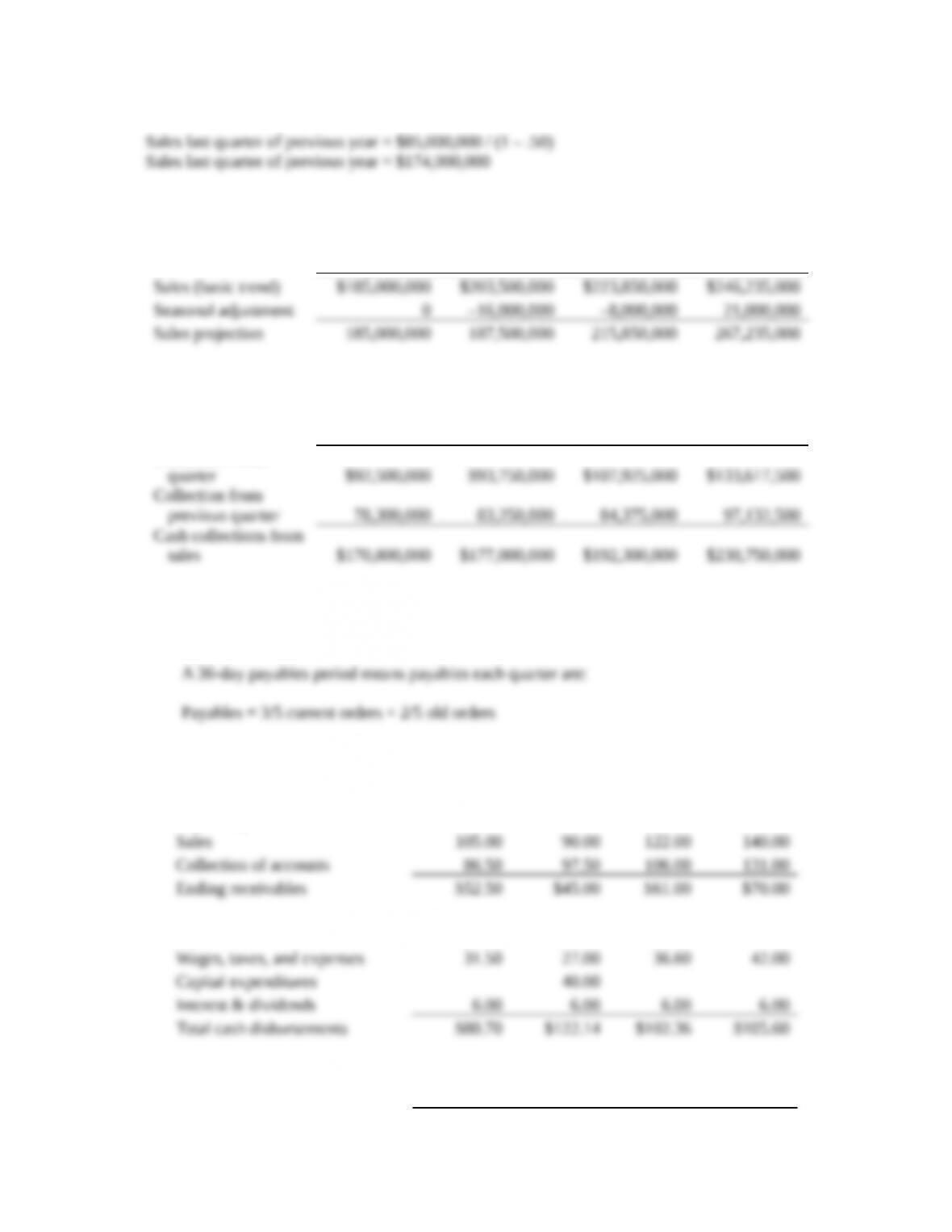

12. First, we need to calculate the sales from the last quarter of the previous year. Since 50 percent of the

sales were collected in that quarter, the sales figure must have been:

7

CHAPTER 26 –

Now we can estimate the sales growth each quarter, and calculate the net sales including the seasonal

adjustments. The sales figures for each quarter will be:

Quarter 1 Quarter 2 Quarter 4 Quarter 4

Since 50 percent of sales are collected in the quarter the sales are made, and 45 percent of sales are

collected in the quarter after the sales are made, the cash budget is:

Quarter 1 Quarter 2 Quarter 4 Quarter 4

Collected within

13. a. A 45-day collection period means sales collections each quarter are:

Collections = 1/2 current sales + 1/2 old sales

So, the cash inflows and disbursements each quarter are:

Q1 Q2 Q3 Q4

Beginning receivables $34.00 $52.50 $45.00 $61.00

Payment of accounts $43.20 $49.14 $59.76 $57.60

Total cash collections $86.50 $97.50 $106.00 $131.00

Total cash disbursements 80.70 122.14 102.36 105.60

8

CHAPTER 26 –

The company’s cash budget will be:

WILDCAT, INC.

Cash Budget

(in millions)

Q1 Q2 Q3 Q4

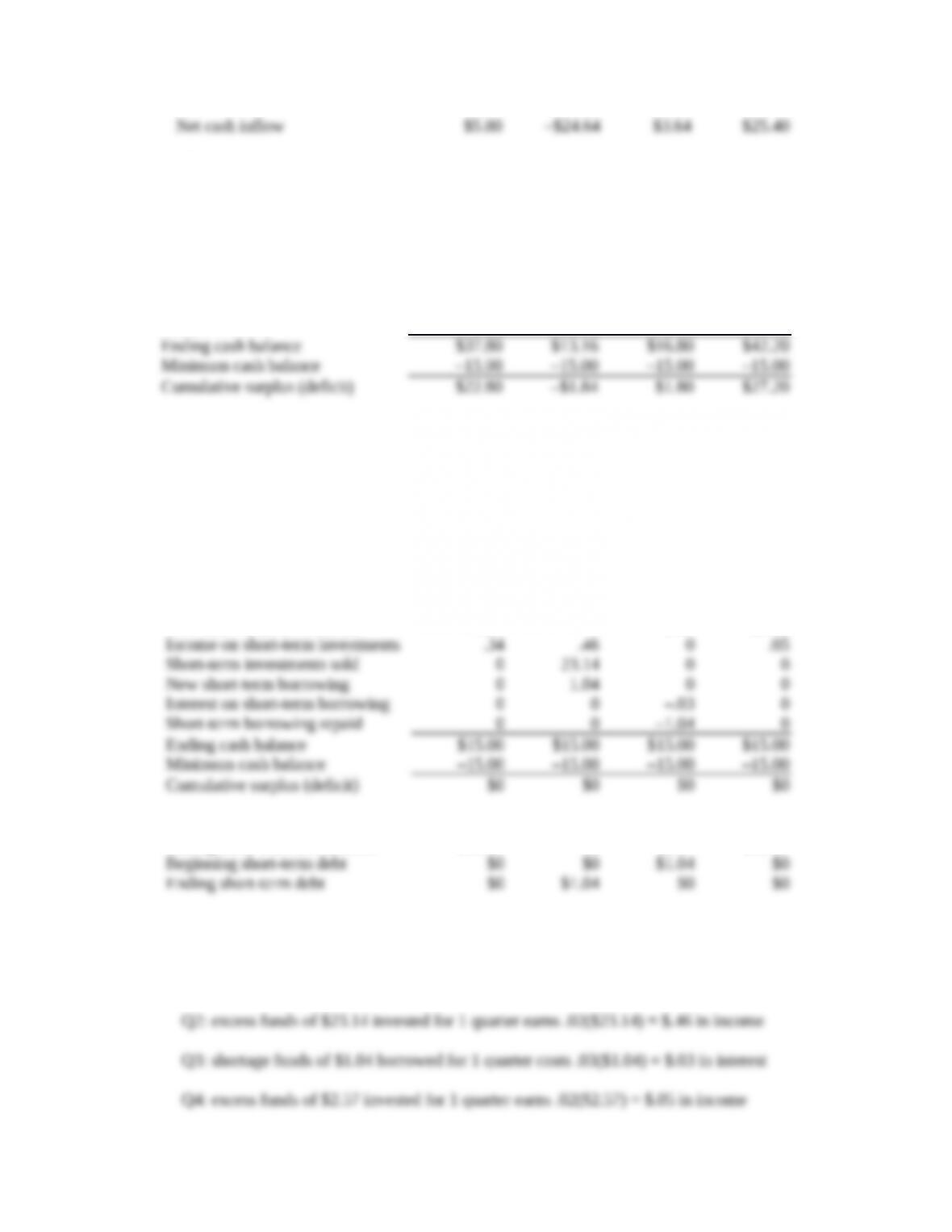

Beginning cash balance $32.00 $37.80 $13.16 $16.80

Net cash inflow 5.80 –24.64 3.64 25.40

With a $15 million minimum cash balance, the short-term financial plan will be:

WILDCAT, INC.

Short-Term Financial Plan

(in millions)

b. Q1 Q2 Q3 Q4

Beginning cash balance $15.00 $15.00 $15.00 $15.00

Net cash inflow 5.80 –24.64 3.64 25.40

New short-term investments –6.14 0 –2.57 –25.45

Beginning short-term investments $17.00 $23.14 $0 $2.57

Ending short-term investments $23.14 $0 $2.57 $28.07

Below you will find the interest paid (or received) for each quarter:

Q1: excess funds at start of quarter of $17 invested for 1 quarter earns .02($17) = $.34 income

9

CHAPTER 26 –

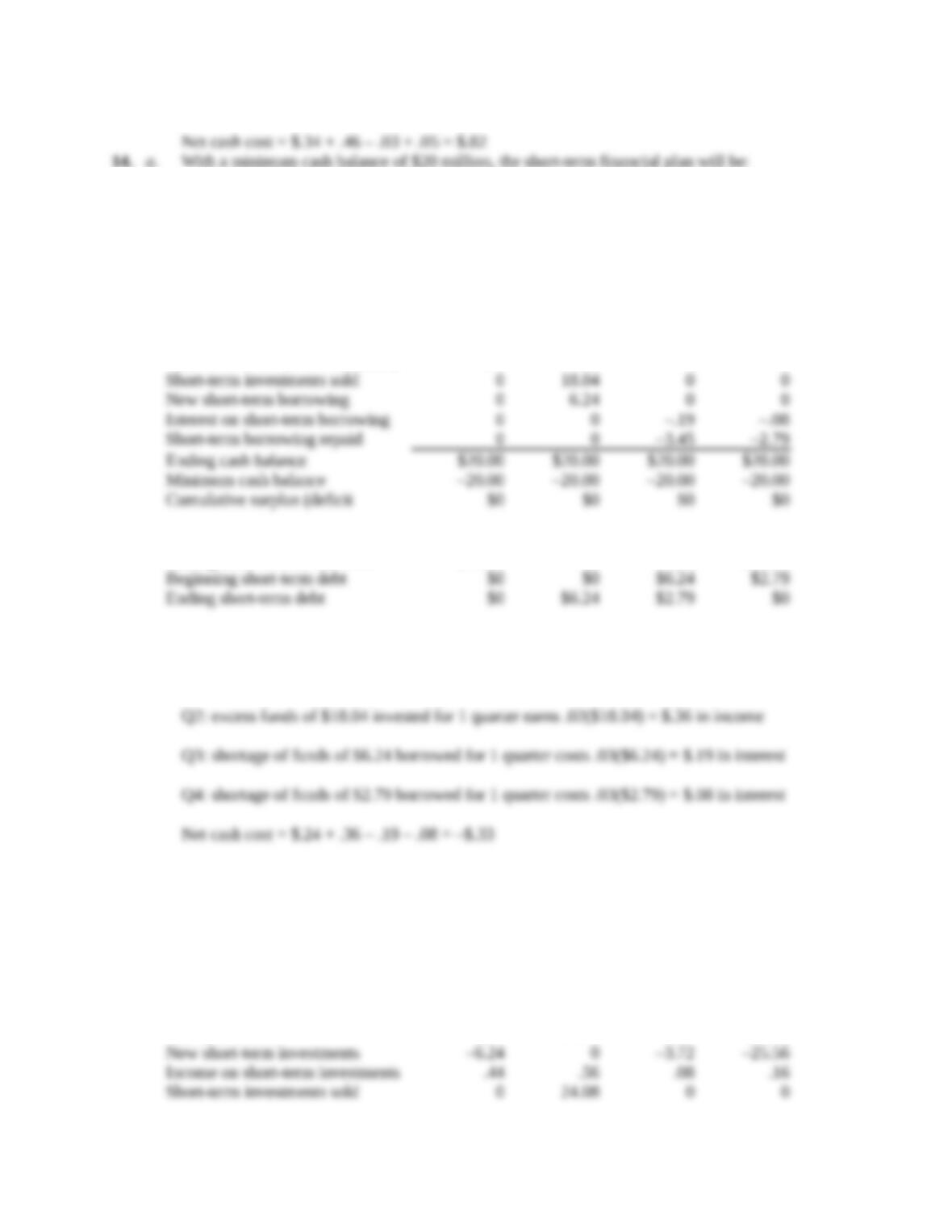

14. a. With a minimum cash balance of $20 million, the short-term financial plan will be:

WILDCAT, INC.

Short-Term Financial Plan

(in millions)

Q1 Q2 Q3 Q4

Beginning cash balance $20.00 $20.00 $20.00 $20.00

Net cash inflow 5.80 –24.64 3.64 25.40

New short-term investments –6.04 0 0 –22.53

Income on short-term investments .24 .36 0 0

Beginning short-term investments $12.00 $18.04 $0 $0

Ending short-term investments $18.04 $0 $0 $22.53

Below you will find the interest paid (or received) for each quarter:

Q1: excess funds at start of quarter of $12 invested for 1 quarter earns .02($12) = $.24 income

b. And with a minimum cash balance of $10 million, the short-term financial plan will be:

WILDCAT, INC.

Short-Term Financial Plan

(in millions

Q1 Q2 Q3 Q4

Beginning cash balance $10.00 $10.00 $10.00 $10.00

Net cash inflow 5.80 –24.64 3.64 25.40

10

CHAPTER 26 –

New short-term borrowing 0 0 0 0

Interest on short-term borrowing 0 0 0 0

Short-term borrowing repaid 0 0 0 0

Beginning short-term investments $22.00 $28.24 $4.16 $7.89

Ending short-term investments $28.24 $4.16 $7.89 $33.60

Below you will find the interest paid (or received) for each quarter:

Q1: excess funds at start of quarter of $22 invested for 1 quarter earns .02($22) = $.44 income

Q2: excess funds of $28.24 invested for 1 quarter earns .02($28.24) = $.56 in income

Since cash has an opportunity cost, the firm can boost its profit if it keeps its minimum cash balance

15. a. The current assets of Cleveland Compressor are financed largely by retained earnings. From

2015 to 2016, total current assets grew by $7,212. Only $2,126 of this increase was financed by

b. Cleveland Compressor holds the larger investment in current assets. It has current assets of

c. Cleveland Compressor is more likely to incur shortage costs because the ratio of current assets

11