Archives

978-0077862220 Chapter 1 Solution Manual Part 1

CHAPTER 1 THE EQUITY METHOD OF ACCOUNTING FOR INVESTMENTS Chapter Outline I. Three methods are principally used to account for an investment in equity securities along with a fair value option. A. Fair value method: applied by an investor when […]

978-0077862220 Chapter 1 Solution Manual Part 2

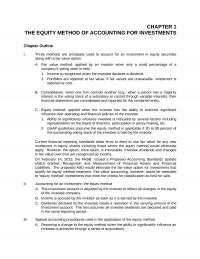

17. (10 minutes) (Equity entries for one year, includes intra-entity transfers but no unearned gross profit) Purchase price of Burks stock…………….………..………….…..….….… $210,000 Book value of Burks stock ($360,000 × 40%)……………………….….. (144 ,000) No unearned intra-entity profit exists at year’s end […]

978-0077862220 Chapter 1 Solution Manual Part 3

27. (30 minutes) (Conversion to equity method, sale of investment, and unrealized gross profit) Part a Allocation and annual amortization—first purchase Purchase price of 10 percent interest……………..………..…………. $92,000 Net book value ($800,000 × 10%)…………….…………………..………. (80 ,000) Annual Amortization…..………..…………………..………..……………………. $ 750 […]

978-0077862220 Chapter 1 Solution Manual Part 4

32. (65 Minutes) (Journal entries for several years. Includes conversion to equity method and a sale of a portion of the investment) 1/1/13 Investment in Sumter…………..……… 192,000 Cash……….……….…….…..….….….. 192,000 (To record cost of 16,000 shares of Sumter Company.) day, a […]

978-0077862220 Chapter 10 Solution Manual Part 1

CHAPTER 10 TRANSLATION OF FOREIGN CURRENCY FINANCIAL STATEMENTS Chapter Outline I. In today’s global economy, many companies have invested in operations in foreign countries. A. In preparing consolidated financial statements on a worldwide basis, the foreign currency accounts prepared by […]

978-0077862220 Chapter 10 Solution Manual Part 2

25. (15 minutes) (Determine the amounts at which foreign currency balances are reported on a foreign subsidiary’s trial balance and in the parent’s consolidated financial statements) a. Remeasurement of Swiss franc (CHF) balances into Israeli shekels (ILS) to report on […]

978-0077862220 Chapter 10 Solution Manual Part 3

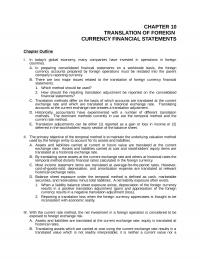

35. (continued) b. and c. The following C$ financial statements are produced by combining the figures from the main operation with the remeasured figures from the branch remeasured in C$. Income Statement c. Translation into U.S. dollars— For the Year […]

978-0077862220 Chapter 10 Solution Manual Part 4

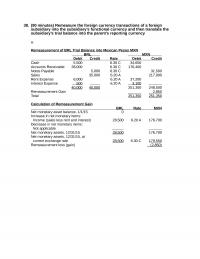

38. (90 minutes) Remeasure the foreign currency transactions of a foreign subsidiary into the subsidiary’s functional currency and then translate the subsidiary’s trial balance into the parent’s reporting currency a. Remeasurement of BRL Trial Balance into Mexican Pesos MXN BRL […]

978-0077862220 Chapter 10 Solution Manual Part 5

Excel and Analysis Case (continued) a. Translation of Suffolk’s December 31, 2015 trial balance from British pounds to U.S. dollars. Suffolk PLC Trial Balance December 31, 2015 Exchange Pounds Rate Dollars Cash £ 1,500,000$1.68 $ 2,520,000 Accounts receivable 5,200,000$1.68 8,736,000 […]

978-0077862220 Chapter 11 Solution Manual Part 1

CHAPTER 11 WORLDWIDE ACCOUNTING DIVERSITY AND INTERNATIONAL STANDARDS Chapter Outline I. Accounting and financial reporting rules differ across countries. There are a variety of factors influencing a country’s accounting system. A. Legal system—primarily relates to how accounting principles are established; […]

978-0077862220 Chapter 11 Solution Manual Part 2

Answers to Problems 1. B 2. C 13. A 14. C Problems 15-19 are based on the comprehensive illustration. 15. (15 minutes) (Carrying inventory at the lower of cost or “market”) Historical cost $120,000 Replacement cost $111,900 Net realizable value […]

978-0077862220 Chapter 12 Solution Manual Part 1

CHAPTER 12 FINANCIAL REPORTING AND THE SECURITIES AND EXCHANGE COMMISSION Chapter Outline I. In the United States, the Securities and Exchange Commission (SEC), created by Act of Congress, is responsible for ensuring that complete and reliable information concerning publicly traded […]

978-0077862220 Chapter 12 Solution Manual Part 2

Answers to Problems 1. D – A is false because intrastate offerings are typically exempt from registration; B is false because the 1934 Securities Act regulates post-issuance trading of securities; and C is false because blue sky legislation is state […]

978-0077862220 Chapter 13 Solution Manual Part 1

CHAPTER 13 ACCOUNTING FOR LEGAL REORGANIZATIONS AND LIQUIDATIONS Chapter Outline I. Because of a myriad of possible financial or business difficulties, a company may become insolvent, unable to pay its debts as they come due. A. To ensure the equitable […]

978-0077862220 Chapter 13 Solution Manual Part 2

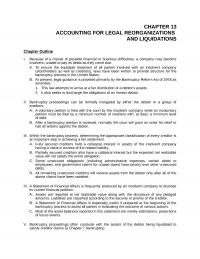

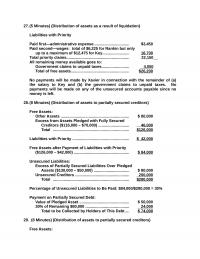

27.(5 Minutes) (Distribution of assets as a result of liquidation) Liabilities with Priority Paid first—administrative expense………………………..…. $3,450 Paid second—wages: total of $6,225 for Rankin but only up to a maximum of $12,475 for Key……………………. 18,700 No payments will be made […]

978-0077862220 Chapter 13 Solution Manual Part 3

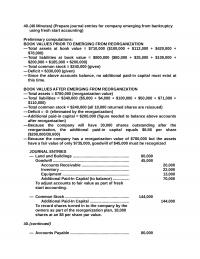

40.(40 Minutes) (Prepare journal entries for company emerging from bankruptcy using fresh start accounting) Preliminary computations: BOOK VALUES PRIOR TO EMERGING FROM REORGANIZATION — Total assets at book value = $710,000 ($100,000 + $112,000 + $420,000 + $78,000) BOOK VALUES […]

978-0077862220 Chapter 13 Solution Manual Part 4

46.(25 Minutes) (Prepare statement of realization and liquidation) a. LITZ CORPORATION Statement of Realization and Liquidation Stock- Liabilities Fully Partially Unsecured holders’ Noncash with Secured Secured Nonpriority Equity Cash Assets Priority Creditors Creditors Liabilities (Deficits) Payment is made on note […]

978-0077862220 Chapter 13 Solution Manual Part 5

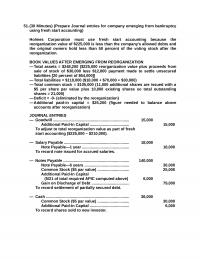

51.(30 Minutes) (Prepare Journal entries for company emerging from bankruptcy using fresh start accounting) Holmes Corporation must use fresh start accounting because the reorganization value of $225,000 is less than the company’s allowed debts and the original owners hold less […]

978-0077862220 Chapter 13 Solution Manual Part 6

(2) Reflects the adjustments to assets and liabilities to estimated fair value, or other measurements specified by FASB ASC 805, in conjunction with the adoption of fresh start accounting. Significant adjustments are summarized as follows and all are considered a […]

978-0077862220 Chapter 14 Solution Manual Part 1

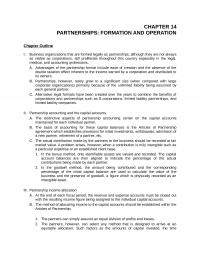

CHAPTER 14 PARTNERSHIPS: FORMATION AND OPERATION Chapter Outline I. Business organizations that are formed legally as partnerships, although they are not always as visible as corporations, still proliferate throughout this country especially in the legal, medical, and accounting professions. A. […]

978-0077862220 Chapter 14 Solution Manual Part 2

11.A ASSIGNMENT OF INCOME—YEAR ONE WINSTON DURHAM SALEM TOTAL Interest—10% of beginning capital ..…..….…. $11,000 $ 8,000 $11,000 $30,000 Salary……………..….…..….….…… 20,000 -0- 10,000 30,000 Allocation of remaining loss ($80,000 divided on a 5:2:3 basis) (40 ,000) (16 ,000) (24 ,000) […]

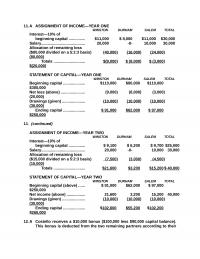

978-0077862220 Chapter 14 Solution Manual Part 3

26. (45 Minutes) (P&L allocations and admission of a new partner) a. The interest factor was probably inserted to reward Hugh for contributing $50,000 more to the partnership than Jacobs. The salary allowance gives b. The drawings show the assets […]

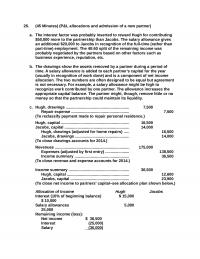

978-0077862220 Chapter 14 Solution Manual Part 4

31.(75 Minutes) (Recording of changes in the composition of a partnership including allocation of income) a. 1/1/13 Building ………….………..……….…………….….. 52,000 Equipment……….……….………..……….……….. 16,000 12/31/13 Reese, capital ………..……….……..….…..……. 22,000 O’Donnell, capital ..…………………………. 12,000 Income summary ……………………..….…. 10,000 (The allocation plan specifies that […]

978-0077862220 Chapter 15 Solution Manual Part 1

CHAPTER 15 PARTNERSHIPS: TERMINATION AND LIQUIDATION Chapter Outline I. The termination of a partnership and liquidation of its property may take place for a number of reasons. A. The death, withdrawal, or retirement of a partner can lead to cessation […]

978-0077862220 Chapter 15 Solution Manual Part 2

19.(10 minutes) (Determine amount to be contributed by partner with a deficit capital balance) White and Blue are both insolvent and have negative capital balances (after offsetting the loan from White) totaling $15,000 (White, $3,000; Blue, $12,000). Absorption by the […]

978-0077862220 Chapter 15 Solution Manual Part 3

26. (25 minutes) (Prepare journal entries for a partnership liquidation) JOURNAL ENTRIES a. Cash ………………..………..………..………..………………..…. 56,000 March, Capital (2/6 of loss) ……………………..………….. 6,000 April, Capital (3/6) …………..………..………..………….…… 9,000 May, Capital (1/6) ………..………..………….…..…..…..…… 3,000 Inventory ………..…………………..………..…………..….. 74,000 d. Cash ………………..………..………..………..………………..…. 45,000 […]

978-0077862220 Chapter 15 Solution Manual Part 4

31. (50 minutes) (Prepare a predistribution plan and journal entries for a partnership liquidation) Part A Preparation of Predistribution Plan Schedule 1 Maximum Loss Capital Balance/ That Can Be Partner Loss Allocation Absorbed Wingler $120,000/30% $400,000 Schedule 2 Maximum Loss […]

978-0077862220 Chapter 16 Solution Manual Part 1

CHAPTER 16 ACCOUNTING FOR STATE AND LOCAL GOVERNMENTS (PART ONE) Chapter Outline I. State and local government units are different than for-profit entities in a number of specific ways. A. Governments serve a broader group of stakeholders. B. Most government […]

978-0077862220 Chapter 16 Solution Manual Part 2

16. C (Under the consumption method, the inventory is recorded when acquired and then reclassified as an expenditure as consumed.) fund financial statements as in the government-wide financial statements.) 21. A 22. C (Debt issuance costs are not capitalized in […]

978-0077862220 Chapter 16 Solution Manual Part 3

40. (25 Minutes) (Answer questions about ledger account balances) a. As the Appropriations account balance in the General Fund shows a total of $171,000, that amount of money has been authorized for b. The governmental funds are all designed to […]

978-0077862220 Chapter 16 Solution Manual Part 4

Part b — FUND FINANCIAL STATEMENTS STATEMENT OF REVENUES, EXPENDITURES AND CHANGES IN FUND BALANCE For the Year Ended December 31, 2015 General Fund Revenues —Property Taxes $370,000 —Student Fees 3 ,000 Total Revenues $373,000 Expenditures Change in Fund Balance […]

978-0077862220 Chapter 16 Solution Manual Part 5

52. (12 Minutes) (The financial impact of fund transfers) A. False—A transfer out will be shown by the governmental activities and a transfer in will be reported by the business-type activities. Those two figures will be netted together so that […]

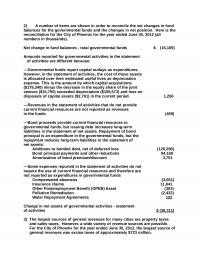

978-0077862220 Chapter 16 Solution Manual Part 6

2) A number of items are shown in order to reconcile the net changes in fund balances for the governmental funds and the changes in net position. Here is the reconciliation for the City of Phoenix for the year ended […]

978-0077862220 Chapter 17 Solution Manual Part 1

CHAPTER 17 ACCOUNTING FOR STATE AND LOCAL GOVERNMENTS (PART TWO) Chapter Outline I. This chapter looks at the reporting for a number of significant transactions that are common for state and local governments. For example, these entities often obtain property […]

978-0077862220 Chapter 17 Solution Manual Part 2

Answers to Problems 1. A (Both the asset and liability are reported at the present value of the minimum lease payments.) 6. D 7. C (The liability must be increased from 8 percent of $1 million to 19 percent. The […]

978-0077862220 Chapter 17 Solution Manual Part 3

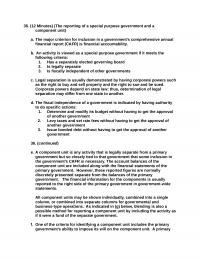

36. (12 Minutes) (The reporting of a special purpose government and a component unit) a. The major criterion for inclusion in a government’s comprehensive annual financial report (CAFR) is financial accountability. b. An activity is viewed as a special purpose […]

978-0077862220 Chapter 17 Solution Manual Part 4

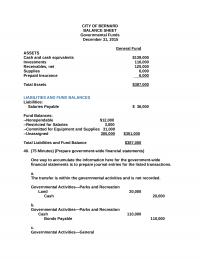

CITY OF BERNARD BALANCE SHEET Governmental Funds December 31, 2015 General Fund ASSETS Cash and cash equivalents $139,000 Investments 116,000 LIABILITIES AND FUND BALANCES Liabilities: Salaries Payable $ 36,000 Fund Balances: –Nonspendable $12,000 –Restricted for Salaries 3,000 –Committed for Equipment […]

978-0077862220 Chapter 17 Solution Manual Part 5

41. (continued) City of Pfeiffer Statement of Revenues, Expenditures, and Changes in Fund Balance Fund Financial Statements – Governmental Funds Year ending December 31, 2015 Total General Special Capital Projects Governmental Fund Revenue Funds Funds Funds Revenues -Property Taxes $560,000 […]

978-0077862220 Chapter 17 Solution Manual Part 6

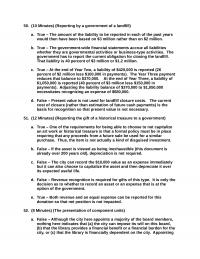

50. (10 Minutes) (Reporting by a government of a landfill) a. True – The amount of the liability to be reported in each of the past years would then have been based on $3 million rather than on $2 million. […]

978-0077862220 Chapter 18 Solution Manual Part 1

CHAPTER 18 ACCOUNTING AND REPORTING FOR PRIVATE NOT-FOR-PROFIT ENTITIES Chapter Outline I. Historically, the financial reporting for private not-for-profit entities has differed significantly according to the type of organization (such as a health care entity versus a college or university). […]

978-0077862220 Chapter 18 Solution Manual Part 2

20. B (This transaction is an acquisition and the acquired entity is not supported predominantly by contributions or investment income. Thus, the difference 23.C 24.C (The charity care work should not be recorded in any way because the entity has […]

978-0077862220 Chapter 18 Solution Manual Part 3

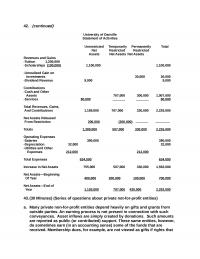

42. (continued) University of Danville Statement of Activities Unrestricted Temporarily Permanently Total Net Restricted Restricted Assets Net Assets Net Assets Revenues and Gains -Tuition 1,200,000 Contributions -Cash and Other Assets 707,000 300,000 1,007,000 -Services 80,000 80,000 Total Revenues, Gains, And […]

978-0077862220 Chapter 18 Solution Manual Part 4

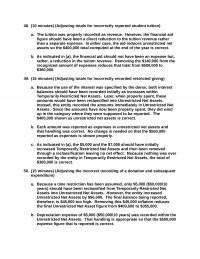

48. (10 minutes) (Adjusting totals for incorrectly reported student tuition) a. The tuition was properly recorded as revenue. However, the financial aid figure should have been a direct reduction to the tuition revenue rather 49. (15 minutes) (Adjusting totals for […]

978-0077862220 Chapter 19 Solution Manual Part 1

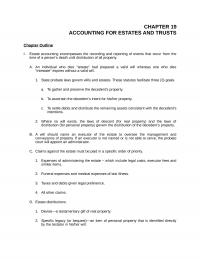

CHAPTER 19 ACCOUNTING FOR ESTATES AND TRUSTS Chapter Outline I. Estate accounting encompasses the recording and reporting of events that occur from the time of a person’s death until distribution of all property. A. An individual who dies “testate” had […]

978-0077862220 Chapter 19 Solution Manual Part 2

30.(30 Minutes) (Define terms used in estate accounting) a. Will—the instructions, prepared consistent with the applicable state laws, given by an individual to direct the distribution to be made of the person’s property after death. result of the specifications of […]

978-0077862220 Chapter 19 Solution Manual Part 3

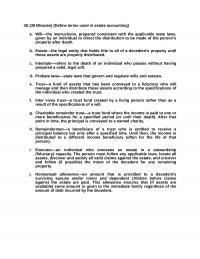

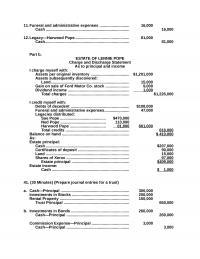

Cash……………..………..………..………..………..………….…. 81,000 Part b. ESTATE OF LENNIE POPE Charge and Discharge Statement As to principal and income I charge myself with: Assets per original inventory ……………………………… $1,201,000 Assets subsequently discovered: Land…………..………..………..………..………..…………… 15,000 Gain on sale of Ford Motor Co. stock […]

978-0077862220 Chapter 2 Solution Manual Part 1

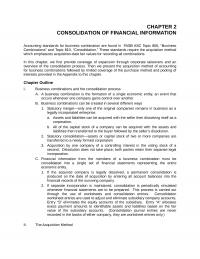

CHAPTER 2 CONSOLIDATION OF FINANCIAL INFORMATION Accounting standards for business combination are found in FASB ASC Topic 805, “Business Combinations” and Topic 810, “Consolidation.” These standards require the acquisition method which emphasizes acquisition-date fair values for recording all combinations. In […]

978-0077862220 Chapter 2 Solution Manual Part 2

24. (20 Minutes) (Determine selected consolidated balances) Under the acquisition method, the shares issued by Wisconsin are recorded at fair value using the following journal entry: Investment in Badger (value of debt and shares issued). 900,000 Common Stock (par value)……………………..…………….… […]

978-0077862220 Chapter 2 Solution Manual Part 3

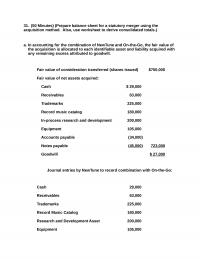

31. (50 Minutes) (Prepare balance sheet for a statutory merger using the acquisition method. Also, use worksheet to derive consolidated totals.) a. In accounting for the combination of NewTune and On-the-Go, the fair value of the acquisition is allocated to […]

978-0077862220 Chapter 3 Solution Manual Part 1

CHAPTER 3 CONSOLIDATIONS—SUBSEQUENT TO THE DATE OF ACQUISITION I. Several factors serve to complicate the consolidation process when it occurs subsequent to the date of acquisition. In all combinations within its own internal records the acquiring company will utilize a […]

978-0077862220 Chapter 3 Solution Manual Part 2

17. (20 minutes) (Record a merger combination with subsequent testing for goodwill impairment). a. In accounting for the combination, the total fair value of Beltran (consideration transferred) is allocated to each identifiable asset acquired and liability assumed with any remaining […]

978-0077862220 Chapter 3 Solution Manual Part 3

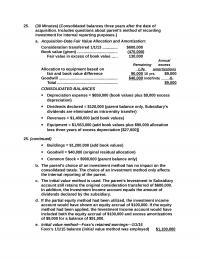

25. (30 Minutes) (Consolidated balances three years after the date of acquisition. Includes questions about parent’s method of recording investment for internal reporting purposes.) a. Acquisition-Date Fair Value Allocation and Amortization: Consideration transferred 1/1/13 ………….. $600,000 Book value (given) ………………..…..…..……. […]

978-0077862220 Chapter 3 Solution Manual Part 4

30. (65 Minutes) (Consolidated totals and worksheet five years after acquisition. Parent uses equity method. Includes goodwill impairment.) a. Acquisition-date fair value allocations (given) Remaining Annual excess life amortizations Land $90,000 — — earnings) less $5,000 in amortization expense computed […]

978-0077862220 Chapter 3 Solution Manual Part 5

36. (20 Minutes) (Consolidated balances three years after acquisition. Parent has applied the equity method.) a. Schedule 1—Acquisition-Date Fair Value Allocation and Amortization Jasmine’s acquisition-date fair value $206,000 Excess fair value assigned to specific accounts based on individual fair values […]

978-0077862220 Chapter 3 Solution Manual Part 6

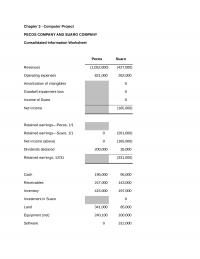

Chapter 3 – Computer Project PECOS COMPANY AND SUARO COMPANY Consolidated Information Worksheet Pecos Suaro Revenues (1,052,000) (427,000) Retained earnings—Pecos, 1/1 Retained earnings—Suaro, 1/1 0 (201,000) Net income (above) 0 (165,000) Dividends declared 200,000 35,000 Retained earnings, 12/31 (331,000) Cash […]

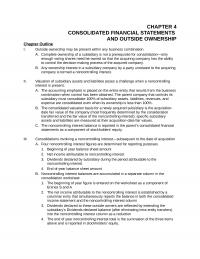

978-0077862220 Chapter 4 Solution Manual Part 1

CHAPTER 4 CONSOLIDATED FINANCIAL STATEMENTS AND OUTSIDE OWNERSHIP Chapter Outline I. Outside ownership may be present within any business combination. A. Complete ownership of a subsidiary is not a prerequisite for consolidation—only enough voting shares need be owned so that […]

978-0077862220 Chapter 4 Solution Manual Part 2

27. (15 minutes) Consolidated figures with noncontrolling interest Fair value of company (given) $60,000 Book value (10 ,000) Fair value in excess of book value 50,000 Consolidated figures: Net income attributable to noncontrolling interest = 40% ($50,000 revenues less […]

978-0077862220 Chapter 4 Solution Manual Part 3

35. (Acquisition Method Consolidated Balances) Adjustments December 31, 2015 Paloma San Marco & Eliminations NCI Consolidated Revenues (1,843,000) (675,000) (2,518,000) Cost of goods sold 1,100,000 322,000 1,422,000 net income (437,000) (215,000) Consolidated net income (450,500) To noncontrolling interest (13,500) (13,500) […]

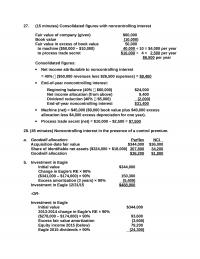

978-0077862220 Chapter 4 Solution Manual Part 4

39. (25 minutes) (Consolidated balances after a mid-year acquisition) a. Investment account balance indicates the initial value method. Consideration transferred by Gibson……. $528,000 Noncontrolling interest fair value ………… 352 ,000 Davis acquisition-date fair value …..…..…. 880,000 5 years………………………..…..…..…..$(6,000) Goodwill ………..……………….…..…..… […]

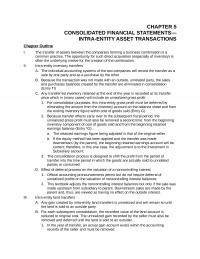

978-0077862220 Chapter 5 Solution Manual Part 1

CHAPTER 5 CONSOLIDATED FINANCIAL STATEMENTS— INTRA-ENTITY ASSET TRANSACTIONS Chapter Outline I. The transfer of assets between the companies forming a business combination is a common practice. The opportunity for such direct acquisition (especially of inventory) is often the underlying motive […]

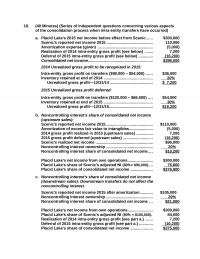

978-0077862220 Chapter 5 Solution Manual Part 2

18. (40 Minutes) (Series of independent questions concerning various aspects of the consolidation process when intra-entity transfers have occurred) a. Placid Lake’s 2015 net income before effect from Scenic…… $300,000 Scenic’s reported net income 2015 ……………..…….……..…….… 110,000 Consolidated net income…………..……….………..……….…………… […]

978-0077862220 Chapter 5 Solution Manual Part 3

26. (35 Minutes) (Prepare consolidation entries for a business combination with intra-entity inventory and equipment transfers; includes an outside ownership.) a. Entry *G Retained earnings, 1/1/15 (Sledge) ……..…..… 2,000 remaining inventory ($5,000). Entry *TA Equipment……….………….………….…..…..…..…… 4,000 Investment in Sledge ……….…..…..…..…..….…. […]

978-0077862220 Chapter 5 Solution Manual Part 4

30. (continued) A Liabilities ………..………..………..………..……….………. 32,000 Equipment ………….………..……….………..………..…… 15,000 Brand names ………..………..…………….…..….…..….. 45,000 Investment in Kirby ……………………….…..….…. 82,800 Noncontrolling interest in Kirby (10%) ………. 9,200 (To recognize unamortized balance of excess allocations as of 1/1/15. Figures have been reduced by […]

978-0077862220 Chapter 5 Solution Manual Part 5

35. (60 Minutes) (Consolidation worksheet for combination with upstream inventory transfers and downstream transfer of land. Also asks about transfer of a building. Parent uses partial equity method.) Consideration transferred …………….……..….…. $570,000 Noncontrolling interest fair value…………………. 380 ,000 to customer […]

978-0077862220 Chapter 6 Solution Manual Part 1

CHAPTER 6 VARIABLE INTEREST ENTITIES, INTRA-ENTITY DEBT, CONSOLIDATED CASH FLOWS, AND OTHER ISSUES Chapter Outline I. Variable interest entities (VIEs) A. VIEs typically take the form of a trust, partnership, joint venture, or corporation. In most cases a sponsoring firm […]

978-0077862220 Chapter 6 Solution Manual Part 2

25. (40 minutes) (Acquisition-date consolidated worksheet for a parent and a variable interest entity) Access Net Adjust. & Elim. Consolidated IT Connect NCI Balances Cash 61,000 41,000 102,000 equipment 916,000 336,000 1,252,000 Research and development asset A1,960,000 1,960,000 Patent 191,000 […]

978-0077862220 Chapter 6 Solution Manual Part 3

33.(15 Minutes) (The effect that various events have on a consolidated statement of cash flows.) Sale of building. The $44,000 in cash received from the sale is listed as a cash inflow within the company’s investing activities. If the company […]

978-0077862220 Chapter 6 Solution Manual Part 4

43.(45 Minutes) (Prepare consolidation entries after intra-entity bond acquisition.) a. Allocation of Acquisition-date Excess Fair Value Consideration transferred $312,000 Noncontrolling interest fair value 208,000 Acquisition-date fair value $520,000 Total $20,500 CONSOLIDATION ENTRIES Entry *TL Investment in Herman ………..…………….………………… 7,000 Land […]

978-0077862220 Chapter 6 Solution Manual Part 5

46.(40 Minutes) (Compute basic and diluted earnings per share. Subsidiary has stock warrants outstanding and convertible debt.) Basic EPS—Austin, Inc. Consolidated net income to parent….…..…..…..…..…..… $284,000 Austin’s preferred dividends …………………………..………. (40 ,000) Diluted EPS—Austin, Inc. Subsidiary earnings and shares for […]

978-0077862220 Chapter 7 Solution Manual Part 1

CHAPTER 7 CONSOLIDATED FINANCIAL STATEMENTS—OWNERSHIP PATTERNS AND INCOME TAXES Chapter Outline I. Indirect subsidiary control A. Control of subsidiary companies within a business combination is often of an indirect nature; one subsidiary possesses the stock of another rather than the […]

978-0077862220 Chapter 7 Solution Manual Part 2

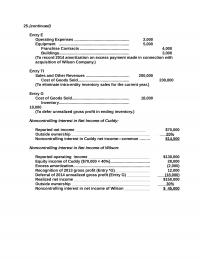

17. (30 Minutes) (Consolidated net income figures for a connecting affiliation) UNREALIZED GROSS PROFIT: Wisconsin ($40,000 remaining inventory × 30% markup) = $12,000 NONCONTROLLING INTERESTS: CLEVELAND: Operating income (sales minus cost of goods sold and expenses) ………..………..………..………..…………..…..….…… $60,000 Defer unrealized […]

978-0077862220 Chapter 7 Solution Manual Part 3

25.(continued) Entry E Operating Expenses ………….………..………..………..….. 2,000 Equipment ………..………..………..………..………..…..….. 5,000 Franchise Contracts …………………..….…..….….….. 4,000 Cost of Goods Sold………….……….….…..….….……. 200,000 (To eliminate intra-entity inventory sales for the current year.) Entry G Cost of Goods Sold………….………..………..………….….. 18,000 Inventory……………………………..………..………….…… 18,000 (To defer unrealized […]

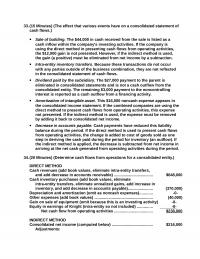

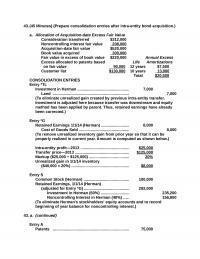

978-0077862220 Chapter 7 Solution Manual Part 4

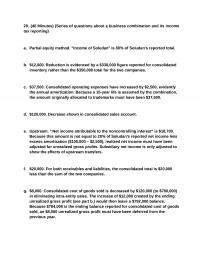

28. (40 Minutes) (Series of questions about a business combination and its income tax reporting) a. Partial equity method. “Income of Soludan” is 80% of Soludan’s reported total. b. $12,000. Reduction is evidenced by a $338,000 figure reported for consolidated […]

978-0077862220 Chapter 8 Solution Manual Part 1

CHAPTER 8 SEGMENT AND INTERIM REPORTING Chapter Outline I. FASB Accounting Standards Codification Topic 280, Segment Reporting (FASB ASC 280), provides current guidance on segment reporting. A. ASC 280 follows a management approach in which segments are based on the […]

978-0077862220 Chapter 8 Solution Manual Part 2

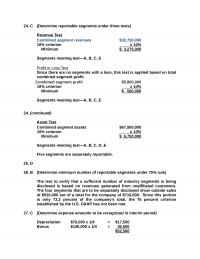

24. C (Determine reportable segments under three tests) Revenue Test Combined segment revenues $32,750,000 10% criterion x 10% Minimum $ 3,275,000 24. (continued) Asset Test Combined segment assets $67,500,000 10% criterion x 10% Minimum $ 6,750,000 Segments meeting test—A, B, […]

978-0077862220 Chapter 8 Solution Manual Part 3

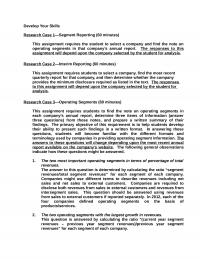

Develop Your Skills Research Case 1—Segment Reporting (60 minutes) This assignment requires the student to select a company and find the note on operating segments in that company’s annual report. The responses to this assignment will depend upon the company […]

978-0077862220 Chapter 9 Solution Manual Part 1

CHAPTER 9 FOREIGN CURRENCY TRANSACTIONS AND HEDGING FOREIGN EXCHANGE RISK Chapter Outline I. In today’s global economy, a great many companies deal in currencies other than their reporting currencies. A. Merchandise may be imported or exported with prices stated in […]

978-0077862220 Chapter 9 Solution Manual Part 2

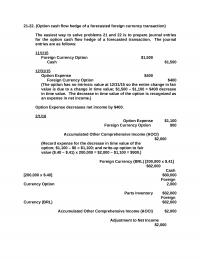

21-22. (Option cash flow hedge of a forecasted foreign currency transaction) The easiest way to solve problems 21 and 22 is to prepare journal entries for the option cash flow hedge of a forecasted transaction. The journal entries are as […]

978-0077862220 Chapter 9 Solution Manual Part 3

32. (40 minutes) (Forward contract hedge of foreign currency payable) a. Cash Flow Hedge 32. (continued) a. Cash Flow Hedge (continued) 32. (continued) b. Fair Value Hedge 32. (continued) b. Fair Value Hedge (continued) 33. (30 minutes) (Option hedge of […]

978-0077862220 Chapter 9 Solution Manual Part 4

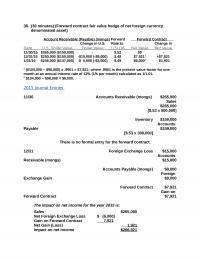

36. (30 minutes) (Forward contract fair value hedge of net foreign currency denominated asset) Account Receivable (Payable) (mongs) Forward Forward Contract Change in U.S. Rate to Change in Date U.S. Dollar Value Dollar Value 1/31/16 Fair Value Fair Value 11/30/15 […]

978-0077862220 Chapter 9 Solution Manual Part 5

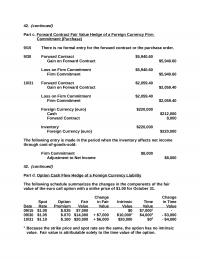

42. (continued) Part c. Forward Contract Fair Value Hedge of a Foreign Currency Firm Commitment (Purchase) 9/15 There is no formal entry for the forward contract or the purchase order. 9/30 Forward Contract $5,940.60 Gain on Forward Contract $5,940.60 Foreign […]

AC 427

2) Kaycee Corporation’s revenues for the year ended December 31, 2012, were as follows: Consolidated Revenue per the Income Statement: $1,200,000 Upstream Intersegment Sales: $180,000 Downstream Intersegment Sales: $60,000 For purposes of the Revenue Test, what amount will be used […]

AC 503

2) Webb Company owns 90% of Jones Company. The original balances presented for Jones and Webb as of January 1, 2013 are as follows: Assume Jones issues 20,000 new shares of its common stock for $15 per share. Of this […]

AC 522 Quiz 1

1) A company incurs research and development costs of $200,000 in 2013 of which $50,000 of these costs relate to development activities because certain criteria have been met which suggest that an intangible asset has been created. As a result […]

AC 581 Test

1) Mills Inc. had a receivable from a foreign customer that is due in the local currency of the customer (stickles). On December 31, 2012, this receivable for §200,000 was correctly included in Mills’ balance sheet at $132,000. When the […]

AC 854 Test

1) Which entry would be the correct entry on the donor’s books when the donor relinquishes control of an asset that it contributes to a not-for-profit organization? A.Option A B.Option B C.Option C D.Option D E.Option E 2) The financial […]

AC 892 Quiz 1

1) Pot Co. holds 90% of the common stock of Skillet Co. During 2013, Pot reported sales of $1,120,000 and cost of goods sold of $840,000. For this same period, Skillet had sales of $420,000 and cost of goods sold […]

Acc 131 Quiz 1

1) Natarajan, Inc. had the following operating segments, with the indicated amounts of segment revenues and segment expenses: For purposes of the profit or loss test, segment C’s operating profit or (loss) is A.$1,300,000 B.$700,000 C.$2,000,000 D.$200,000 E.$(200,000) 2) Bullen […]

ACC 472 Midterm 1 West Corp owned

1) West Corp. owned 70% of the voting common stock of East Co. East owned 60% of Compass Co. West and East both used the initial value method to account for their investments. The following information was available from the […]

Acc 660 Quiz 1

1) Baker Corporation changed from the LIFO method to the FIFO method for inventory valuation during 2013. Baker has an effective income tax rate of 30 percent and 100,000 shares of common stock issued and outstanding. The following additional information […]

Acc 670 Midterm 1

1) On January 1, 2013, Riney Co. owned 80% of the common stock of Garvin Co. On that date, Garvin’s stockholders’ equity accounts had the following balances: The balance in Riney’s Investment in Garvin Co. account was $552,000, and the […]

ACC 779 Test

1) Keenan Company has had bonds payable of $20,000 outstanding for several years. On January 1, 2013, there was an unamortized premium of $2,000 with a remaining life of 10 years, Keenan’s parent, Ross, Inc., purchased the bonds in the […]

Acc 793

1) Pell Company acquires 80% of Demers Company for $500,000 on January 1, 2014. Demers reported common stock of $300,000 and retained earnings of $210,000 on that date. Equipment was undervalued by $30,000 and buildings were undervalued by $40,000, each […]

Accounting 644 Quiz 2

1) Bullen Inc. acquired 100% of the voting common stock of Vicker Inc. on January 1, 2013. The book value and fair value of Vicker’s accounts on that date (prior to creating the combination) follow, along with the book value […]

Accounting 706 Quiz 3

1) On January 1, 2013, Riley Corp. acquired some of the outstanding bonds of one of its subsidiaries. The bonds had a carrying value of $421,620, and Riley paid $401,937 for them. How should you account for the difference between […]

Accounting 721 Test

1) Presented below are the financial balances for the Atwood Company and the Franz Company as of December 31, 2012, immediately before Atwood acquired Franz. Also included are the fair values for Franz Company’s net assets at that date. Note: […]

Accounting 773 Homework

1) On May 1, 2013, Mosby Company received an order to sell a machine to a customer in Canada at a price of 2,000,000 Mexican pesos. The machine was shipped and payment was received on March 1, 2014. On May […]

Accounting 856 Final

1) On January 1, 2013, Deuce Inc. acquired 15% of Wiz Co.’s outstanding common stock for $62,400 and categorized the investment as an available-for-sale security. Wiz earned net income of $96,000 in 2013 and paid dividends of $36,000. On January […]

ACCT 148 Midterm

1) On January 1, 2013, Riney Co. owned 80% of the common stock of Garvin Co. On that date, Garvin’s stockholders’ equity accounts had the following balances: The balance in Riney’s Investment in Garvin Co. account was $552,000, and the […]

ACCT 178 Homework 1 When a company

1) When a company applies the initial method in accounting for its investment in a subsidiary and the subsidiary reports income in excess of dividends paid, what entry would be made for a consolidation worksheet? A) A above B) B […]

Acct 492 Test 2

1) Quadros Inc., a Portuguese firm was acquired by a U.S. company on January 1, 2012. Selected account balances are available for the year ended December 31, 2013, and are stated in Euro, the local currency. Assume the functional currency […]

Acct 660 Quiz 1

1) Watkins, Inc. acquires all of the outstanding stock of Glen Corporation on January 1, 2012. At that date, Glen owns only three assets and has no liabilities: If Watkins pays $450,000 in cash for Glen, at what amount would […]

ACCT 735 Test 2

1) Campbell Inc. owned all of Gordon Corp. For 2013, Campbell reported net income (without consideration of its investment in Gordon) of $280,000 while the subsidiary reported $112,000. The subsidiary had bonds payable outstanding on January 1, 2013, with a […]

ACCT 838 Quiz

1) A new truck was ordered for the sanitation department at a cost of $122,200 on September 3, 2013. Required: (A) Prepare the required journal entry in the General Fund for the Fund Financial Statements. (B) Prepare the required journal […]

ACCT 871 Test 2

1) Certain balance sheet accounts of a foreign subsidiary of Parker Company at December 31, 2013, have been restated into U.S. dollars as follows: Assuming the functional currency of the subsidiary is the local currency, what total should be included […]

Acct 891 Test 2

1) Quadros Inc., a Portuguese firm was acquired by a U.S. company on January 1, 2012. Selected account balances are available for the year ended December 31, 2013, and are stated in Euro, the local currency. Assume the functional currency […]

ACT 195 Homework

1) The Fratilo Co. had three operating segments with the following information: In addition, revenues generated at corporate headquarters are $1,400 What is the minimum amount of revenue that each of these segments must earn to be considered separately reportable? […]

ACT 611 Quiz 3

1) The following information pertains to inventory held by a company at December 31, 2013. As a result of inventory loss, what is the difference in income between reporting using U.S. GAAP and IFRS? A.U.S. GAAP income is $1,000 higher. […]

MET MG 107

2) On January 3, 2013, Austin Corp. purchased 25% of the voting common stock of Gainsville Co., paying $2,500,000. Austin decided to use the equity method to account for this investment. At the time of the investment, Gainsville’s total stockholders’ […]

MET MG 423 Quiz

1) Bullen Inc. acquired 100% of the voting common stock of Vicker Inc. on January 1, 2013. The book value and fair value of Vicker’s accounts on that date (prior to creating the combination) follow, along with the book value […]

MET MG 808 Midterm 2

1) The following information pertains to inventory held by a company at December 31, 2013. What amount of inventory should be reported under U.S. GAAP? A.$25,000. B.$21,000. C.$20,000. D.$16,800. E.$16,000. 2) Cleary, Wasser, and Nolan formed a partnership on January […]

SMG AC 134 Midterm

1) White Company owns 60% of Cody Company. Separate tax returns are required. For 2012, White’s operating income (excluding taxes and any income from Cody) was $300,000 while Cody reported a pretax income of $125,000. During the period, Cody paid […]

SMG AC 540

1) A company sells a building to a bank in 2013 at a gain of $100,000 and immediately leases the building back for period of five years. The lease is accounted for as an operating lease. The building was originally […]

SMG AC 679

1) Pell Company acquires 80% of Demers Company for $500,000 on January 1, 2014. Demers reported common stock of $300,000 and retained earnings of $210,000 on that date. Equipment was undervalued by $30,000 and buildings were undervalued by $40,000, each […]