39. (25 minutes) (Consolidated balances after a mid-year acquisition)

a. Investment account balance indicates the initial value method.

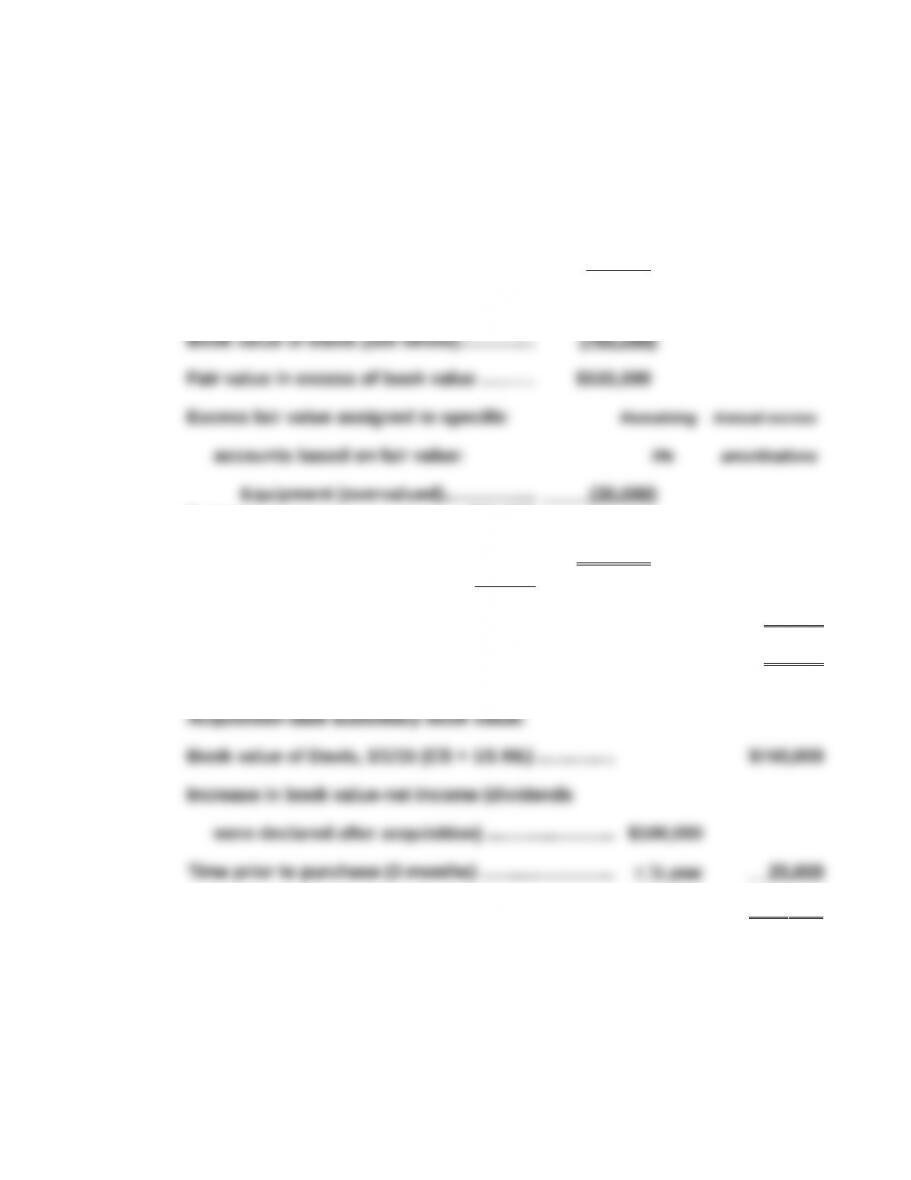

Consideration transferred by Gibson....... $528,000

Noncontrolling interest fair value ............ 352 ,000

Davis acquisition-date fair value …..…..…. 880,000

5 years………………………..…..…..…..$(6,000)

Goodwill ………..……………….…..…..… $145 ,000

indefinite…………………..……………… -0-

Total …..………..………..………..……….…….. $(6 ,000)

Amortization for 9 months ………………. $(4 ,500)

Book value of Davis, 4/1/15 (acquisition date) ........ $765 ,000

Consolidated income statement:

Revenues (1) $825,000

Cost of goods sold (2) $405,000

Operating expenses (3) 214 ,500 619 ,500

(2) $440,000 combined COGS less $35,000 (preacquisition subsidiary COGS)

(3) $234,000 combined operating expenses less $15,000 (preacquisition

subsidiary operating expenses) less nine month excess overvalued

equipment depreciation reduction of $4,500

(4) 40% of post-acquisition subsidiary net income less excess amortization

b. Goodwill = $145,000 (original allocation)

Equipment = $774,500 (add the two book values less $30,000

reduction to fair value plus $4,500 nine months excess

amortization)

40. (40 minutes) Determine consolidated balance for a mid-year acquisition.

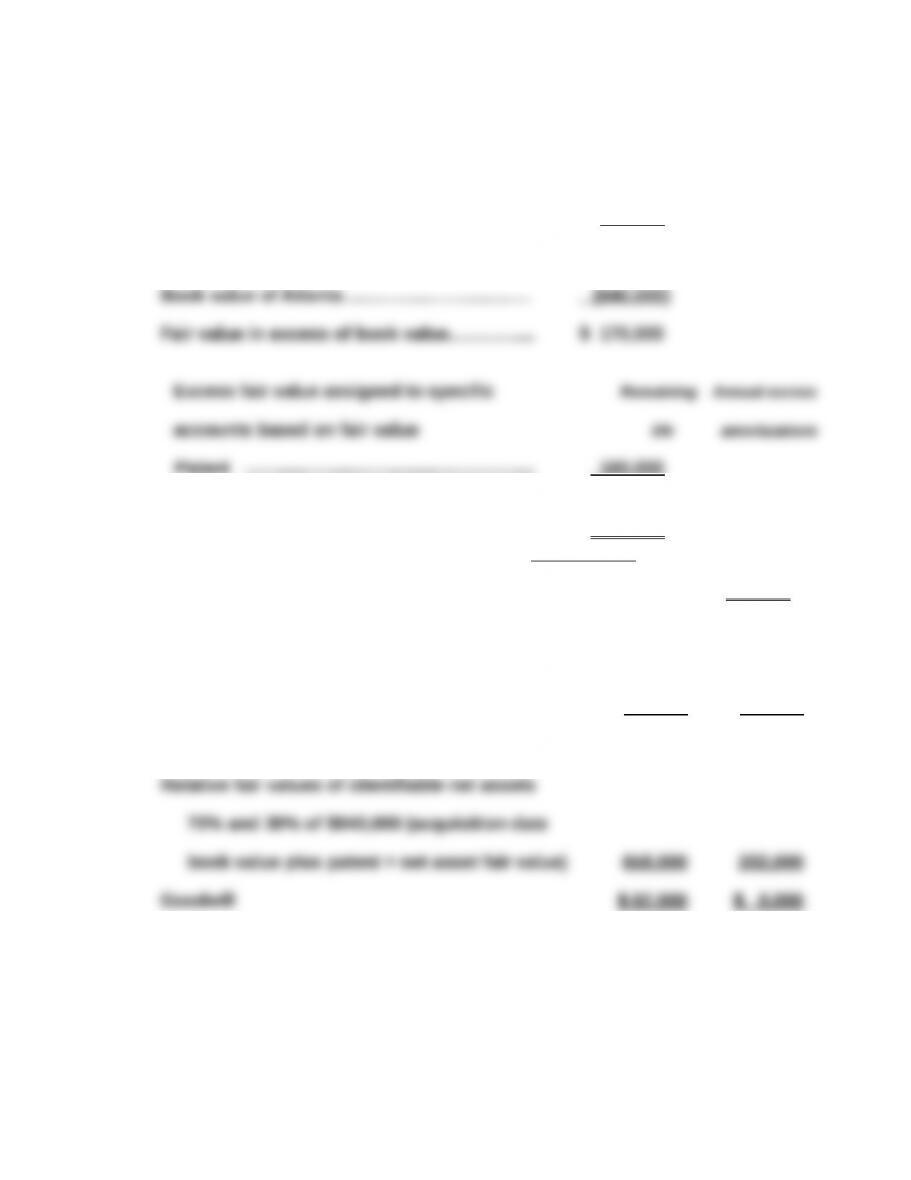

a. Consideration transferred by Truman ….….... $720,000

Noncontrolling interest fair value …………..…. 290 ,000

Atlanta’s acquisition-date total fair value...... $1,010,000

Patent ……….………..…………..…..…..……….... 100 ,000

5 years………………..……….…………...$20,000

Goodwill …………………..…..…..…..…..…..…..… $ 70 ,000

indefinite…………………..……………..…..…..… -0 –

Total …………..………..………..………..……….... $20,000

b. Goodwill allocation with control premium Controlling Noncontrolling

Interest Interest

Fair values at acquisition date $720,000 $290,000

c. Initial value at acquisition date $720,000

Truman’s share of Atlanta’s net income for half year

([$120,000 – 20,000 amortization × ½ year] × 70%) 35,000

40. (continued)

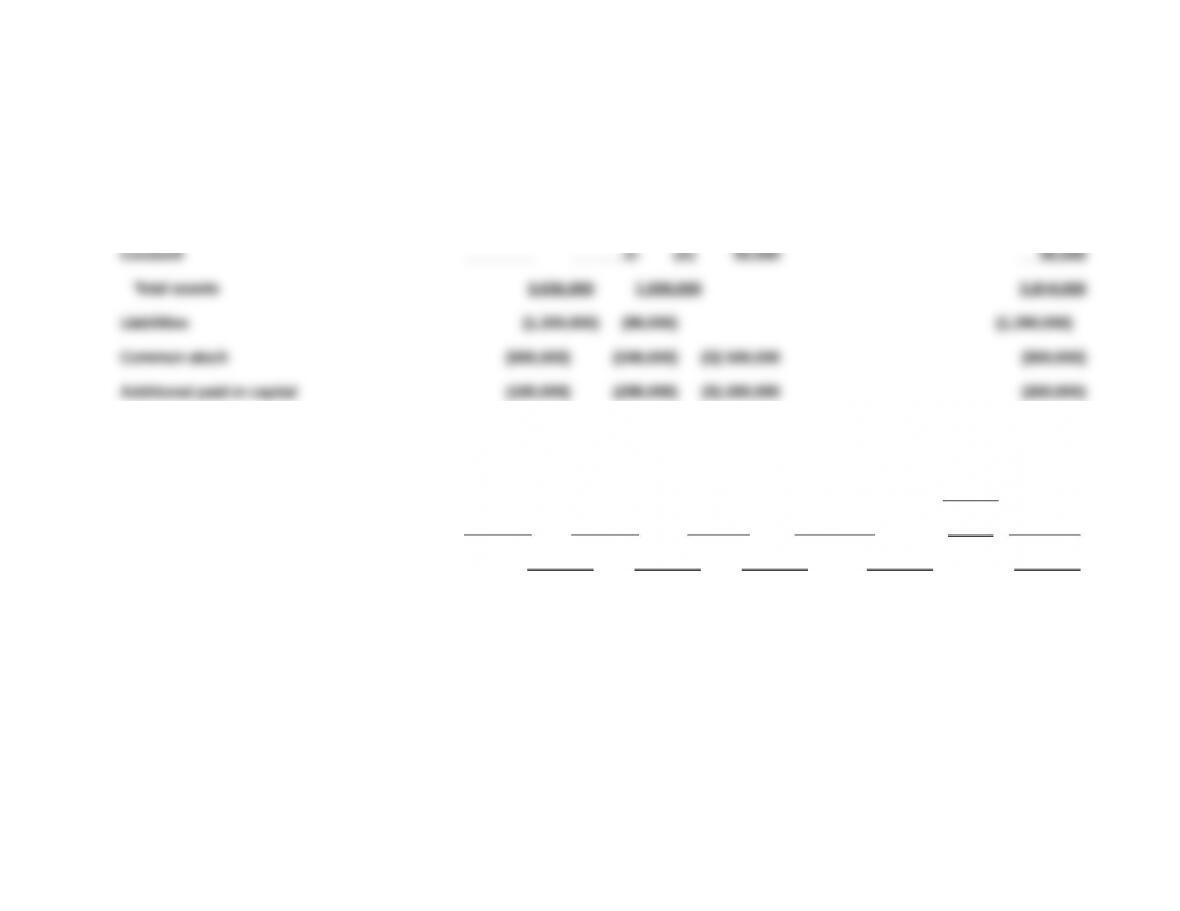

d. Consolidated Worksheet

TRUMAN COMPANY AND SUBSIDIARY ATLANTA COMPANY

Consolidation Worksheet

For Year Ending December 31, 2015

Truman Atlanta Adjustments & Eliminations NCI Cons.

Revenues (670,000) (400,000) (S)200,000 (870,000)

Operating Expenses 402,000 280,000 (E) 10,000 (S)140,000 552,000

Net income of subsidiary (35,000) (I) 35,000 -0-

Separate company net income (303,000) (120,000)

Retained earnings, 1/1 (823,000) (500,000) (S) 500,000 (823,000)

Net income (above) (303,000) (120,000) (303,000)

Dividends declared 145,000 80,000 (S) 40,000 12,000

(I) 35,000

(A1) 70,000

(A2) 62,000

Land 388,000 200,000 588,000

Buildings 701,000 630,000 1,331,000

Goodwill (A2) 70,000 70,000

Total assets 2,297,000 1,220,000 2,950,000

Liabilities (816,000) (360,000)

(1,176,000

)

Noncontrolling interest 7/1 (A1) 30,000

(A2) 8,000

(S) 252,000

(290,000

)

(293,000

(293,000

41. (60 minutes) (Consolidated statements for a step acquisition)

a. Fair value of Sysinger 1/1/15 (given) $1,750,000

Book value of Sysinger 1/1/15 (CS + APIC + RE) 1 ,300,000

To goodwill $50 ,000

b. Equity in earnings of Sysinger

2015 net income (150,000 × 95%) $142,500

Revaluation of 15% block to fair value

Consideration transferred $184,500

2014 net income (100,000 × 15%) 15,000

Investment account balance

Fair value at 1/1/15 (15% block) $262,500

Consideration transferred 1/1/15 (80% block) 1,400,000

Equity earnings 2015

Net income (95% × 150,000) 142,500

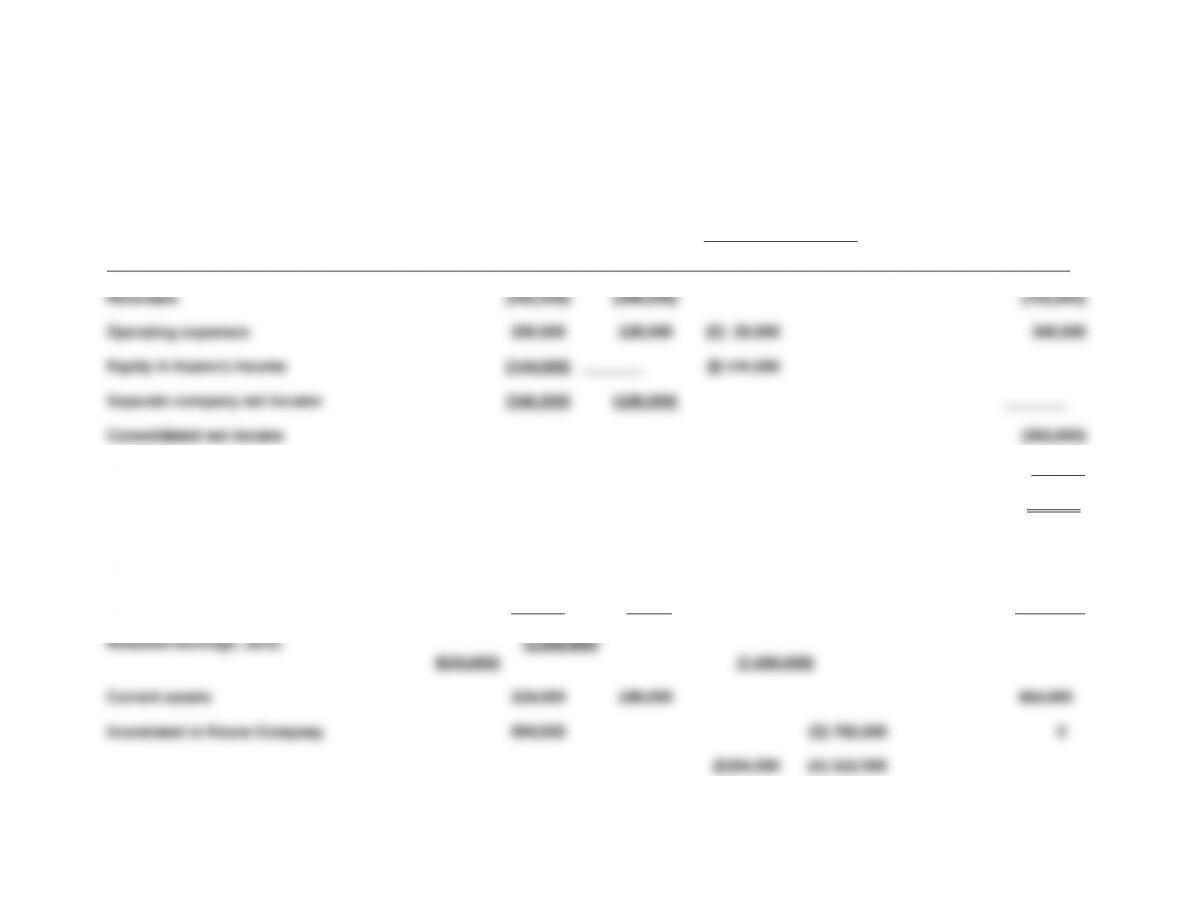

41. (Continued) c. Allan and Sysinger

Consolidation Worksheet

For Year Ending December 31, 2015

Allan Sysinger Consolidation Entries Noncontrolling Consolidated

Accounts Company Company Debit Credit Interest Totals

Consolidated net income (433,500)

NI attributable to noncontrolling interest (2,500) 2 ,500

NI attributable to Allan Company (431 ,000)

Retained earnings, 1/1 (965,000) (600,000) (S) 600,000 (965,000)

Net income (431,000) (150,000) (431,000)

(I) 47,500

(A) 427,500

Property, plant, and equipment 826,000 590,000 1,416,000

Patented technology 850,000 370,000 1,220,000

Customer contract -0- -0- (A) 400,000 (E) 100,000 300,000

Retained earnings 12/31 (1,256,000) (710,000) (1,256,000)

NCI in Sysinger, 1/1 -0- -0- (S) 65,000

(A) 22,500 (87 ,500)

NCI in Sysinger, 12/31 -0 – -0 – (88 ,000) (88 ,000)

Total liab. and stockholders’ equity (3 ,636,000) (1 ,500,000) 1 ,935,500 1 ,935,500 (3 ,814,000)

42. (60 minutes) (Step acquisition—control previously acquired.)

a. According to the acquisition method, the valuation basis for a subsidiary is

established on the date control is obtained, in this case January 1, 2014.

Fair value of Keane Company 1/1/14 ($573,000 ÷ 60%) $955,000

Percent acquired in step acquisition 30 %

Value assigned to 30% acquisition 301,500

Cash paid for the 30% acquisition 300 ,000

Credit to APIC from 30% step acquisition $ 1 ,500

Entry to record 30% additional investment in Keane:

1/1/15 Investment in Keane 301,500

Cash 300,000

APIC from step acquisition 1,500

b. Investment in Keane Company 1/1/14 $573,000

2015 Dividends from Keane (90% × $60,000) (54 ,000)

Investment in Keane Company 12/31/15 $994 ,500

42. (continued) part c. BRETZ, INC. AND KEANE COMPANY

Consolidation Worksheet

Year Ending December 31, 2015

Consolidation Entries Noncontrolling Consolidated

Accounts Bretz, Inc. Keane Co. Debit Credit Interest Totals

NI attributable to noncontrolling interest (16,000) 16 ,000

NI attributable to Bretz, Inc. (346 ,000)

Retained earnings, 1/1 (797,000) (500,000) (S) 500,000 (797,000)

Net income (above) (346,000) (180,000) (346,000)

Dividends declared 143 ,000 60 ,000 (D) 54,000 6,000 143 ,000

(I) 144,000

Trademarks 106,000 600,000 706,000

Equipment (net) 380,000 110,000 490,000

Goodwill (A) 25,000 25 ,000

Retained earnings,12/31 (1,000,000) (620,000) (1,000,000)

Non-controlling interest 1/1 (A) 12,500

(S) 88,000 (100 ,500)

Non-controlling interest 12/31 (110 ,500)

(110,500)

ACCOUNTING THEORY RESEARCH CASE: NONCONTROLLING INTEREST

In deliberations prior to the issuance of SFAS 160, “Noncontrolling Interests in

Consolidated Financial Statements,” the FASB considered three alternatives for

displaying the noncontrolling interest in the consolidated balance sheet

What were these three alternatives?

What criteria did the FASB use to evaluate the desirability of each alternative?

The FASB evaluated whether the classifications conformed to current definitions

In what specific ways did FASB Concept Statement 6 affect the FASB’s evaluation

of these alternatives?

From SFAS 160 paragraphs 32-34

If it required that the noncontrolling interest be reported in the mezzanine,

the Board would have had to create a new element—noncontrolling

interest in subsidiaries—specifically for consolidated financial

statements. The Board concluded that no compelling reason exists to

The Board concluded that a noncontrolling interest in a subsidiary does

not meet the definition of a liability in the Board’s conceptual framework.

The Board concluded that a noncontrolling interest represents the

residual interest in the net assets of a subsidiary within the consolidated

RESEARCH CASE: COCA-COLA’S ACQUISITION OF COCA-COLA ENTERPRISES

1. How did Coca-Cola allocate the acquisition-date fair value of CCE among the assets

acquired and liabilities assumed?

Note 2 (Acquisitions and Divestitures) of Coca-Cola’s 2010 10-K shows the following

allocation for the CCE acquisition:

Cash and cash equivalents $ 49

Marketable securities 7

Trade accounts receivable 1,194

Total identifiable assets acquired 14,468

Accounts payable and accrued expenses 1,826

Loans and notes payable 266

Long-term debt 9,345

Pension and other postretirement liabilities 1,313

2. What are employee replacement awards? How did Coca-Cola account for the

replacement award value provided to the former employees of CCE?

Employee replacement award represent various share-based payments to employees

that the acquiring firm replaces with new awards based on its shares. The ASC

3. How did Coca-Cola account for its 33 percent interest in CCE prior to the acquisition

of the 67 percent not already owned by Coca-Cola?

4. Upon acquisition of the additional 67 percent interest, how did Coca-Cola account for

the change in fair value of its original 33 percent ownership interest?

“We remeasured our equity interest in CCE to fair value upon the close of the

INSTAPOWER: FASB ASC AND IFRS RESEARCH CASE

1. What is the total consideration transferred by Q-Car to acquire its 90 percent

controlling interest in InstaPower?

Cash $60,000,000

Shares of Q-Car stock 27,000,000

2. What values should Q-Car assign to identifiable assets and liabilities as part of the

acquisition accounting?

Cash $ 270,000

Accounts receivable 800,000

Land 2,930,000

Building 19,000,000

Machinery 46,000,000

(ASC 805-20-30-1)

3. What is the acquisition-date value assigned to the 10 percent noncontrolling interest?

What are the noncontrolling interest valuation alternatives available under IFRS?

Under U.S. GAAP, the acquisition-date noncontrolling interest is measured at its fair

value. In this case, there are no readily available market values for the noncontrolling

4. Under U.S. GAAP, what amount should Q-Car recognize as goodwill from the

acquisition? What alternative valuations are available for goodwill under IFRS?

Goodwill under U.S. GAAP (ASC 805-30-30-1) and IFRS alternative 1 (IFRS 3 IN 8):

Consideration transferred (above) $ 97,000,000

Acquisition-date noncontrolling interest fair value 11,000,000

Acquisition-date value assigned to subsidiary $106,000,000

Net assets acquired fair value (above) 90,000,000

Goodwill $ 16,000,000