CHAPTER 11 CASE C-1

CHAPTER 11

A JOB AT EAST COAST YACHTS,

PART 2

1. There should be little, if any, money allocated to the company stock. The principle of diversification

indicates that an individual should hold a diversified portfolio. Investing heavily in company stock

does not create a diversified portfolio. This is especially true since income also comes from the

2. This is not the portfolio with the least risk. By adding stocks, a riskier asset, the overall risk of the

3. We can use the equations for the expected return of the portfolio, and the portfolio standard

deviation, that is:

E(RP) = XEE(RE) + XDE(RD)

2

2

2

2

Using these equations and equity portfolio weights from zero to 100 percent at intervals of 10

percent, we get the following portfolio expected returns and standard deviations:

Weight of stock fund Portfolio E(R)

Portfolio standard

deviation

0% 6.45% 9.8500%

10% 6.66% 9.5182%

20% 6.88% 9.8006%

30% 7.09% 10.6484%

The graph of the opportunity set of feasible portfolios will look like the following:

CHAPTER 11 CASE C-2

8% 10% 12% 14% 16% 18% 20% 22% 24% 26%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

Investment Opportunity Set

Portfolio Standard Deviation

Portfolio Expected Return

4. Now we can use Solver to maximize this expression by changing the weight of the equity input cell.

The constraint is that the standard deviation of the portfolio is equal to the standard deviation of the

bond fund. Using Solver, the weight of the large cap stock fund and bond fund in this portfolio is:

So, the expected return and standard deviation of this portfolio is:

This is the exact same standard deviation as the bond fund, but the expected return is about one-half

percent higher.

5. To find the weights of each asset in the minimum variance portfolio, we begin with the equation for

the variance of the portfolio. Using S to represent the large company fund and B to represent the

bond fund, the variance of a portfolio of two assets equals:

CHAPTER 11 CASE C-3

P

2

= X

S

2

S

2

+ X

B

2

B

2

+ 2XSXBS,B

Since the weights of the assets must sum to one, we can write the variance of the portfolio as:

P

2

= X

S

2

S

2

+ (1 – XS)2

B

2

+ 2XS(1 – XS)SBS,B

To find the minimum for any function, we find the derivative and set the derivative equal to zero.

Finding the derivative of the variance function, setting the derivative equal to zero, and solving for

the weight of the stock fund, we find:

2

Using this expression, we find the weight of the stock fund, must be:

XS = [.09852 – (.2382)(.0985)(.15)] / [.23822 + .09852 – 2(.2382)(.0985)(.15)]

XS = .1041

This implies the weight of the bond fund is:

The expected return of this portfolio is:

The variance of the portfolio is:

P

2

= X

S

2

S

2

+ X

B

2

B

2

+ 2XSXBSBS,B

P

2

= (.10412)(.23822) + (.89592)(.09852) + 2(.1041)(.8959)(.2382)(.0985)(.15)

P

2

= .009059

And the standard deviation is:

= .0090591/2

= .0952, or 9.52%

With these returns and variances, the minimum variance portfolio is important because no investor

would ever hold a portfolio with a greater weight in bonds. If an investor increases the weight of

S

B

2

S

2

B

2

CHAPTER 11 CASE C-4

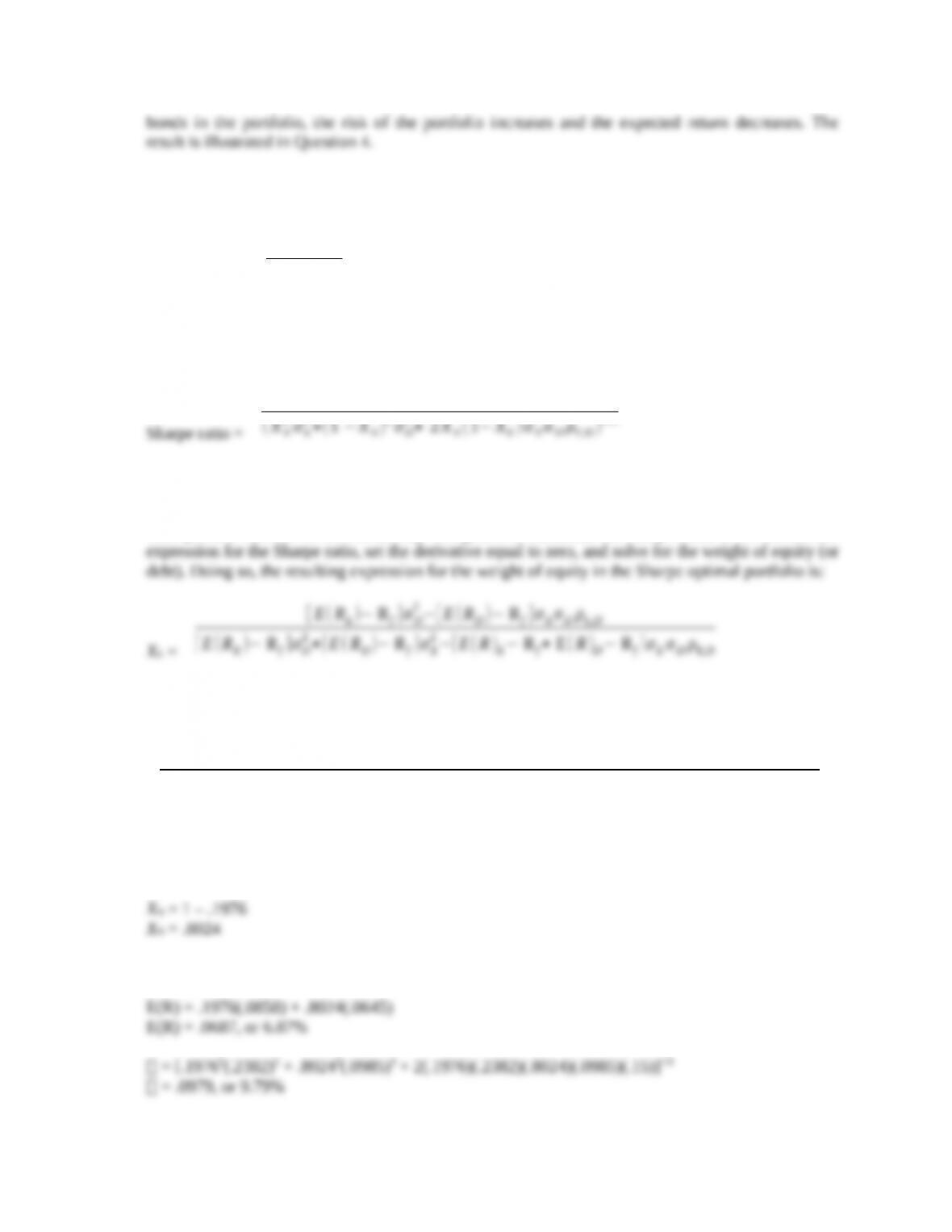

6. We can find the Sharpe optimal portfolio by using Solver. To use Solver, we input the Sharpe ratio in

a cell. The Sharpe ratio is:

Sharpe ratio =

E(R)− Rf

σP

We also need to recognize that the weight of debt in the portfolio is one minus the weight of equity.

Substituting the equations for the expected return of the portfolio and the standard deviation of the

portfolio, we get:

XEE(RE)+(1 −XE)E(RD)− Rf

(XE

2σE

2+(1 −XE)2σD

2+ 2 XE(1−XE)σEσDρE,D )1/2

CHAPTER 11 CASE C-5

The Sharpe ratio of the Sharpe optimal portfolio is:

Sharpe ratio =

. 0687 −. 0320

. 0979

Sharpe ratio = .3751

The Sharpe optimal portfolio is the best risky portfolio for all investors because it delivers a greater

reward-to-risk ratio than any other portfolio. If a line is drawn from the risk-free rate to the Sharpe