46.(40 Minutes) (Compute basic and diluted earnings per share. Subsidiary has

stock warrants outstanding and convertible debt.)

Basic EPS—Austin, Inc.

Consolidated net income to parent….…..…..…..…..…..… $284,000

Austin’s preferred dividends …………………………..………. (40 ,000)

Diluted EPS—Austin, Inc.

Subsidiary earnings and shares for Austin’s diluted EPS calculation:

Rio Grande net income after amortization……………..…. $105,000

Interest saved assuming conversion of bonds

(net of tax) ………..……………….……………………..…..…... 22 ,000

Net income applicable to diluted EPS ………..…..…..…... $127 ,000

Shares outstanding …………..…………………….…..…..…..… 30,000

Shares controlled by parent (24,000 plus 50% of incre-

ment created by warrants [or 1,250]) ..…..…..…........ 25,250

Portion owned by parent (25,250 ÷ 42,500) …………..….. 59.4% (rounded)

Net income applicable to parent—diluted EPS

Austin’s outstanding common shares ..…..…..…..…..…. 50,000

Assumed conversion of preferred stock

(10,000 × 2 shares) …………..…………….………..…..….... 20,000

Shares applicable to diluted EPS ……………….……………. 70,000

Diluted earnings per share ($275,438 ÷ 70,000) …..…..….... $3.93 (rounded)

47.(50 Minutes) (Determine consolidated totals. Subsidiary has preferred shares

outstanding that are equity instruments.)

Annual amortization $11,000

Ending Unrealized Gain

Ending inventory (at transfer price) ……………..………….. $18,000

Historical cost:

Recorded value………..………………..……………….………………..………… $30,000

Depreciation expense ($12,000 ÷ 4)………………………..…..………..… $3,000

Accumulated depreciation ($18,000 + $3,000)…….…..…..…..……… $21,000

47. (continued)

Paisley, Inc. and Skyler Corp.

Consolidation Worksheet

Year Ending December 31, 2014

Consolidation Entries Consolidated

Accounts Paisley, Inc. Skyler Corp. Debit Credit Totals

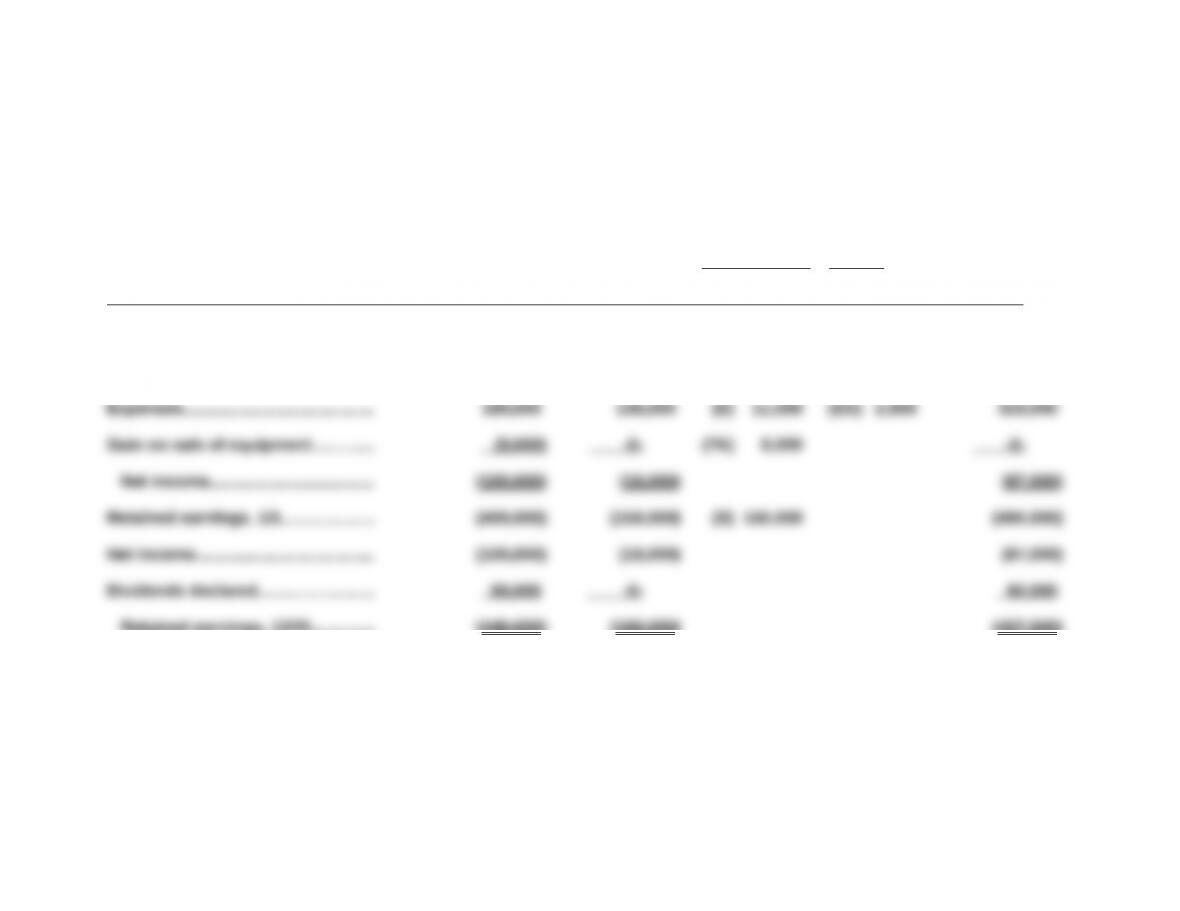

Sales…….…….…….…....…............….. (800,000) (400,000) (TI) 90,000 (1,110,000)

Cost of goods sold......…................ 528,000 260,000 (G) 6,000 (TI) 90,000 704,000

Retained earnings, 12/31............. (440 ,000) (160 ,000) (427 ,000)

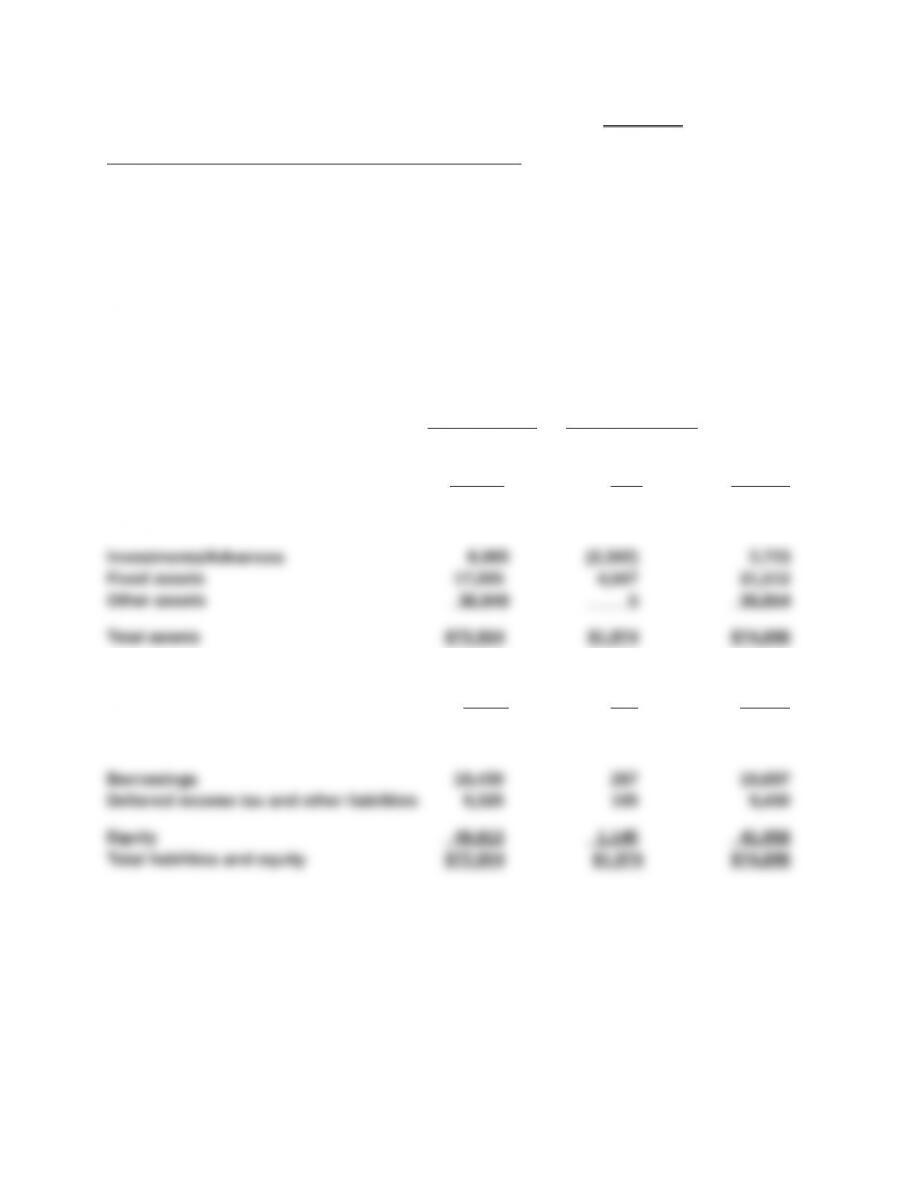

Cash……………………………….………… 30,000 40,000 70,000

Accounts receivable……........…...... 300,000 100,000 (P) 28,000 372,000

Inventory…………………………………... 260,000 180,000 (G) 6,000 434,000

Investment in Skyler Corp….....…... 560,000 -0- (S) 450,000 -0-

Land, buildings, and equipment.... 680,000 500,000 (TA) 10,000 1,190,000

Accumulated depreciation............. (180,000) (90,000) (ED) 2,000 (TA) 18,000 (286,000)

Intangible Asset….…............…........ -0- -0- (A) 110,000 (E) 11,000 99 ,000

Total assets……........…..........….... 1 ,650,000 730 ,000 1 ,879,000

Accounts payable…..........…........... (140,000) (90,000) (P) 28,000 (202,000)

Total liab. and stockholders’ equity (1 ,650,000) (730 ,000) 715,000 715,000 (1 ,879,000)

47. (continued)

CONSOLIDATED TOTALS

Sales = $1,110,000 (add book values and eliminate intra-entity transfers)

Cost of Goods Sold = $704,000 (add book values, eliminate intra-entity

transfers, and eliminate ending unrealized gain [computed above])

subsidiary was not acquired until current year)

Dividends Declared = $60,000 (parent balance only)

Retained Earnings, 12/31 = $427,000 (consolidated beginning retained

earnings plus net income less dividends declared)

Cash = $70,000 (add book values)

Intangible Asset = $99,000 (original allocations less one year amortization)

Total Assets = $1,879,000 (summation of consolidated accounts)

Retained Earnings, 12/31 = $427,000 (computed above)

Total Liabilities and Equities = $1,879,000 (summation of consolidated

accounts)

47. (continued): Consolidation entries and explanations:

Entry S

Preferred Stock (Skyler)…..…….…….…….…….….…............ 100,000

Common Stock (Skyler)………….…….…......…..........…....... 200,000

Entry E

Amortization Expense…….…….…….…….…….............…..... 11,000

Intangible Asset….…….…….…….…….…............…......... 11,000

(To record current year’s amortization of intangible asset.)

Entry P

Accounts Payable……………………………………………….……. 28,000

Accounts Receivable…………………………………………… 28,000

(To eliminate intra-entity debt.)

Entry TA

Entry G

Cost of Goods Sold…..…….…….…….……...…............…...... 6,000

Inventory…………………………………………………………….. 6,000

(To defer unrealized intra-entity gain remaining at the end of the current year. Markup

is 33⅓% [30,000 gross profit ÷ 90,000 transfer price] indicating that the ending inventory of

18,000 contains an unrealized profit of 6,000 [18,000 × 33⅓%].)

Entry ED

Accumulated Depreciation………………………………………... 2,000

Depreciation Expense………………………………………….. 2,000

48. (30 minutes) (Consolidated Cash Flow Statement with current year business

combination)

Plaster Inc. and Subsidiary Stucco Company

Consolidated Statement of Cash Flows

For the year ended 12/31/14

CASH FLOW FROM OPERATING ACTIVITIES

Consolidated net income $274,000

Depreciation expense 187,500

Net cash flow provided by operating activities $363,850

CASH FLOW FROM INVESTING ACTIVITIES

Purchase of Stucco Company assets (net of cash acquired)

Net cash flow used in investing activities (856,000)

CASH FLOW FROM FINANCING ACTIVITIES

Net cash flow provided by financing activities $692 ,000

Increase in cash 1/1/14 to 12/31/14 $199,850

Excel Case–Intra-entity Bonds

Bonds with a stated rate of 11% sold to yield 12%

Eff. Yield

12% 1,000,000.00 0.32197 321,973.24

110,000.00 5.65022 621,524.53

943,497.77 56,502.23

2016 958,885.93 115,066.31 110,000.00 5,066.31

2017 963,952.24 115,674.27 110,000.00 5,674.27

Consolidated Worksheet Entry 12 /31/14

Bonds Payable 954,362.43

Interest Income 117,523.20

Loss on Retirement 0.00

Bonds retired by affiliate on 1/1/14 at 904,024.59

Eff. Yield

13% 1,000,000.00 0.37616 376,159.86

110,000.00 4.79877 527,864.73

904,024.59 95,975.41

2014 904,024.59 117,523.20 110,000.00 7,523.20

2015 911,547.79 118,501.21 110,000.00 8,501.21

2016 920,049.00 119,606.37 110,000.00 9,606.37

1,000,000.00 95,975.41

Financial Reporting Research and Analysis Case

The number of potential solutions is large. Searches in Lexis-Nexis, Edgar, etc. will

produce numerous examples of consolidations of VIEs. For example, Walt Disney

Company prepares a before and after disclosure of its consolidated VIEs Euro

Disney, Hong Kong Disneyland, and Shanghai Disney Resort as follows (9-29-12):

Before International International

Theme Parks Theme Parks

Consolidation and Adjustments

Cash and cash equivalents $2,839 $548 $ 3,387

Other current assets 10,066 256 10,322

Total current assets 12,905 804 13,709

Current portion of borrowings 3,614 -0- 3,614

Other current liabilities 8,742 457 9,199

Total current liabilities 12,356 457 12,813