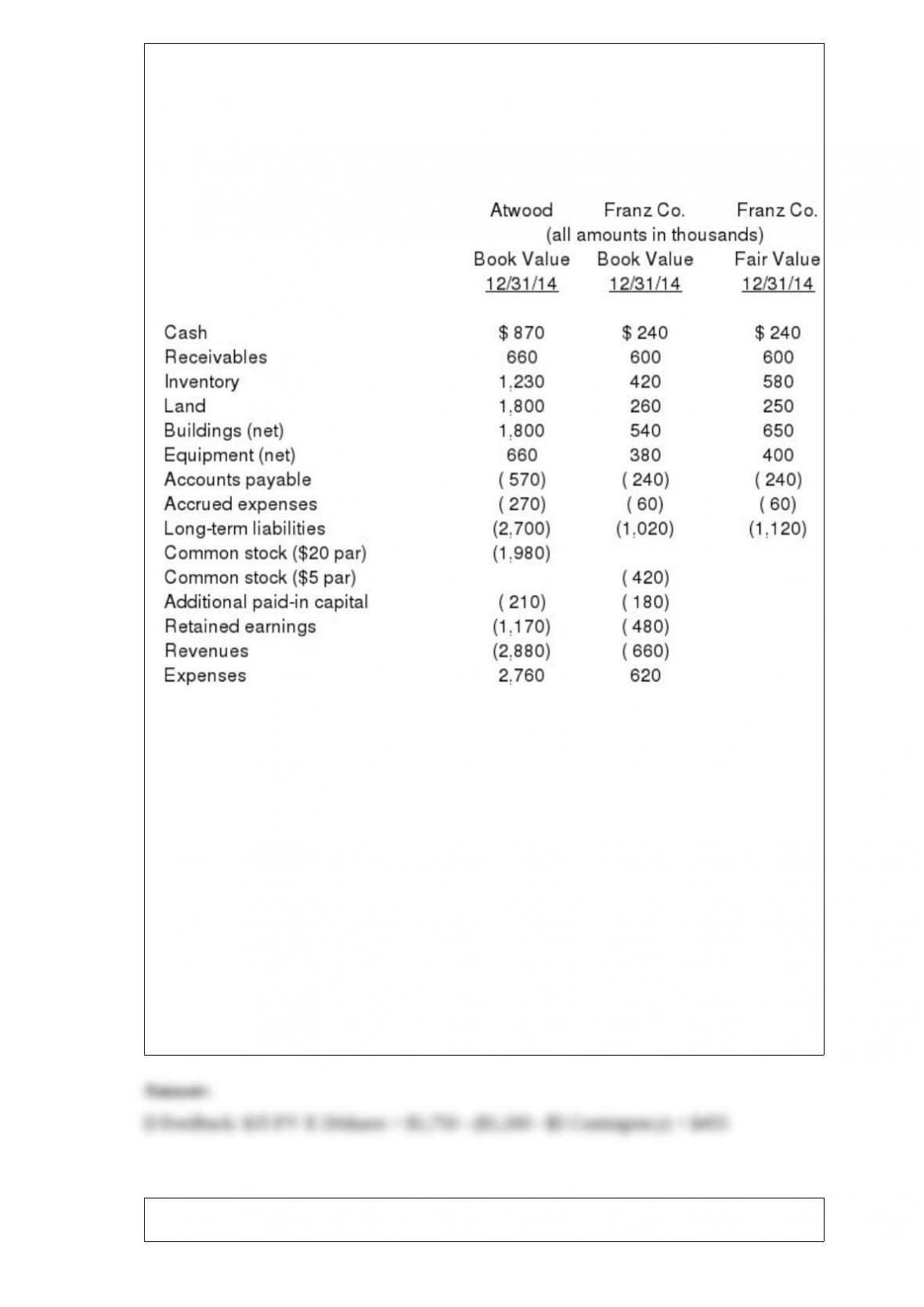

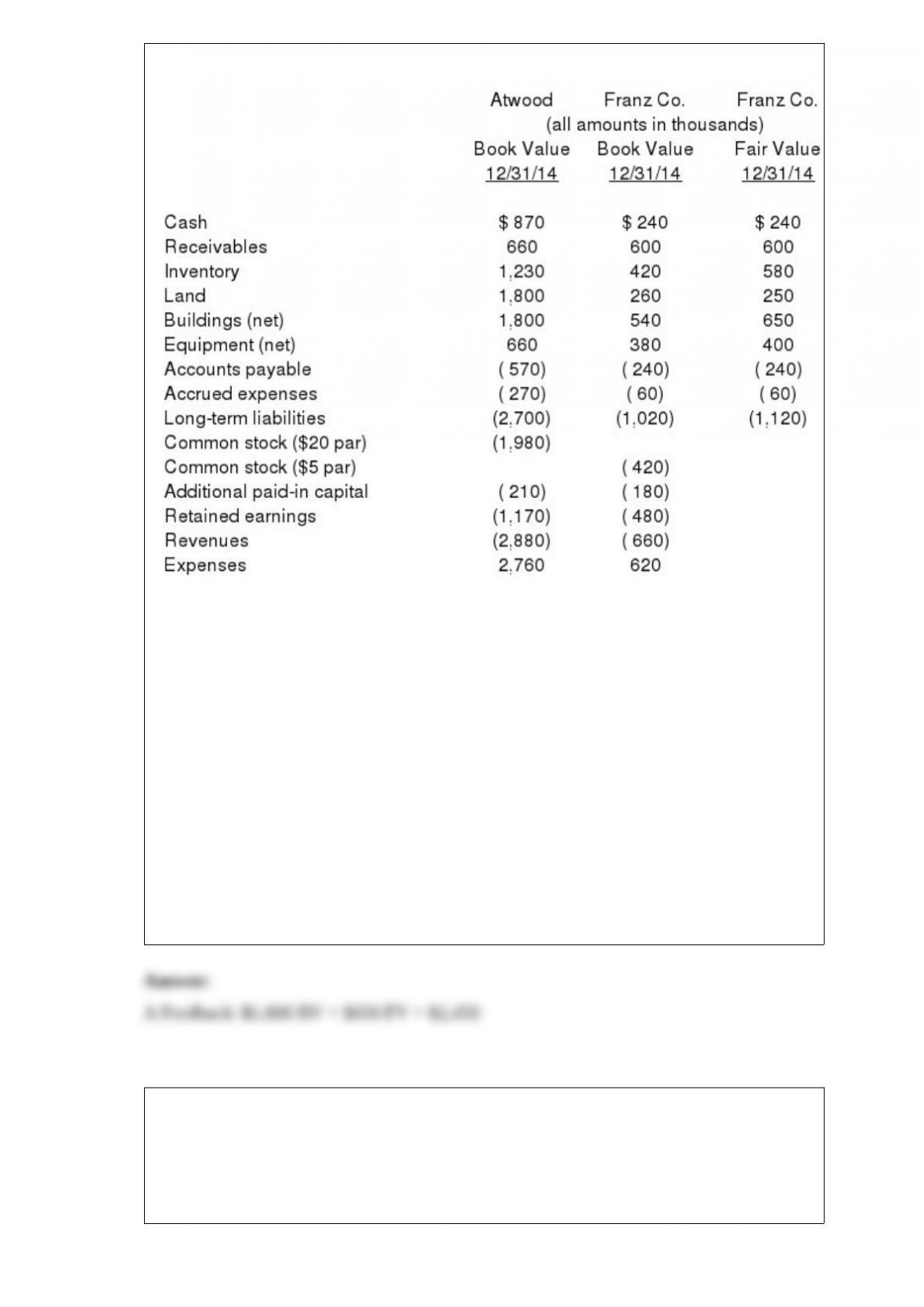

1) Presented below are the financial balances for the Atwood Company and the Franz

Company as of December 31, 2012, immediately before Atwood acquired Franz. Also

included are the fair values for Franz Company’s net assets at that date.

Note: Parenthesis indicate a credit balance

Assume a business combination took place at December 31, 2012. Atwood issued 50

shares of its common stock with a fair value of $35 per share for all of the outstanding

common shares of Franz. Stock issuance costs of $15 (in thousands) and direct costs of

$10 (in thousands) were paid to effect this acquisition transaction. To settle a difference

of opinion regarding Franz’s fair value, Atwood promises to pay an additional $5.2 (in

thousands) to the former owners if Franz’s earnings exceed a certain sum during the

next year. Given the probability of the required contingency payment and utilizing a 4%

discount rate, the expected present value of the contingency is $5 (in thousands).

Compute consolidated goodwill at date of acquisition.

A) $440.

B) $442.

C) $450.

D) $455.

E) $452.

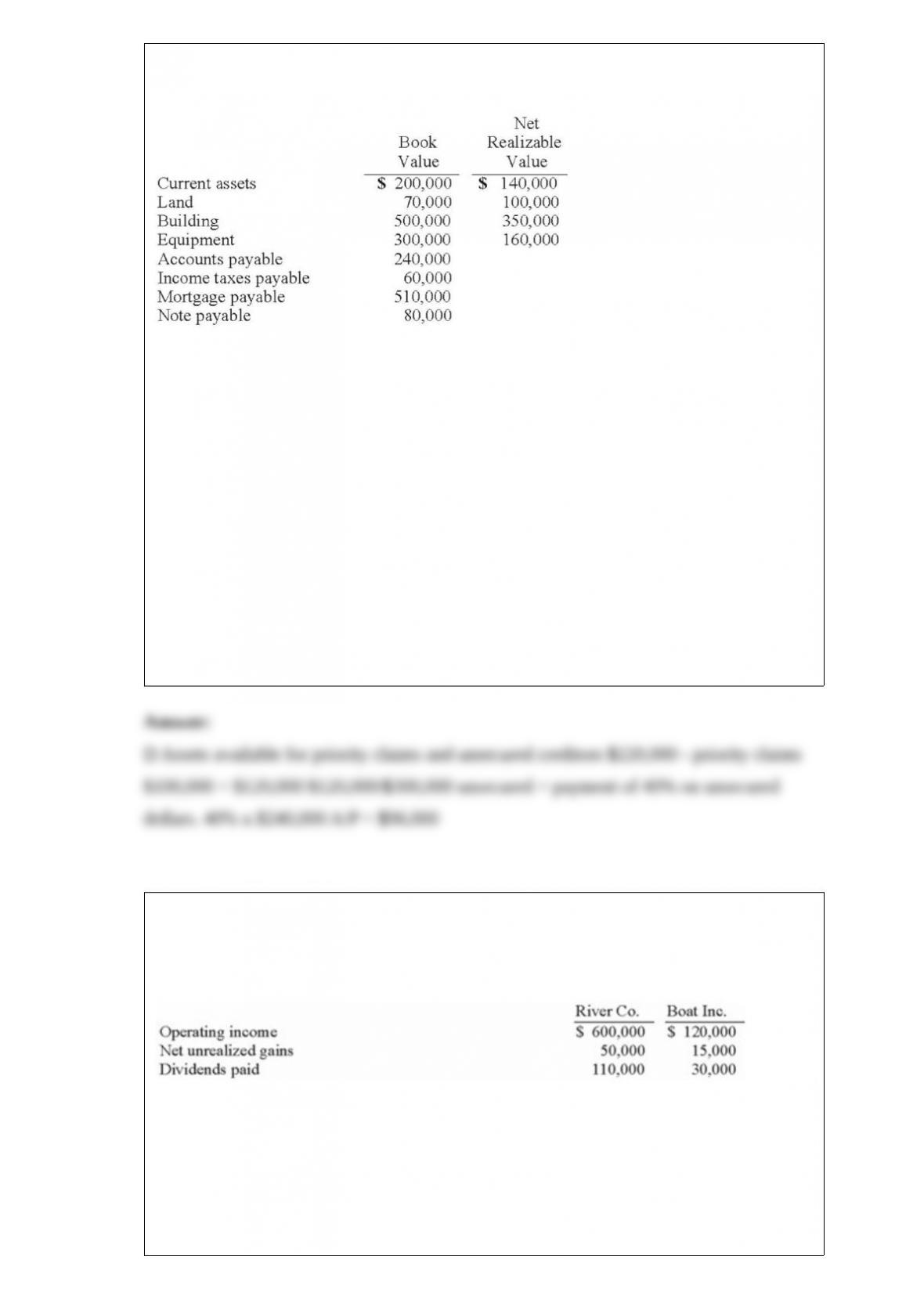

2) Quincy Corp., about to be liquidated, has the following amounts for its assets and

liabilities:

The mortgage is secured by the land and building, and the note payable is secured by

the equipment. Quincy expects that the expenses of administering the liquidation will

total $40,000.

How much should Quincy expect to pay on the accounts payable?

A.$240,000.

B.$128,000.

C.$120,000.

D.$96,000.

E.$146,000.

3) River Co. owned 80% of Boat Inc. The two companies filed a consolidated income

tax return and River used the initial value method to account for the investment. The

following information was available from the two companies’ financial statements:

Operating income included net unrealized gains, which are associated with transfers of

inventories between the two companies, but it did not include dividends received from a

subsidiary. The income tax rate was 30%.

What was the amount of income tax expense that should have been assigned to Boat

using the percentage allocation method?

A.$31,500

B.$32,750

C.$36,000

D.$32,660

E.$30,390

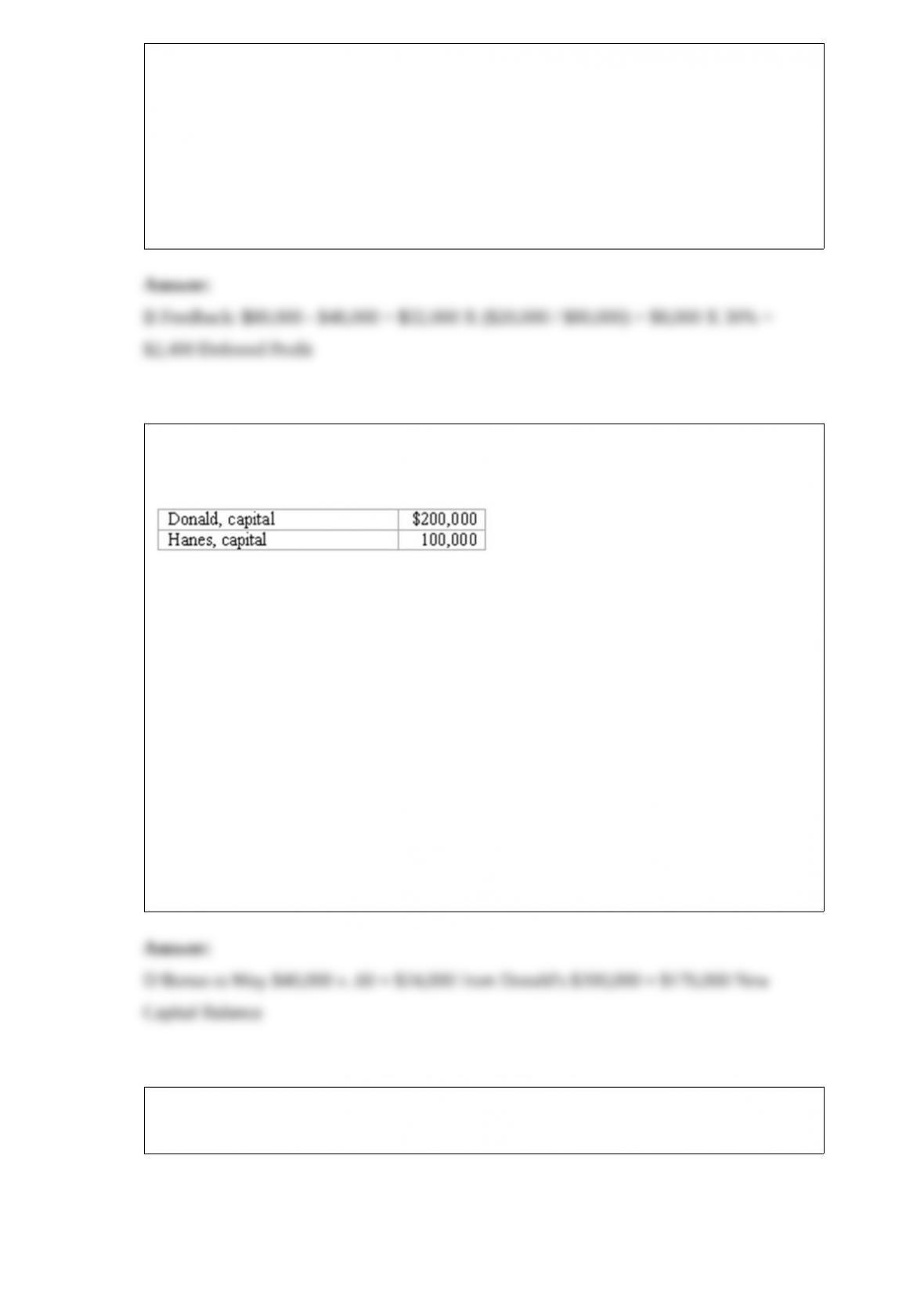

4) The capital account balances for Donald & Hanes LLP on January 1, 2013, were as

follows:

Donald and Hanes shared net income and losses in the ratio of 3:2, respectively. The

partners agreed to admit May to the partnership with a 35% interest in partnership

capital and net income. May invested $100,000 cash, and no goodwill was recognized.

What is the balance of Hanes’s capital account after the new partnership is created?

A.$84,000.

B.$100,000.

C.$140,000.

D.$176,000.

E.$200,000.

5) Cayman Inc. bought 30% of Maya Company on January 1, 2013 for $450,000. The

equity method of accounting was used. The book value and fair value of the net assets

of Maya on that date were $1,500,000. Maya began supplying inventory to Cayman as

follows:

Maya reported net income of $100,000 in 2013 and $120,000 in 2014 while paying

$40,000 in dividends each year.What is the amount of unrealized inventory profit to be

deferred on December 31, 2014?

A) $1,500.

B) $2,400.

C) $3,600.

D) $4,000.

E) $8,000.

6) The capital account balances for Donald & Hanes LLP on January 1, 2013, were as

follows:

Donald and Hanes shared net income and losses in the ratio of 3:2, respectively. The

partners agreed to admit May to the partnership with a 35% interest in partnership

capital and net income. May invested $100,000 cash, and no goodwill was recognized.

What is the balance of Donald’s capital account after the new partnership is created?

A.$84,000.

B.$100,000.

C.$140,000.

D.$176,000.

E.$200,000.

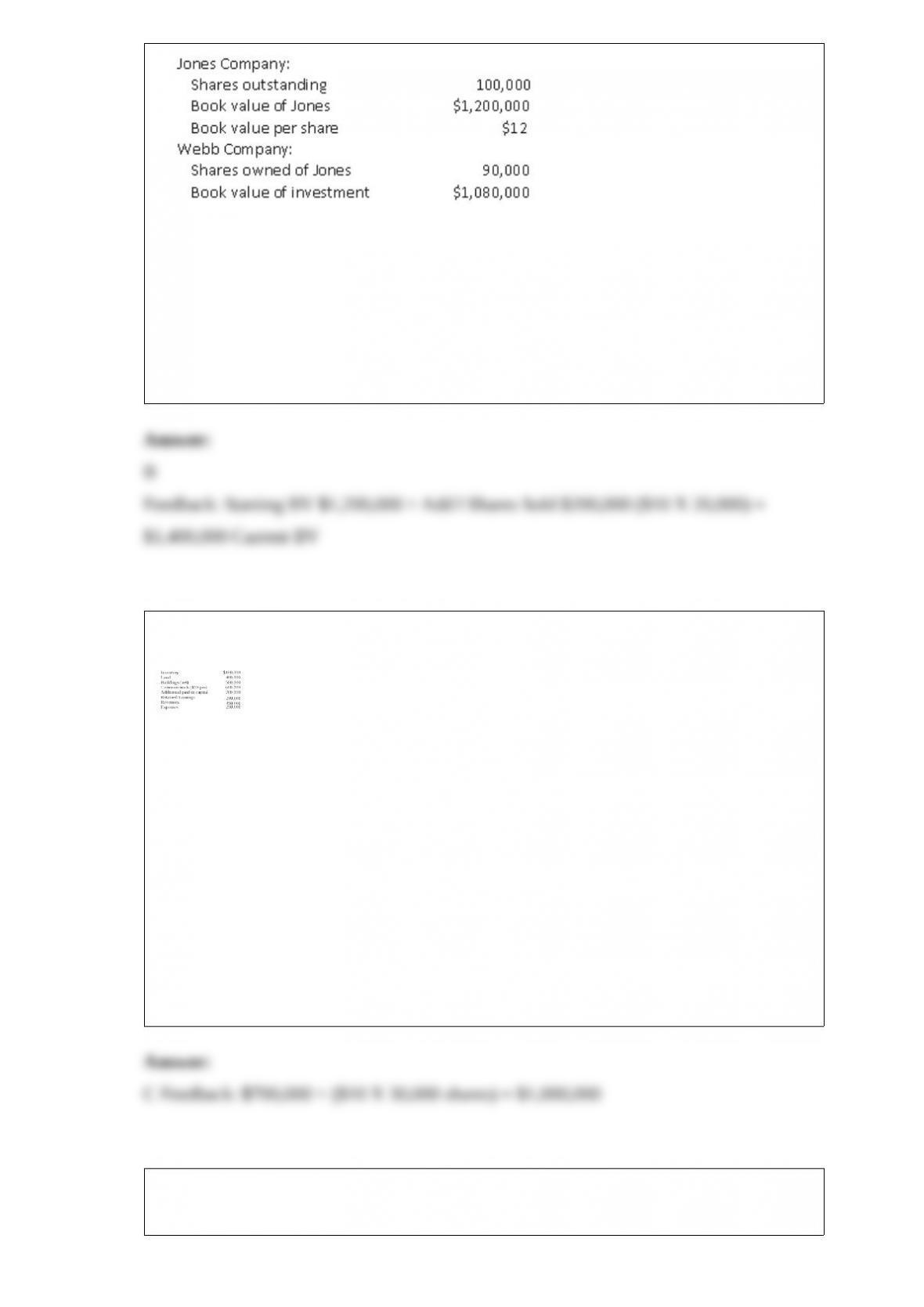

7) Webb Company owns 90% of Jones Company. The original balances presented for

Jones and Webb as of January 1, 2013, are as follows:

Jones sells 20,000 shares of

previously unissued shares of its common stock to outside parties for $10 per share.

What is the adjusted book value of Jones after the sale of the shares?

A) $ 200,000.

B) $1,400,000.

C) $1,280,000.

D) $1,050,000.

E) $1,440,000.

8) Carnes has the following account balances as of May 1, 2012 before an acquisition

transaction takes place.

The fair value of Carnes’ Land and Buildings are $650,000 and $550,000, respectively.

On May 1, 2012, Riley Company issues 30,000 shares of its $10 par value ($25 fair

value) common stock in exchange for all of the shares of Carnes’ common stock. Riley

paid $10,000 for costs to issue the new shares of stock. Before the acquisition, Riley

has $700,000 in its common stock account and $300,000 in its additional paid-in capital

account.

What will be Riley’s balance in its common stock account as a result of this acquisition?

A) $ 300,000.

B) $ 990,000.

C) $1,000,000.

D) $1,590,000.

E) $1,600,000.

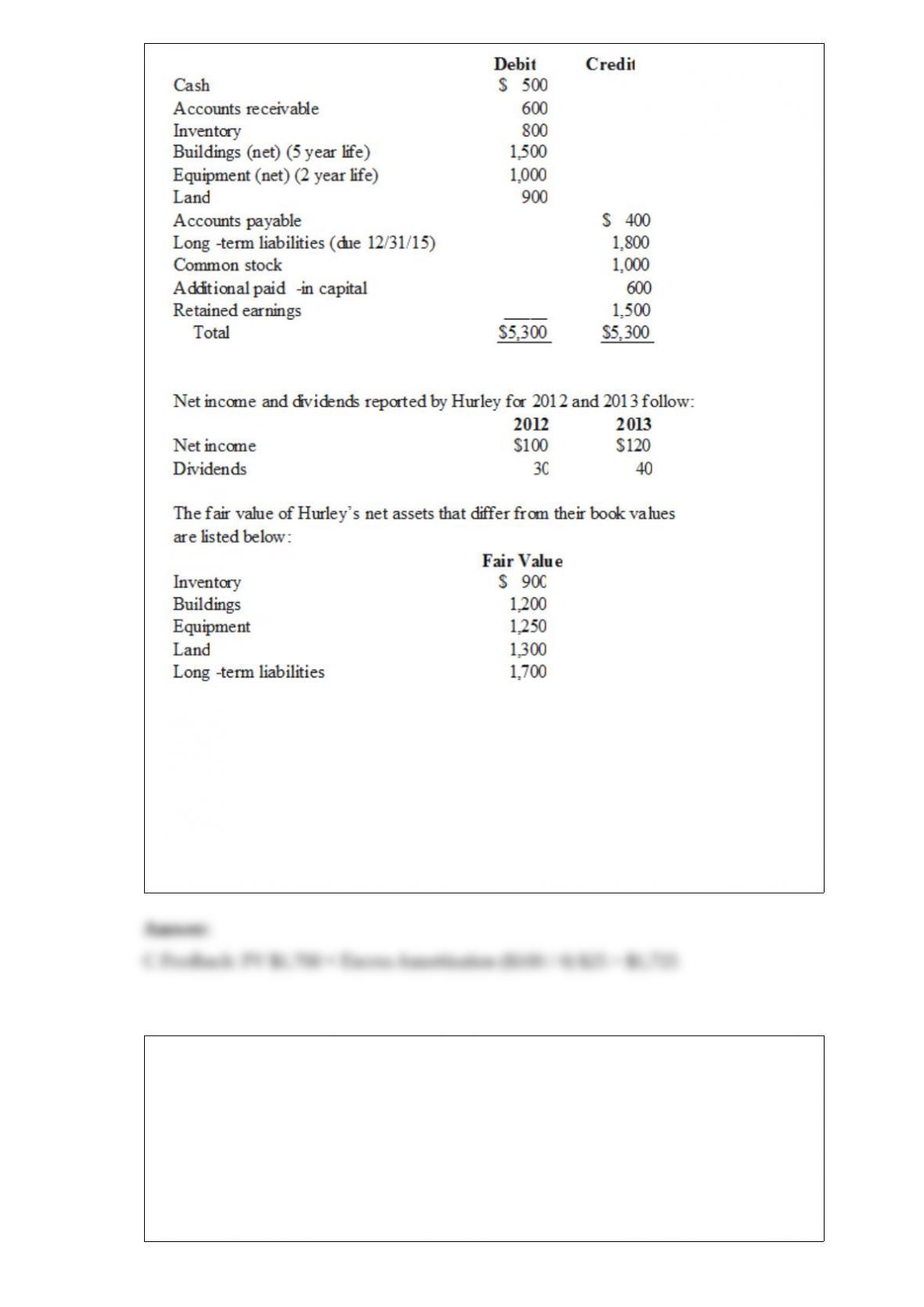

9) Perry Company acquires 100% of the stock of Hurley Corporation on January 1,

2012, for $3,800 cash. As of that date Hurley has the following trial balance;

Compute

the amount of Hurley’s long-term liabilities that would be reported in a December 31,

2012, consolidated balance sheet.

A) $1,800.

B) $1,700.

C) $1,725.

D) $1,675.

E) $3,500.

10) Pot Co. holds 90% of the common stock of Skillet Co. During 2013, Pot reported

sales of $1,120,000 and cost of goods sold of $840,000. For this same period, Skillet

had sales of $420,000 and cost of goods sold of $252,000.

Included in the amounts for Pot’s sales were Pot’s sales of merchandise to Skillet for

$140,000. There were no sales from Skillet to Pot. Intra-entity sales had the same

markup as sales to outsiders. Skillet still had 40% of the intra-entity sales as inventory

at the end of 2013. What are consolidated sales and cost of goods sold for 2013?

A) $1,400,000 and $ 952,000.

B) $1,400,000 and $ 966,000.

C) $1,540,000 and $1,078,000.

D) $1,400,000 and $1,022,000.

E) $1,540,000 and $1,092,000.

11) Clemente Co. owned all of the voting common stock of Snider Co. On January 2,

2012, Clemente sold equipment to Snider for $125,000. The equipment had cost

Clemente $140,000. At the time of the sale, the balance in accumulated depreciation

was $40,000. The equipment had a remaining useful life of five years and a $0 salvage

value. Straight-line depreciation is used by both Clemente and Snider.

At what amount should the equipment (net of depreciation) be included in the

consolidated balance sheet dated December 31, 2013?

A) $110,000.

B) $105,000.

C) $100,000.

D) $ 90,000.

E) $ 60,000.

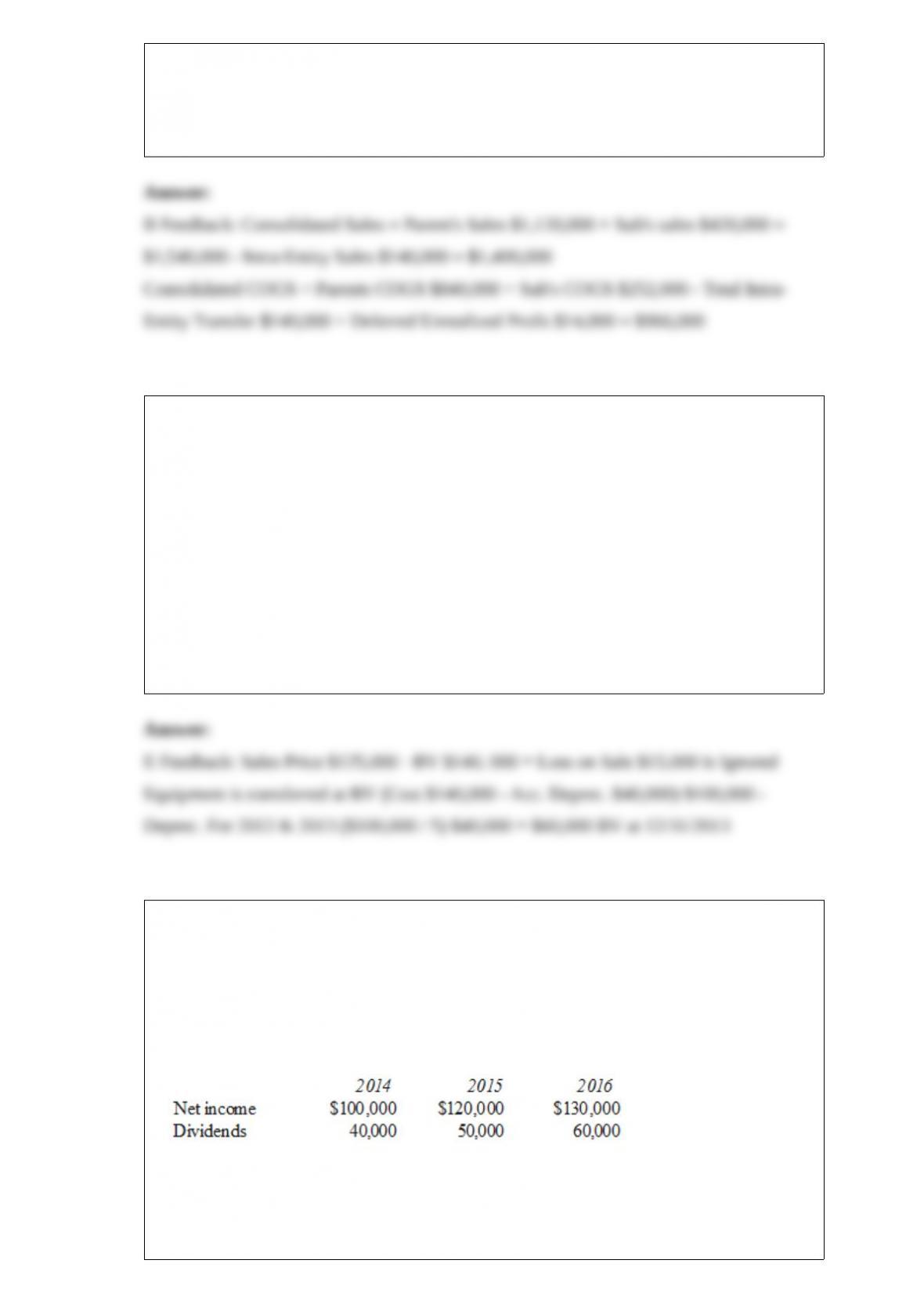

12) Pell Company acquires 80% of Demers Company for $500,000 on January 1, 2014.

Demers reported common stock of $300,000 and retained earnings of $210,000 on that

date. Equipment was undervalued by $30,000 and buildings were undervalued by

$40,000, each having a 10-year remaining life. Any excess consideration transferred

over fair value was attributed to goodwill with an indefinite life. Based on an annual

review, goodwill has not been impaired.

Demers earns income and pays dividends as follows:

Assume the EQUITY METHOD is applied.

Compute the non-controlling interest in the net income of Demers at December 31,

2016.

A) $20,400.

B) $24,600.

C) $26,000.

D) $14,000.

E) $12,600.

13) Cayman Inc. bought 30% of Maya Company on January 1, 2013 for $450,000. The

equity method of accounting was used. The book value and fair value of the net assets

of Maya on that date were $1,500,000. Maya began supplying inventory to Cayman as

follows:

Maya reported net income of $100,000 in 2013 and $120,000 in 2014 while paying

$40,000 in dividends each year.

What is the balance in Cayman’s Investment in Maya account at December 31, 2014?

A) $488,700.

B) $489,600.

C) $492,000.

D) $494,400.

E) $514,500.

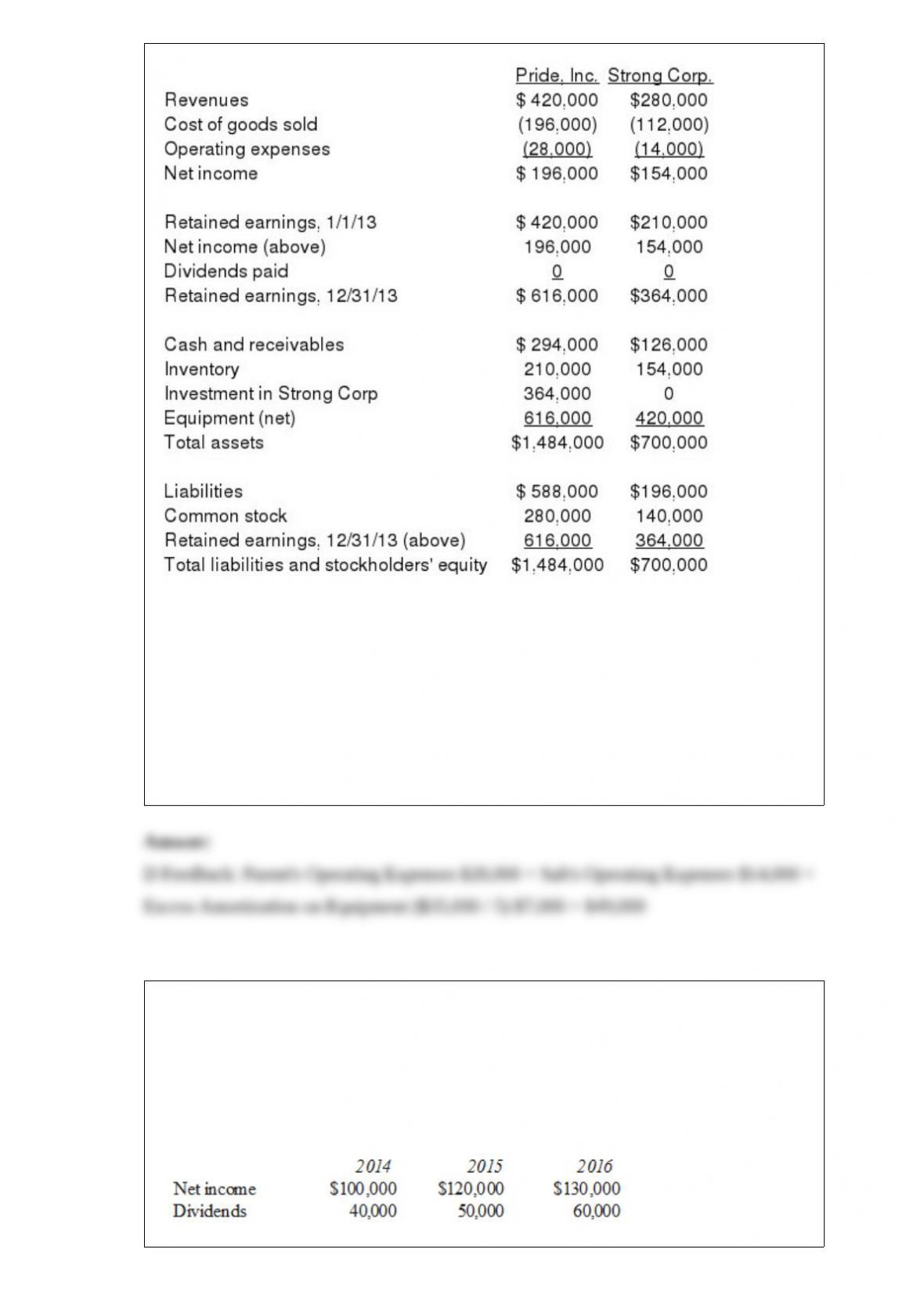

14) On January 1, 2013, Pride, Inc. acquired 80% of the outstanding voting common

stock of Strong Corp. for $364,000. There is no active market for Strong’s stock. Of this

payment, $28,000 was allocated to equipment (with a five-year life) that had been

undervalued on Strong’s books by $35,000. Any remaining excess was attributable to

goodwill which has not been impaired.

As of December 31, 2013, before preparing the consolidated worksheet, the financial

statements appeared as follows:

During 2013, Pride bought inventory for $112,000 and sold it to Strong for $140,000.

Only half of this purchase had been paid for by Strong by the end of the year. 60% of

these goods were still in the company’s possession on December 31, 2013. What is the

total of consolidated operating expenses?

A) $42,000.

B) $47,600.

C) $53,200.

D) $49,000.

E) $35,000.

15) Pell Company acquires 80% of Demers Company for $500,000 on January 1, 2014.

Demers reported common stock of $300,000 and retained earnings of $210,000 on that

date. Equipment was undervalued by $30,000 and buildings were undervalued by

$40,000, each having a 10-year remaining life. Any excess consideration transferred

over fair value was attributed to goodwill with an indefinite life. Based on an annual

review, goodwill has not been impaired.

Demers earns income and pays dividends as follows:

Assume the EQUITY METHOD is applied.

Compute Pell’s income from Demers for the year ended December 31, 2015.

A) $90,400.

B) $89,000.

C) $50,400.

D) $56,000.

E) $96,000.

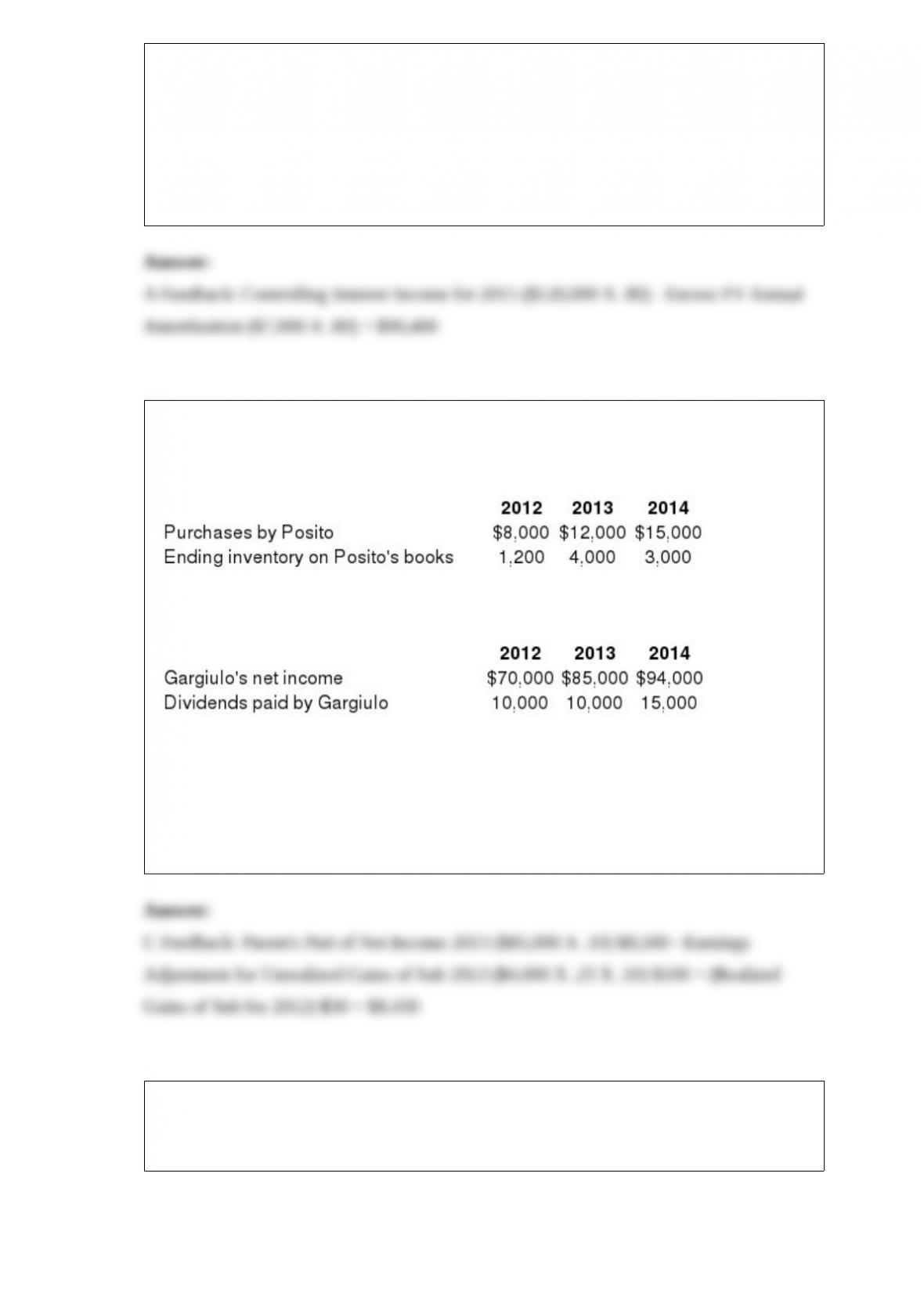

16) Gargiulo Company, a 90% owned subsidiary of Posito Corporation, sells inventory

to Posito at a 25% profit on selling price. The following data are available pertaining to

intra-entity purchases. Gargiulo was acquired on January 1, 2012.

Assume the equity method is used. The following data are available pertaining to

Gargiulo’s income and dividends.

Compute the non-controlling interest in Gargiulo’s net income for 2013.

A) $8,500.

B) $8,570.

C) $8,430.

D) $8,400.

E) $7,580.

17) Presented below are the financial balances for the Atwood Company and the Franz

Company as of December 31, 2012, immediately before Atwood acquired Franz. Also

included are the fair values for Franz Company’s net assets at that date.

Note: Parenthesis indicate a credit balance

Assume a business combination took place at December 31, 2012. Atwood issued 50

shares of its common stock with a fair value of $35 per share for all of the outstanding

common shares of Franz. Stock issuance costs of $15 (in thousands) and direct costs of

$10 (in thousands) were paid to effect this acquisition transaction. To settle a difference

of opinion regarding Franz’s fair value, Atwood promises to pay an additional $5.2 (in

thousands) to the former owners if Franz’s earnings exceed a certain sum during the

next year. Given the probability of the required contingency payment and utilizing a 4%

discount rate, the expected present value of the contingency is $5 (in thousands).

Compute consolidated buildings (net) at date of acquisition.

A) $2,450.

B) $2,340.

C) $1,800.

D) $ 650.

E) $1,690.

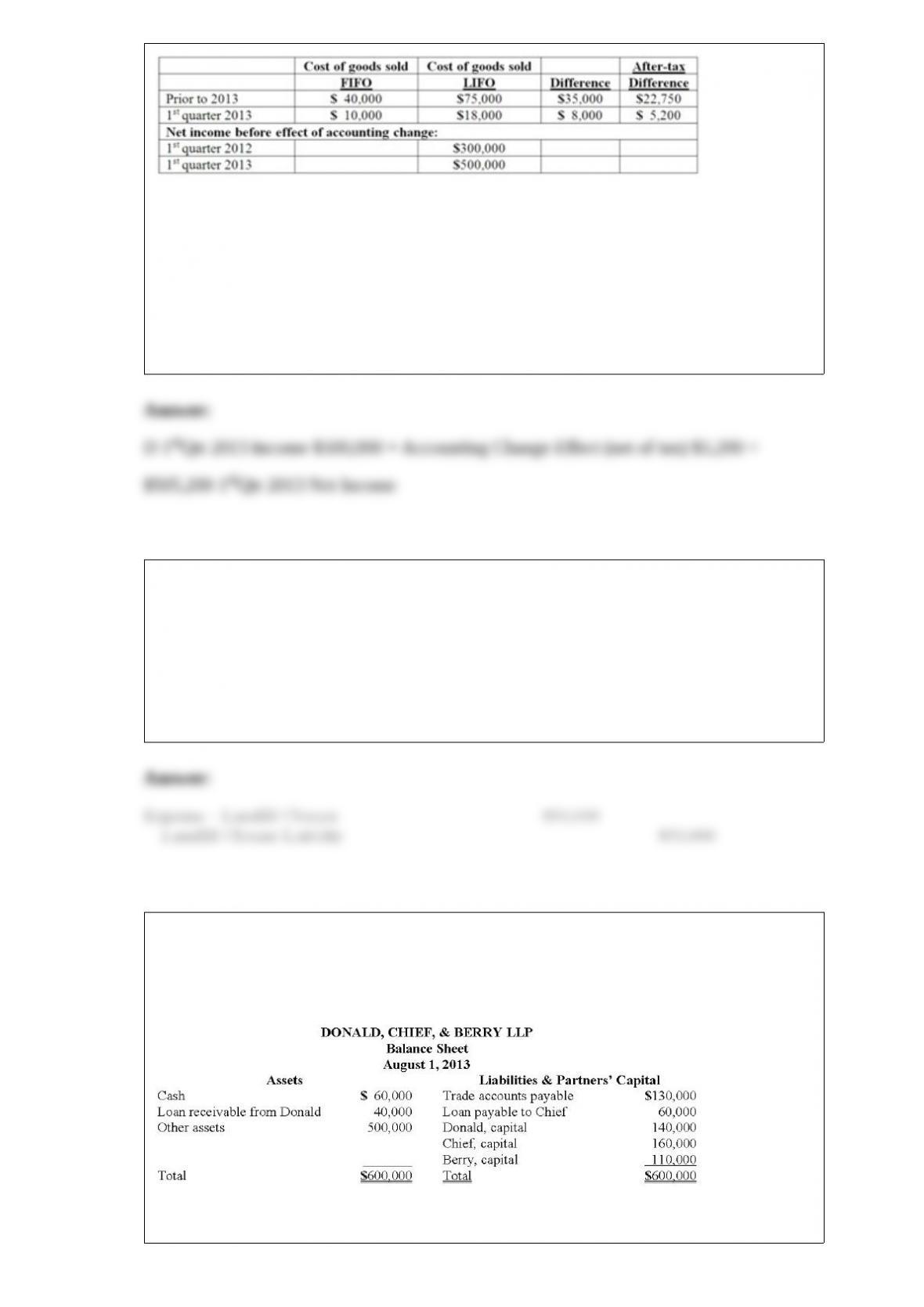

18) Baker Corporation changed from the LIFO method to the FIFO method for

inventory valuation during 2013. Baker has an effective income tax rate of 30 percent

and 100,000 shares of common stock issued and outstanding. The following additional

information is available:

Assuming Baker makes the change in the first quarter of 2013, how much is reported as

net income for the first quarter of 2013?

A.$492,000

B.$494,800

C.$500,000

D.$505,200

E.$527,950

19) The Town of Wakefield opened a solid waste landfill in 2012 that was at 20%

capacity on December 31, 2012 and at 50% capacity on December 31, 2013. The city

initially anticipated closure costs of $2.3 million but in 2013 revised the estimate of the

closure costs to be $2.7 million. None of these costs will be incurred until the landfill is

scheduled to be closed.

What is the journal entry that should be recorded on December 31, 2013 for

Government-wide Financial Statements?

20) The partners of Donald, Chief & Berry LLP decided to liquidate on August 1, 2013.

The balance sheet of the partnership is as follows, with the profit and loss ratio of 25%,

45%, and 30%, respectively.

The disposal of Other Assets with a carrying amount of $200,000 realized $140,000,

and all available cash was distributed.

Prepare the journal entry for Donald, Chief & Berry LLP on August 1, 2013, to record

the realization of Other Assets.

21) The Town of Wakefield opened a solid waste landfill in 2012 that was at 20%

capacity on December 31, 2012 and at 50% capacity on December 31, 2013. The city

initially anticipated closure costs of $2.3 million but in 2013 revised the estimate of the

closure costs to be $2.7 million. None of these costs will be incurred until the landfill is

scheduled to be closed.

Assuming the landfill is recorded within the General fund, what is the journal entry that

should be recorded in the Fund Financial Statements on December 31, 2013?

22) Virginia Corp. owned all of the voting common stock of Stateside Co. Both

companies use the perpetual inventory method, and Virginia decided to use the partial

equity method to account for this investment. During 2012, Virginia made cash sales of

$400,000 to Stateside. The gross profit rate was 30% of the selling price. By the end of

2012, Stateside had sold 75% of the goods to outside parties for $420,000 cash.

Prepare journal entries for Virginia and Stateside to record the sales/purchases during

2012.

23) The board of commissioners of the city of Jarmaine adopted a General Fund budget

for the year ending June 30, 2013, which indicated revenues of $1,300,000, bond

proceeds of $520,000, appropriations of $1,170,000, and operating transfers out of

$390,000.

Required:

If this budget was formally integrated into the accounting records used to produce the

Fund Financial Statements, what was the required journal entry at the beginning of the

year?

24) Direct combination costs and stock issuance costs are often incurred in the process

of making a controlling investment in another company. How should those costs be

accounted for in a pre-2009 purchase transaction?

26) For the month of December 2013, patient charges at Northfield Hospital (a

not-for-profit hospital) were $2,720,000. Third-party payors were billed $1,800,000.

The hospital estimated that contractual adjustments would reduce the amount collected

from third-party payors to $1,710,000.

Required:

Prepare the necessary journal entry to record the contractual adjustments.

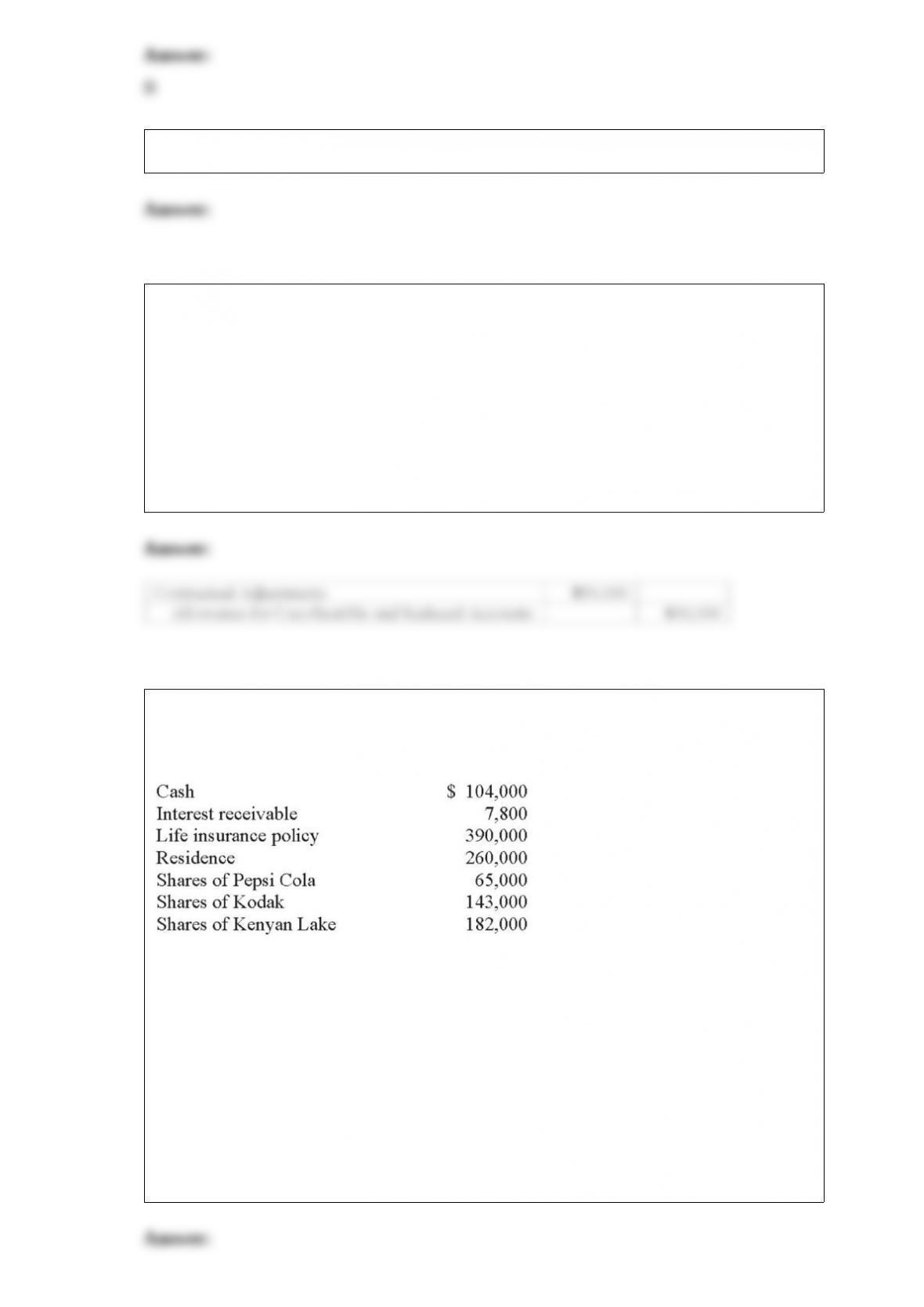

27) The executor of the Estate of Kate Tweed discovered the following assets (at fair

value):

The will of Kate Tweed had the following provisions:

– $195,000 in cash went to Victor Vickery.

– All shares of PepsiCo went to Duchess Doyle.

– The residence went to Louis Tweed.

– All other estate assets were to be liquidated with the resulting cash going to the Sacred

Church of Liberty, Missouri.

An additional savings account of $15,600 was located by the executor.

Prepare the journal entry to record the transaction.