Answers to Problems

1. B

2. C

13. A

14. C

Problems 15-19 are based on the comprehensive illustration.

15. (15 minutes) (Carrying inventory at the lower of cost or “market”)

Historical cost $120,000

Replacement cost $111,900

a. 1. Under U.S. GAAP, the company reports inventory on the balance sheet at the

lower of historical cost or market, where market is defined as replacement

2. In accordance with IAS 2, the company reports inventory on the balance

sheet at the lower of historical cost and net realizable value. As a result,

b. As a result of the differing amounts of inventory loss recognized under U.S.

16. (25 minutes) (Measurement of property, plant, and equipment subsequent to

acquisition)

Cost $78,400

Residual value $10,000

Useful life 6 years

Straight-line depreciation $11,400 per year

a. 1. Under U.S. GAAP, the company would report the equipment at its

depreciated historical cost. Straight-line depreciation expense is $11,400 per

2. Under IFRS, the equipment would be depreciated by $11,400 in 2015,

resulting in a book value of $67,000 at December 31, 2015. Under IAS 16’s

The journal entry to record the revaluation on January 1, 2016 would be:

Dr. Equipment $7,500

Depreciation expense on a straight-line basis in 2016, 2017, and beyond

would be $12,900 per year [($74,500 – $10,000) / 5 years]. The equipment

The differences can be summarized as follows:

Depreciation expense 2015 2016 2017

IFRS $11,400 $12,900 $12,900

U.S. GAAP $11,400 $11,400 $11,400

Difference $0 $1,500 $1,500

Book value of equipment 12/31/15 12/31/16 12/31/17

16. (continued)

b. There is no difference in net income between IFRS and U.S. GAAP in 2015, so

no reconciliation adjustments are necessary in 2015.

In 2016, the additional amount of depreciation expense of $1,500 related to the

revaluation surplus under IFRS must be subtracted from U.S. GAAP income to

reconcile to IFRS net income. The additional depreciation taken under IFRS

In 2017, $1,500 again is added to IFRS net income to reconcile to U.S. GAAP

net income, and $4,500 is subtracted from IFRS stockholders’ equity to reconcile

17. (15 minutes) (Research and development costs)

Research and development costs $650,000 (30% related to development)

Useful life 10 years

a. 1. Under U.S. GAAP, $650,000 of research and development costs would be

expensed in 2015.

2. In accordance with IAS 38, $455,000 [$650,000 x 70%] of research and

development costs would be expensed in 2015, and $195,000 [$650,000 x

b. In 2015, $195,000 would be added to U.S. GAAP net income to reconcile to

IFRS and the same amount would be added to U.S. GAAP stockholders’ equity.

In 2016, the company would recognize $19,500 [$195,000 / 10 years] of

amortization expense on the deferred development costs under IFRS that would

not be recognized under U.S. GAAP. In 2016, $19,500 would be subtracted from

IFRS.

18. (15 minutes) (Gain on sale and leaseback transaction)

Gain on sale of asset $76,000

Life of leaseback 4 years

a. 1. Under U.S. GAAP, the gain of $76,000 on the sale and leaseback transaction

is deferred and amortized to income over the life of the lease. With a lease

b. In 2015, IFRS net income exceeds U.S. GAAP net income by $57,000, the

difference ($76,000 vs. $19,000) in the amount of gain recognized on the sale

In 2016, a gain of $19,000 would be recognized under U.S. GAAP that would not

exist under IFRS. As a result, $19,000 would be subtracted from U.S. GAAP net

19. (20 minutes) (Impairment of property, plant, and equipment)

Cost of equipment $135,000

Salvage value zero

a. 1. Under U.S. GAAP, an asset is impaired when its carrying value exceeds the

expected future cash flows (undiscounted) to be derived from use of the

2. In accordance with IAS 36, an asset is impaired when its carrying value

exceeds its recoverable amount, which is the greater of (a) value in use

(present value of expected future cash flows), and (b) net selling price, less

b. An impairment loss of $8,000 was recognized in 2015 under IFRS but not under

U.S. GAAP. Therefore, $8,000 must be subtracted from U.S. GAAP net income

In 2016, depreciation under IFRS will be $25,000 [$100,000 / 4 years], whereas

stockholders’ equity to IFRS at December 31, 2016, $6,000 must be subtracted

from U.S. GAAP stockholders’ equity. This is the difference between the

impairment loss of $8,000 in 2015 taken under IFRS and the difference in

depreciation expense recognized under the two sets of standards in 2016. It

also is equal to the difference in the carrying value of the equipment at

December 31, 2016 under the two sets of accounting rules:

IFRS U.S. GAAP

Cost $135,000 $135,000

Depreciation, 2015 (27,000) (27,000)

Chapter 11 Develop Your Skills

Analysis Case 1—Application of IAS 16

This assignment demonstrates the effect one difference between IFRS and U.S.

GAAP would have on a company’s net income and stockholders’ equity over a

20-year period.

The building has a book value of $9,000,000 on January 1, Year 3. On that date,

under IFRS, Abacab would revalue the building through the following journal entry:

Dr. Building $3,000,000

Cr. Accumulated Other Comprehensive Income (AOCI) $3,000,000

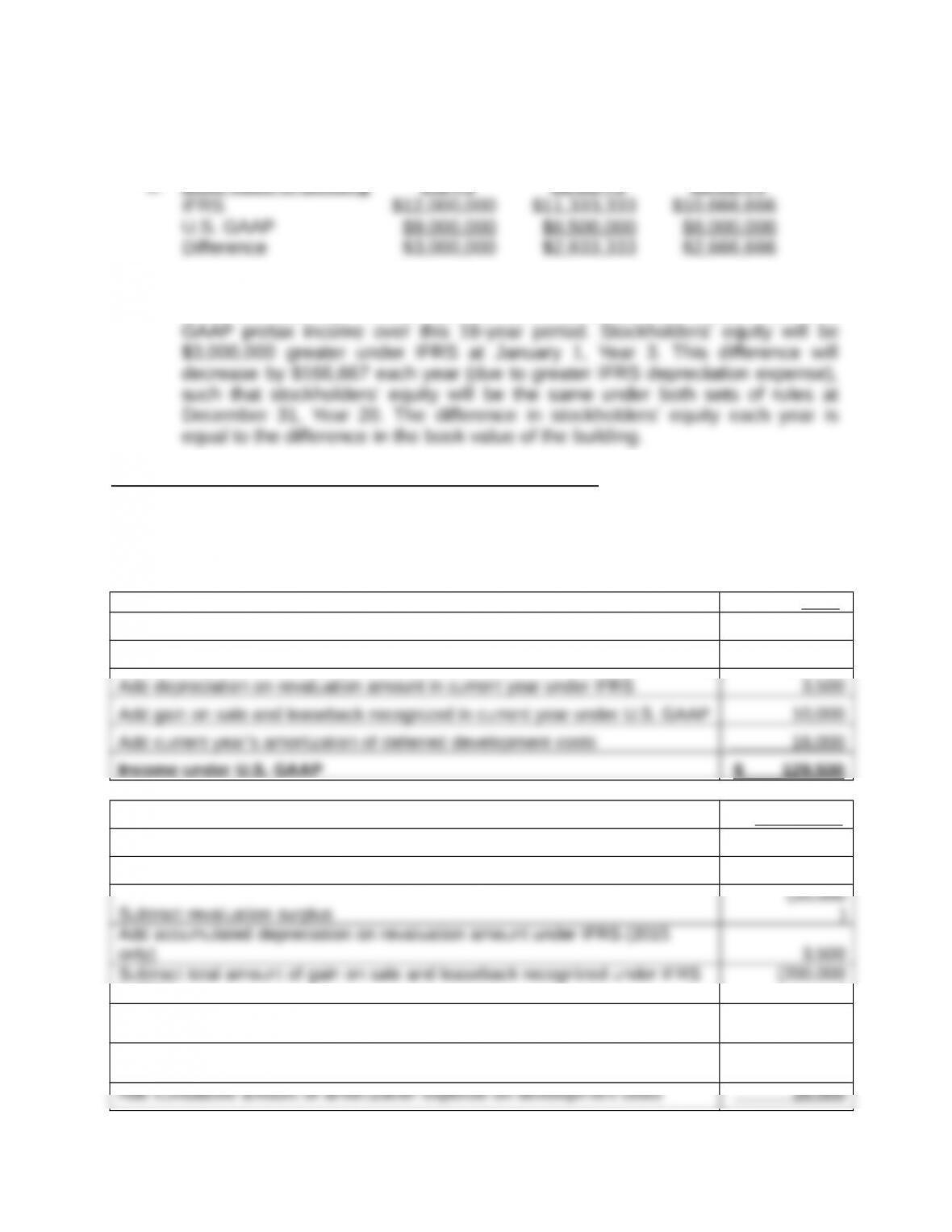

a. Depreciation Expense Year 2 Year 3 Year 4

IFRS $500,000 $666,667 $666,667

U.S. GAAP $500,000 $500,000 $500,000

b. Book Value of Building 1/2/Y3 12/31/Y3 12/31/Y4

c. Pre-tax income will be $166,667 smaller in each year (Year 3 -Year 20) under

IFRS. Cumulatively, IFRS-pretax income will be $3,000,000 smaller than U.S.

Analysis Case 2— Reconciliation of IFRS to U.S. GAAP

Quantacc Ltd.

Schedule to Reconcile IFRS Net Income and Stockholders’ Equity

to U.S. GAAP

2015

Income under IFRS $ 100,000

Adjustments:

12/31/2015

Stockholders’ equity under IFRS $ 1,000,000

Adjustments:

(35,000

in 2014

)

Add cumulative amount of gain on sale and leaseback that would have been

recognized under U.S. GAAP in 2014 and 2015 20,000

Subtract total amount of development costs capitalized under IFRS in 2014

(80,000

)

1. Under IFRS – Quantacc recorded a Revaluation Surplus (stock equity account) of

$35,000 on 1/1/2015. In 2015, $3,500 of depreciation expense was taken on the

revaluation amount ($35,000 / 10 years).

2. Under IFRS – Quantacc recognized a gain on sale/leaseback of $200,000 in 2014.

No gain was recognized in 2015.

Under GAAP – Quantacc would recognize a gain on sale/leaseback of $10,000 in

both 2014 and 2015.

3. Under IFRS – Quantacc recognized a development cost asset of $80,000 in 2014.

In 2015, amortization expense related to this asset was $16,000 ($80,000 / 5 years).

Research Case—Reconciliation to U.S. GAAP

Note to instructors: The SEC no longer requires a U.S. GAAP reconciliation

from foreign companies using IFRS. As more foreign companies adopt IFRS

selected company from the company’s website.

This assignment requires students to find the note in Form 20–F in which foreign

companies reconcile net income and stockholders’ equity from foreign GAAP to

Communication Case—Voluntary Adoption of IFRS

The response to the requirement in this case will vary by student. Potential benefits

and potential risks from the voluntary adoption of IFRS that students might discuss in

their memo include the following:

Potential benefits.

Preparing IFRS financial statements would make it easier for analysts to compare

Potential risks.

The major risk of voluntary adoption of IFRS is that the SEC might ultimately decide

not to require the use of IFRS in the United States. In that case, the company

Internet Case—Foreign Company Annual Report

The responses to this assignment will depend on the company selected by the

student. A comparison of the findings across companies selected by students can

lead to a lively classroom discussion.