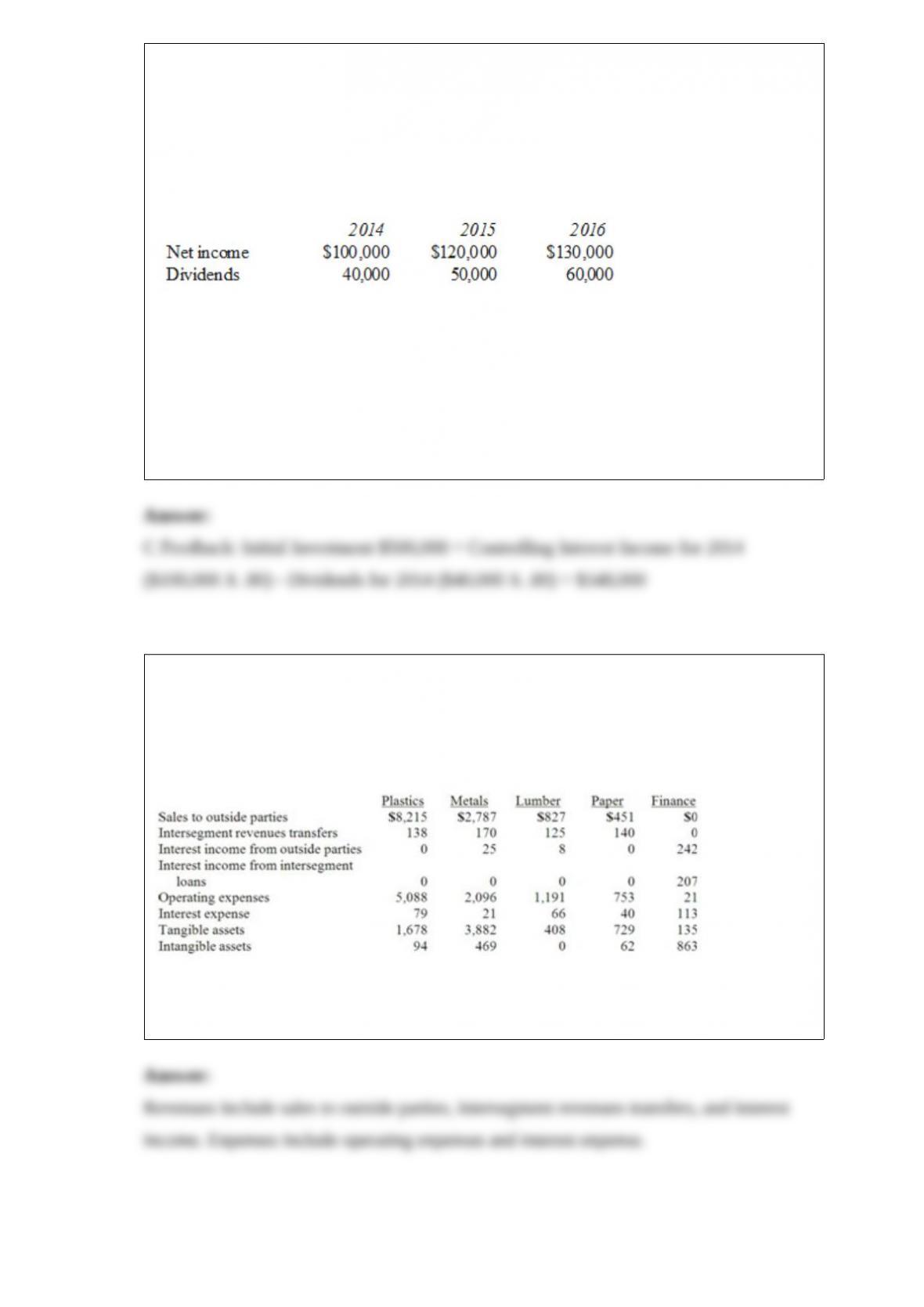

1) Pell Company acquires 80% of Demers Company for $500,000 on January 1, 2014.

Demers reported common stock of $300,000 and retained earnings of $210,000 on that

date. Equipment was undervalued by $30,000 and buildings were undervalued by

$40,000, each having a 10-year remaining life. Any excess consideration transferred

over fair value was attributed to goodwill with an indefinite life. Based on an annual

review, goodwill has not been impaired.

Demers earns income and pays dividends as follows:

Assume the PARTIAL EQUITY method is applied.

Compute Pell’s investment in Demers at December 31, 2014.

A) $625,000.

B) $574,400.

C) $548,000.

D) $542,400.

E) $532,000.

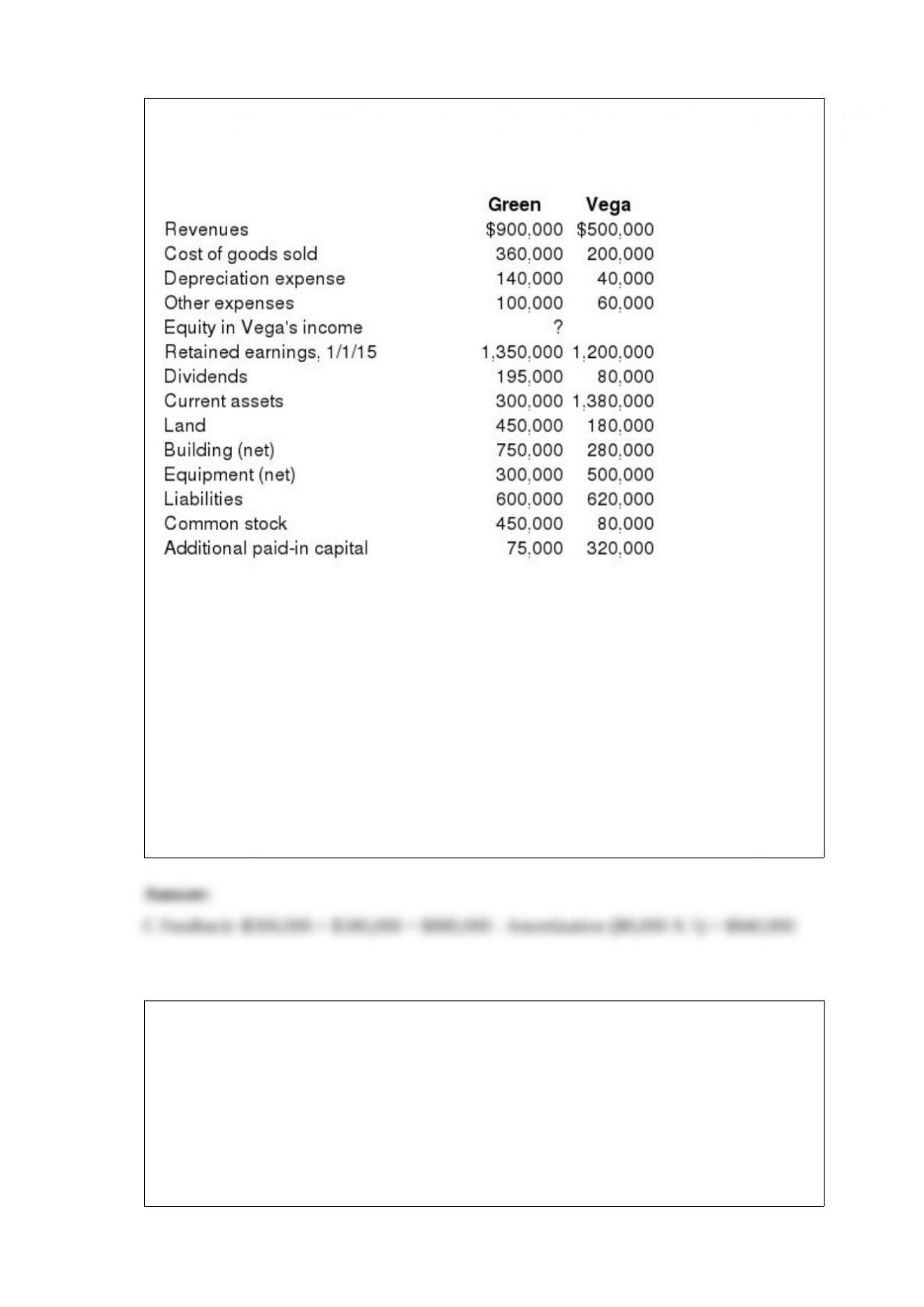

2) Faru Co. identified five industry segments: (1) plastics, (2) metals, (3) lumber, (4)

paper, and (5) finance. Each of these segments had been consolidated appropriately by

the company in producing its annual financial statements. Information describing each

segment is presented below (in thousands).

Prepare the profit or loss test and determine which of these segments was separately

reportable.

3) A foreign subsidiary was acquired on January 1, 2013. Determine the exchange rate

used to restate the following accounts at December 31, 2013. Land was purchased on

October 1, 2013. Relevant exchange dates follow:

(A) January 1, 2013

(B) October 1, 2013

(C) December 31, 2013

(D) Average, 2013

(E) Composite, using multiple dates.

Identify the exchange rate used to translate items 1-5 when the functional currency is

the foreign currency:

____ 1> Land.

____ 2> Equipment.

____ 3> Bonds payable.

____ 4> Common stock.

____ 5> Retained earnings.

Identify the exchange rate used to remeasure the items 6-10 when the functional

currency is the U.S. dollar:

____ 6> Land.

____ 7> Equipment.

____ 8> Bonds payable.

____ 9> Common stock.

____ 10> Retained earnings.

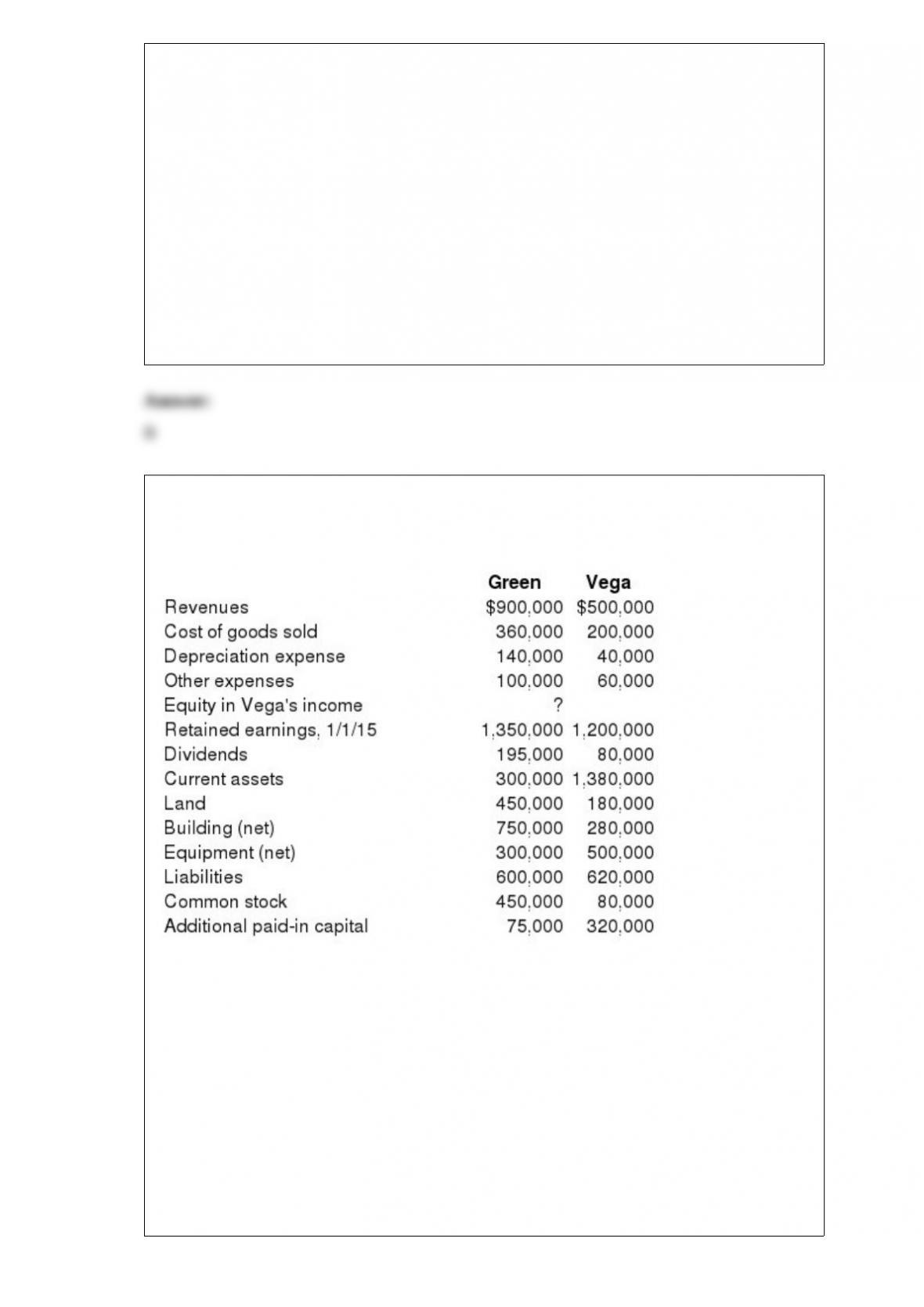

5) Following are selected accounts for Green Corporation and Vega Company as of

December 31, 2015. Several of Green’s accounts have been omitted.

Green acquired 100% of Vega on January 1, 2011, by issuing 10,500 shares of its $10

par value common stock with a fair value of $95 per share. On January 1, 2011, Vega’s

land was undervalued by $40,000, its buildings were overvalued by $30,000, and

equipment was undervalued by $80,000. The buildings have a 20-year life and the

equipment has a 10-year life. $50,000 was attributed to an unrecorded trademark with a

16-year remaining life. There was no goodwill associated with this investment.

Compute the December 31, 2015, consolidated equipment.

A) $800,000.

B) $808,000.

C) $840,000.

D) $760,000.

E) $848,000.

6) Wilson owned equipment with an estimated life of 10 years when it was acquired for

an original cost of $80,000. The equipment had a book value of $50,000 at January 1,

2012. On January 1, 2012, Wilson realized that the useful life of the equipment was

longer than originally anticipated, at ten remaining years.

On April 1, 2012 Simon Company, a 90% owned subsidiary of Wilson Company,

bought the equipment from Wilson for $68,250 and for depreciation purposes used the

estimated remaining life as of that date. The following data are available pertaining to

Simon’s income and dividends:

Compute the amortization of gain through a depreciation adjustment for 2012 for

consolidation purposes.

A) $1,950.

B) $1,825.

C) $1,500.

D) $2,000.

E) $5,250.

7) Knight Co. owned 80% of the common stock of Stoop Co. Stoop had 50,000 shares

of $5 par value common stock and 2,000 shares of preferred stock outstanding. Each

preferred share received an annual per share dividend of $10 and is convertible into

four shares of common stock. Knight did not own any of Stoop’s preferred stock. Stoop

also had 600 bonds outstanding, each of which is convertible into ten shares of common

stock. Stoop’s annual after-tax interest expense for the bonds was $22,000. Knight did

not own any of Stoop’s bonds. Stoop reported income of $300,000 for 20

Stoop’s diluted earnings per share (rounded) is calculated to be

A) $5.62.

B) $3.26.

C) $3.11.

D) $5.03.

E) $4.28.

8) Pell Company acquires 80% of Demers Company for $500,000 on January 1, 2014.

Demers reported common stock of $300,000 and retained earnings of $210,000 on that

date. Equipment was undervalued by $30,000 and buildings were undervalued by

$40,000, each having a 10-year remaining life. Any excess consideration transferred

over fair value was attributed to goodwill with an indefinite life. Based on an annual

review, goodwill has not been impaired.

Demers earns income and pays dividends as follows:

Assume the EQUITY METHOD is applied.

Compute the non-controlling interest in Demers at December 31, 2016.

A) $107,800.

B) $140,000.

C) $165,200.

D) $160,800.

E) $146,800.

9) Yukon Co. acquired 75% percent of the voting common stock of Ontario Corp. on

January 1, 2013. During the year, Yukon made sales of inventory to Ontario. The

inventory cost Yukon $260,000 and was sold to Ontario for $390,000. Ontario still had

$60,000 of the goods in its inventory at the end of the year. The amount of unrealized

intra-entity profit that should be eliminated in the consolidation process at the end of

2013 is

A) $ 15,000.

B) $ 20,000.

C) $ 32,500.

D) $ 30,000.

E) $110,000.

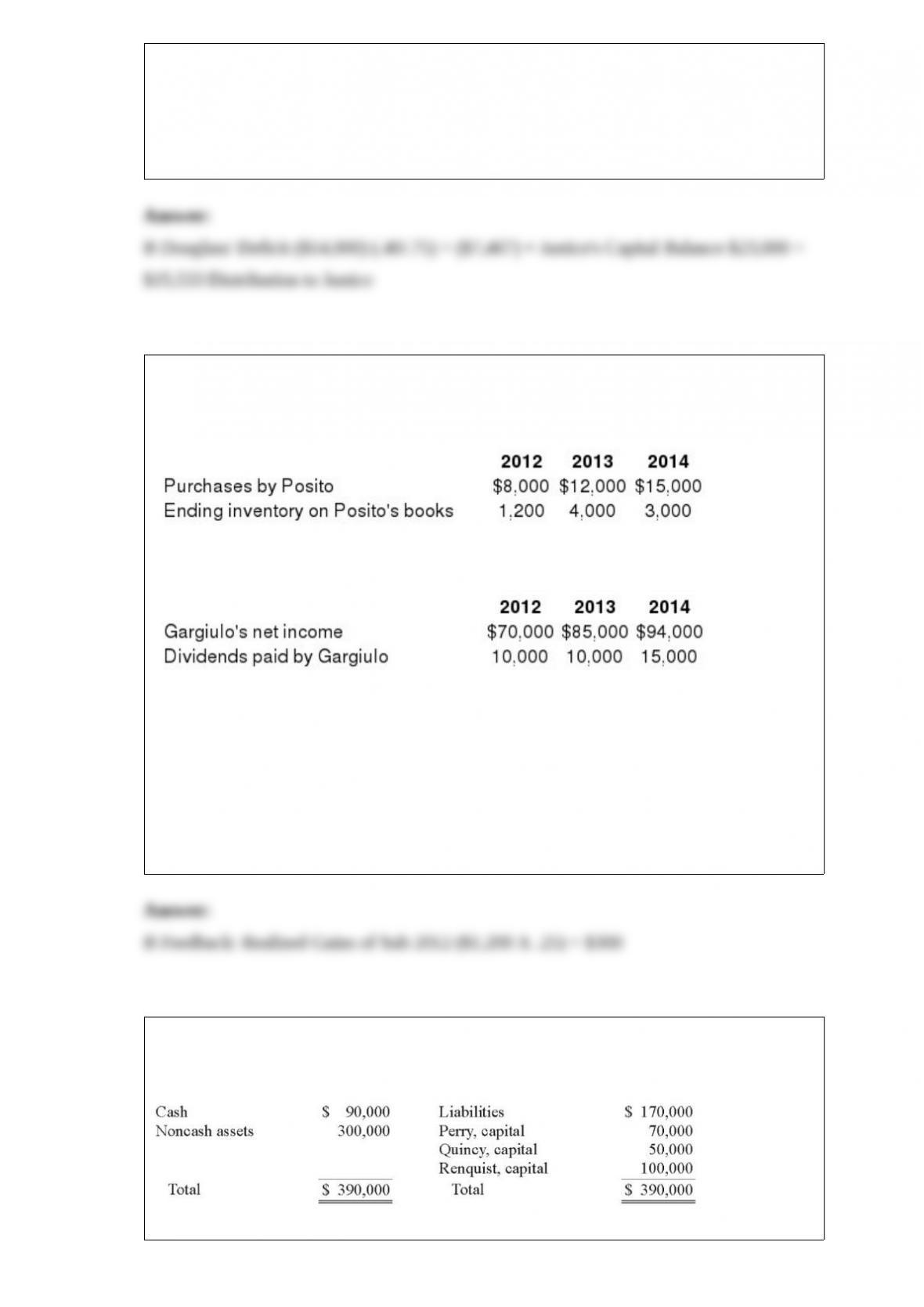

10) A local partnership was in the process of liquidating and reported the following

capital balances:

Douglass indicated that the $14,000 deficit would be covered by a forthcoming

contribution. However, the two remaining partners asked to receive the $31,000 that

was then in the cash account.

How much of this money should Justice receive?

A.$15,467.

B.$15,533.

C.$17,333.

D.$16,533.

E.$15,867.

11) Gargiulo Company, a 90% owned subsidiary of Posito Corporation, sells inventory

to Posito at a 25% profit on selling price. The following data are available pertaining to

intra-entity purchases. Gargiulo was acquired on January 1, 2012.

Assume the equity method is used. The following data are available pertaining to

Gargiulo’s income and dividends.

For consolidation purposes, what amount would be debited to January 1 retained

earnings for the 2013 consolidation worksheet entry with regard to the unrealized gross

profit of the 2012 intra-entity transfer of merchandise?

A) $ 240.

B) $ 300.

C) $2,000.

D) $1,600.

E) $ 270.

12) The following account balances were available for the Perry, Quincy, and Renquist

partnership just before it entered liquidation:

Included in Perry’s capital balance is a $20,000 partnership loan owed to Perry. Perry,

Quincy, and Renquist shared profits and losses in a ratio of 2:4:4. Liquidation expenses

were expected to be $15,000.

All partners were solvent.

What would be the minimum amount for which the noncash assets must have been sold,

in order for Quincy to receive some cash from the liquidation?

A.any amount in excess of $170,000.

B.any amount in excess of $190,000.

C.any amount in excess of $260,000.

D.any amount in excess of $280,000.

E.any amount in excess of $300,000.

13) Following are selected accounts for Green Corporation and Vega Company as of

December 31, 2015. Several of Green’s accounts have been omitted.

Green acquired 100% of Vega on January 1, 2011, by issuing 10,500 shares of its $10

par value common stock with a fair value of $95 per share. On January 1, 2011, Vega’s

land was undervalued by $40,000, its buildings were overvalued by $30,000, and

equipment was undervalued by $80,000. The buildings have a 20-year life and the

equipment has a 10-year life. $50,000 was attributed to an unrecorded trademark with a

16-year remaining life. There was no goodwill associated with this investment.

Compute the December 31, 2015, consolidated additional paid-in capital.

A) $ 210,000.

B) $ 75,000.

C) $1,102,500.

D) $ 942,500.

E) $ 525,000.

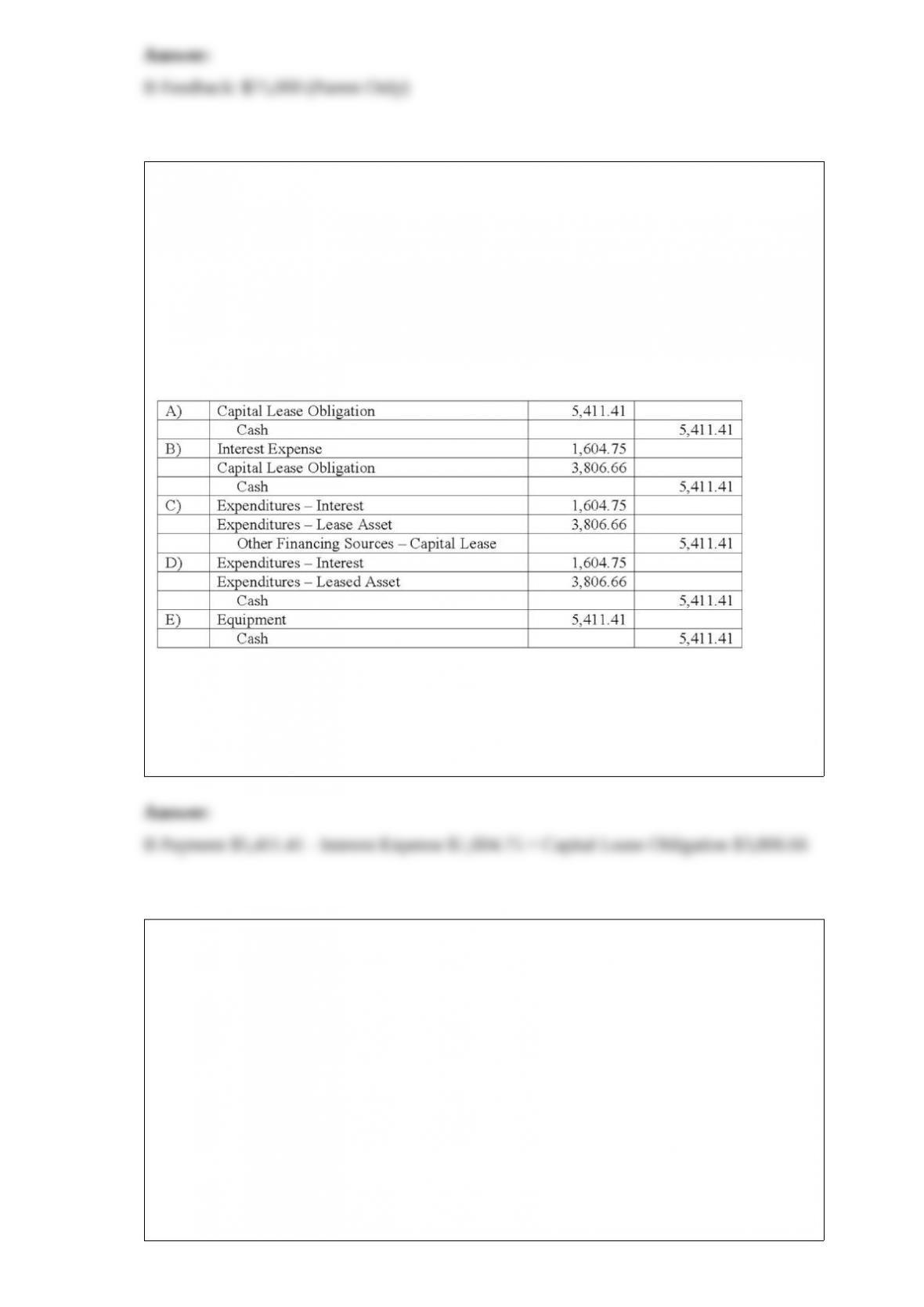

14) A five-year lease is signed by the City of Wachovia for equipment with a seven-year

life. The asset will be returned to the lessor at the end of the lease. The present value of

the lease is $20,000, and annual payments of $5,411.41 are payable beginning on the

date the lease is signed. The interest portion of the second payment is $1,604.75. The

equipment is to be used in City Hall and was purchased from appropriated funds of the

General Fund.

What entry should be made for the government-wide financial statements one year from

the date the lease is signed?

A.Option A

B.Option B

C.Option C

D.Option D

E.Option E

15) Goehler, Inc. acquires all of the voting stock of Kenneth, Inc. on January 4, 2012, at

an amount in excess of Kenneth’s fair value. On that date, Kenneth has equipment with

a book value of $90,000 and a fair value of $120,000 (10-year remaining life). Goehler

has equipment with a book value of $800,000 and a fair value of $1,200,000 (10-year

remaining life). On December 31, 2013, Goehler has equipment with a book value of

$975,000 but a fair value of $1,350,000 and Kenneth has equipment with a book value

of $105,000 but a fair value of $125,000.

If Goehler applies the partial equity method in accounting for Kenneth, what is the

consolidated balance for the Equipment account as of December 31, 2013?

A) $1,080,000.

B) $1,104,000.

C) $1,100,000.

D) $1,468,000.

E) $1,475,000.

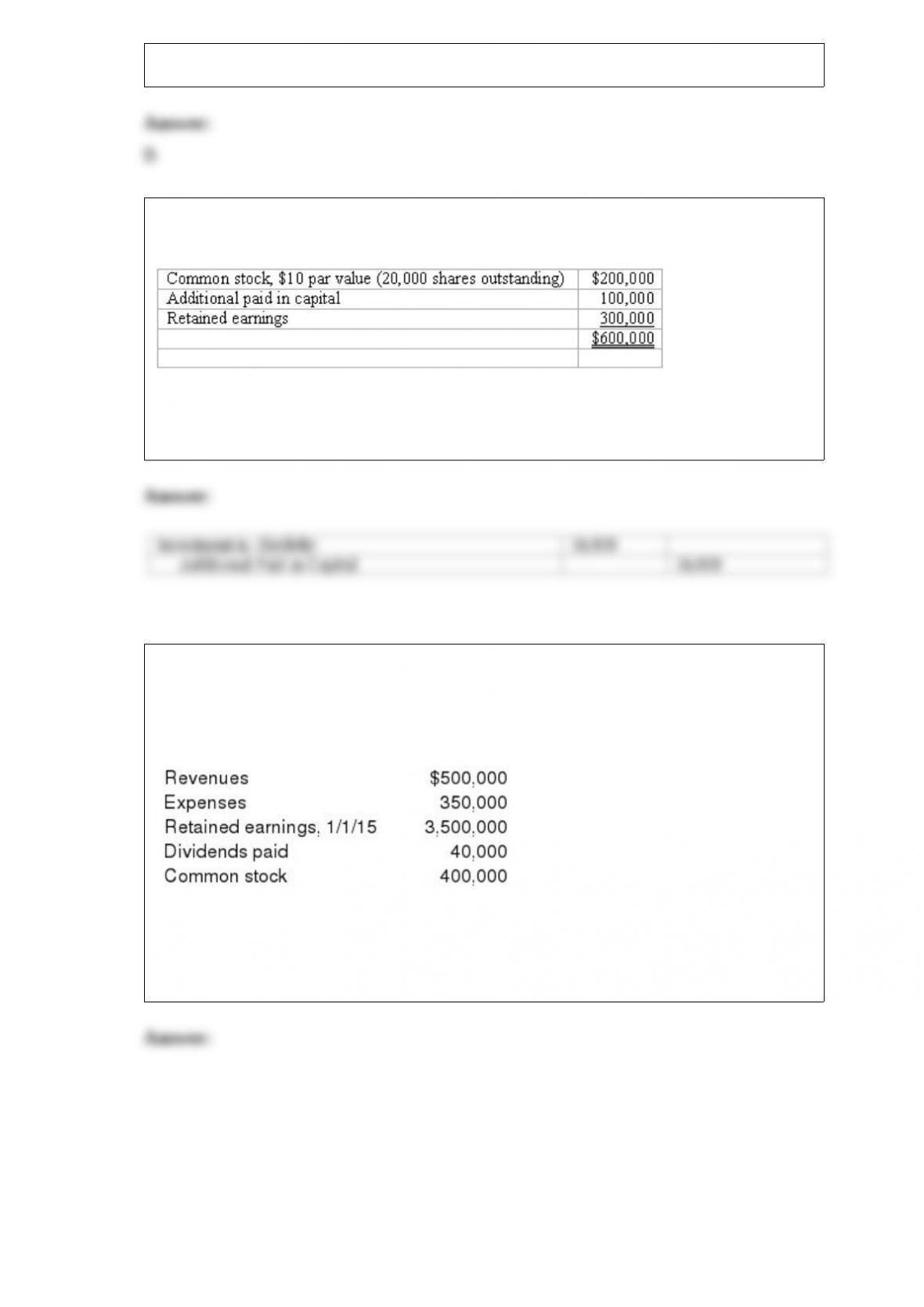

16) Panton, Inc. acquired 18,000 shares of Glotfelty Corp. several years ago. At the

present time, Glotfelty is reporting the following stockholders’ equity:

Glotfelty issues

5,000 shares of previously unissued stock to the public for $40 per share. None of this

stock is purchased by Panton.

Prepare Panton’s journal entry to recognize the impact of this transaction.

17) McLaughlin, Inc. acquires 70 percent of Ellis Corporation on September 1, 2014,

and an additional 10 percent on November 1, 2015. Annual amortization of $8,400

attributed to the controlling interest relates to the first acquisition. Ellis reports the

following figures for 2015:

Without regard for this investment, McLaughlin earns $480,000 in net income

($840,000 revenues less $360,000 expenses; incurred evenly through the year) during

2015. Required: Prepare a schedule of consolidated net income and apportionment to

non-controlling and controlling interests for 2015.

18) For the month of December 2013, patient charges at Northfield Hospital (a

not-for-profit hospital) were $2,720,000. Third-party payors were billed $1,800,000.

In this month, there were several patients that had no health insurance and due to their

low income level, the hospital decided that $85,000 of receivables would not be

collectible.

Required:

Prepare the necessary journal entry to reflect the decision to consider the $85,000 as

charity care.

19) On August 21, 2013, Fred City transferred $100,000 to the School System to cover

repairs to a school building.

Required:

Prepare all the required journal entries and identify the fund in which each entry was

recorded for the Fund Financial Statements.

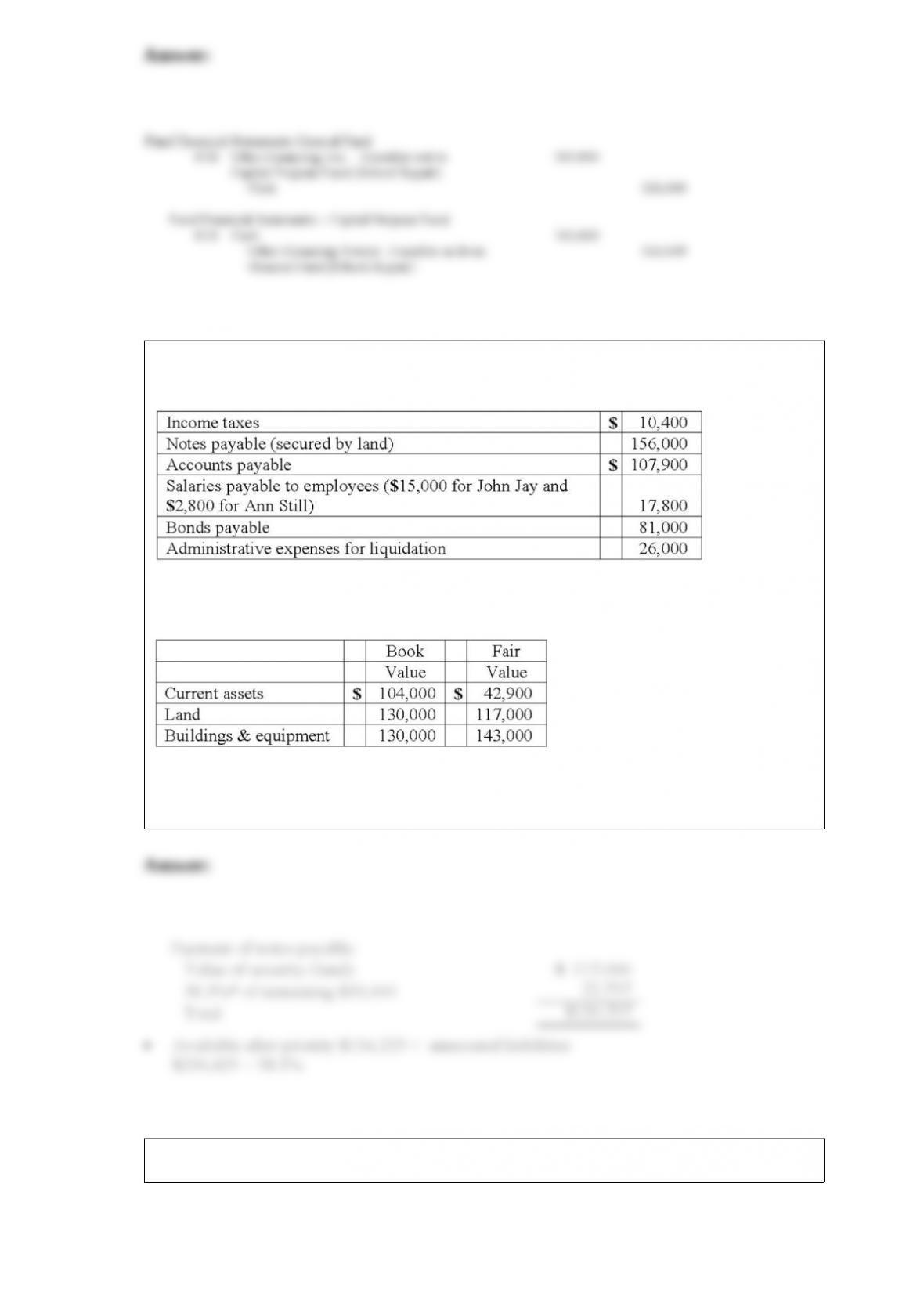

20) A company that was to be liquidated had the following liabilities:

The company had the following assets:

Total payment on notes payable is calculated to be what amount? (Round the payout

percentage to one decimal place.)

21) Thomas Inc. had the following stockholders’ equity accounts as of January 1, 2013:

K

uried Co. acquired all of the voting common stock of Thomas on January 1, 2013, for

$20,656,000. The preferred stock remained in the hands of outside parties and had a fair

value of $3,060,000. A database valued at $656,000 was recognized and amortized over

five years. During 2013, Thomas reported earning $630,000 in net income and paid

$504,000 in total cash dividends. Kuried used the equity method to account for this

investment.

What is the amount of goodwill resulting from this acquisition?

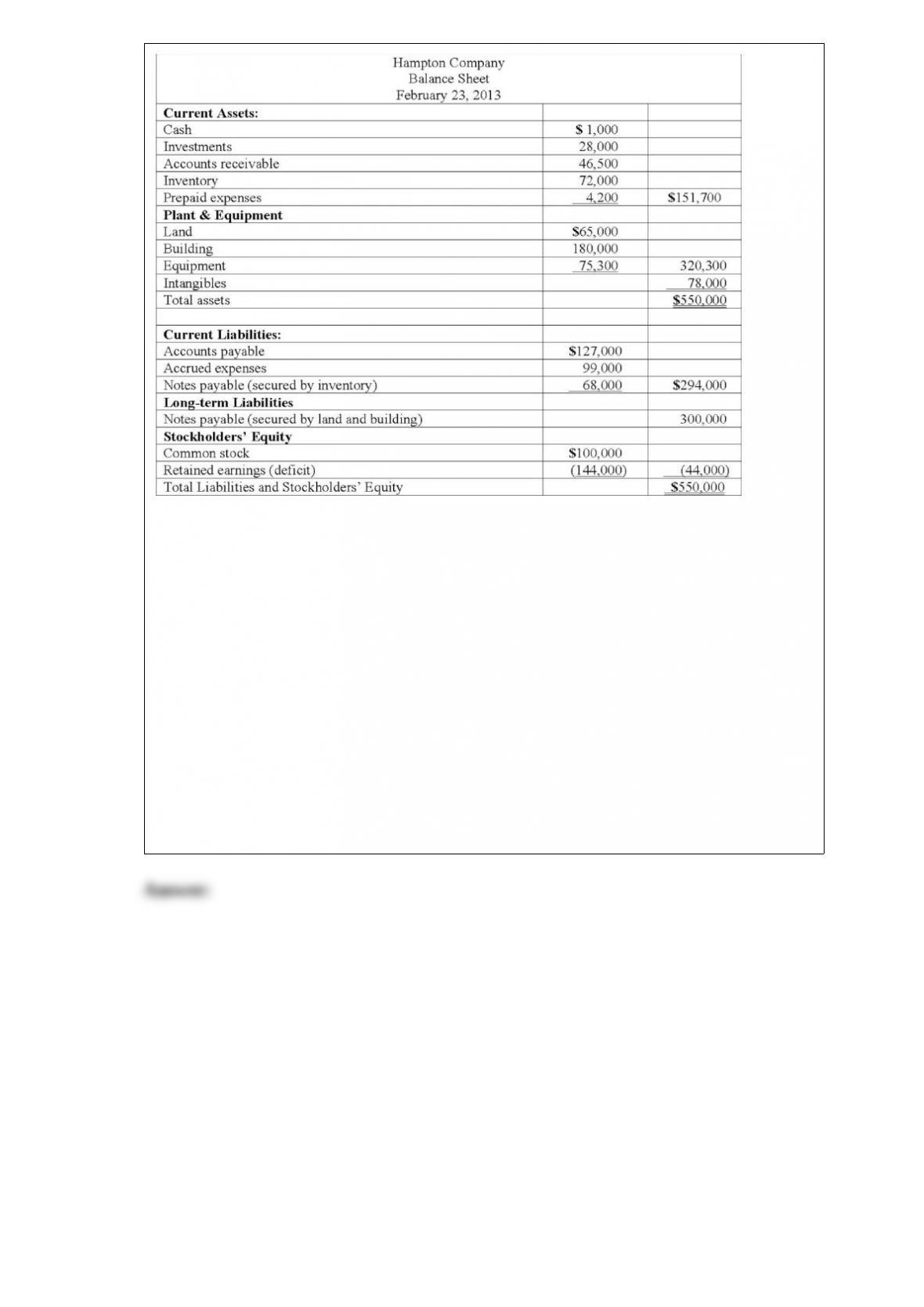

22) Hampton Company is trying to decide whether to seek liquidation or

reorganization. Hampton has provided the following balance sheet:

Additional information is as follows:

– The investments are currently worth $13,000.

– It is estimated that $32,000 of the accounts receivable are collectible.

– The inventory can be sold for $74,000.

– The prepaid expenses and the intangible assets have no net realizable value.

– The land and building are currently valued at $250,000.

– The equipment can be sold for $60,000.

– Administrative expenses (not yet recorded) are estimated to be $12,500.

– Accrued expenses include $17,000 of salaries payable ($11,000 to one employee and

$3,000 each to two other employees).

– Accrued expenses include $7,000 of unpaid payroll taxes.

Prepare a Statement of Financial Affairs.

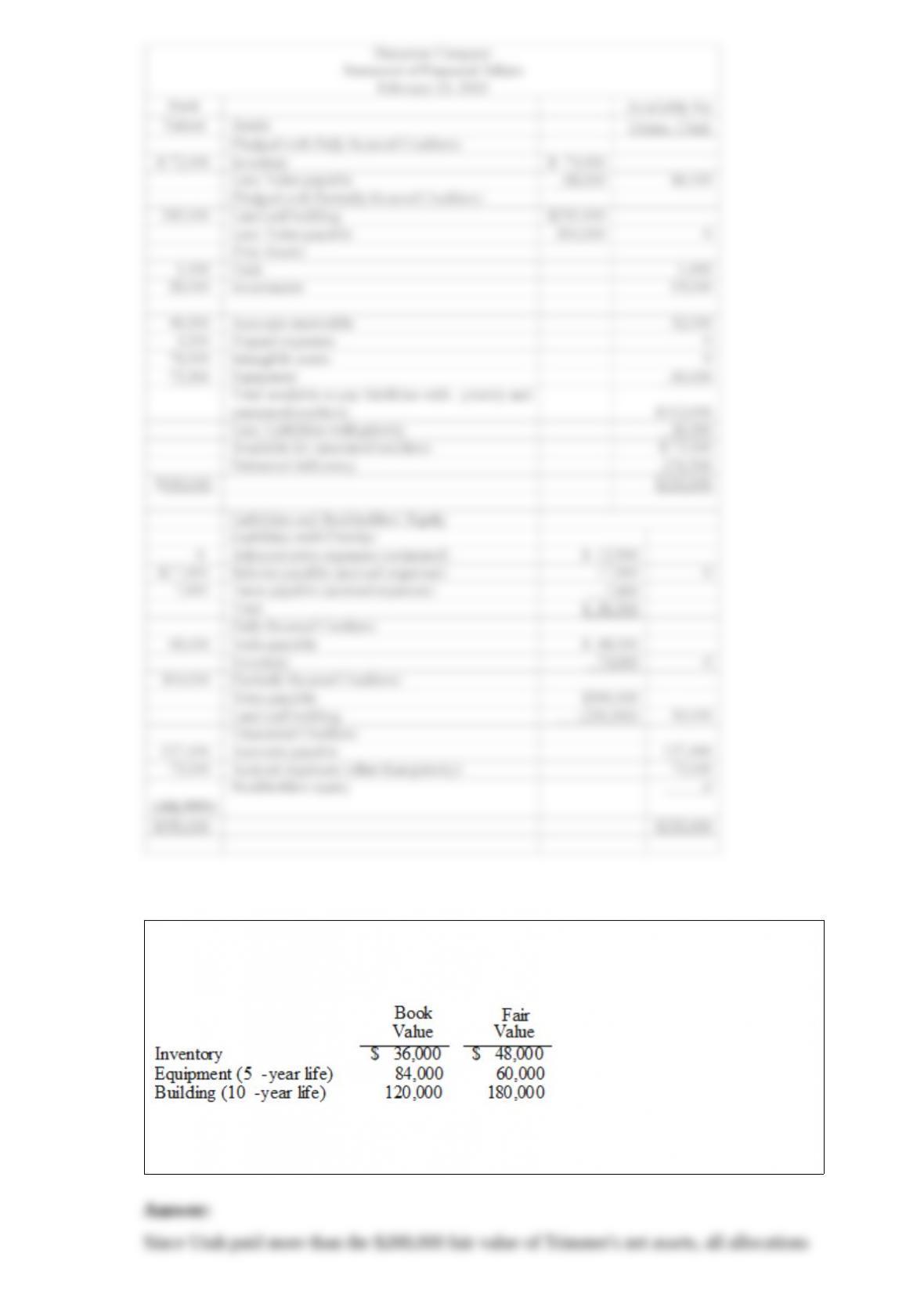

23) Utah Inc. acquired all of the outstanding common stock of Trimmer Corp. on

January 1, 2011. At that date, Trimmer owned only three assets and had no liabilities:

If Utah paid $300,000 in cash

for Trimmer, what allocation should have been assigned to the subsidiary’s Building

account and its Equipment account in a December 31, 2013 consolidation?