1) Campbell Inc. owned all of Gordon Corp. For 2013, Campbell reported net income

(without consideration of its investment in Gordon) of $280,000 while the subsidiary

reported $112,000. The subsidiary had bonds payable outstanding on January 1, 2013,

with a book value of $297,000. The parent acquired the bonds on that date for

$281,000. During 2013, Campbell reported interest income of $31,000 while Gordon

reported interest expense of $29,000. What is consolidated net income for 2013?

A) $406,000.

B) $374,000.

C) $378,000.

D) $410,000.

E) $394,000.

3) The provisions of a will currently undergoing probate are: “Two thousand shares of

Dorn stock to my son; $30,000 in cash from my savings account to my brother; $50,000

in cash to my daughter; and any remaining property divided equally between my son

and daughter.”

Assume that the estate included 1,200 shares of Dorn stock, $22,000 cash in the savings

account, and $70,000 in cash from other sources. What would the daughter have

received from the settlement of the estate?

A.$60,000 cash.

B.$50,000 cash.

C.$55,000 cash.

D.$62,000 cash.

E.$56,000 cash.

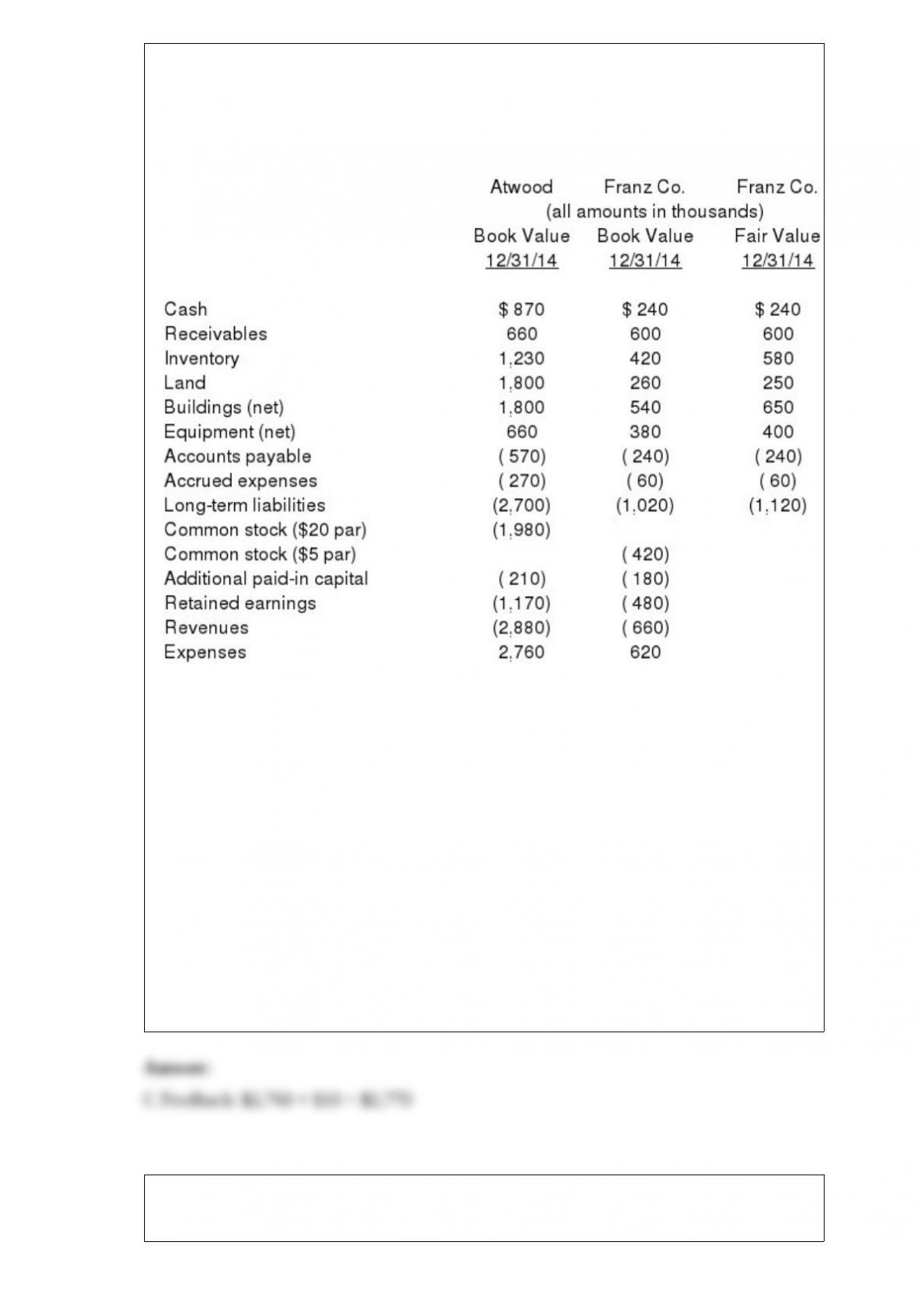

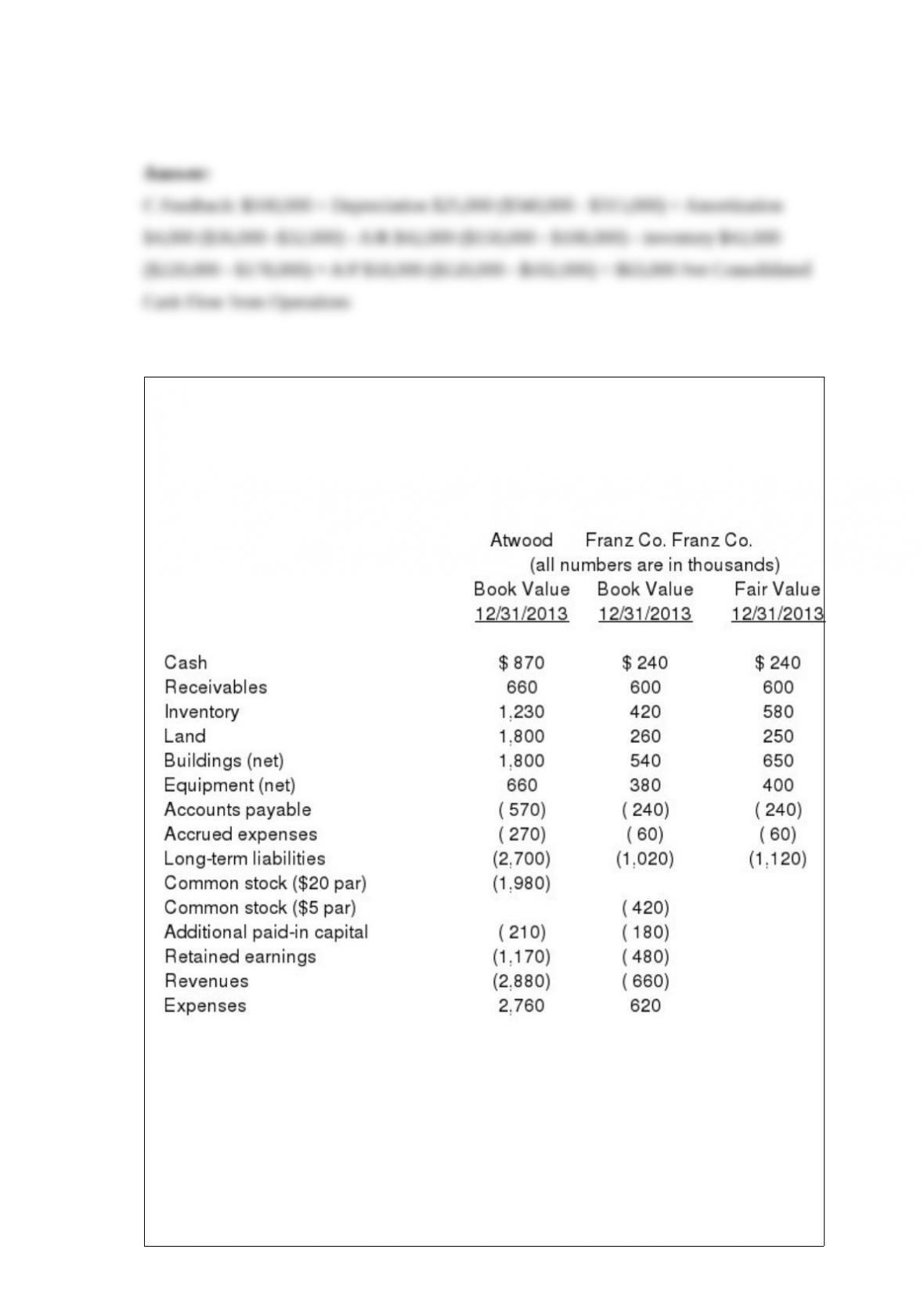

4) Presented below are the financial balances for the Atwood Company and the Franz

Company as of December 31, 2012, immediately before Atwood acquired Franz. Also

included are the fair values for Franz Company’s net assets at that date.

Note: Parenthesis indicate a credit balance

Assume a business combination took place at December 31, 2012. Atwood issued 50

shares of its common stock with a fair value of $35 per share for all of the outstanding

common shares of Franz. Stock issuance costs of $15 (in thousands) and direct costs of

$10 (in thousands) were paid to effect this acquisition transaction. To settle a difference

of opinion regarding Franz’s fair value, Atwood promises to pay an additional $5.2 (in

thousands) to the former owners if Franz’s earnings exceed a certain sum during the

next year. Given the probability of the required contingency payment and utilizing a 4%

discount rate, the expected present value of the contingency is $5 (in thousands).

Compute consolidated expenses at date of acquisition.

A) $2,735.

B) $2,760.

C) $2,770.

D) $2,785.

E) $3,380.

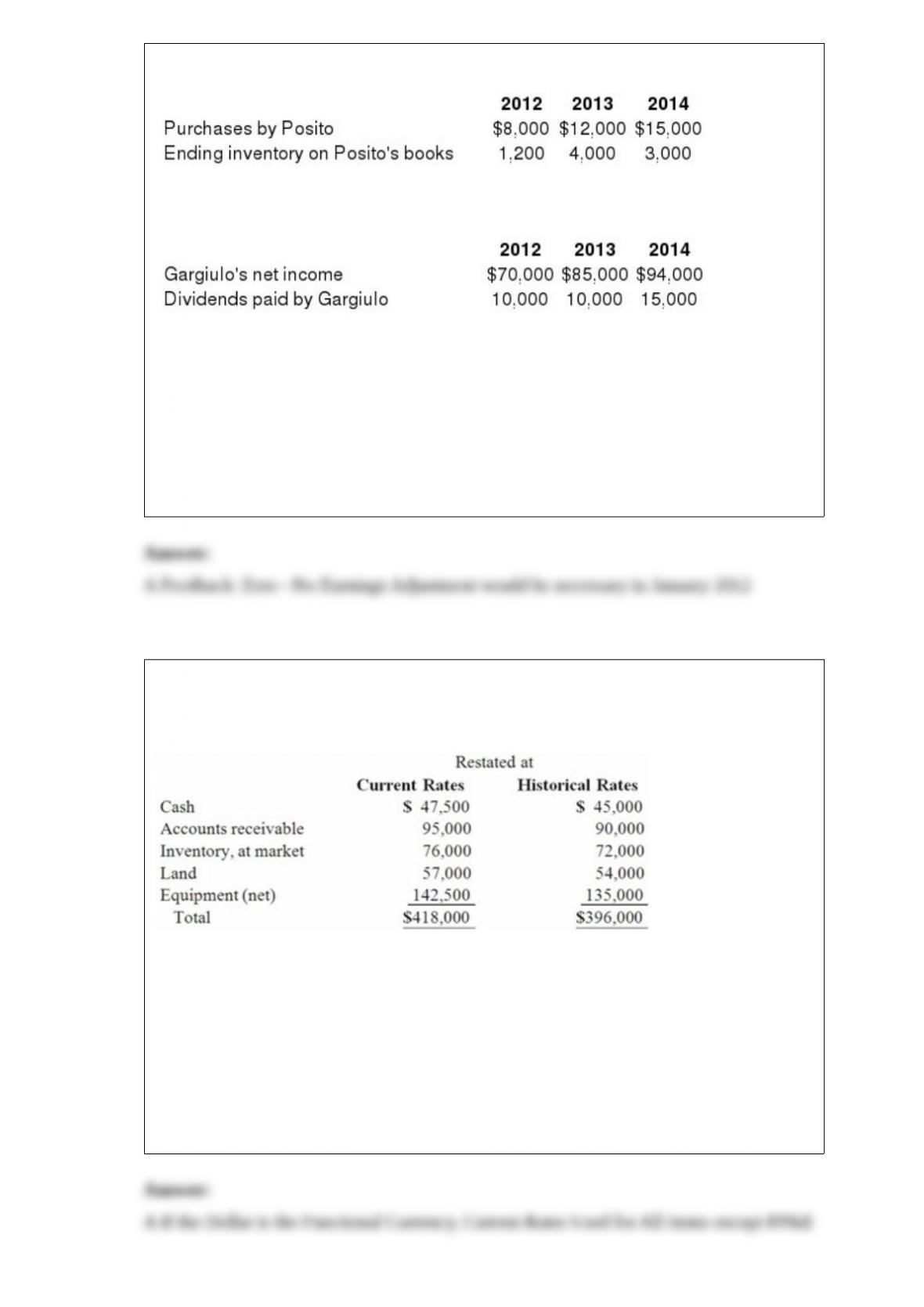

5) Gargiulo Company, a 90% owned subsidiary of Posito Corporation, sells inventory to

Posito at a 25% profit on selling price. The following data are available pertaining to

intra-entity purchases. Gargiulo was acquired on January 1, 2012.

Assume the equity method is used. The following data are available pertaining to

Gargiulo’s income and dividends.

For consolidation purposes, what amount would be debited to January 1 retained

earnings for the 2012 consolidation worksheet entry with regard to the unrealized gross

profit of the 2012 intra-entity transfer of merchandise?

A) $ 0.

B) $1,600.

C) $ 300.

D) $ 240.

E) $ 270.

6) Certain balance sheet accounts of a foreign subsidiary of Parker Company at

December 31, 2013, have been restated into U.S. dollars as follows:

Assuming the functional currency of the subsidiary is the U.S. dollar, what total should

be included in Parker’s consolidated balance sheet at December 31, 2013, for the above

items?

A.$407,500

B.$418,000

C.$396,000

D.$403,500

E.$398,500

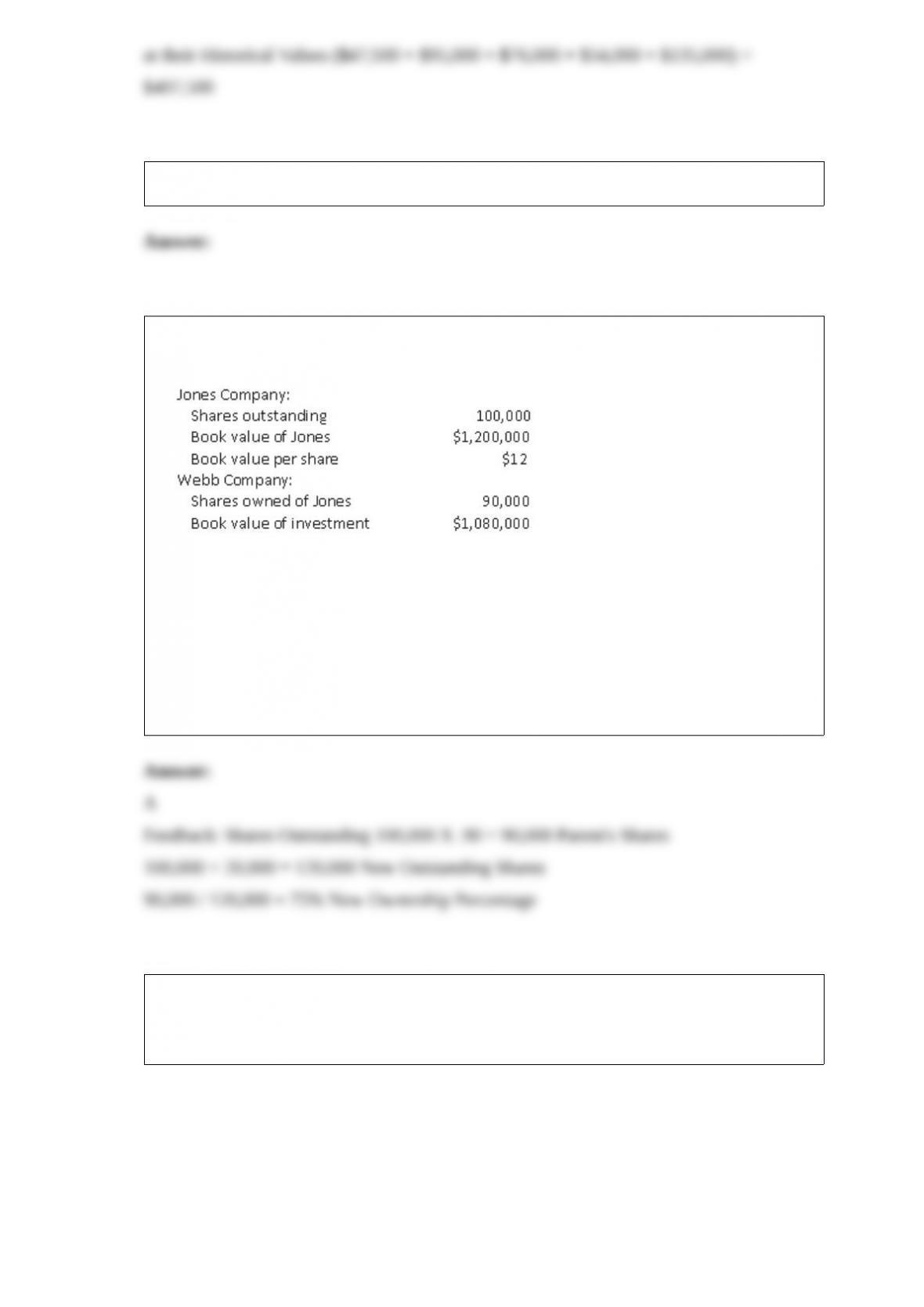

8) Webb Company owns 90% of Jones Company. The original balances presented for

Jones and Webb as of January 1, 2013, are as follows:

Jones sells 20,000 shares of

previously unissued shares of its common stock to outside parties for $10 per share.

What is the new percent ownership of Webb in Jones after the stock issuance?

A) 75%.

B) 90%.

C) 80%.

D) 64%.

E) 60%.

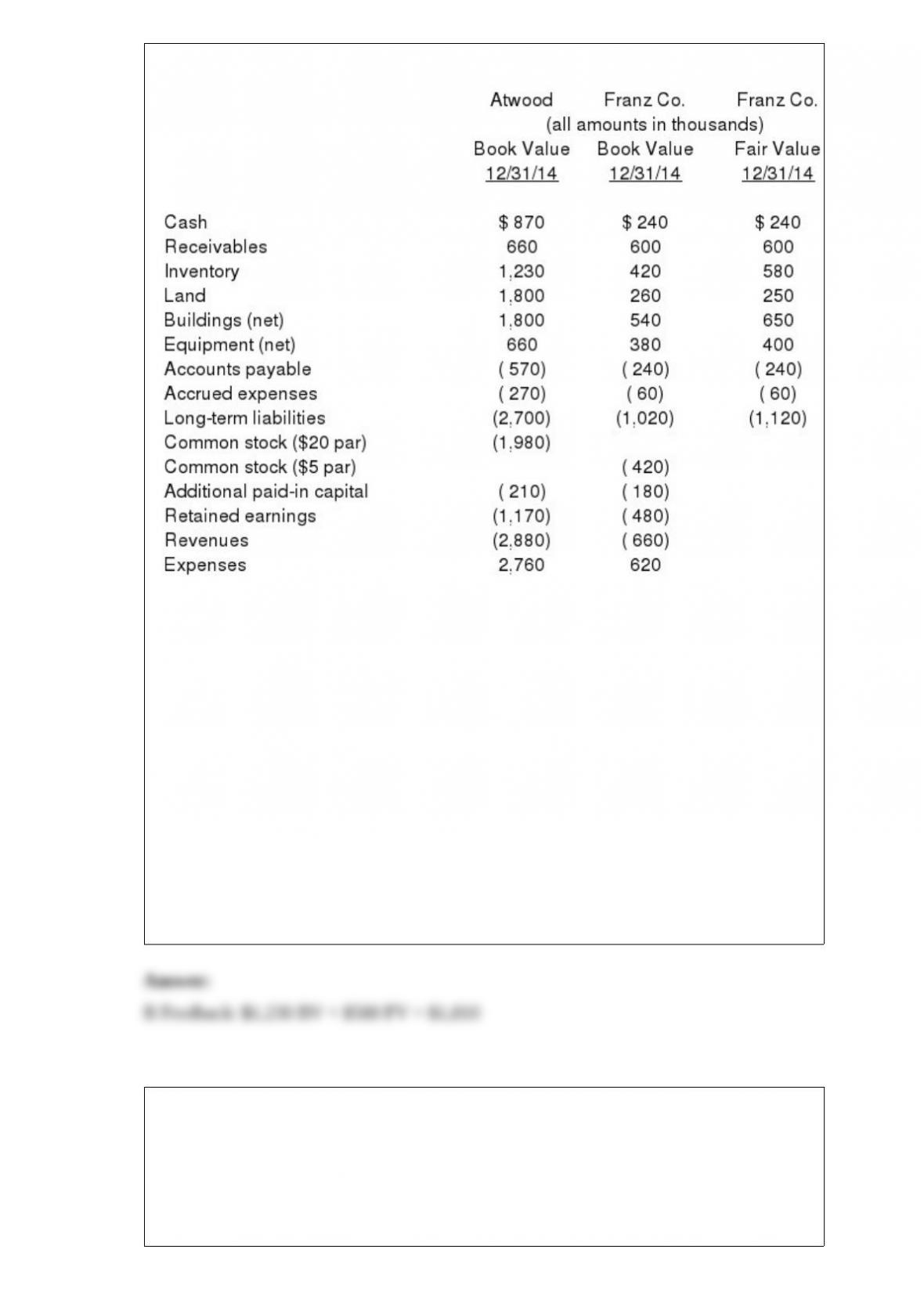

9) Presented below are the financial balances for the Atwood Company and the Franz

Company as of December 31, 2012, immediately before Atwood acquired Franz. Also

included are the fair values for Franz Company’s net assets at that date.

Note: Parenthesis indicate a credit balance

Assume a business combination took place at December 31, 2012. Atwood issued 50

shares of its common stock with a fair value of $35 per share for all of the outstanding

common shares of Franz. Stock issuance costs of $15 (in thousands) and direct costs of

$10 (in thousands) were paid to effect this acquisition transaction. To settle a difference

of opinion regarding Franz’s fair value, Atwood promises to pay an additional $5.2 (in

thousands) to the former owners if Franz’s earnings exceed a certain sum during the

next year. Given the probability of the required contingency payment and utilizing a 4%

discount rate, the expected present value of the contingency is $5 (in thousands).

Compute consolidated inventory at date of acquisition.

A) $1,650.

B) $1,810.

C) $1,230.

D) $ 580.

E) $1,830.

10) Renfroe, Inc. acquires 10% of Stanley Corporation on January 1, 2012, for $90,000

when the book value of Stanley was $1,000,000. During 2012, Stanley reported net

income of $215,000 and paid dividends of $50,000. On January 1, 2013, Renfroe

purchased an additional 30% of Stanley for $325,000. Any excess of cost over book

value is attributable to goodwill with an indefinite life. During 2013, Renfroe reported

net income of $320,000 and paid dividends of $50,000.

What is the balance in the Investment in Stanley Corporation on December 31, 2013?

A) $415,000.

B) $512,500.

C) $523,000.

D) $539,500.

E) $544,500.

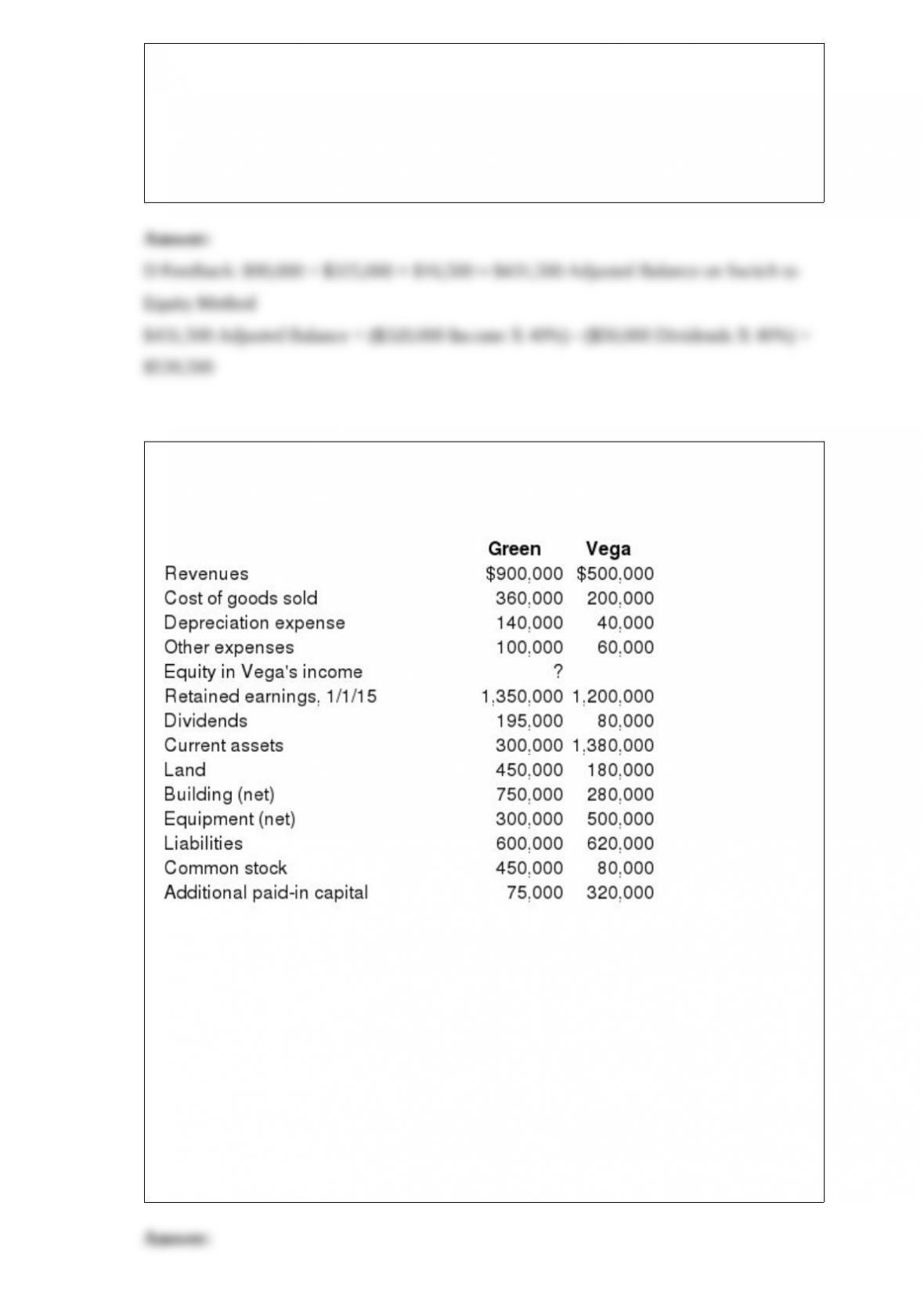

11) Following are selected accounts for Green Corporation and Vega Company as of

December 31, 2015. Several of Green’s accounts have been omitted.

Green acquired 100% of Vega on January 1, 2011, by issuing 10,500 shares of its $10

par value common stock with a fair value of $95 per share. On January 1, 2011, Vega’s

land was undervalued by $40,000, its buildings were overvalued by $30,000, and

equipment was undervalued by $80,000. The buildings have a 20-year life and the

equipment has a 10-year life. $50,000 was attributed to an unrecorded trademark with a

16-year remaining life. There was no goodwill associated with this investment.

Compute the December 31, 2015, consolidated buildings.

A) $1,037,500.

B) $1,007,500.

C) $1,000,000.

D) $1,022,500.

E) $1,012,500.

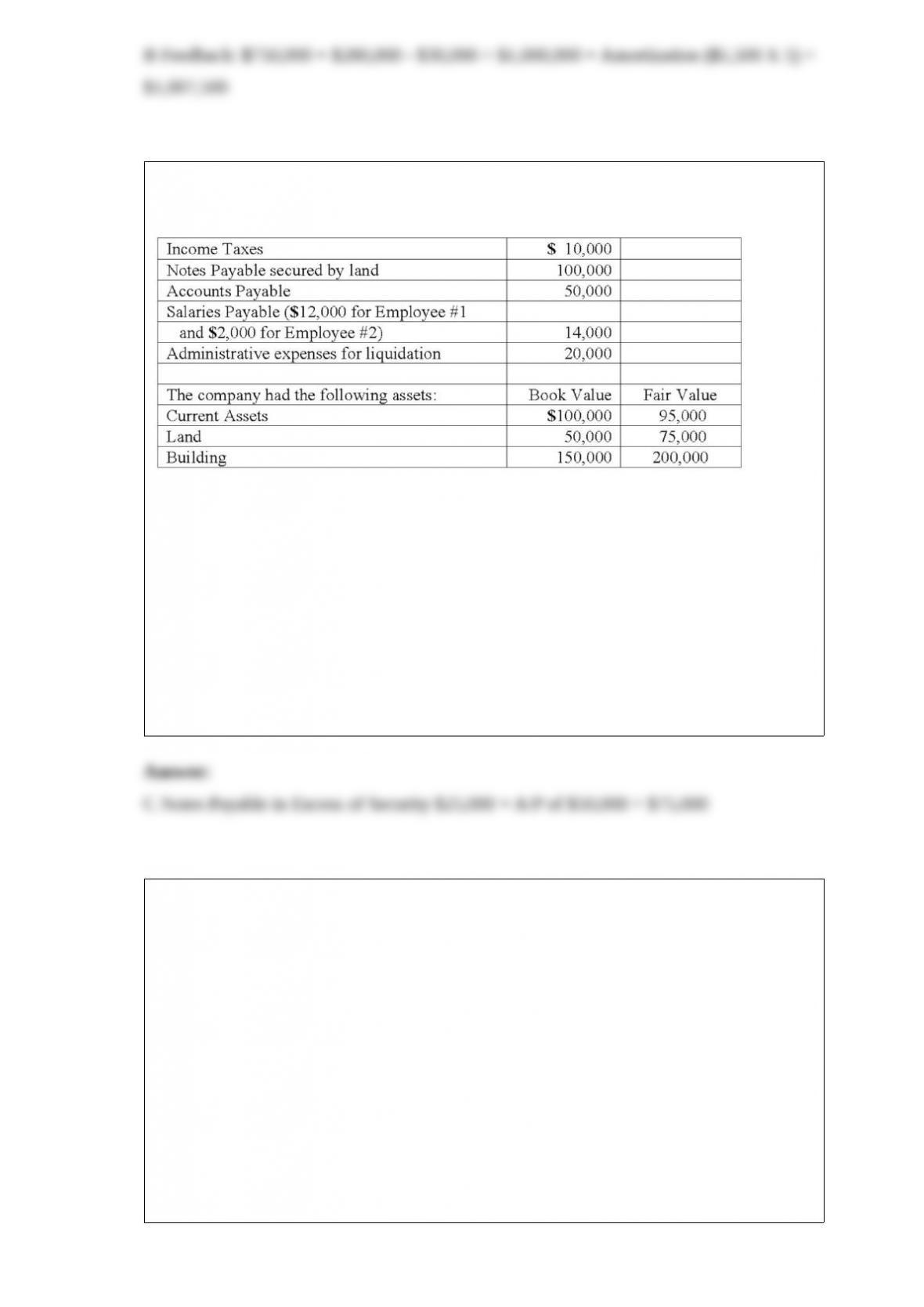

12) A company that was to be liquidated had the following liabilities:

Total unsecured non-priority liabilities are calculated to be what amount?

A.$44,000.

B.$51,050.

C.$75,000.

D.$85,000.

E.$194,000.

13) Goehler, Inc. acquires all of the voting stock of Kenneth, Inc. on January 4, 2012, at

an amount in excess of Kenneth’s fair value. On that date, Kenneth has equipment with

a book value of $90,000 and a fair value of $120,000 (10-year remaining life). Goehler

has equipment with a book value of $800,000 and a fair value of $1,200,000 (10-year

remaining life). On December 31, 2013, Goehler has equipment with a book value of

$975,000 but a fair value of $1,350,000 and Kenneth has equipment with a book value

of $105,000 but a fair value of $125,000.

If Goehler applies the equity method in accounting for Kenneth, what is the

consolidated balance for the Equipment account as of December 31, 2013?

A) $1,080,000.

B) $1,104,000.

C) $1,100,000.

D) $1,468,000.

E) $1,475,000.

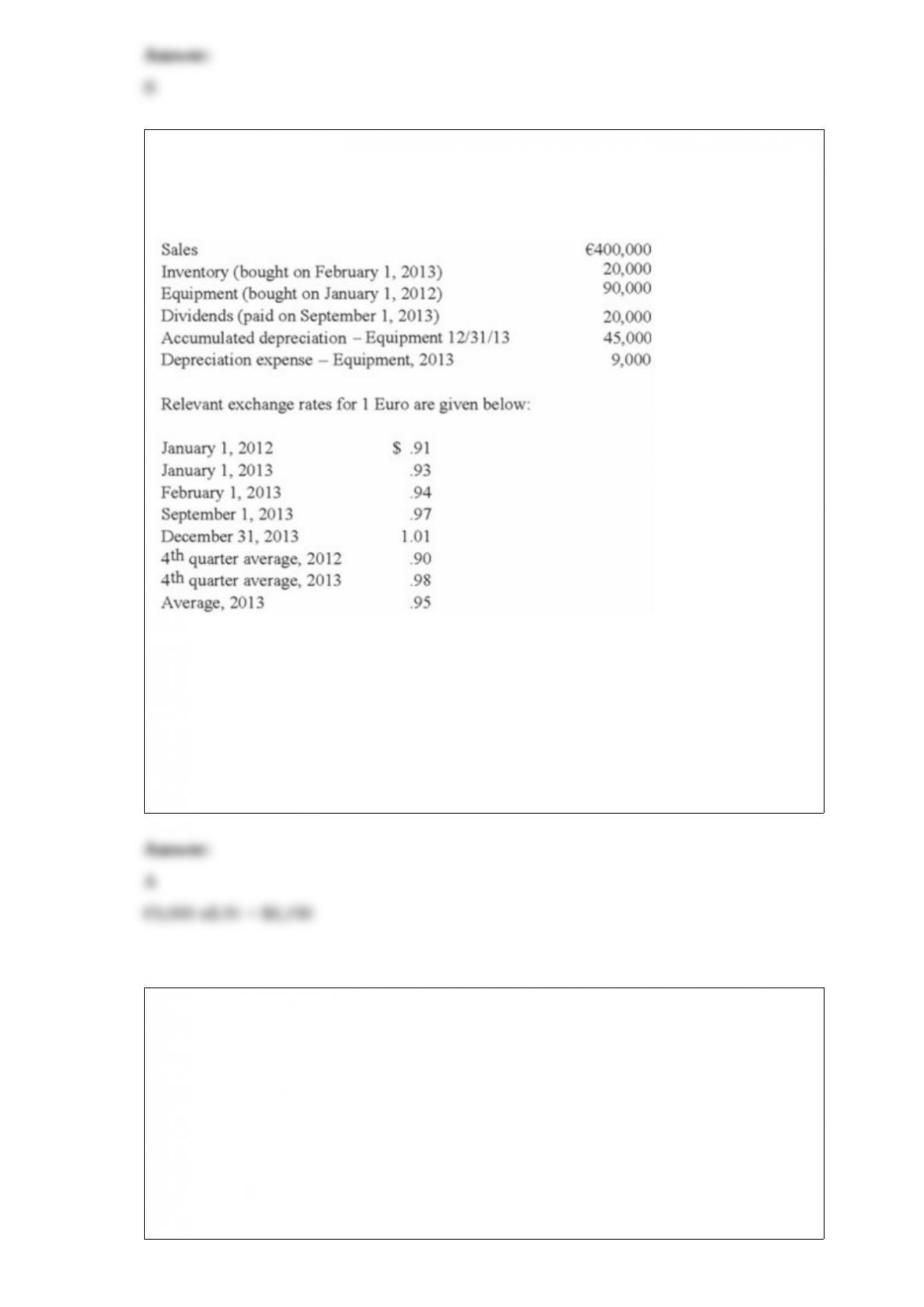

14) Quadros Inc., a Portuguese firm was acquired by a U.S. company on January 1,

2012. Selected account balances are available for the year ended December 31, 2013,

and are stated in Euro, the local currency.

Assume the functional currency is the U.S. Dollar; compute the U.S. income statement

amount for depreciation expense for 2013

A.$8,190

B.$8,370

C.$8,820

D.$9,090

E.$8,550

15) Walsh Company sells inventory to its subsidiary, Fisher Company, at a profit during

2012. One-third of the inventory is sold by Walsh uses the equity method to account for

its investment in Fisher.

In the consolidation worksheet for 2012, which of the following choices would be a

credit entry to eliminate unrealized intra-entity gross profit with regard to the 2012

intra-entity sales?

A) Retained earnings.

B) Cost of goods sold.

C) Inventory.

D) Investment in Fisher Company.

E) Sales.

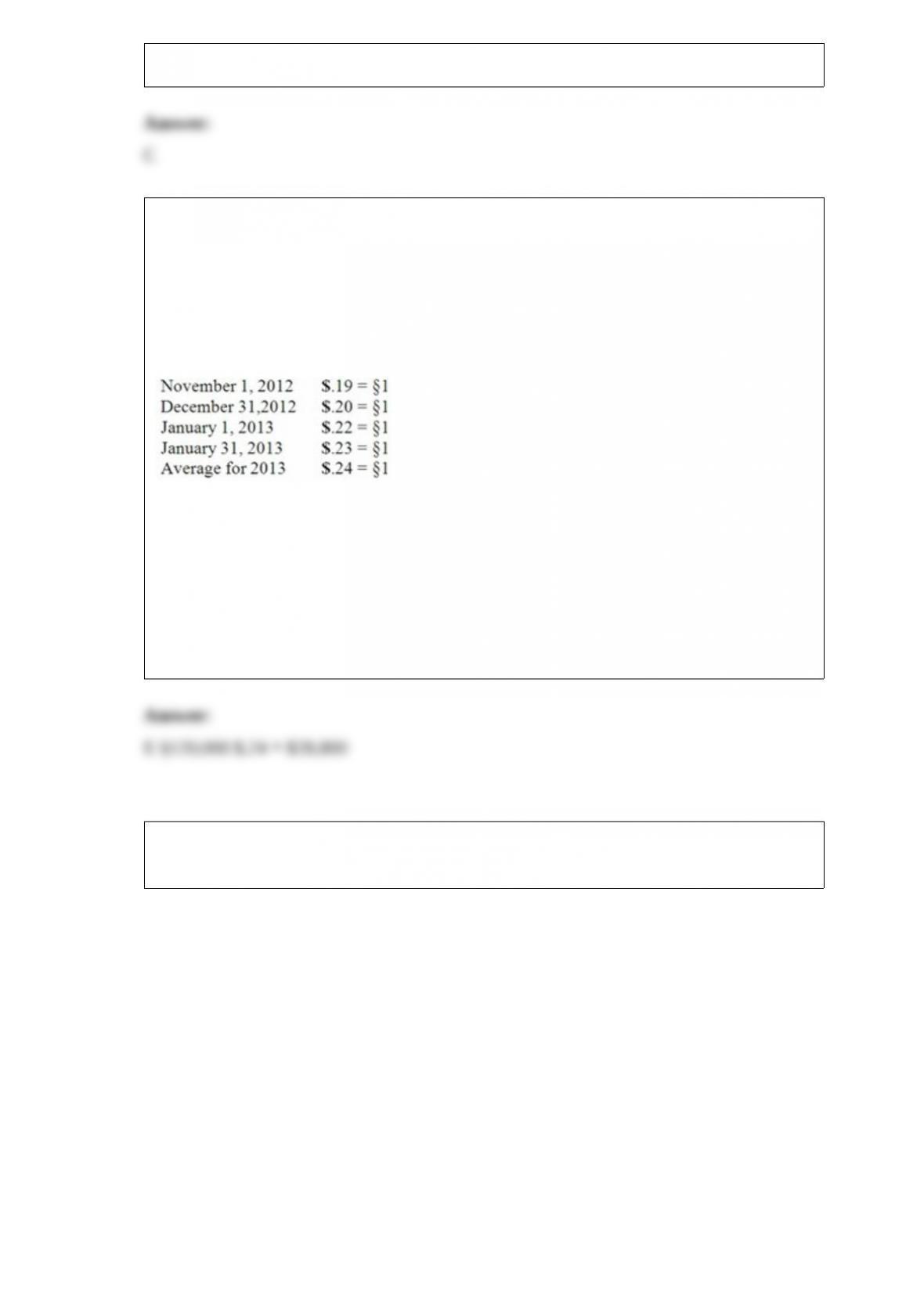

16) A subsidiary of Porter Inc., a U.S. company, was located in a foreign country. The

functional currency of this subsidiary was the Stickle (§), the local currency where the

subsidiary is located. The subsidiary acquired inventory on credit on November 1,

2012, for §120,000 that was sold on January 17, 2013 for §156,000. The subsidiary paid

for the inventory on January 31, 2013. Currency exchange rates between the dollar and

the Stickle were as follows:

What amount would have been reported for cost of goods sold on Porter’s consolidated

income statement at December 31, 2013?

A.$24,000

B.$26,400

C.$22,800

D.$27,600

E.$28,800

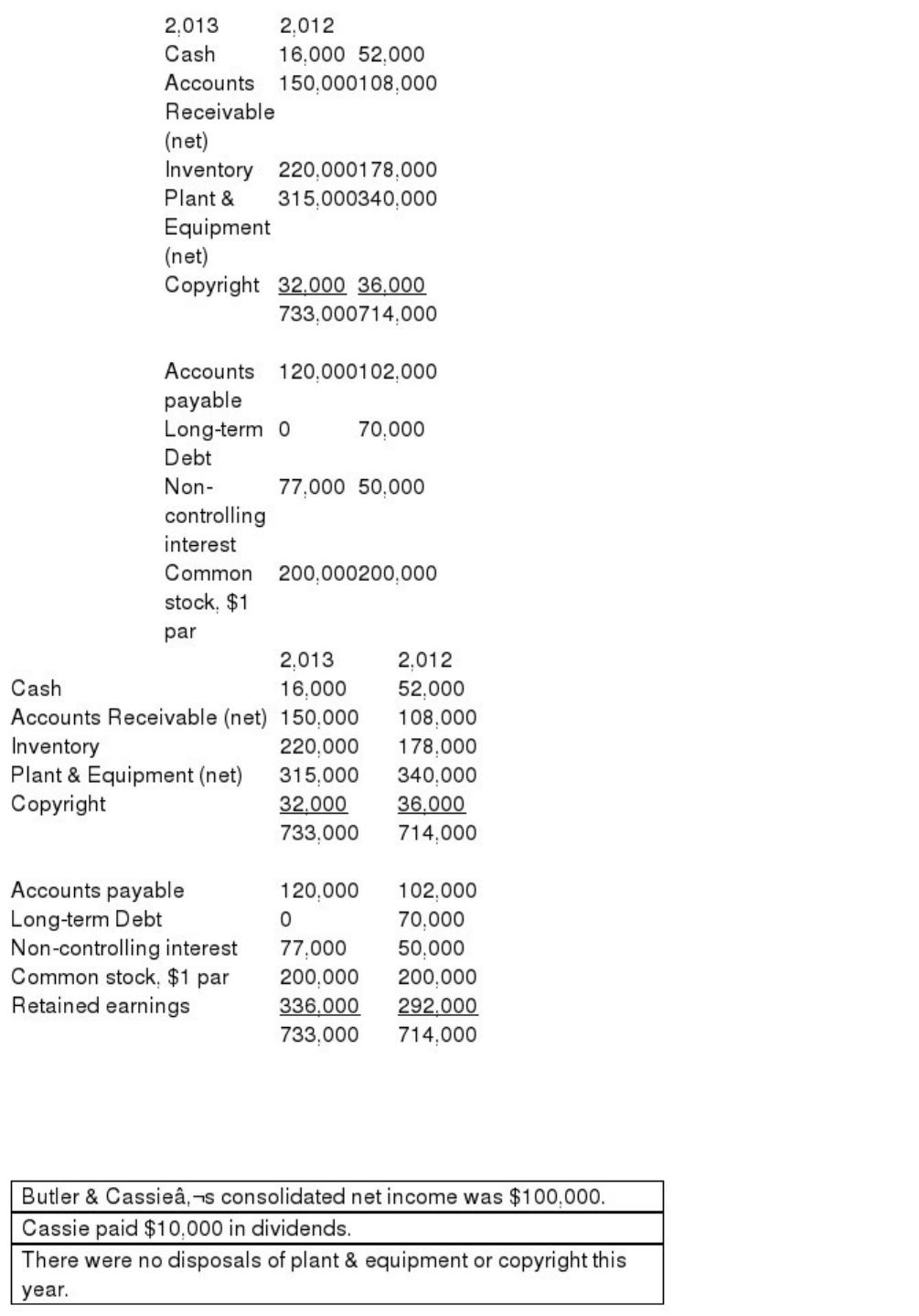

17) The balance sheets of Butler, Inc. and its 70 percent-owned subsidiary, Cassie

Corp., are presented below:

Additional information for 2013:

Net cash flow from operating activities was:

A) $92,000.

B) $27,000.

C) $63,000.

D) $29,000.

E) $34,000.

18) The financial balances for the Atwood Company and the Franz Company as of

December 31, 2013, are presented below. Also included are the fair values for Franz

Company’s net assets.

Note: Parenthesis indicate a credit balance

Assume an acquisition business combination took place at December 31, 2013. Atwood

issued 50 shares of its common stock with a fair value of $35 per share for all of the

outstanding common shares of Franz. Stock issuance costs of $15 (in thousands) and

direct costs of $10 (in thousands) were paid.

Compute consolidated equipment (net) at the date of the acquisition.

A) $ 400.

B) $ 660.

C) $1,060.

D) $1,040.

E) $1,050.

19) A company sells a building to a bank in 2013 at a gain of $100,000 and immediately

leases the building back for period of five years. The lease is accounted for as an

operating lease. The building was originally purchased for $200,000 and currently had a

book value of $50,000 at the date of the sale.

As a result of the sale and leaseback transaction in 2013, what is the difference between

income using U.S. GAAP and IFRS in 2013?

A.U.S. GAAP income is $80,000 higher.

B.U.S. GAAP income is $100,000 higher.

C.IFRS income is $50,000 lower.

D.IFRS income is $100,000 lower.

E.IFRS income is $80,000 higher.

20) McGraw Corp. owned all of the voting common stock of both Ritter Co. and

Lawler Co. During 2013, Ritter sold inventory to Lawler. The goods had cost Ritter

$65,000, and they were sold to Lawler for $100,000. At the end of 2013, Lawler still

held 30% of the inventory.

Required:

How should the sale between Lawler and Ritter be accounted for in a consolidation

worksheet? Show worksheet entries to support your answer.

21) Varton Corp. acquired all of the voting common stock of Caleb Co. on January 1,

2013. Varton owned some land with a book value of $84,000 that was sold to Caleb for

its fair value of $120,000. How should this transaction be accounted for by the

consolidated entity?

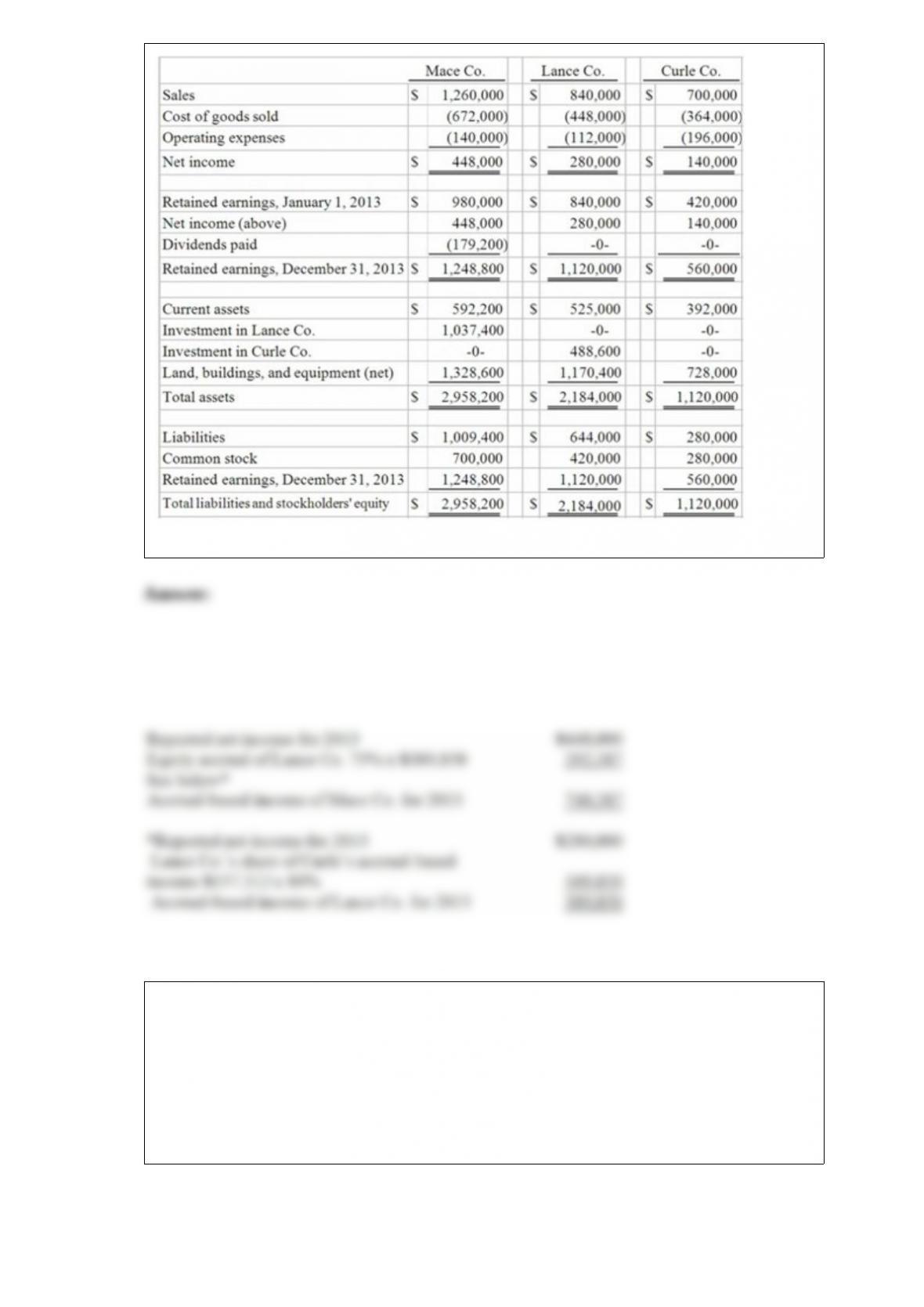

22) On January 1, 2012, Mace Co. acquired 75% of Lance Co.’s outstanding common

stock. On the same date, Lance acquired an 80% interest in Curle Co. Both of these

investments were acquired when book value was equal to fair value of identifiable net

assets acquired. Both of these investments were accounted using the initial value

method. No dividends were distributed by either Lance or Curle during 2012 or 2013.

Mace paid cash dividends each year equal to 40% of operating income. Reported

operating income totals for 2012 were as follows:

Following are the 2013 financial statements for these three companies. Curle made

numerous transfers of inventory to Lance since the takeover: $112,000 (2012) and

$140,000 (2013). These transactions included the same markup applicable to Curle’s

outside sales. In each of these years, Lance carried 20% of this inventory into the

succeeding year before disposing of it.

An effective income tax rate of 45% was applicable to all companies.

Determine the accrual-based income of Mace Co. for the year 2013.

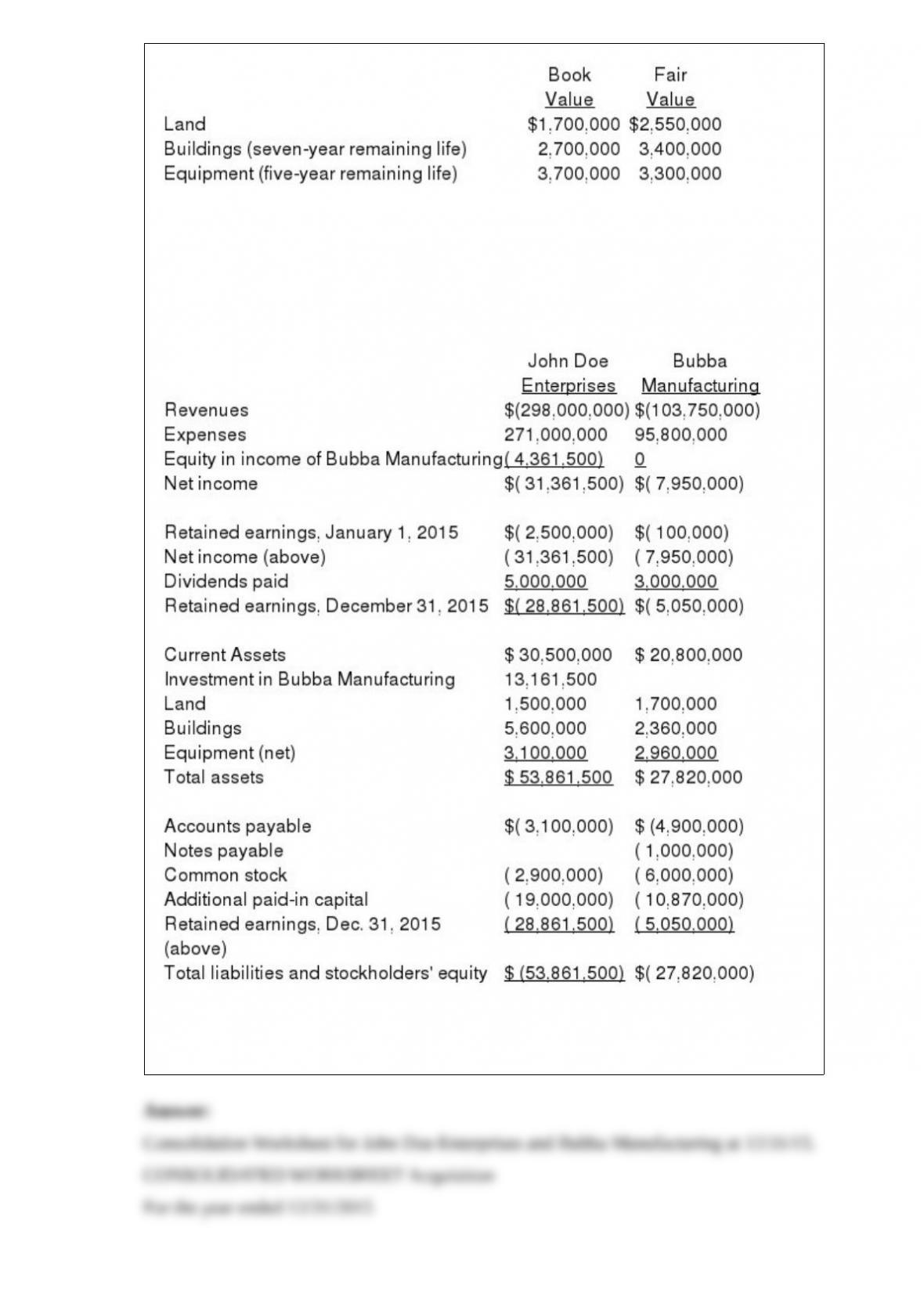

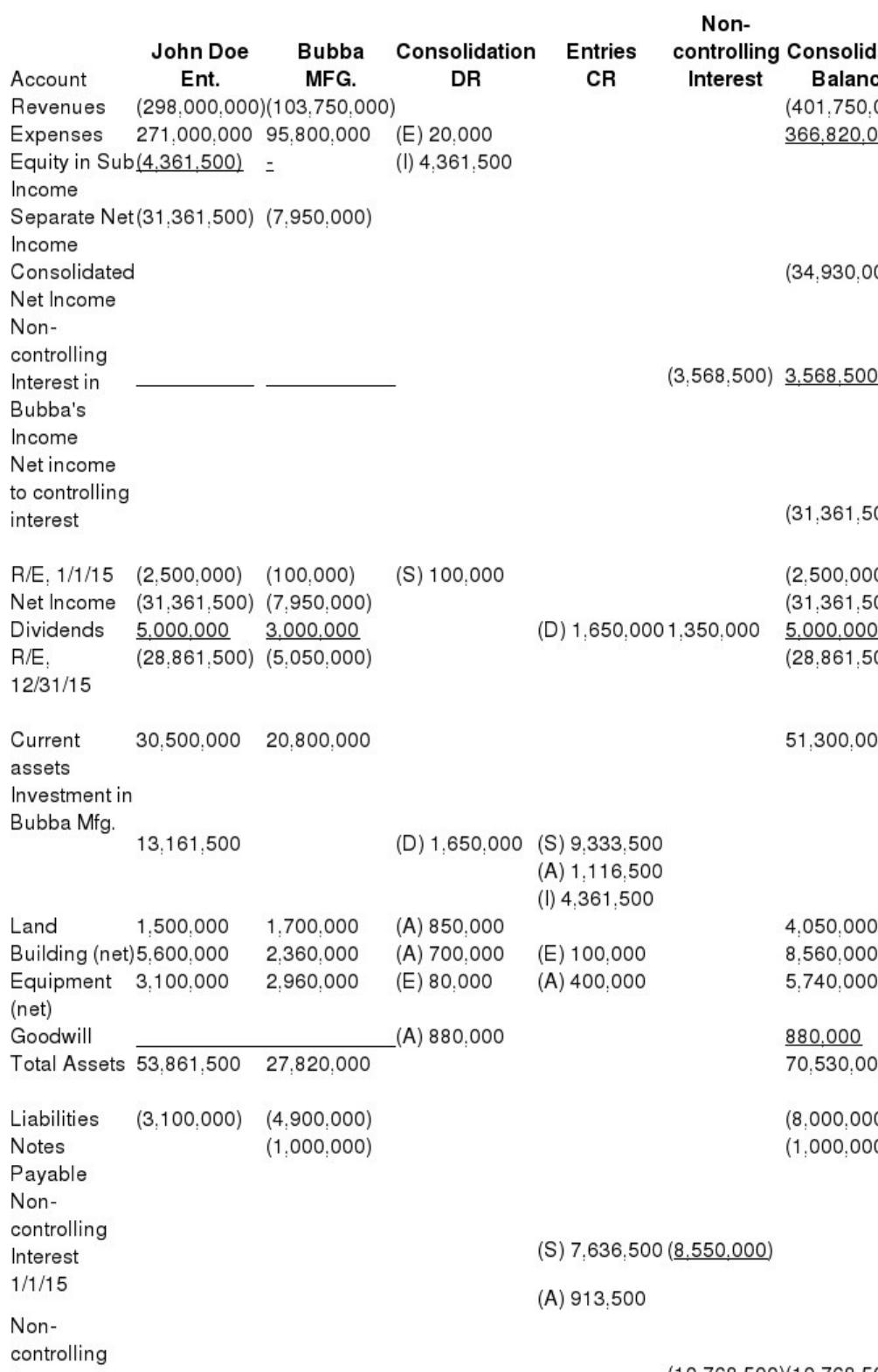

23) On January 1, 2015, John Doe Enterprises (JDE) acquired a 55% interest in Bubba

Manufacturing, Inc. (BMI). JDE paid for the transaction with $3 million cash and

500,000 shares of JDE common stock (par value $1.00 per share). At the time of the

acquisition, BMI’s book value was $16,970,000.

On January 1, JDE stock had a market value of $14.90 per share and there was no

control premium in this transaction . Any consideration transferred over book value is

assigned to goodwill. BMI had the following balances on January 1, 2015.

For internal reporting purposes, JDE employed the equity method to account for this

investment.

The following account balances are for the year ending December 31, 2015 for both

companies.

Required:

Prepare a consolidation worksheet for this business combination. Assume goodwill has

been reviewed and there is no goodwill impairment.

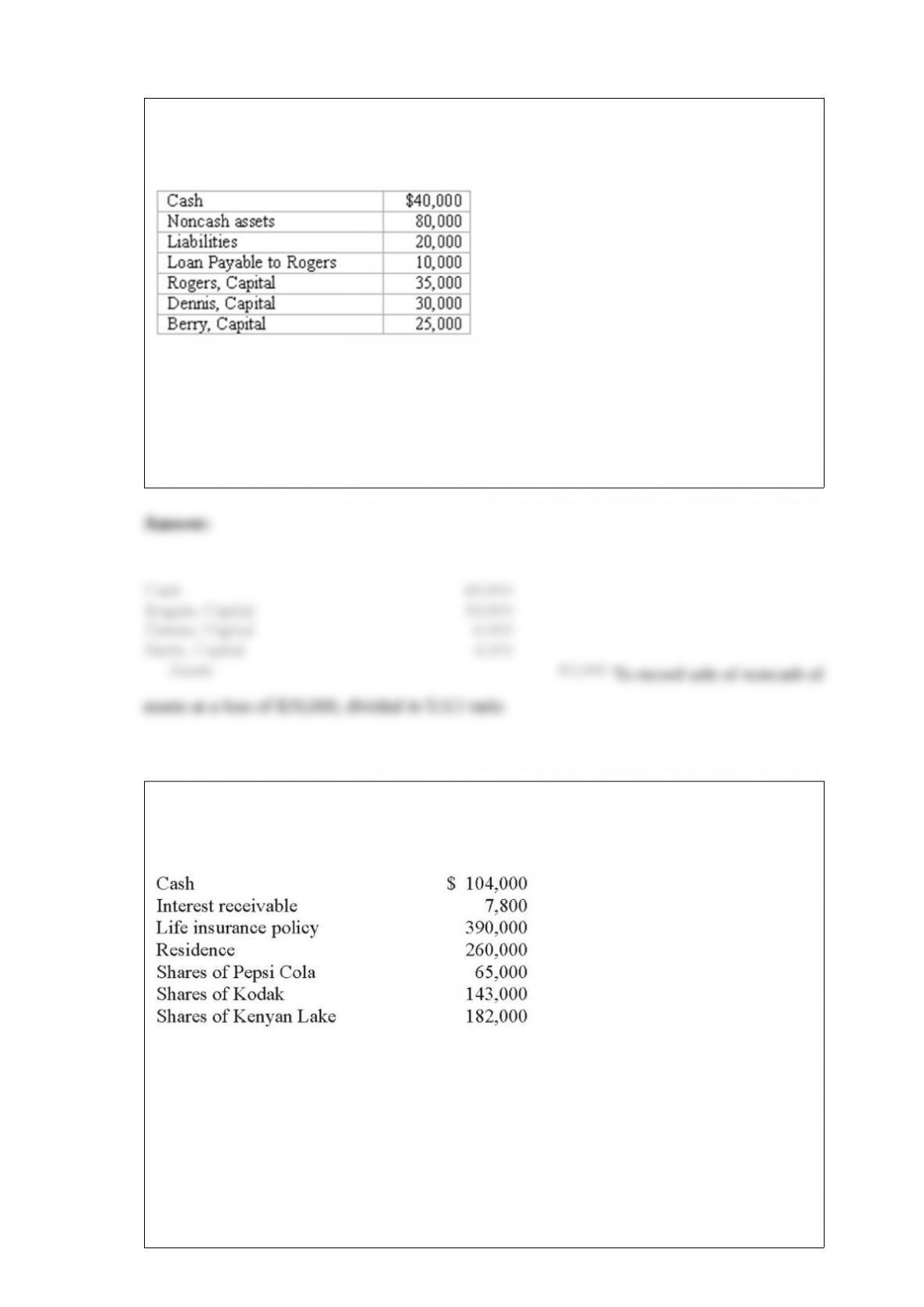

24) The balance sheet of Rogers, Dennis & Berry LLP prior to liquidation included the

following:

The three partners shared net income and losses in a 5:3:2 ratio, respectively. Noncash

assets were sold for $60,000. Creditors were paid in full, partners were paid $35,000,

and the balance of cash was retained pending future developments.

Record the journal entry for the sale of the noncash assets.

25) The executor of the Estate of Kate Tweed discovered the following assets (at fair

value):

The will of Kate Tweed had the following provisions:

-$195,000 in cash went to Victor Vickery.

-All shares of PepsiCo went to Duchess Doyle.

-The residence went to Louis Tweed.

-All other estate assets were to be liquidated with the resulting cash going to the Sacred

Church of Liberty, Missouri.

For the Estate of Kate Tweed, interest of $9,100 was collected.

Prepare the journal entry to record the collection.