2) Kaycee Corporation’s revenues for the year ended December 31, 2012, were as

follows:

Consolidated Revenue per the Income Statement: $1,200,000

Upstream Intersegment Sales: $180,000

Downstream Intersegment Sales: $60,000

For purposes of the Revenue Test, what amount will be used as the benchmark for

determining whether a segment is reportable?

A.$24,000

B.$120,000

C.$138,000

D.$144,000

E.$0

3) A company sells a building to a bank in 2013 at a gain of $100,000 and immediately

leases the building back for period of five years. The lease is accounted for as an

operating lease. The building was originally purchased for $200,000 and currently had a

book value of $50,000 at the date of the sale.

What amount should be recognized in 2013 as a gain on the sale using U.S. GAAP?

A.$20,000.

B.$50,000.

C.$100,000.

D.$150,000.

E.$200,000.

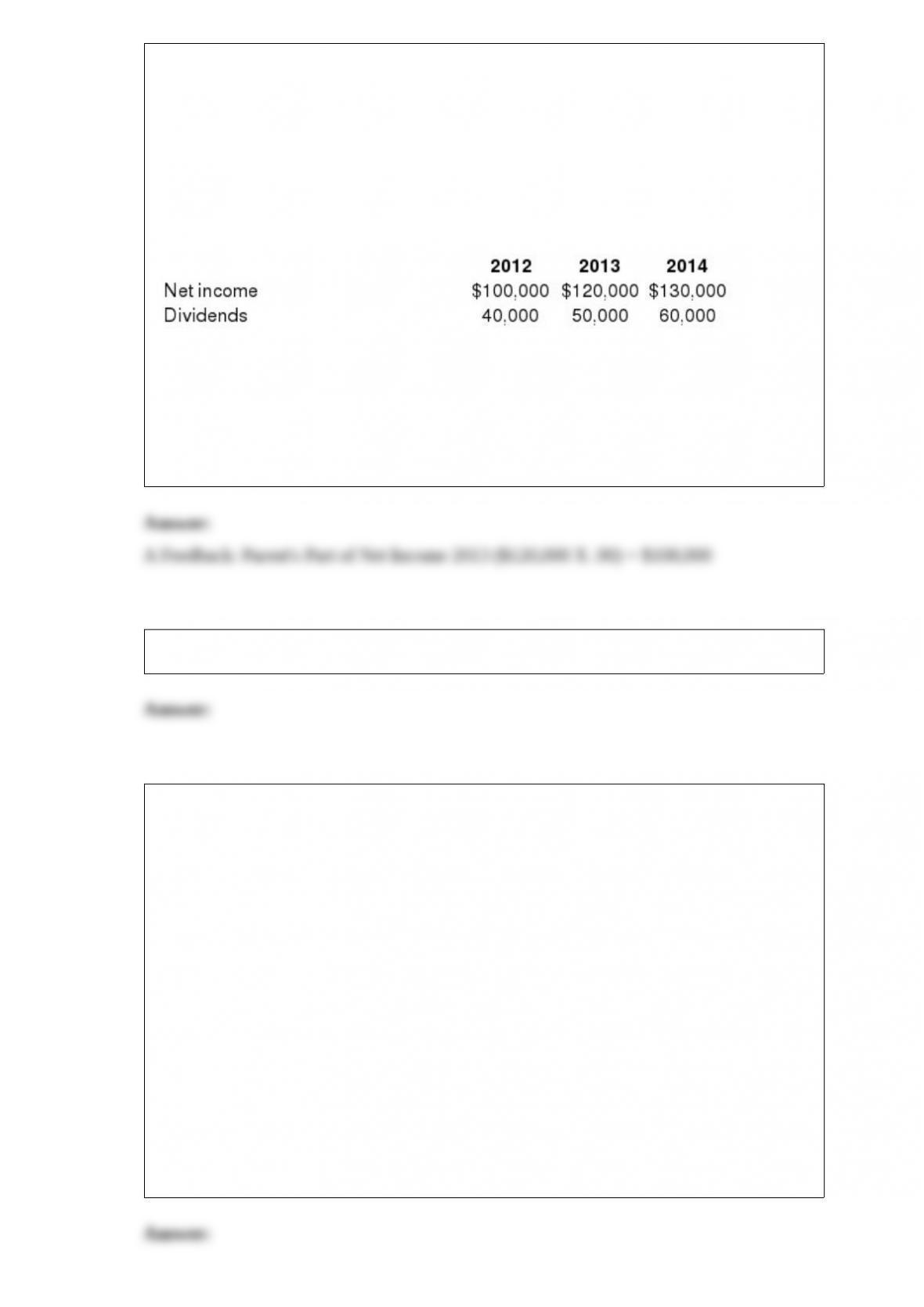

4) Wilson owned equipment with an estimated life of 10 years when it was acquired for

an original cost of $80,000. The equipment had a book value of $50,000 at January 1,

2012. On January 1, 2012, Wilson realized that the useful life of the equipment was

longer than originally anticipated, at ten remaining years.

On April 1, 2012 Simon Company, a 90% owned subsidiary of Wilson Company,

bought the equipment from Wilson for $68,250 and for depreciation purposes used the

estimated remaining life as of that date. The following data are available pertaining to

Simon’s income and dividends:

Compute Wilson’s share of income from Simon for consolidation for 2013.

A) $108,000

B) $110,000.

C) $106,000.

D) $109,825.

E) $109,800.

6) Kennedy Company acquired all of the outstanding common stock of Hastie

Company of Canada for U.S. $350,000 on January 1, 2013, when the exchange rate for

the Canadian dollar (CAD) was U.S. $.70. The fair value of the net assets of Hastie was

equal to their book value of CAD 450,000 on the date of acquisition. Any acquisition

consideration excess over fair value was attributed to an unrecorded patent with a

remaining life of five years. The functional currency of Hastie is the Canadian dollar.

For the year ended December 31, 2013, Hastie’s trial balance net income was translated

at U.S. $25,000. The average exchange rate for the Canadian dollar during 2013 was

U.S. $.68, and the 2013 year-end exchange rate was U.S. $.65.

Compute the amount of the patent reported in the consolidated balance sheet at

December 31, 2013

A.$28,200

B.$25,700

C.$35,000

D.$27,200

E.$26,000

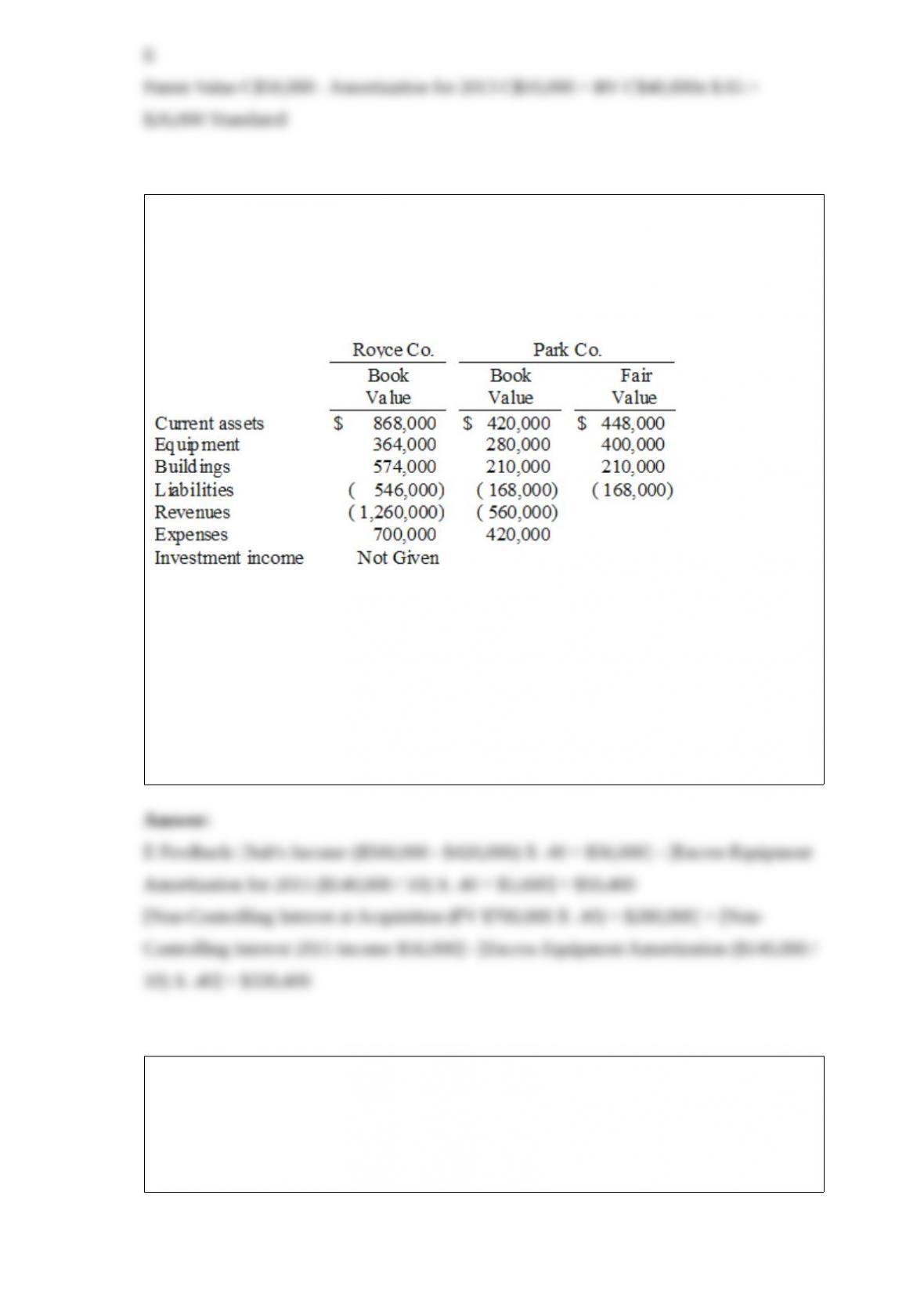

7) Royce Co. acquired 60% of Park Co. for $420,000 on December 31, 2014 when

Park’s book value was $560,000. The Royce stock was not actively traded. On the date

of acquisition, Park had equipment (with a ten-year life) that was undervalued in the

financial records by $140,000. One year later, the following selected figures were

reported by the two companies. Additionally, no dividends have been paid.

What is the non-controlling interest’s share of the subsidiary’s net income for the year

ended December 31, 2015 and what is the ending balance of the non-controlling interest

in the subsidiary at December 31, 2015?

A) $56,000 and $280,000.

B) $50,400 and $218,400.

C) $56,000 and $224,000.

D) $56,000 and $336,000.

E) $50,400 and $330,400.

8) On January 4, 2013, Bailey Corp. purchased 40% of the voting common stock of

Emery Co., paying $3,000,000. Bailey properly accounts for this investment using the

equity method. At the time of the investment, Emery’s total stockholders’ equity was

$5,000,000. Bailey gathered the following information about Emery’s assets and

liabilities whose book values and fair values differed:

Any excess of cost over fair value was attributed to goodwill, which has not been

impaired. Emery Co. reported net income of $400,000 for 2013, and paid dividends of

$200,000 during that year.

What is the amount of excess amortization expense for Bailey’s investment in Emery

for the first year?

A) $ 0

B) $ 84,000

C) $100,000

D) $160,000

E) $400,000

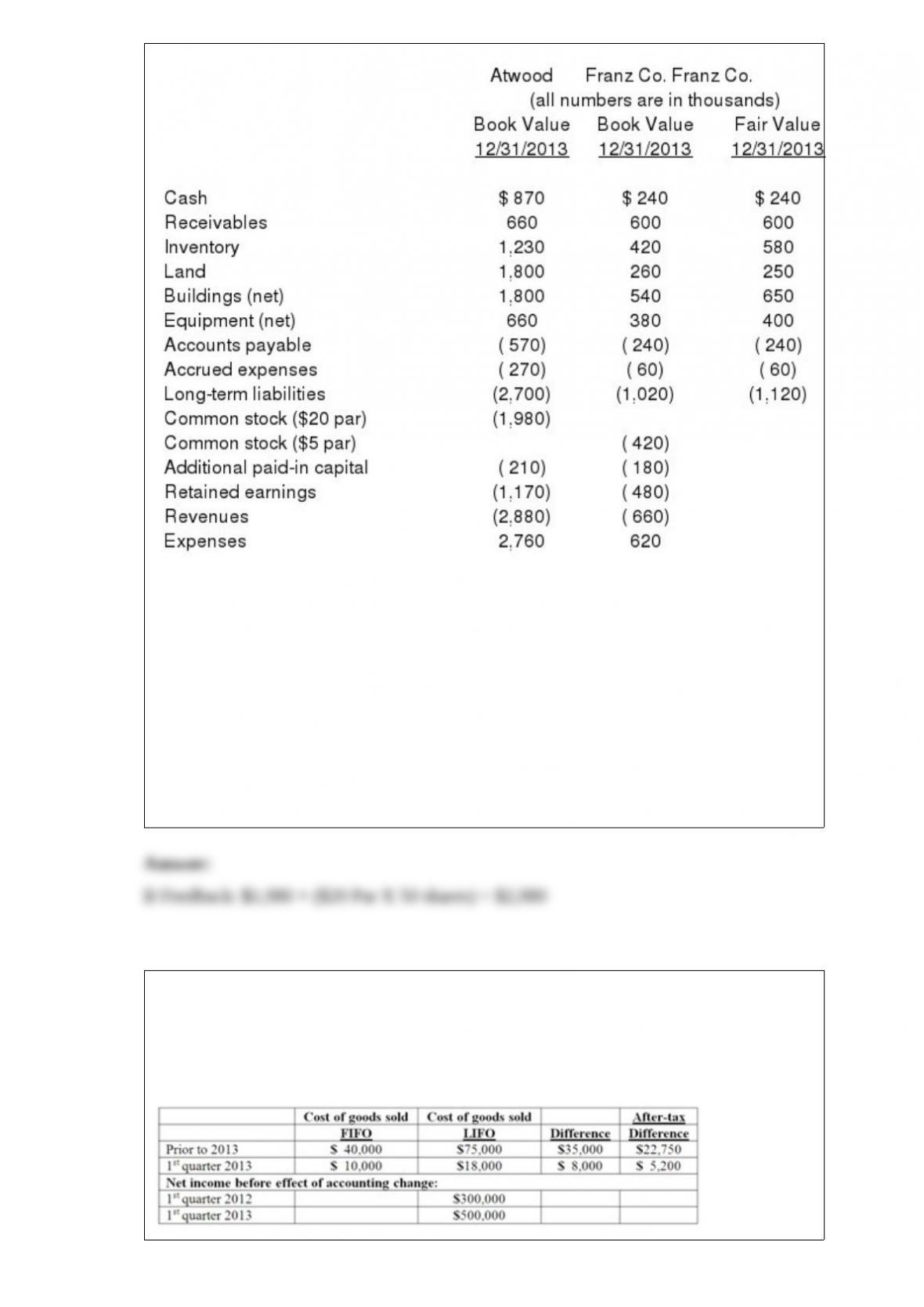

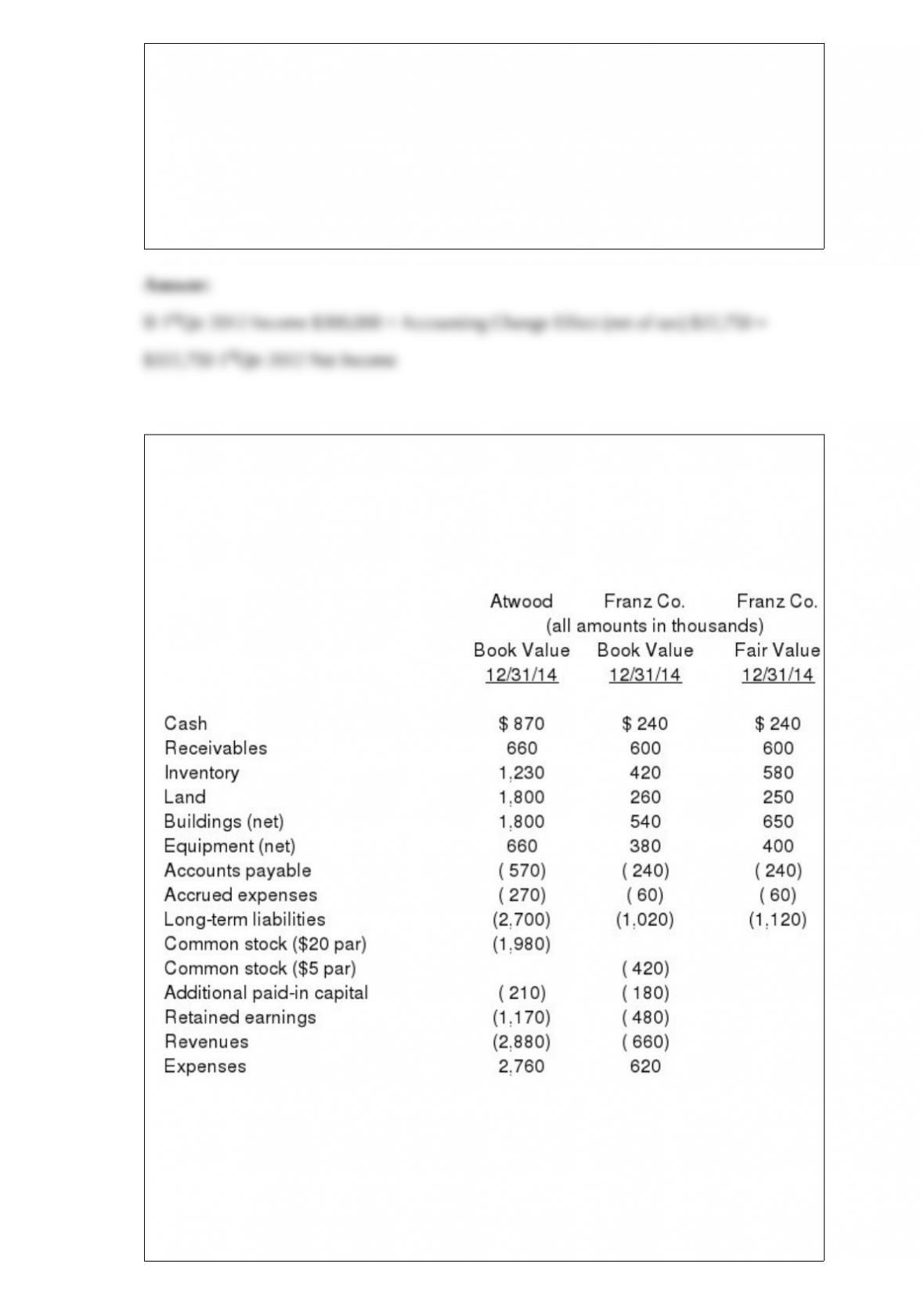

9) The financial balances for the Atwood Company and the Franz Company as of

December 31, 2013, are presented below. Also included are the fair values for Franz

Company’s net assets.

Note: Parenthesis indicate a credit balance

Assume an acquisition business combination took place at December 31, 2013. Atwood

issued 50 shares of its common stock with a fair value of $35 per share for all of the

outstanding common shares of Franz. Stock issuance costs of $15 (in thousands) and

direct costs of $10 (in thousands) were paid.

Compute the consolidated common stock at date of acquisition.

A) $1,000.

B) $2,980.

C) $2,400.

D) $3,400.

E) $3,730.

10) Baker Corporation changed from the LIFO method to the FIFO method for

inventory valuation during 2013. Baker has an effective income tax rate of 30 percent

and 100,000 shares of common stock issued and outstanding. The following additional

information is available:

Assuming Baker makes the change in the first quarter of 2012, how much is reported as

net income for the first quarter of 2012?

A.$300,000

B.$322,750

C.$335,000

D.$265,000

E.$277,250

11) Presented below are the financial balances for the Atwood Company and the Franz

Company as of December 31, 2012, immediately before Atwood acquired Franz. Also

included are the fair values for Franz Company’s net assets at that date.

Note: Parenthesis indicate a credit balance

Assume a business combination took place at December 31, 2012. Atwood issued 50

shares of its common stock with a fair value of $35 per share for all of the outstanding

common shares of Franz. Stock issuance costs of $15 (in thousands) and direct costs of

$10 (in thousands) were paid to effect this acquisition transaction. To settle a difference

of opinion regarding Franz’s fair value, Atwood promises to pay an additional $5.2 (in

thousands) to the former owners if Franz’s earnings exceed a certain sum during the

next year. Given the probability of the required contingency payment and utilizing a 4%

discount rate, the expected present value of the contingency is $5 (in thousands).

Compute consolidated land at date of acquisition.

A) $2,060.

B) $1,800.

C) $ 260.

D) $2,050.

E) $2,070.