CHAPTER 7 –

23. a. The NPV of the project is the sum of the present value of the cash flows generated by the

project. The cash flows from this project are an annuity, so the NPV is:

b. The company should abandon the project if the PV of the revised cash flows for the next nine

years is less than the project’s aftertax salvage value. Since the option to abandon the project

occurs in Year 1, discount the revised cash flows to Year 1 as well. To determine the level of

expected cash flows below which the company should abandon the project, calculate the

equivalent annual cash flows the project must earn to equal the aftertax salvage value. We will

24. a. The NPV of the project is sum of the present value of the cash flows generated by the project.

The annual cash flow for the project is the number of units sold times the cash flow per unit,

which is:

b. The company will abandon the project if unit sales are not revised upward. If the unit sales are

revised upward, the aftertax cash flows for the project over the last four years will be:

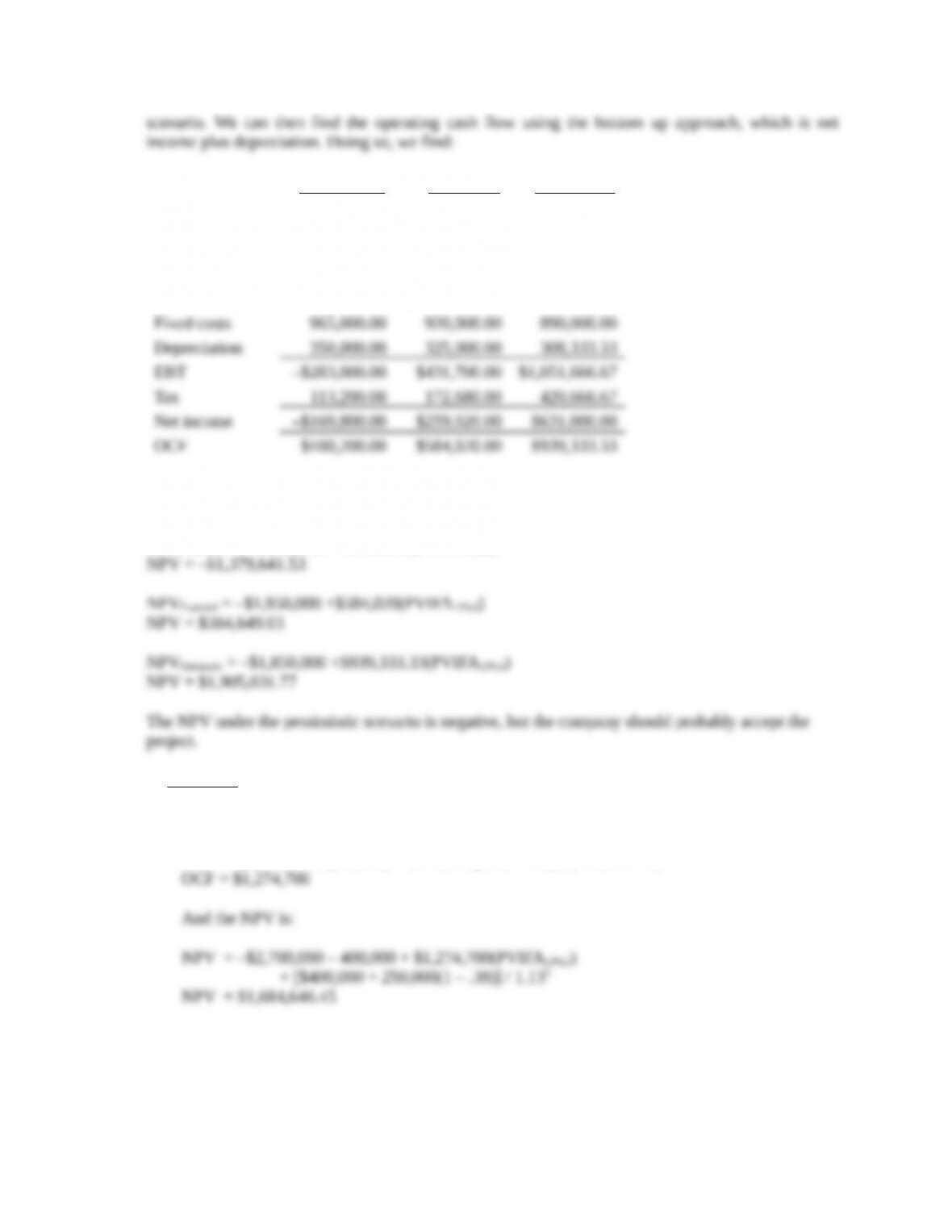

25. To calculate the unit sales for each scenario, we multiply the market sales times the company’s

market share. We can then use the quantity sold to find the revenue each year, and the variable costs

each year. After doing these calculations, we will construct the pro forma income statement for each

1

CHAPTER 7 –

Pessimistic Expected Optimistic

Units per year 24,000 31,050 37,500

Revenue $3,528,000.00

$4,750,650.0

0 $5,925,000.00

Variable costs 2,496,000.00 3,073,950.00 3,675,000.00

Note that under the pessimistic scenario, the taxable income is negative. We assumed a tax credit in

this case. Now we can calculate the NPV under each scenario, which will be:

NPVPessimistic = –$2,100,000 + $180,200(PVIFA13%,6)

Challenge

26. a. Using the tax shield approach, the OCF is:

OCF = [($345 – 265)(25,000) – $275,000](.62) + .38($2,700,000 / 5)

b. In the worst-case, the OCF is:

OCFworst = {[($345)(.9) – 265](25,000) – $275,000}(.62) + .38($3,105,000 / 5)

2

CHAPTER 7 –

OCFworst = $770,730

And the worst-case NPV is:

27. To calculate the sensitivity to changes in quantity sold, we will choose a quantity of 26,000. The

OCF at this level of sales is:

The sensitivity of changes in the OCF to quantity sold is:

The NPV at this level of sales is:

And the sensitivity of NPV to changes in the quantity sold is:

NPV/Q = ($1,684,646.45 – 1,859,101.12) / (25,000 – 26,000)

For a zero NPV, sales would have to decrease 9,657 units, so the minimum quantity is:

3

CHAPTER 7 –

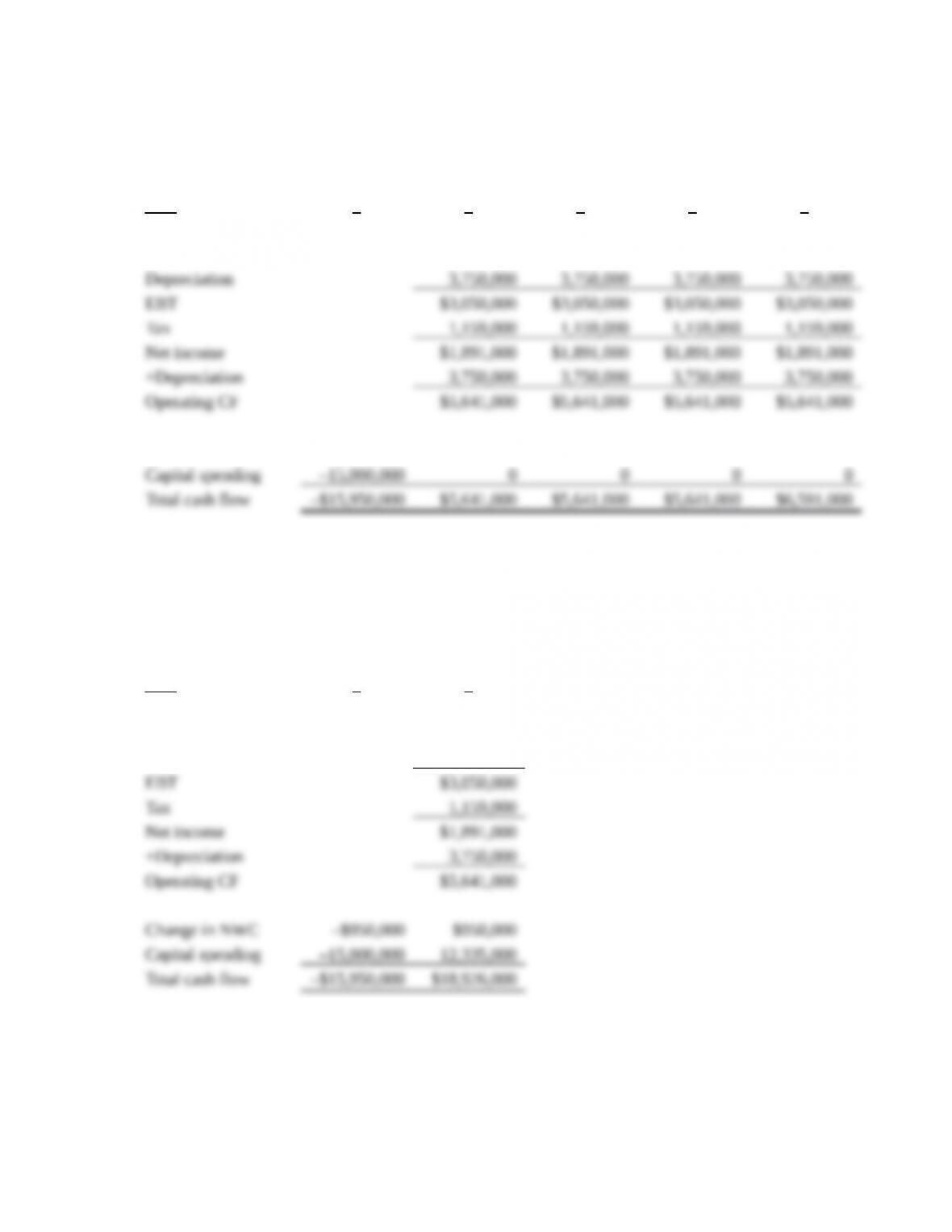

28. We will use the bottom up approach to calculate the operating cash flow. Assuming we operate the

project for all four years, the cash flows are:

Year 0 1 2 3 4

Sales $10,900,000 $10,900,000 $10,900,000 $10,900,000

Operating costs 4,100,000 4,100,000 4,100,000 4,100,000

Change in NWC –$950,000 0 0 0 $950,000

There is no salvage value for the equipment. The NPV is:

NPV = –$15,950,000 + $5,641,000(PVIFA13%,3) + $6,591,000 / 1.134

NPV = $1,411,645.54

The cash flows if we abandon the project after one year are:

Year 0 1

Sales $10,900,000

Operating costs 4,100,000

Depreciation 3,750,000

The book value of the equipment is:

Book value = $15,000,000 – (1)($15,000,000 / 4)

Book value = $11,250,000

4

CHAPTER 7 –

So the taxes on the salvage value will be:

The NPV if we abandon the project after one year is:

NPV = –$15,950,000 + $18,926,000 / 1.13

NPV = $798,672.57

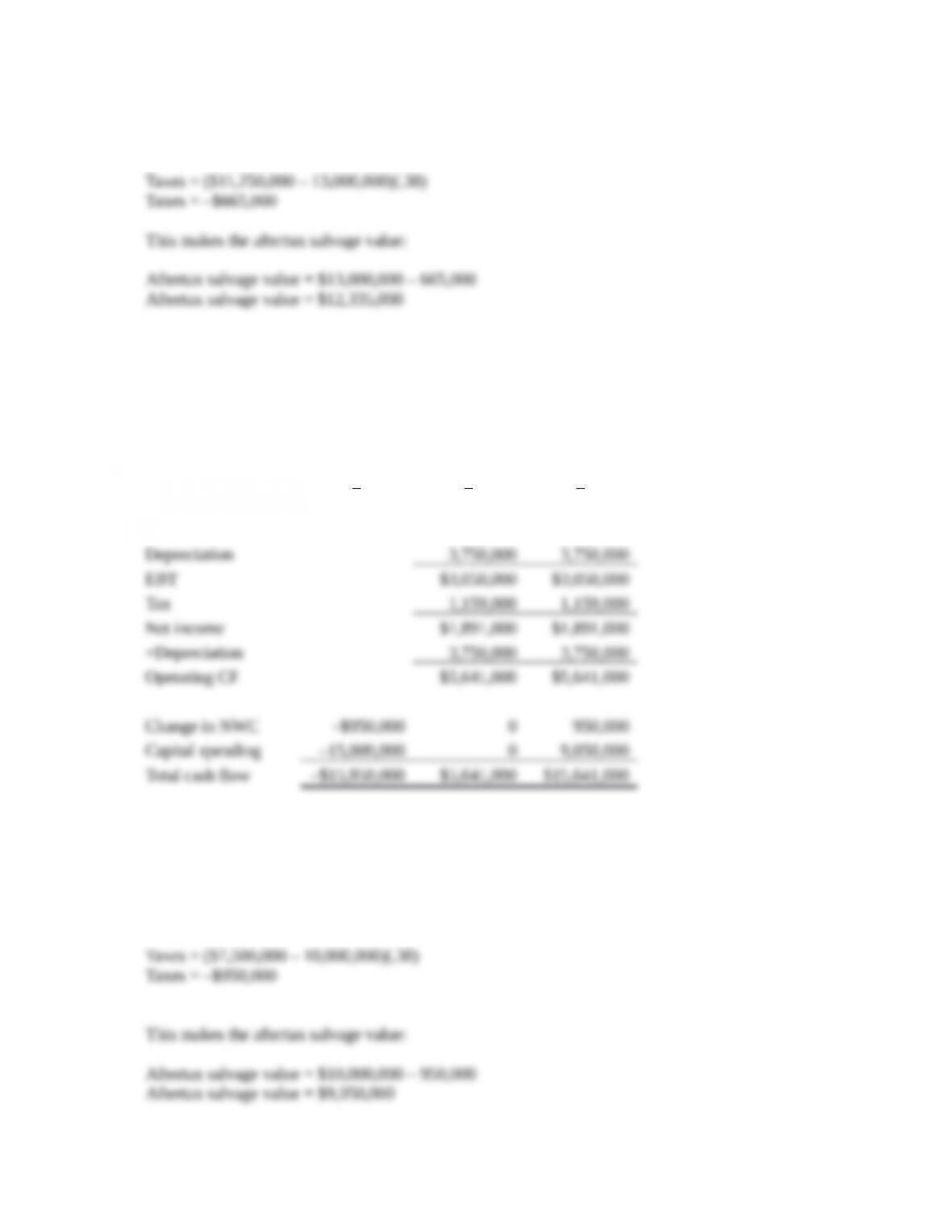

If we abandon the project after two years, the cash flows are:

Year 0 1 2

Sales $10,900,000 $10,900,000

Operating costs 4,100,000 4,100,000

The book value of the equipment is:

Book value = $15,000,000 – (2)($15,000,000 / 4)

Book value = $7,500,000

So the taxes on the salvage value will be:

5

CHAPTER 7 –

The NPV if we abandon the project after two years is:

If we abandon the project after three years, the cash flows are:

Year 0 1 2 3

Sales $10,900,000 $10,900,000 $10,900,000

Operating costs 4,100,000 4,100,000 4,100,000

Depreciation 3,750,000 3,750,000 3,750,000

EBT $3,050,000 $3,050,000 $3,050,000

The book value of the equipment is:

Book value = $15,000,000 – (3)($15,000,000 / 4)

Book value = $3,750,000

So the taxes on the salvage value will be:

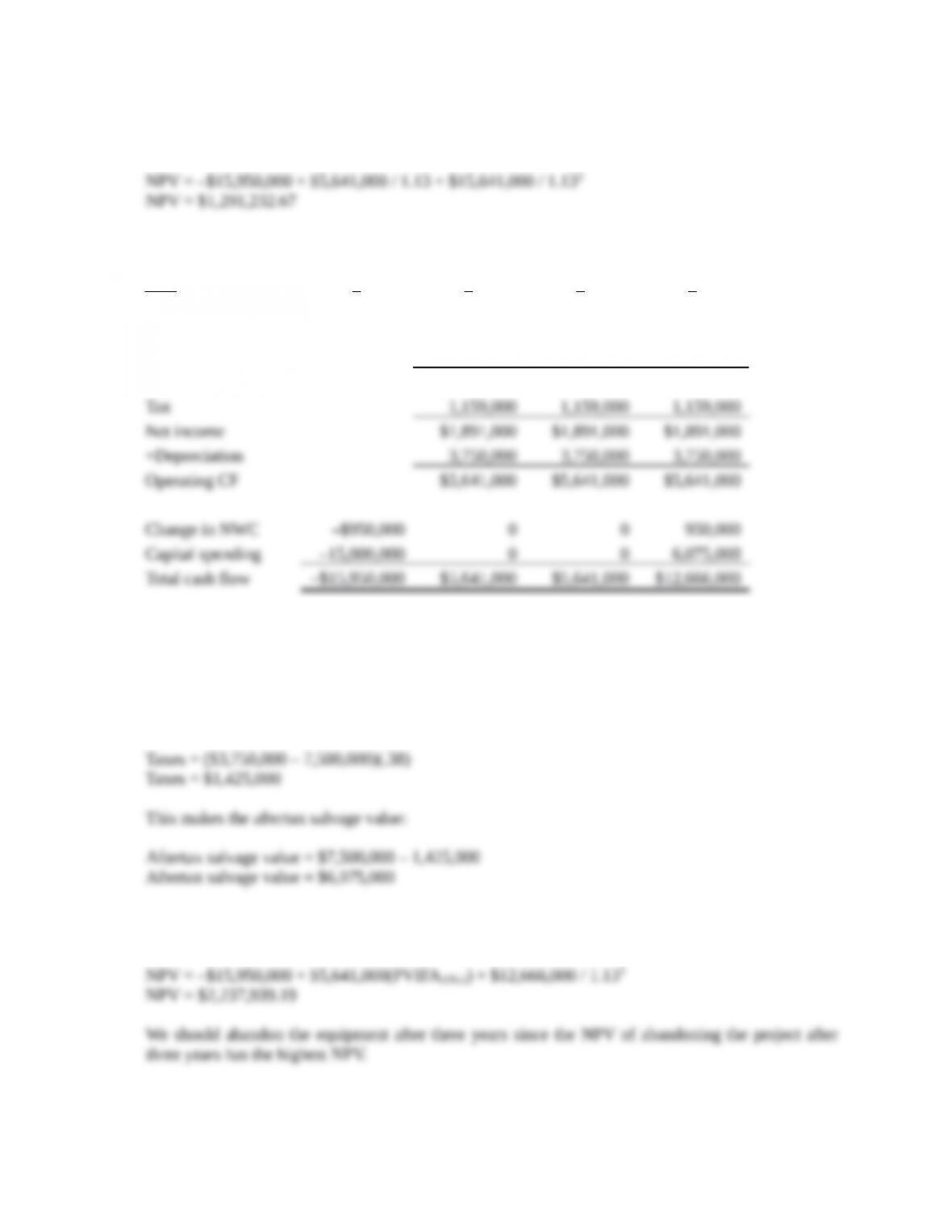

The NPV if we abandon the project after three years is:

6

CHAPTER 7 –

29. a. The NPV of the project is the sum of the present value of the cash flows generated by the

project. The cash flows from this project are an annuity, so the NPV is:

b. The company will abandon the project if the value of abandoning the project is greater than the

value of the future cash flows. The present value of the future cash flows if the company revises

its sales downward will be:

Since this is less than the abandonment value, the company should abandon the project if sales

are revised downward. So, the revised NPV of the project will be the initial cost, plus the PV of

the expected cash flow in Year 1, plus the PV of the expected cash flows based on the upward

sales projection, plus the PV of the abandonment value. We need to remember that the

30. First, determine the cash flow from selling the old harvester. When calculating the salvage value,

remember that tax liabilities or credits are generated on the difference between the resale value and

the book value of the asset. Using the original purchase price of the old harvester to determine

Since the machine is five years old, the firm has accumulated five annual depreciation charges,

reducing the book value of the machine. The current book value of the machine is equal to the initial

Since the firm is able to resell the old harvester for $21,000, which is less than the $43,333 book

value of the machine, the firm will generate a tax credit on the sale. The aftertax salvage value of the

old harvester will be:

7

CHAPTER 7 –

Next, we need to calculate the incremental depreciation. We need to calculate the depreciation tax

shield generated by the new harvester less the forgone depreciation tax shield from the old harvester.

Let P be the break-even purchase price of the new harvester. So, we find:

So, the incremental depreciation tax, which is the depreciation tax shield from the new harvester,

minus the depreciation tax shield from the old harvester, is:

The present value of the incremental depreciation tax shield will be:

The new harvester will generate year-end pre-tax cash flow savings of $12,000 per year for 10 years.

We can find the aftertax present value of the cash flows savings as:

The break-even purchase price of the new harvester is the price, P, which makes the NPV of the

machine equal to zero.

8