31. (50 minutes) (Prepare a predistribution plan and journal entries for a

partnership liquidation)

Part A Preparation of Predistribution Plan

Schedule 1

Maximum Loss

Capital Balance/ That Can Be

Partner Loss Allocation Absorbed

Wingler $120,000/30% $400,000

Schedule 2

Maximum Loss

Capital Balance/ That Can Be

Partner Loss Allocation Absorbed

Wingler $75,000/(30/60) $150,000 (most vulnerable to loss)

Schedule 3

Maximum Loss

Capital Balance/ That Can Be

Partner Loss Allocation Absorbed

31. (continued)

Schedule 4

Rodgers,

Wingler, Norris, Loan and Guthrie,

Capital Capital Capital Capital

Beginning balances …..…..….. $120,000 $88,000 $109,000 $60,000

Loss of $150,000 assumed (al-

Loss of $150,000 assumed (al-

located on a 30:10:20 basis)

see Schedule 2 .….….…......... (75,000) (25,000) (50,000) -0-

Step Two balances ………..….... $ -0- $48,000 $ 29,000 $ -0-

Loss of $43,500 assumed

PREDISTRIBUTION PLAN

Payment of all liabilities and liquidation expenses must be assured.

Next $33,500 goes entirely to Norris.

Next $43,500 is allocated to Norris (10/30) and Rodgers (20/30).

31. (continued)

Part B Journal Entries

1. Cash ……………………….………………..………………….….... 65,600

Wingler, Capital (30% of $16,400 loss) ………….….…. 4,920

2. Cash ……………………….………………..………………….….... 150,000

Wingler, Capital (30% of $103,000 loss) …………….... 30,900

Norris, Capital (10%) ………………..……….….….…..….… 10,300

3. Wingler, Capital …………..……………….…..….…..….….… 31,800

Norris, Capital …………..………………..……………………… 58,600

Rodgers extinguishes the loan made to the

partnership.

First $90,000 is held to pay liabilities ($74,000) and estimated liquidation

expenses ($16,000); $140,600 is paid to partners.

31.b. (continued)

4. No journal entry is currently required by Guthrie’s insolvency.

5. Liabilities …………..………………..………………..…. 74,000

Cash ……………………….………..….…..….… 74,000

All liabilities are paid.

6. Cash ……………………….………………..…….…..…... 71,000

Inventory……………….………………..…..….. 101,000

Inventory is sold with loss allocated to partners.

7. Wingler, Capital………..………………..……………… 35,500

Norris, Capital………..……………….…………..….… 11,833

Rodgers, Capital…………….……………….….….…. 23,667

Cash…………………….……………..….….…... 71,000

Distribution of available cash according to predistribution plan.

Although $87,000 in cash is held by the partnership, $16,000 must

8. Wingler, Capital (30% of expenses)……………. 3,300

Norris, Capital (10%).…………….…..….…..….….. 1,100

9.a. Wingler, Capital (30/60 of deficit)……………….. 2,080

31.b. (continued)

CAPITAL ACCOUNT BALANCES

Rodgers,

Wingler, Norris, Loan and Guthrie,

Capital Capital Capital Capital

Beginning balances…..….….…. $120,000 $88,000 $109,000 $60,000

Loss on accounts receivable. (4,920) (1,640) (3,280) (6,560)

Loss on land, building, and

9.b. Wingler, Capital…………..………………..…………… 2,500

Norris, Capital………..……………….…………..….… 834

Chapter 15 Develop Your Skills

Research Case

1. Students often seem to believe that definitive answers can be found for all

2. Several questions can be raised that may impact the ultimate resolution:

In what state will the court case be handled? Different states have

somewhat different laws as to the potential liabilities incurred by partners

and different courts seem to have varying ways of interpreting those laws.

The answers to such questions as these can have a huge impact on the extent of

the liability of the other doctors.

Here are several quotes from The Wall Street Journal article mentioned in the

case that might pertain to the issue at hand:

“Concerns are growing among Andersen‘s roughly 1,750 U.S. partners that even

“The limited-liability partnership is a comparatively new corporate structure,

untested by the kind of stress now besetting Andersen. But that testing appears

“Because it is unclear how much protection the LLP structure will provide

Andersen partners, partnership and bankruptcy lawyers are expected to be

“The limited-liability partnership was invented about a decade ago in the wake of

“‘There is a strong legal tradition that you don’t pierce the corporate veil and go

after individual partners except under extraordinary circumstances,’ said Lynn

“In 1990, prior to the advent of limited-liability partnerships, the accounting firm

of Laventhol & Horwath filed for Chapter 11 bankruptcy-court protection, in part

due to lawsuits over questionable accounting. The firm’s assets were insufficient

Analysis Case

1. In looking at the financial statements of a partnership, a number of obvious

differences can be spotted in comparison to the financial statements of a

corporation. For example, in looking at this set of statements, the following

differences can be noted:

The balance sheet shows “partners’ (deficiency) capital” rather than

stockholders’ equity.

2. There is a considerable amount of information provided in the notes to the

financial statements about the unique characteristics of a limited partnership:

Note 1 – Organization and Summary of Significant Accounting Policies

discusses the creation and structure of this limited partnership under the

heading “Organization.”

In addition, in Item 5 (page 5), which precedes the financial statements,

disclosures are provided related to the market for partnership interests. Because

the partnership’s “shares” are not publicly traded, an individual investor may not

be able to sell his/her limited partner interest in the partnership.

Communication Case

The bankruptcy of Laventhol & Horwath was one of the main reasons for the

creation of the limited liability partnership business structure. As a general

partnership, the litigation losses of this partnership that arose from poor

accounting and auditing practices fell on all partners and not just on those

involved. Partners were required to make contributions from their own personal

Excel Case

There are a number of different ways that a spreadsheet could be created to solve

this particular problem. Here is one possible approach:

—Create Column Headings:

In Cell A1, enter label text “Partner”.

In Cell B1, enter label text “Capital Balance”.

—Enter Account Information for each partner:

In Cell A2, enter label text “Wilson.” In Cell B2, enter Wilson’s Capital Balance of

$200,000 and, in Cell C2, enter 40% as share of profit and loss.

—Enter the amounts on which to base the calculations for each partner:

—Calculate Initial Loss Share:

B9 respectively and the reference to Cell C2 will change to C3 and C4 respectively

in order to adjust for the new cell position. The change to C3 and C4 is correct

because those are the individual profit and loss percentages. No change, though,

—Calculate the Partners’ Share of any Subsequent Losses:

—Calculate the Remaining Capital Balance:

To calculate the Remaining Capital Balance, the beginning Capital Balance must

be reduced by the Initial Loss Share and Subsequent Loss Share.

100%.

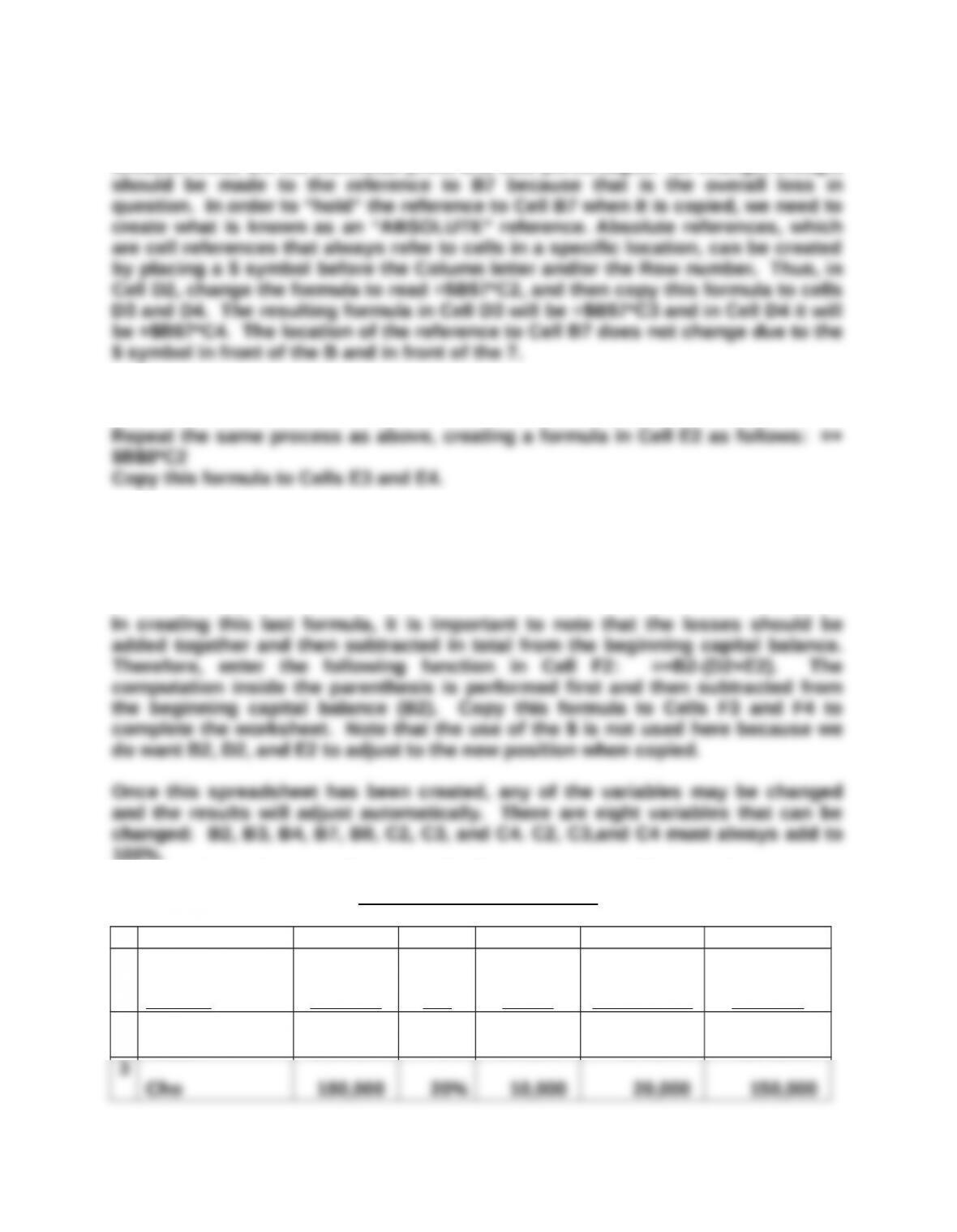

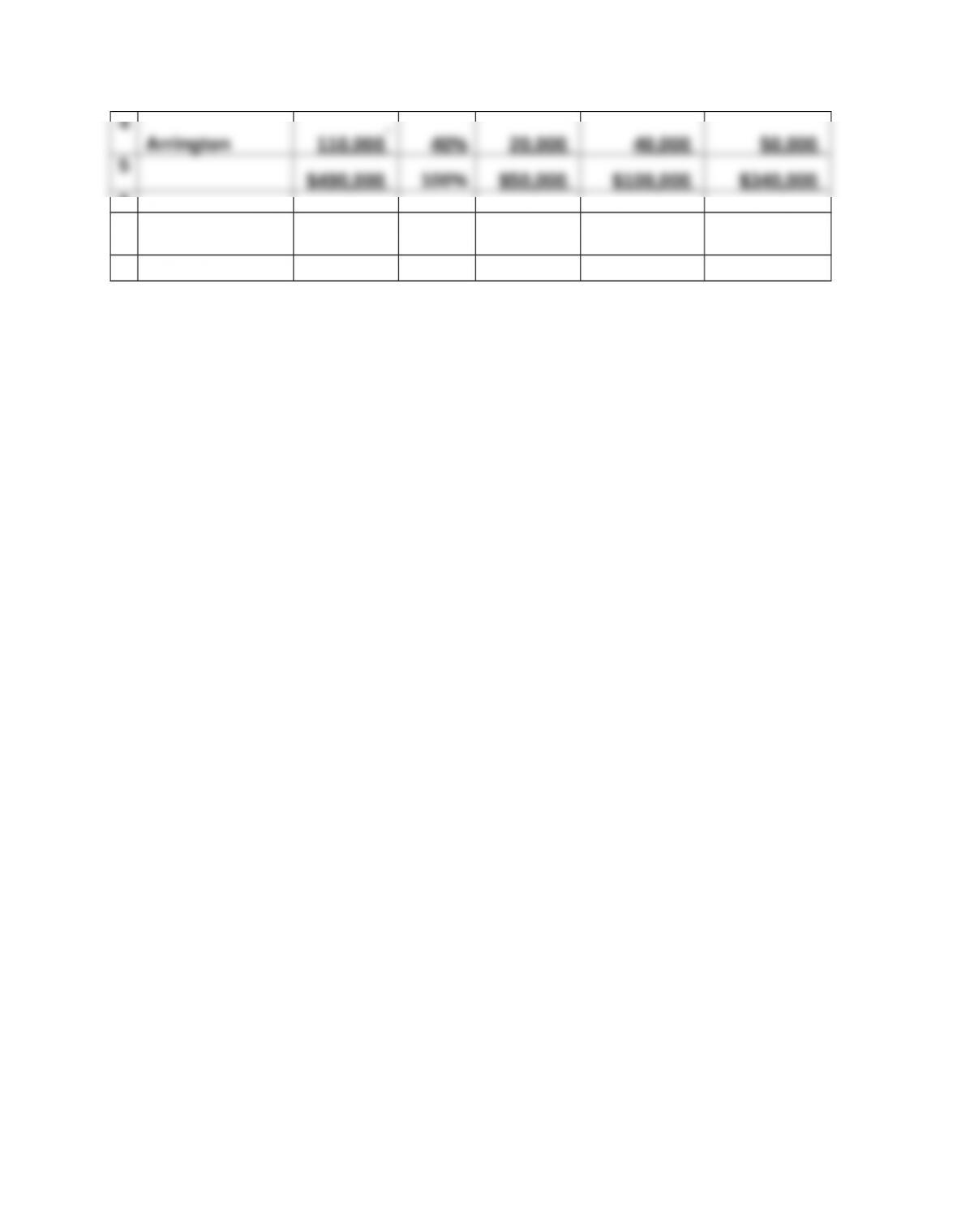

Spreadsheet to Determine the Remaining Capital Balances for

Wilson, Cho, and Arrington

A B C D E F

1

Partner

Capital

Balance

Share

P/L

Initial

Loss

Share

Subsequent

Loss Share

Remaining

Balance

2

Wilson $200,000 40% $20,000 $40,000 $140,000

6

7 Losses during

liquidation

50,000

8Final losses 100,000