21-22. (Option cash flow hedge of a forecasted foreign currency transaction)

The easiest way to solve problems 21 and 22 is to prepare journal entries

for the option cash flow hedge of a forecasted transaction. The journal

entries are as follows:

11/1/15

Foreign Currency Option $1,500

Cash $1,500

2/1/16

Option Expense $1,100

Foreign Currency Option 900

Accumulated Other Comprehensive Income (AOCI)

$2,000

Foreign Currency (BRL) [200,000 x $.41]

$82,000

Cash

[200,000 x $.40] $80,000

Foreign

Currency Option 2,000

21-22. (continued)

Net impact on 2016 net income:

Option Expense $ (1,100)

Cost-of-Goods-Sold (82,000)

21. B

23. (10 minutes) (Foreign currency payable — import purchase)

a. The decrease in the dollar value of the LCU payable from November 1

(60,000 x .345 = $20,700) to December 31 (60,000 x .333 = $19,980) is

24. (10 minutes) (Foreign currency receivable – export sale)

a. The ostra receivable decreases in dollar value from (50,000 x $1.05)

$52,500 at December 20 to $51,000 (50,000 x $1.02) at December 31,

25. (10 minutes) (Foreign currency receivable – export sale)

9/15 Accounts Receivable (FCU) [100,000 x $.40] $40,000

Sales $40,000

9/30 Accounts Receivable (FCU) $2,000

Foreign Exchange Gain $2,000

[100,000 x ($.42 – $.40)]

26. (10 minutes) (Foreign currency payable — import purchase)

12/1/15 Inventory $52,800

Accounts Payable (LCU) [60,000 x $.88] $52,800

12/31/15 Accounts Payable (LCU) [60,000 x ($.82 – $.88)] $3,600

Foreign Exchange Gain $3,600

27. (15 minutes) (Determine U.S. dollar balance for foreign currency transactions)

Inventory and Cost of Goods Sold are reported at the spot rate at the date the

inventory was purchased. Sales are reported at the spot rate at the date of

a. Inventory [50,000 pesos x 40% x $.17]…………………..…..…..…..………..…..$3,400

b. COGS [50,000 pesos x 60% x $.17]…………….………..……….…………..…..….$5,100

f. Cash [(40,000 x $.19) – (30,000 x $.20)]……………………….………..……….…..$1,600

28. (25 minutes) (Prepare journal entries for foreign currency transactions)

2/1/15 Equipment $17,600

Accounts Payable (L) [40,000 x $.44] $17,600

4/1/15 Accounts Payable (L) $17,600

Foreign Exchange Loss 400

Cash [40,000 x $.45] $18,000

6/1/15 Inventory $14,100

Accounts Payable (L) [30,000 x $.47] $14,100

10/1/15 Cash [30,000 x $.49] $14,700

Accounts Receivable (L) [$19,200 x 3/4] $14,400

Foreign Exchange Gain 300

Accounts Receivable (L) [10,000 x ($.52 – $.48)] $400

Foreign Exchange Gain $400

2/1/16 Cash [10,000 x $.54] $5,400

Accounts Receivable (L) [10,000 x $.52] $5,200

Foreign Exchange Gain 200

29. (20 minutes) (Determine income effect of foreign currency payable – import

purchase)

a. Benjamin, Inc. has a liability of AL 160,000. On the date that this liability

was created (December 1, 2015), the liability had a dollar value of $70,400

(AL 160,000 x $.44). On December 31, 2015, the dollar value has risen to

b. Benjamin, Inc. has a liability of AL 160,000. On the date that this liability

was created (September 1, 2015), the liability had a dollar value of

c. Benjamin, Inc. has a liability of AL 160,000. On the date that this liability

was created (September 1, 2015), the liability had a dollar value of

$73,600 (AL 160,000 x $.46). On December 31, 2015, the dollar value has

30. (30 minutes) (Foreign currency borrowing)

a. 9/30/15 Cash $100,000

Note payable (dudek) [1,000,000 x $.10] $100,000

(To record the note and conversion of 1 million

dudeks into $ at the spot rate.)

9/30/16 Interest Expense [15,000 dudeks x $.12] $1,800

Interest Payable (dudek) 525

Foreign Exchange Loss [5,000 dudeks x

($.12 – $.105)] 75

Cash [20,000 dudeks x $.12] $2,400

(To record the first annual interest payment,

30. (continued)

9/30/17 Interest Expense [15,000 dudeks x $.15] $2,250

Interest Payable (dudek) 625

Foreign Exchange Loss [5,000 dudeks x

($.15 – $.125)] 125

b. The effective cost of borrowing can be determined by considering the total

interest expense and foreign exchange losses related to the loan and

comparing this with the amount borrowed:

2015

Interest expense $525

Foreign exchange loss 5 ,000

Total $5,525 / $100,000 = 5.525% for 3 months

5.525% x 12/3 = 22.1% for 12 months

2016

Interest expense $2,425

Foreign exchange losses 20 ,075

Total $22,500 / $100,000 = 22.5% for 12 months

2017

30. (continued)

The net cash flow from this borrowing is:

Cash outflows:

Interest ($2,400 + $3,000) $5,400

Principal 150 ,000

Ignoring compounding, this results in an effective borrowing cost of approximately 27.7% per year [($55,400 /

$100,000) = 55.4% over two years;

55.4% / 2 years = 27.7% per year].

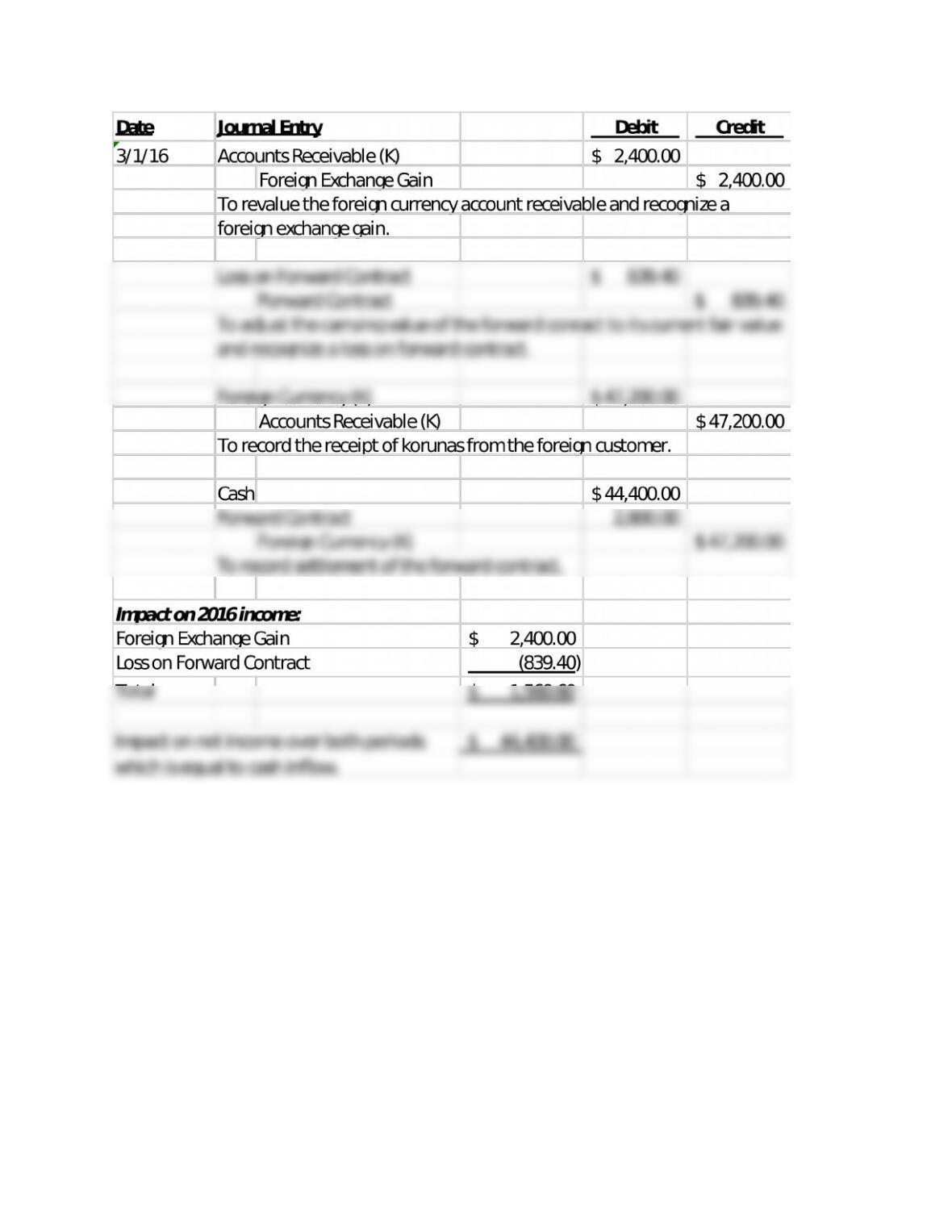

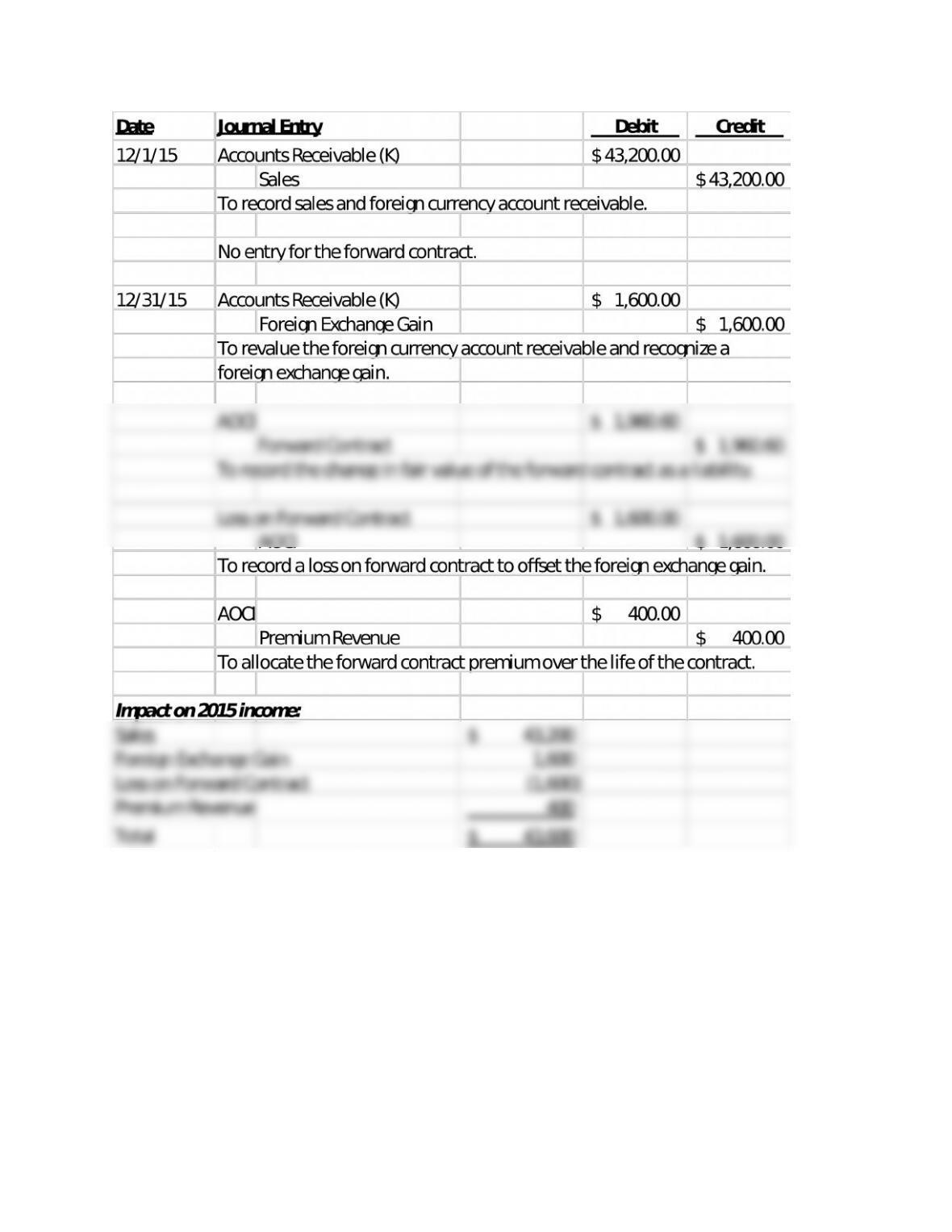

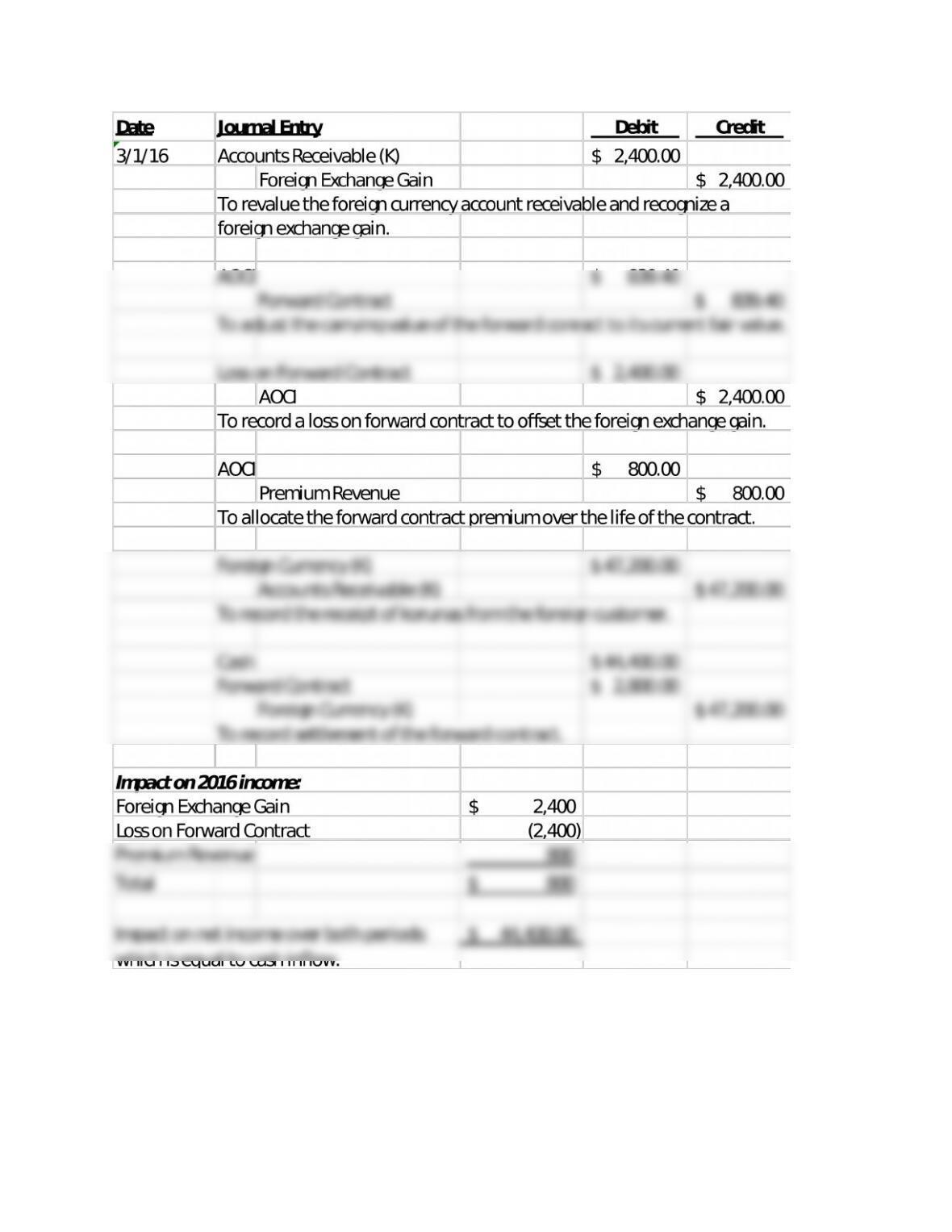

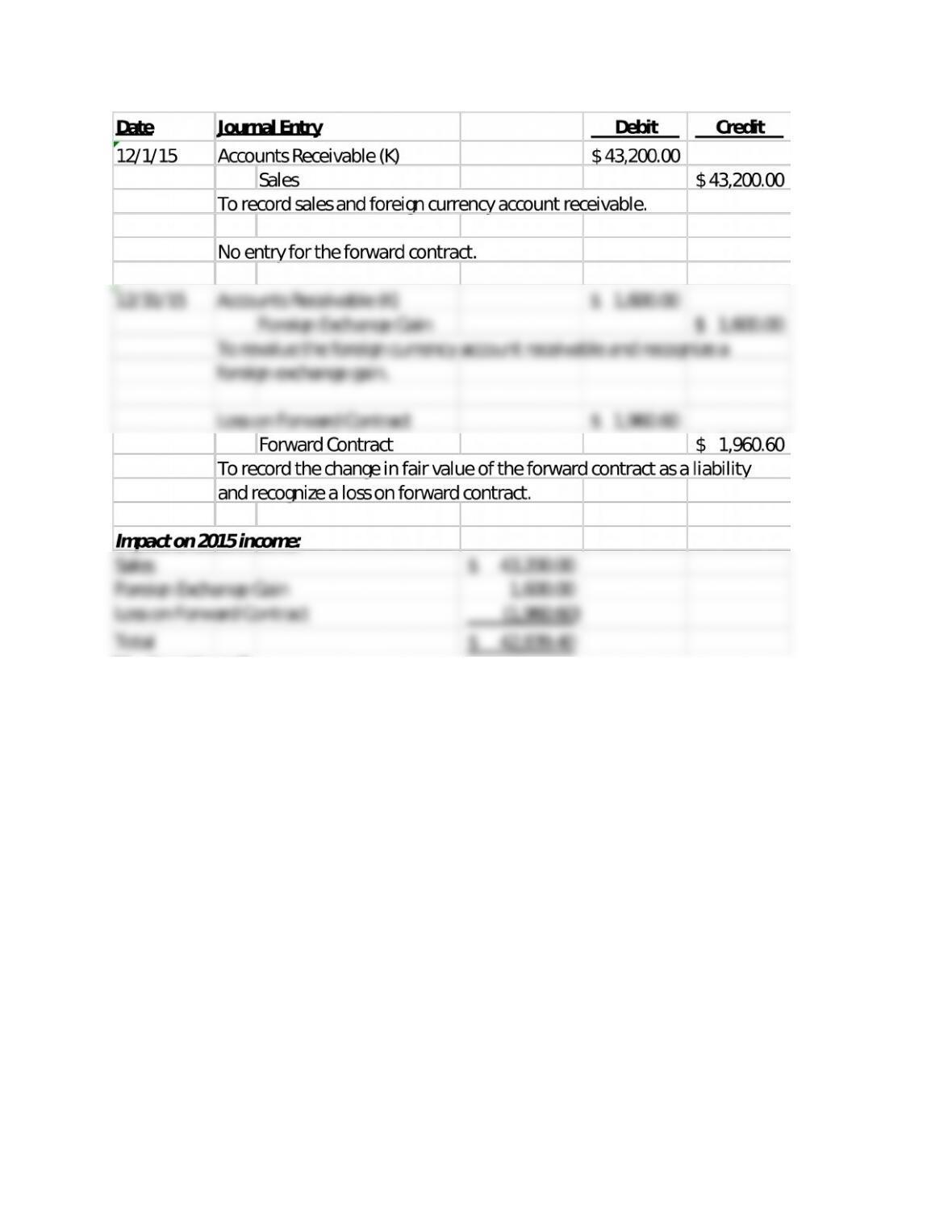

31. (40 minutes) (Forward contract hedge of foreign currency receivable)

31. (continued)

a. Cash Flow Hedge (continued)

31. (continued)

b. Fair Value Hedge

31. (continued)

b. Fair Value Hedge (continued)