24. (20 Minutes) (Determine selected consolidated balances)

Under the acquisition method, the shares issued by Wisconsin are recorded at

fair value using the following journal entry:

Investment in Badger (value of debt and shares issued). 900,000

Common Stock (par value)……………………..…………….… 150,000

Additional Paid-In Capital……………..…………….…..…..…..…. 40,000

Cash ………………..………..……….………..………..………..…... 70,000

Allocation of Acquisition-Date Excess Fair Value:

Consideration transferred (fair value) for Badger Stock $900,000

Book Value of Badger, 6/30……………….……….……………..…. 770 ,000

Net income (adjusted for professional services expense. The

figures earned by the subsidiary prior to the takeover

are not included)…………………..………..……….………..………..……. $ 210,000

Retained earnings, 1/1 (the figures earned by the subsidiary

prior to the takeover are not included)…………..…..…..…..….... 800,000

Additional Paid-in Capital (the parent’s book value

after recording the two entries above)……………….……….…..… 680,000

25. (20 minutes) (Preparation of a consolidated balance sheet)*

CASEY COMPANY AND CONSOLIDATED SUBSIDIARY KENNEDY

Worksheet for a Consolidated Balance Sheet

January 1, 2015

Casey Kennedy Adjust. & Elim. Consolidated

Cash 457,000 172,500 629,500

Accounts receivable 1,655,000 347,000 2,002,000

Inventory 1,310,000 263,500 1,573,500

Investment in Kennedy 3,300,000 -0- (S) 2,600,000

(A) 700,000 -0-

Buildings (net) 6,315,000 2,090,000 (A) 382,000 8,787,000

Licensing agreements -0- 3,070,000 (A) 108,000 2,962,000

Accounts payable (394,000) (393,000) (787,000)

Long-term debt (3,990,000) (2,950,000) (6,940,000)

Common stock (3,000,000) (1,000,000) (S) 1,000,000 (3,000,000)

Additional paid-in cap. -0- (500,000) (S) 500,000 -0-

Retained earnings (6 ,000,000) (1 ,100,000) (S) 1 ,100,000 (6 ,000,000)

*Although this solution uses a worksheet to compute the consolidated amounts, the

problem does not require it.

26. (50 Minutes) (Determine consolidated balances for a bargain purchase.)

a. Marshall’s acquisition of Tucker represents a bargain purchase because

the fair value of the net assets acquired exceeds the fair value of the

consideration transferred as follows:

Fair value of net assets acquired $515,000

In a bargain purchase, the acquisition is recorded at the fair value of the

Investment in Tucker……………….………..……..….…... 515,000

Long-term Liabilities…………….………..……….………..………..…... 200,000

Common Stock (par value)…………………………….…..….…..…... 20,000

26. (continued)

Professional Services Expense…..…..…..…..…... 30,000

Cash ………………..………..……….………..………… 30,000

(to record payment of professional fees)

Additional Paid-In Capital……………..……….…..…. 12,000

Cash ………………..………..……….………..………… 12,000

(To record payment of stock issuance costs)

Marshall’s trial balance is adjusted for these transactions (as shown in the

worksheet that follows).

Book value (assets minus liabilities or

total stockholders’ equity)…………..………..……..…..….…..…. 460 ,000

Book value in excess of consideration transferred ......... (60,000)

Allocation to specific accounts based on fair value:

Inventory…………………..………..……….………….…..….... 5,000

CONSOLIDATED TOTALS

Cash = $38,000. Add the two book values less acquisition and stock issue

costs

Receivables = $360,000. Add the two book values.

Inventory = $505,000. Add the two book values plus the fair value

adjustment

Total assets = $2,183,000. Summation of the above individual figures.

Accounts payable = $190,000. Add the two book values.

Long-term liabilities = $830,000. Add the two book values plus the debt

incurred by the parent in acquiring the subsidiary.

Common stock = $130,000.The parent’s book value after stock issue to

acquire the subsidiary.

26. (continued)

b. MARSHALL COMPANY AND CONSOLIDATED SUBSIDIARY

Worksheet

January 1, 2015

Marshall Tucker Consolidation Entries Consolidated

Accounts Company* Company Debit Credit Totals

Inventory ………..………..…………… 360,000 140,000 (A) 5,000 505,000

Land ………………….…..…..…..….... 200,000 180,000 (A) 20,000 400,000

Buildings (net) …………..………….. 420,000 220,000 (A) 30,000 670,000

Equipment (net) ….…..…..…..…... 160,000 50,000 210,000

Investment in Tucker ….…..…..… 515,000 (S) 460,000

(A) 55,000 -0-

Total assets ……..…..…..…..…..…. 1,943,000 700,000 2,183,000

Accounts payable…………..…..…. (150,000) (40,000) (190,000)

Long-term liabilities …............... (630,000) (200,000) (830,000)

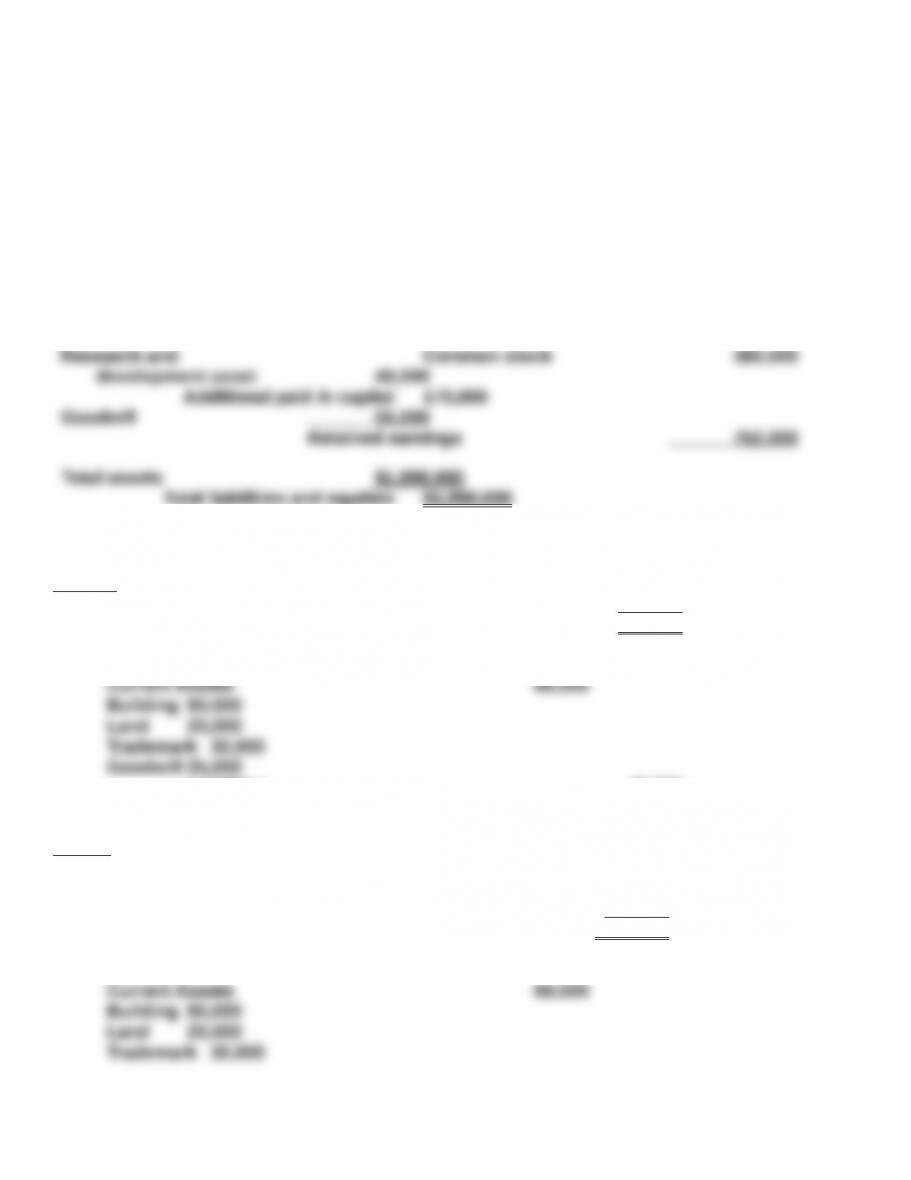

27. (Prepare a consolidated balance sheet)

Consideration transferred at fair value………….….…..… $495,000

Book value ……..………..………..……….……………….…..….. 265,000

Excess fair over book value…………..……….…………..….. 230,000

Allocation of excess fair value to

to notes payable………..………..…………..…..…..….. (5 ,000) 175,000

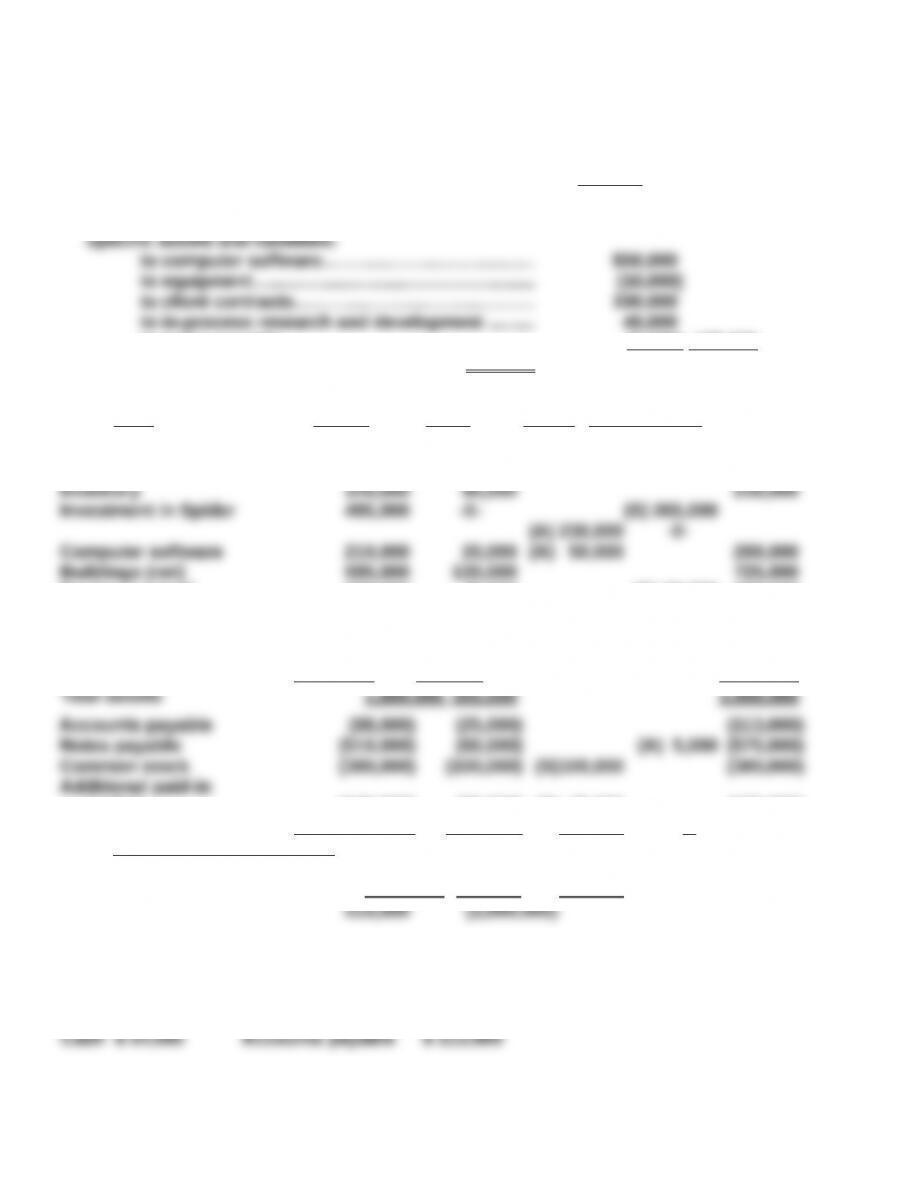

Goodwill ………..………..……….……………..…...$ 55,000

Pratt Spider Debit Credit Consolidated

Cash 36,000 18,000 54,000

Receivables 116,000 52,000 168,000

Equipment (net) 308,000 40,000 (A) 10,000 338,000

Client contracts -0- -0- (A) 100,000 100,000

Research and

devlopment asset -0- -0- (A) 40,000 40,000

Goodwill -0- -0 – (A) 55,000 55 ,000

capital (170,000) (25,000) (S) 25,000 (170,000)

Retained earnings (752 ,000) (140 ,000) (S)140 ,000

(752 ,000)

Total liabilities

and equities (1 ,900,000)(350 ,000) 510 ,000

27. (continued) Pratt Company and Subsidiary

Consolidated Balance Sheet

December 31, 2015

Assets Liabilities and Owners’ Equity

Receivables 168,000

Notes payable 575,000

Inventory 230,000

Computer software 280,000

Buildings (net) 725,000

Equipment (net) 338,000

Client contracts 100,000

28. (15 minutes) (Acquisition method entries for a merger)

Case 1: Fair value of consideration transferred $145,000

Fair value of net identifiable assets 120,000

Excess to goodwill $25,000

Case 1 journal entry on Allerton’s books:

Liabilities 40,000

Cash 145,000

Case 2: Bargain Purchase under acquisition method

Fair value of consideration transferred $110,000

Fair value of net identifiable assets 120,000

Gain on bargain purchase $ 10,000

Case 2 journal entry on Allerton’s books:

Gain on Bargain Purchase 10,000

Liabilities 40,000

Cash 110,000

Problem 28. (continued)

In a bargain purchase, the acquisition method employs the fair value of the net

29. (25 minutes) (Combination entries—acquired entity dissolved)

Cash consideration transferred $310,800

Contingent performance obligation 17,900

Consideration transferred (fair value) 328,700

Fair value of net identifiable assets 294,700

Goodwill $ 34,000

Journal entries:

Receivables 83,900

Inventory 70,250

Contingent Performance Liability 17,900

Cash 310,800

Professional Services Expense 15,100

Cash 15,100

30. (30 Minutes) (Overview of the steps in applying the acquisition method when

shares have been issued to create a combination. Part h. includes a bargain

purchase.)

a. The fair value of the consideration includes

Fair value of stock issued $1,500,000

c. In a business combination, direct acquisition costs (such as fees paid to

d. The par value of the 20,000 shares issued is recorded as an increase of

e. Fair value of consideration transferred (above) $1,530,000

Receivables $ 80,000

Patented technology 700,000

f. Revenues and expenses of the subsidiary from the period prior to the

combination are omitted from the consolidated totals. Only the operational

h. The fair value of the consideration transferred is now $1,030,000. This

amount indicates a bargain purchase calculated as follows:

Fair value of consideration transferred $1,030,000

Receivables $ 80,000

Patented technology 700,000

The values of SafeData’s assets and liabilities would be recorded at fair value,