19.(10 minutes) (Determine amount to be contributed by partner with a deficit

capital balance)

White and Blue are both insolvent and have negative capital balances (after

offsetting the loan from White) totaling $15,000 (White, $3,000; Blue, $12,000).

Absorption by the other partners of these losses would be as follows (on a

30:10:20 basis):

Current Adjusted

Partner Capital Balance Share of Loss Capital Balance

Black, who is also insolvent, now has a deficit capital balance of $4,500 that

would have to be absorbed by Brown and Green (on a 10:20 basis):

Current Adjusted

Partner Capital Balance Share of Loss Capital Balance

Thus, Green must contribute $7,000 that will go to Brown.

20.(50 minutes) (Determine payments under a variety of circumstances; safe

capital balances; predistribution plan)

a. Dobbs receives the entire $10,000.

Maximum potential losses of $250,000 on noncash assets would be allocated

as follows:

Partner Share of Loss New Capital Balance

Adams 2/10 x $250,000 = $50,000 $ 30,000

Dobbs 2/10 x $250,000 = $50,000 $ 40,000

Maximum total potential losses of $60,000 to be absorbed from Baker and

Carvil above would then be allocated to Adams and Dobbs as follows on a 2:2

basis:

Partner Share of Loss New Capital Balance

b. Adams receives the entire $10,000.

Maximum potential losses of $250,000 on noncash assets would be allocated

as follows:

Partner Share of Loss New Capital Balance

Adams 2/10 x $250,000 = $50,000 $ 30,000

Maximum total potential losses of $35,000 to be absorbed from Baker and

Carvil above would be allocated to Adams and Dobbs as follows on a 2:3

basis:

Partner Share of Loss New Capital Balance

Absorbing the final $6,000 loss from Dobbs would leave Adams with a safe

capital balance of $10,000.

20. (continued)

c. Adams receives $57,500 and Dobbs gets $22,500.

The $50,000 loss on sale of the building would be allocated as follows:

Partner Share of Loss New Capital Balance

Adams 10% x $50,000 = $5,000 $ 75,000

Maximum potential loss of $130,000 on the land would be allocated as follows:

Partner Share of Loss New Capital Balance

Adams 10% x $130,000 = $13,000 $ 62,000

Maximum potential loss of $24,000 to be absorbed from Baker would be

allocated as follows on a 1:3:3 basis:

Partner Share of Loss New Capital Balance

Adams 1/7 x $24,000 = $3,428 $ 58,572

Maximum potential loss of $4,286 to be absorbed from Carvil would be

allocated as follows on a 1:3 basis:

Partner Share of Loss New Capital Balance

Adams 1/4 x $4,286 = $1,072 $57,500

20. (continued)

d. The land and building must be sold for over $115,000 to ensure that Carvil will

receive some cash.

This can be determined by preparing a predistribution plan as follows:

Adams Baker Carvil Dobbs

Beginning balances $ 80,000 $ 30,000 $ 60,000 $ 90,000

Assumed loss of $90,000

(Schedule 3) (1:0:0:2) (30 ,000) – 0 – – 0 – (60 ,000)

Step Three balances $ 35 ,000 $ – 0 – $ – 0 – $ – 0 –

Schedule 1

Maximum Loss

Capital Balance/ That Can

Partner Loss Allocation Be Absorbed

Adams $80,000/10% $800,000

Schedule 2

Maximum Loss

Capital Balance/ That Can

Partner Loss Allocation Be Absorbed

Schedule 3

Maximum Loss

Capital Balance/ That Can

Partner Loss Allocation Be Absorbed

Adams $65,000/(1/3) $195,000

20.d. (continued)

PREDISTRIBUTION PLAN

The first $35,000 available goes to Adams. Next $90,000 is split between

Adams and Dobbs on a 1:2 basis. Next $35,000 is split between Adams, Carvil,

and Dobbs on a 1:4:2 basis. All remaining cash is split between Adams, Baker,

Carvil, and Dobbs on the original profit and loss ratio.

21. (30 minutes) (Prepare journal entries for a partnership liquidation; prepare a

final statement of partnership liquidation)

Part A. Preparation of journal entries.

a. The partnership has $100,000 in cash, liabilities of $80,000 and estimated

liquidation expenses of $10,000. Thus, there is $10,000 that can be safely

paid to the partners before the liquidation of noncash assets. This amount

is allocated to the two partners on the basis of their potential capital

balances assuming that noncash assets are scrapped for a loss of

$200,000 and liquidation expenses are $10,000:

Current Capital Share of Potential

Partner Balance Maximum Loss* Capital

Because Fred has a potential deficit capital balance, the entire $10,000

currently available is distributed to George, which reduces this partner’s

capital balance to $110,000.

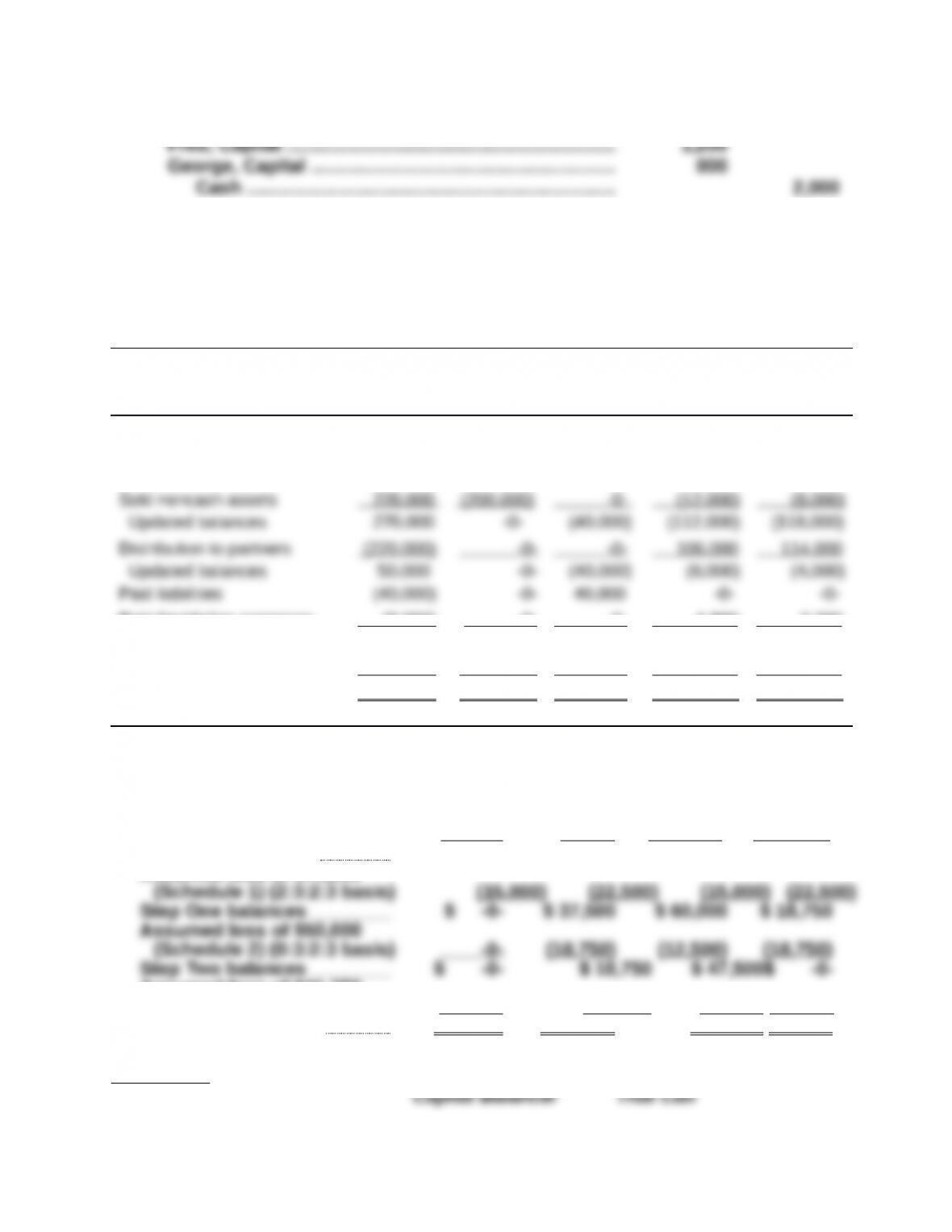

George, Capital………..……………….………………………… 10,000

Cash ……………………….…………………….……………… 10,000

b. Liabilities ………..……………….……………….……………….. 40,000

21. (continued)

d. To determine the safe payments to be made at this point in the liquidation,

the accountant prepares the following proposed schedule of liquidation:

Fred, George,

Non-cash Capital Capital

Cash Assets Liabilities (60 %) (40 %)

Beginning balances $100,000 $200,000 $(80,000) $(100,000)

Sold noncash assets 220 ,000 (200 ,000) -0 – (12 ,000) (8 ,000)

Updated balances 270,000 -0- (40,000) (112,000)

(118,000)

Safe payments of $106,000 and $114,000 can be made to Fred and George,

respectively at this point in the liquidation.

Fred, Capital …………..……………….……………….………… 106,000

George, Capital …………..……………….…………………….. 114,000

Cash ……………………….…………………….……………… 220,000

g. The statement of partnership liquidation presented on the next page shows

that $2,000 cash remains after paying liquidation expenses. The partners

have positive capital balances of $1,200 and $800, respectively, and the

remaining partnership cash can be distributed based on these ending

totals.

21. (continued)

Part B. Prepare a final statement of partnership liquidation.

Fred and George Partnership

Statement of Partnership Liquidation

Cash

Non-cash

Assets Liabilities

Fred,

Capital

(60%)

George,

Capital

(40%)

Beginning balances $100,000 $200,000 $(80,000) $(100,000) $(120,000)

Distribution to partners (10,000) -0- -0- -0- 10,000

Paid liabilities (40,000) -0- 40,000 -0- -0-

Paid liquidation expenses (8,000) -0- -0- 4,800 3,200

Updated balances 2,000 -0- -0- (1,200) (800)

Distribution to partners (2,000) -0- -0- 1,200 800

Closing balances $ -0- $ -0- $ -0- $ -0- $ -0-

22. (30 minutes) (Prepare a predistributlon plan)

An assumed series of losses is simulated which eliminates each partner’s

capital account in turn:

Larson Norris Spencer Harrison

Beginning balances $ 15,000 $ 60,000 $ 75,000 $ 41,250

Assumed loss of $75,000

Assumed loss of $31,250

(Schedule 3) (0:3:2:0 basis) -0- (18 ,750) (12 ,500) -0-

Step Three balances $ -0- $ -0- $ 35 ,000 $ -0-

Schedule 1 Maximum Loss

Partner Loss Allocation Be Absorbed

Larson $15,000/20% $ 75,000

Schedule 2 Maximum Loss

Capital Balance/ That Can

Partner Loss Allocation Be Absorbed

Schedule 3 Maximum Loss

Capital Balance/ That Can

Partner Loss Allocation Be Absorbed

Norris $18,750/(3/5) $ 31,250 (most vulnerable)

Spencer $47,500/(2/5) $118,750

PREDISTRIBUTION PLAN

First $55,000 goes to pay liabilities ($47,000) and liquidation expenses

(estimated at $8,000).

23. (20 minutes) (Prepare and use a predistribution plan)

Part a.

Maximum Losses That Can Be Absorbed

*Able’s balance includes capital and the loan to the partnership.

The assumption is made that a $100,000 loss occurs:

Able Moon Yerkl

Maximum Losses That Now Can Be Absorbed

Able $30,000/.4 $75,000

Moon $30,000/.6 50,000 (most vulnerable to losses)

The assumption is made that a $50,000 loss occurs:

Able Moon

PREDISTRIBUTION PLAN

The first $62,000 will go to pay liquidation expenses ($12,000) and liabilities

($50,000).

Part b.

After the sale of assets for $40,000, the partnership has $76,000 in cash. The

first $62,000 should be held for the liabilities and the liquidation expenses,

24. (25 minutes) (Prepare a predistribution plan for a partnership liquidation)

Maximum Losses That Can Be Absorbed

Simpson $18,000/20% $ 90,000 (most vulnerable to losses)

The assumption is made that a $90,000 loss occurs:

Simpson Hart Bobb Reidl

Reported balances $18,000 $40,000 $48,000 $135,000

Maximum Losses That Now Can Be Absorbed

Hart $4,000/4/8 $ 8,000 (most vulnerable to losses)

The assumption is made that an $8,000 loss occurs:

Hart Bobb Reidl

Reported balances $4,000 $30,000 $117,000

Maximum Losses That Now Can Be Absorbed

Bobb $28,000/2/4 56,000 (most vulnerable to losses)

Reidl $115,000/2/4 230,000

The assumption is made that a $56,000 loss occurs:

Bobb Reidl

Reported balances $28,000 $115,000

PREDISTRIBUTION PLAN

The first $59,000 goes to pay liabilities and expected liquidation expenses.

The next $87,000 goes entirely to Reidl.

25.(30 minutes) (Determine the ramifications of a variety of liquidation situations)

Part A. Partner with Deficit Capital Balance

increase Milburn’s deficit balance by $40,000 (40%).

(b) All $19,000 should go to Thomas. As Ross and Thomas view the current

situation, maximum potential losses total $108,000: $100,000 on the

(c) The minimum cash payment to Thomas would be $35,667.

A loss of $59,000 on the noncash assets would result in the following

capital balances:

Milburn’s deficit further reduces the remaining partner’s balances as

follows:

25. (continued)

Part B. Partners with Deficit Capital Balances; Insolvent Partner

(a) Carton will have to contribute $7,429. The $29,000 in deficits will have to be

(b) Klingon will have to contribute $19,667 [$17,000 + (20/90 x $12,000)] that

will be distributed as follows:

Since Romulan is insolvent, the remaining partners will have to absorb the

$12,000 deficit on a 4:2:3 basis. This allocation increases Klingon’s deficit

by 2/9 of $12,000 or $2,667. Klingon must contribute an amount equal to the

[$5,000 – ($12,000 x 3/9)].

(c) Sampson should receive $500. If Klingon is insolvent, the $17,000 deficit