CHAPTER 25 –

7. The duration of a bond is the average time to payment of the bond’s cash flows, weighted by the

ratio of the present value of each payment to the price of the bond. Since the bond is selling at par,

the market interest rate must equal 8.6 percent, the annual coupon rate on the bond. The price of a

bond selling at par is equal to its face value. Therefore, the price of this bond is $1,000. The relative

Year PV of payment Relative value Payment weight

1 $79.19 .07919 .07919

2 72.92 .07292 .14584

8. The duration of a portfolio of assets or liabilities is the weighted average of the duration of the

a. The total market value of assets in millions is:

So, the market value weight of each asset is:

Federal funds deposits = $31/$1,424 = .022

Accounts receivable = $540/$1,424 = .379

Since the duration of a group of assets is the weighted average of the durations of each

individual asset in the group, the duration of assets is:

b. The total market value of liabilities in millions is:

Note that equity is not included in this calculation since it is not a liability. So, the market value

weight of each asset is:

1

CHAPTER 25 –

Since the duration of a group of liabilities is the weighted average of the durations of each

individual asset in the group, the duration of liabilities is:

c. Since the duration of its assets does not equal the duration of its liabilities, the bank is not

Intermediate

9. a. You’re concerned about a rise in corn prices, so you would buy March contracts. Since each

contract is for 5,000 bushels, the number of contracts you would need to buy is:

By doing so, you’re effectively locking in the settle price in March 2015 of $3.9625 per bushel

of corn, or:

b. If the price of corn at expiration is $4.09 per bushel, the value of your futures position is:

While the price of the corn your firm needs has become $17,850 more expensive since January,

your profit from the futures position has netted out this higher cost.

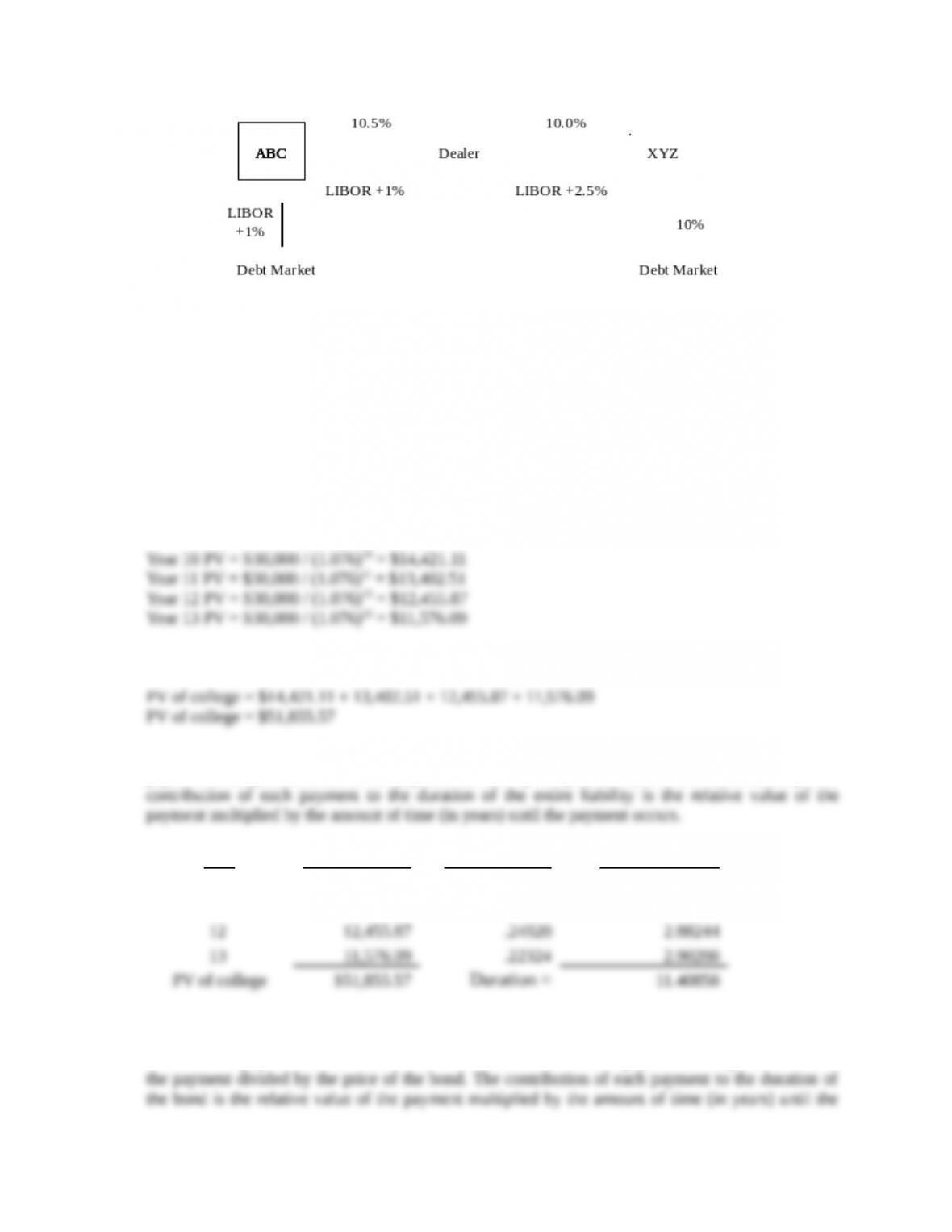

10. a. XYZ has a comparative advantage relative to ABC in borrowing at fixed interest rates, while

ABC has a comparative advantage relative to XYZ in borrowing at floating interest rates. Since

b. If the swap dealer must capture 2% of the available gain, there is 1% left for ABC and XYZ.

Any division of that gain is feasible; in an actual swap deal, the divisions would probably be

negotiated by the dealer. One possible combination is ½% for ABC and ½% for XYZ:

2

CHAPTER 25 –

11. The duration of a liability is the average time to payment of the cash flows required to retire the

liability, weighted by the ratio of the present value of each payment to the present value of all

payments related to the liability. In order to determine the duration of a liability, first calculate the

present value of all the payments required to retire it. Since the cost is $30,000 at the beginning of

each year for four years, we can find the present value of each payment using the PV equation:

PV = FV / (1 + R)t

So, the PV each year of college is:

So, the total PV of the college cost is:

Now, we can set up the following table to calculate the liability’s duration. The relative value of each

payment is the present value of the payment divided by the present value of the entire liability. The

Year PV of payment Relative value Payment weight

10 $14,421.11 .27810 2.78101

11 13,402.51 .25846 2.84304

12. The duration of a bond is the average time to payment of the bond’s cash flows, weighted by the

ratio of the present value of each payment to the price of the bond. We need to find the present value

of the bond’s payments at the market rate. The relative value of each payment is the present value of

3

CHAPTER 25 –

Year PV of payment Relative value Payment weight

.5 $31.23 .03038 .01519

1.0 30.49 .02965 .02965

13. Let R equal the interest rate change between the initiation of the contract and the delivery of the asset.

Cash flows from Strategy 1:

Today 1 Year

Cash flows from Strategy 2:

Today 1 Year

Purchase silver 0 –F

The forward price (F) of a contract on an asset with no carrying costs or convenience value equals

14. a. The forward price of an asset with no carrying costs or convenience value is:

Since you will receive the bond’s face value of $1,000 in 11 years and the 11 year spot interest

rate is currently 7 percent, the current price of the bond is:

Since the forward contract defers delivery of the bond for one year, the appropriate interest rate

to use in the forward pricing equation is the one-year spot interest rate of 5 percent:

4

CHAPTER 25 –

b. If both the 1-year and 11-year spot interest rates unexpectedly shift downward by 2 percent, the

appropriate interest rate to use when pricing the bond is 5 percent, and the appropriate interest

rate to use in the forward pricing equation is 3 percent. Given these changes, the new price of

the bond will be:

15. a. The forward price of an asset with no carrying costs or convenience value is:

Forward price = S0(1 + R)

Since you will receive the bond’s face value of $1,000 in 18 months, we can find the price of

the bond today, which will be:

b. It is important to remember that 100 basis points equals 1 percent and one basis point equals .

01%. Therefore, if all rates increase by 30 basis points, each rate increases by .003. So, the new

price of the bond today will be:

Challenge

16. The financial engineer can replicate the payoffs of owning a put option by selling a forward contract

and buying a call. For example, suppose the forward contract has a settle price of $50 and the

5

CHAPTER 25 –

Price of coal: $40 $45 $50 $55 $60

Value of call option position: 0 0 0 5 10

The payoffs for the combined position are exactly the same as those of owning a put. This means

that, in general, the relationship between puts, calls, and forwards must be such that the cost of the

6