20. B (This transaction is an acquisition and the acquired entity is not supported

predominantly by contributions or investment income. Thus, the difference

23.C

24.C (The charity care work should not be recorded in any way because the entity

has no expectation of collection. That reduction drops the reported amount

25.B (Use of the money is limited to the donor’s specified purpose.)

tax-exempt organization.)

29.D (These volunteer services, although important, do not meet the criteria for

recognition. They do not require a specialized skill that would be otherwise

purchased. They do not enhance a nonfinancial asset.)

32.B

33.A (The fundraising costs and administrative salaries are supporting service

expenses.)

36.(10 minutes) (Reporting of various account balances by a not-for-profit health

care entity)

Donated medicines = an asset is reported as well as an increase in

unrestricted net assets because of the contribution

Donated services (replacing salaried workers) = the fair value of the services

contributed causes an increase in unrestricted net assets along with an

accompanying decrease in unrestricted net assets because the expense is

also recognized

37. (15 Minutes) (Series of questions about the reporting of health care entities)

a. A third-party payor is an entity (such as Medicare or an insurance company)

that pays a portion, or all, of a patient’s medical expenses. They are common

principles and reliable accounting systems.

b. A contractual adjustment is a reduction to patient service revenues created

when a lesser amount is paid by a third-party payor than the billed amount but

is still accepted as payment in full by a health care entity. These outside

parties often establish contractual arrangements whereby the health care

entity agrees to accept a lower amount for a service if the third party

c. At the time that materials are donated to a health care entity (or any private

not-for-profit entity), the asset is recorded at fair value. Because of the

unrestricted net assets each period equal to depreciation expense.

Donated services are recorded as a contribution increasing unrestricted net

assets and as salary expense also within unrestricted net assets. FASB

requires private not-for-profit entities to recognize donated services but only if

38.(6 Minutes) (Reporting of various accounts by a not-for-profit entity)

Only $7.6 million is reported as patient service revenues. Charity care of $1.4

million is not recorded because no attempt at collection is anticipated. Then,

39. a). (8 Minutes) (Recording donations by a voluntary health and welfare

entity)

Pledges ………….………..………..………..………..………….…… $600,000

Anticipated Amount Deemed to be Uncollectible (15%) (90 ,000)

Net Pledge Balance…………………..………..…………..….. $510 ,000

40.(65 Minutes) (Preparation of statements for a private not-for-profit entity)

a. Statement of Activities

Unrestricted

Net Assets

Temporarily Restricted

Net Assets

Permanently Restricted

Net Assets

Public Support

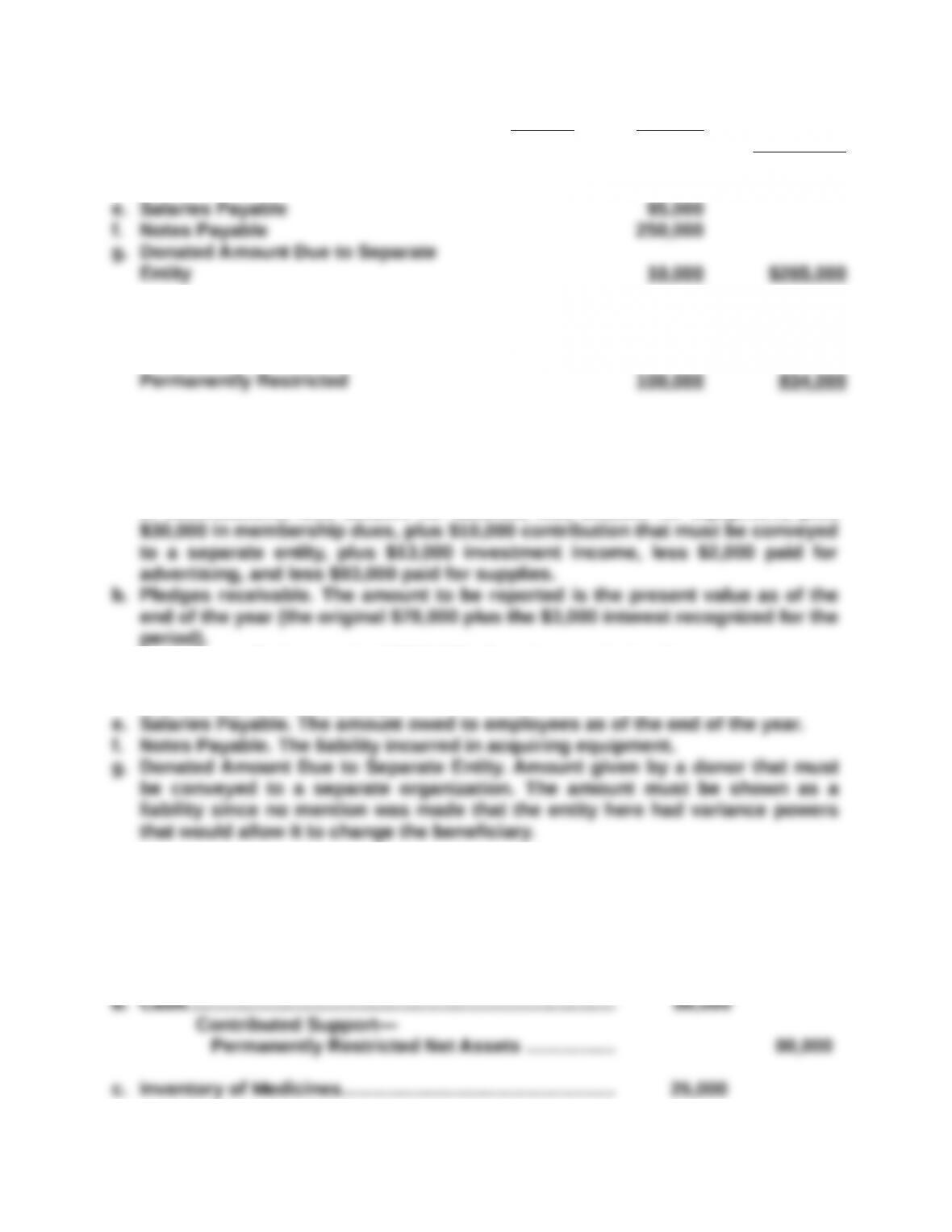

a. Contributions $210,000 $78,000

b. Contribution—Interest 3,000

Revenue

restriction 72 ,000 (72 ,000)

Total Public Support and

Revenue $315,900 $18,100

Expenses

Total (135 ,500)

Supporting service expenses

– General and administrative

i. Salaries (32,000)

j. Depreciation (2 ,000)

Total (30 ,500)

Total Expenses (200 ,000)

Change in Net Assets $115,900 $18,100 -0-

Net Assets – Beginning

40. (continued)

Explanation of Balances

a. Contributions. The balances to be reported are the unrestricted gifts

($210,000) plus present value of unrestricted pledge ($78,000). Pledge is

b. Contribution-Interest. The pledge is recorded at its present value of $78,000.

Interest that is recognized to raise the balance to the pledge amount is

reported as a contribution.

f. Salaries. During the period, $24,000 in salaries were paid (30 percent of

$80,000 was assigned here) and another $2,500 was owed at the end of the

year (50 percent of year-end accrual).

g. Depreciation. Of the total expense ($20,000) for the period, 80 percent was

allocated to program service expenses because that amount of the equipment

was used for that purpose.

m. Depreciation. Of the total for the period ($20,000), 10 percent was allocated to

fundraising expenses.

40. (continued)

b.

Statement of Financial Position

Assets

a. Cash $738,000

d. Accumulated Depreciation (20 ,000) 280,000

Total Assets $1 ,099,000

Liabilities

Net Assets (see Statement of Activities)

Unrestricted $515,900

Temporarily Restricted 218,100

Explanation of Balances:

a. Cash. The final balance is the beginning cash figure of $700,000 plus $210,000

in contributions, less $80,000 for salaries, less $50,000 for equipment, plus

c. Equipment. Entity acquired $300,000 of equipment during the year.

d. Accumulated Depreciation. The $20,000 amount of depreciation recorded for

this initial year of ownership.

41.(50 Minutes) (Effect of various transactions on unrestricted and restricted net

assets)

a. Investments—Internally Restricted ………..……..……..…. 160,000

Cash……….………..………..…………….……..……..…….. 160,000

Cash……….………..………..…………….……..……..…….. 25,000

Reclassification—Temporarily

Accumulated Depreciation……..……..……..……….. 38,000

f. Cash……….………..………..………..………..…..……..……..…….. 15,000

Interest Revenue—

Unrestricted Net Assets (internally restricted) 15,000

g. Provision for Bad Debts………….………..………..……………. 20,000

Allowance for Uncollectible

41.(continued)

h. Supplies Expense ……………………..………..……..……..……. 25,000

Inventory of Medicines……………………..………….... 25,000

i. Cash ……….………..………..………..………..….……………..……. 172,000

41. (continued)

Calculation of Changes in Net Assets

Unrestricted Temporarily Restricted Permanently Restricted

Net Assets Net Assets Net Assets

a. No change

Services 600,000

e. Depreciation (38,000)

f. Interest 15,000

Stipulation

Met—Reclas-

sification 25,000 (25,000)

42. (70 minutes) (Produce journal entries for a private university as well as a

statement of activities)

a. Tuition Receivable 1,200,000

Tuition Revenues 1,200,000

b. Investments 300,000

Contributions—Permanently

Restricted Net Assets 300,000

e. Salary Expenses 310,000

Cash 310,000

f. Salary Expense 80,000

Contributed Support—

Unrestricted Net Assets 80,000

i. Cash 9,000

Dividend Revenue—Unrestricted

Net Assets 9,000

42. (continued)

l. Pledge Receivable 7,000

Contribution—Temporarily

Restricted Net Assets 7,000