Chapter 9

Stock Valuation

SLIDES

CHAPTER WEB SITES

Section Web Address

9.6 www.bloomberg.com

www.nyse.com

www.nasdaq.com

finance.yahoo.com

CHAPTER ORGANIZATION

9.1 The Present Value of Common Stocks

Dividends versus Capital Gains

9.1 Key Concepts and Skills

9.2 Chapter Outline

9.3 The PV of Common Stocks

9.4 Case 1: Zero Growth

9.5 Case 2: Constant Growth

9.6 Constant Growth Example

9.7 Case 3: Differential Growth

9.8 Case 3: Differential Growth

9.9 Case 3: Differential Growth

9.10 Case 3: Differential Growth

9.11 Case 3: Differential Growth

9.12 A Differential Growth Example

9.13 With the Formula

9.14 With Cash Flows

9.15 Estimates of Parameters

9.16 Where Does R Come From?

9.17 Using the DGM to Find R

9.18 Comparables

9.19 Price-Earnings Ratio

9.20 Enterprise Value Ratios

9.21 Valuing Stocks Using Free Cash Flows

9.22 The Stock Markets

9.23 Market and Limit Orders

9.24 Stop Orders

9.25 NASDAQ

9.26 Stock Market Reporting

9.27 Quick Quiz

Valuation of Different Types of Stocks

9.2 Estimates of Parameters in the Dividend Discount Model

Where Does g Come From?

Where Does R Come From?

A Healthy Sense of Skepticism

Dividends or Earnings: Which to Discount?

The No-Dividend Firm

9.3 Comparables

Price-to-Earnings Ratio

Enterprise Value Ratios

9.4 Valuing Stocks Using Free Cash Flows

9.5 The Stock Markets

Dealers and Brokers

Organization of the NYSE

Types of Orders

NASDAQ Operations

Stock Market Reporting

ANNOTATED CHAPTER OUTLINE

Slide 9.0 Chapter 9 Title Slide

Slide 9.1 Key Concepts and Skills

Slide 9.2 Chapter Outline

1. The Present Value of Common Stocks

Slide 9.3 The PV of Common Stocks

Stock valuation is more difficult than bond valuation because the cash

flows are uncertain, the life is (potentially) forever, and the required rate

of return is unobservable.

A. Dividends versus Capital Gains

The cash flows to stockholders consist of dividends plus a future selling

price. You can illustrate that the current stock price is ultimately the

present value of all expected future dividends:

P0 = D1/(1+R) + D2/(1+R)2 + D3/(1+R)3 + …

Ethics Note: The importance of the components of the valuation model is

brought into sharp focus in a discussion of pension funding decisions.

Pension and Investments reports that in November, 1993 the Securities

and Exchange Commission issued a “new, unprecedented warning …to

use only ‘high-grade’ market rates for discounting” for valuing pension

assets. The article reports that many over-funded plans could “slip into

underfunded status.” A practical result of the use of inappropriate return

estimates is found in the case of Witco Chemical, which took large charges

against earnings in 1993 related to its use of an inappropriate rate for

computing its unfunded pension liability. Students might first be asked to

guess how one determines an “appropriate” return estimate for pension

funding purposes. Then,

ask them to whom the actuary owes greater responsibility – future pension

recipients, management, shareholders or the Pension Benefit Guaranty

Corporation? It is easy to see that the ethical issues underlying the

actuarial calculations can become quite complex.

Lecture Tip: Lively discussions can be generated in the area of stock

valuation and dividend cash flows. A stock that currently pays no

dividends may or may not have value; a stock that will NEVER pay a

dividend cannot have any value as long as investors are rational. For a

stock that currently pays no dividend, market value derives from (a) the

hope of future dividends and/or (b) the expectation of a liquidating

dividend. In the latter case, “never pays a dividend” really means “never

pays out cash in any form” to shareholders. Students will often argue

strenuously that a firm never has to pay a dividend because investors can

just rely on the increase in price. It’s important to emphasize that the price

won’t continue to increase forever. The company will eventually run out of

productive ways to use its cash. When this happens, it will need to begin

paying dividends. Another way to think of this is that a company that

never pays a dividend, including a liquidating dividend, is essentially a

perpetual zero-coupon bond. It is a big, black hole where you put money

in, but you never get anything back out.

B. Valuation of Different Types of Stocks

Slide 9.4 Case 1: Zero Growth

Zero growth implies that D0 = D1 = D2 … = D

Since the cash flow is always the same, the PV is a perpetuity:

P0 = D / R

Example: Suppose a stock is expected to pay a $2 dividend each period,

forever, and the required return is 10%. What is the stock worth?

P0 = 2 / .1 = $20

Slide 9.5 Case 2: Constant Growth

Slide 9.6 Constant Growth Example

Constant growth: Dividends are expected to grow at a constant percentage

rate each period.

D1 = D0(1+g)

D2 = D1(1+g)

in general, Dt = D0(1+g)t

Note that this is really just a future value.

Example: If the current dividend is $2 and the expected growth rate is 5%,

what is D1? D5?

D1 = $2(1+.05) = $2.10

D5 = $2(1+.05)5 = $2.55

An amount that grows at a constant rate forever is called a growing

perpetuity. The present value of all expected future dividends under this

scenario can be expressed as follows:

P0 = D1 / (R – g)

and more generally,

Pt = Dt+1 / (R – g)

Example: Consider the stock given above. If the required return is 10%,

what is the expected price today? In 4 years?

P0 = $2.10 / (.1 – .05) = $42

P4 = $2.55 / (.1 – .05) = $51

Lecture Tip: In his book, A Random Walk Down Wall Street, pp. 82 – 89,

(1985, W.W. Norton & Company, New York), Burton Malkiel gives four

“fundamental” rules of stock prices. Loosely paraphrased, the rules are

as follows. Other things equal:

–Investors pay a higher price, the larger the dividend growth rate

–Investors pay a higher price, the larger the proportion of earnings paid

out as dividends

–Investors pay a higher price, the less risky the company’s stock

–Investors pay a higher price, the lower the level of interest rates

If the required return, R, is viewed as a riskless rate of interest, Rf, plus a

risk premium, RP, (R = Rf + RP), it is easily shown that Malkiel’s rules

have counterparts in the dividend growth model.

Of course, the tricky part is estimating the growth rate and required

return. So, while the model is precise, its predictions may be substantially

different from observed stock prices depending on the values used.

Lecture Tip: If your students have had some calculus, you might find it

useful to derive the dividend growth model.

P0=D0(1+g)

(1+R)+D0(1+g)2

(1+R)2+D0(1+g)3

(1+R)3+. ..+D0(1+g)t

(1+R)t

Now multiply both sides by (1+R)/(1+g):

(1+R)

(1+g)P0=D0

[

1+(1+g)

(1+R)+(1+g)2

(1+R)2+...+(1+g)t−1

(1+R)t−1

]

Subtract the first equation from the second and you get:

[

(1+R)−(1+g)

(1+g)

]

P0=D0

[

1−(1+g)t

(1+R)t

]

The term 1 – (1+g)t/(1+R)t goes to one as t approaches infinity, assuming

R > g. If we solve for P0, we get the dividend growth model.

Lecture Tip: Students often ask:

1. “How can g ever be assumed to be constant?” The answer lies in the

competitive equilibrium model of classical macroeconomics. Since g

represents not only the growth rate in dividends but also in earnings

and sales, assuming no change in the firm’s cost structure, we are

simply assuming that the product market the firm operates in “settles

down” to a steady state in which competing firms earn sufficient

returns to remain in business, but not large enough to attract outside

capital. From a more practical standpoint, firms will often attempt to

manage their dividend policy so that there is a reasonably constant

growth in dividends.

2. “Why do we assume that R > g?” At least two answers are possible.

First, R may be less than g in the short-run. The supernormal growth

problem is an example of this situation. Second, in equilibrium, high

returns on investment will attract capital, which, in the absence of

technological change, will ensure that in succeeding periods, higher

returns cannot be earned without taking greater risk. But, taking

greater risk will increase R, so g cannot be increased without raising

R.

Slide 9.7 –

Slide 9.11 Case 3: Differential Growth

Assume that dividends will grow at different rates in the foreseeable future

and then will grow at a constant rate thereafter. This general type of model

is especially useful for valuing firms in the growth stage of their life cycle.

To value a Differential Growth Stock, we need to:

1. Estimate future dividends in the foreseeable future.

2. Estimate the future stock price when the stock becomes a Constant

Growth stock (case 2).

3. Compute the total present value of the estimated future dividends

and future stock price at the appropriate discount rate.

This can be accomplished by:

A) Using the formula

B) Or by finding the cash flows.

Slide 9.12 A Differential Growth Example

Slide 9.13 With the Formula

Slide 9.14 With Cash Flows

An example:

A common stock pays a current dividend of $2. The dividend is expected

to grow at an 8% annual rate for the next three years; then it will grow at

4% in perpetuity. The appropriate discount rate is 12%. What is the price

of this stock today?

R = 12% (required return)

g1 = g2 = g3 = 8%

P=C

R−g1

[

1−(1+g1)T

(1+R)T

]

+

(

DivN+1

R−g2

)

(1+R)N

D0 = $2

D1 = $2 × 1.08 = $2.16, D2 = $2.33, D3 = $2.52

g4 = gn = 4%

Constant growth rate applies to D4 –> use Case 2 (constant growth) to

compute P3

D4 = $2.52 × 1.04 = $2.62

P3 = $2.62 / (.12 – .04) = $32.75

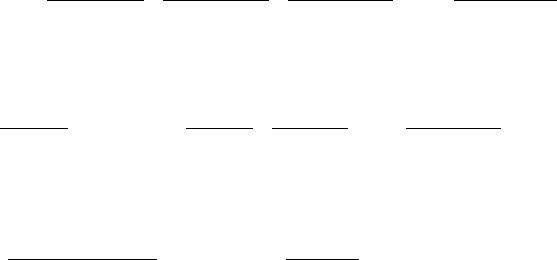

Expected future cash flows of this stock:

0 1 2 3

| | | | (r = 12%)

||||

D1D2D3 + P3

$2.16 $2.33 $2.52 + $32.75

P0 = $2.16/1.12 + $2.33/1.122 + $35.27/1.123 = $28.89

We should note that to this point we have assumed that dividends are the

sole cash payout of the firm to its shareholders. However, in recent times

more firms have undertaken share repurchases, which can essentially be

thought of as a substitute for dividends and should, therefore, also be

included in the dividend valuation model.

2. Estimates of Parameters in the Dividend Discount Model

Slide 9.15 Estimates of Parameters

In addition to the current dividend, the growth rate and the required return

impact the stock price.

A. Where Does g Come From?

g can be found using a form of the sustainable growth rate:

g = (retention ratio) x (return on retained earnings)

B. Where Does R Come From?