30. (continued)

A Liabilities ………..………..………..………..……….………. 32,000

Equipment ………….………..……….………..………..…… 15,000

Brand names ………..………..…………….…..….…..….. 45,000

Investment in Kirby ……………………….…..….…. 82,800

Noncontrolling interest in Kirby (10%) ………. 9,200

(To recognize unamortized balance of excess allocations as of 1/1/15.

Figures have been reduced by one year of amortization)

Tl Sales ……………….………..………..………..…………….… 160,000

Cost of goods sold ……………..……………….…... 160,000

(To eliminate intra-entity transfers for 2015)

G Cost of goods sold ……………..…..….…..…..…..…... 12,800

(To adjust depreciation for current year created by transfer of building)

30. continued: Worksheet (not part of requirements)

Moore Company and Subsidiary

Consolidated Worksheet

December 31, 2015

Moore Kirby NCI Consolidated

Sales and other income (800,000) (600,000) (TI) 160,000 (1,240,000)

Cost of goods sold 500,000 400,000 (G) 12,800 (G*) 8,700 744,100

(TI)160,000

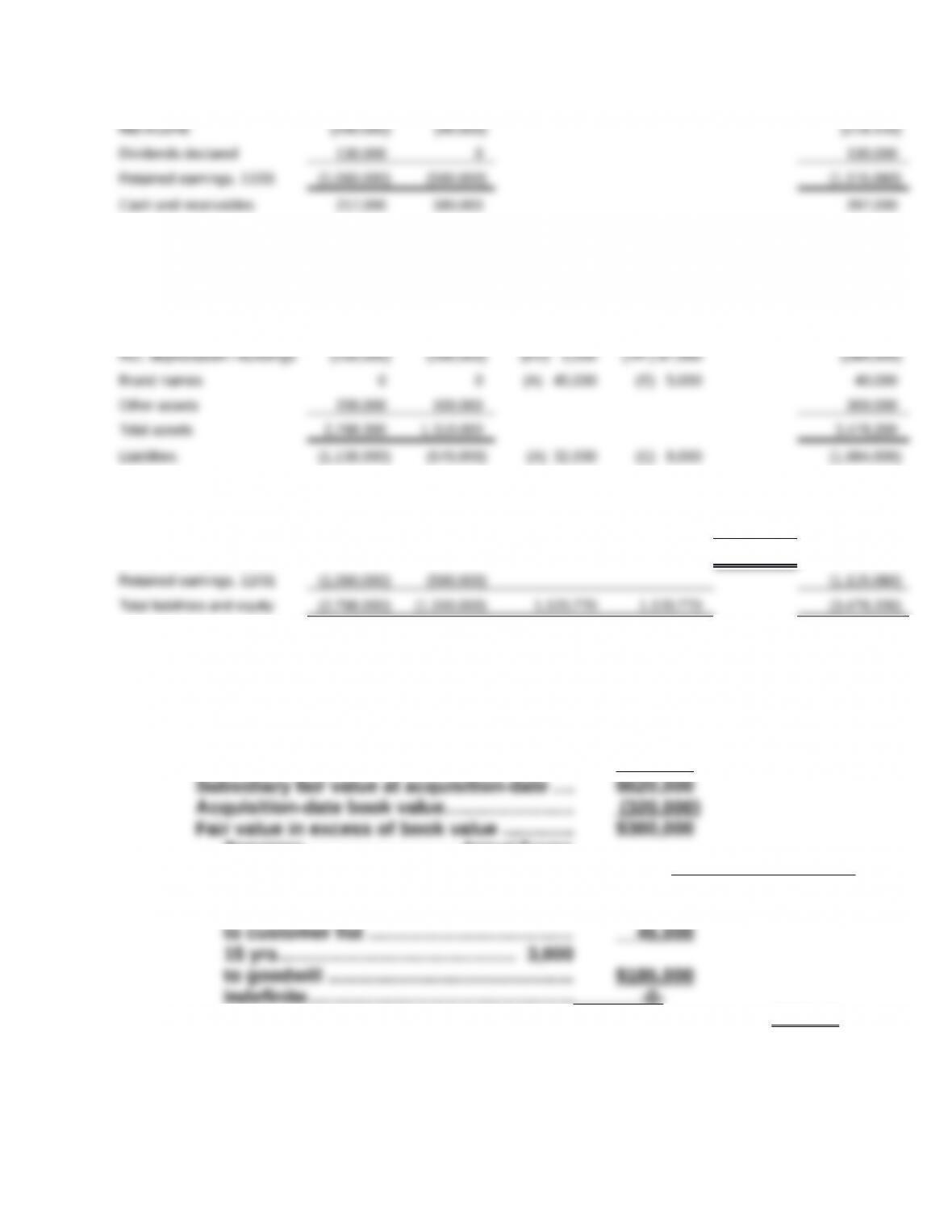

Retained earnings, 1/1 (990,000) (TA*) 12,000 (*C) 47,970 (1,025,970)

(550,000) (S) 541,300

Inventory 224,000 160,000 (G) 12,800 371,200

Investment in Kirby 657,000 0 (*C) 47,970 (S) 622,170 0

(A) 82,800

Equipment (net) 600,000 420,000 (A) 15,000 (E) 5,000 1,030,000

Buildings 1,000,000 650,000 (TA*) 75,000 1,725,000

Common stock (600,000) (150,000) (S)150,000 (600,000)

Noncontrolling interest , 1/1 (S) 69,130

(A) 9,200 (78,330)

Noncontrolling interest,12/31 (80,120) (80,120)

31. (55 Minutes) (Investment account balance and consolidated worksheet

with downstream inventory transfers when parent uses equity method)

Acquisition-date fair value allocation and excess amortizations

a. Consideration transferred ……..….…..…...... $372,000

Noncontrolling interest fair value..….…....... 248 ,000

Remaining ………………………..…...Annual Excess

Excess fair value assignments…………… Life Amortizations

to patents………..………..…..….…..…..…..…. 70,000

10 yrs…………………..……….…..…..…$7,000

$10 ,000

Determination of Investment in Stinson account balance

Consideration transferred ……………..……….…………..…..…...

$372,000

Increase in Stinson’s retained earnings 1/1/14 to 1/1/15

[(280,000 – 220,000) × 60%]…………..………..………..…….. $36,000

Excess fair value amortization × 60%…………….…………. (6,000)

$411,000

* Stinson’s 2015 net income……..………..………..…………….. $60,000

Excess fair value amortization…………..………….…..…..… (10 ,000)

Adjusted net income………………………….…..….…..…..…... $50,000

McIlroy’s percentage ownership…….………..…….…..….... 60 %

McIlroy’s equity in earnings of Stinson…………………….. $28 ,000

Intra-entity profits (downstream) 2014 2015

Intra-entity transfers remaining in inventory $50,000 $40,000

31. (continued)

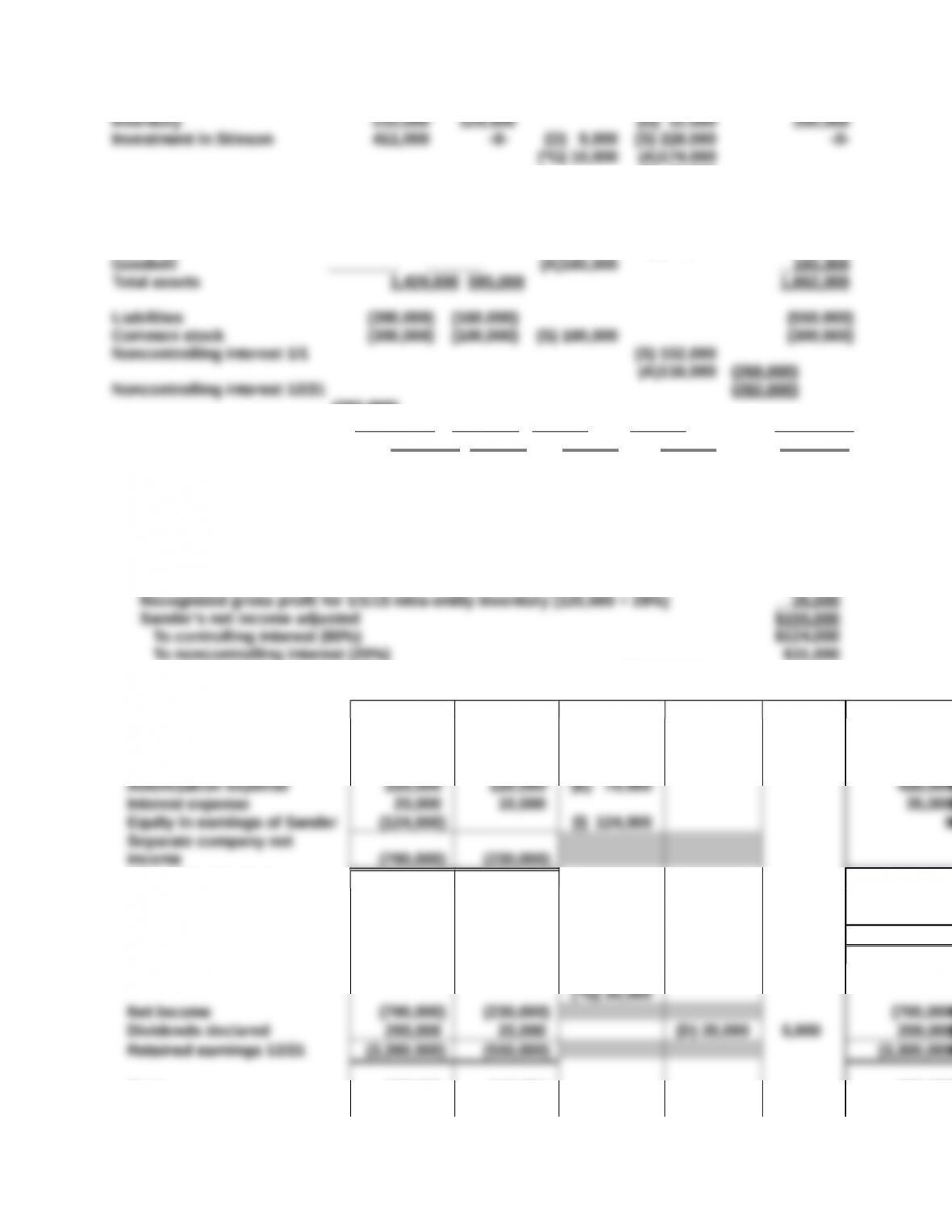

b. McIlroy Stinson Adj. & Elim. NCI Consolidated

Sales (700,000) (335,000) (TI)160,000 (875,000)

Cost of goods sold 460,000 205,000 (G) 12,000 (*G) 10,000 507,000

(TI) 160,000

to noncontrolling interest (20,000) 20 ,000

to McIlroy, Inc. (80 ,000)

Retained earnings, 1/1 (695,000) (280,000) (S) 280,000 (695,000)

Net income (above) (80,000) (60,000) (80,000)

(I) 28,000

Buildings (net) 308,000 202,000 510,000

Equipment (net) 220,000 86,000 306,000

Patents (net) -0- 20,000 (A) 63,000 (E) 7,000 76,000

Customer list (A) 42,000 (E) 3,000 39,000

(282,000)

Retained earnings, 12/31 (730 ,000) (325 ,000) (730 ,000)

Total liabilities and equities (1 ,420,000)(585 ,000) 899 ,000 899 ,000 (1 ,862,000)

32. Investment balance and worksheet preparation—upstream sales, equity

method

a. 2015 net income reported by Sander $230,000

Excess patent fair value amortization ($350,000 ÷ 5 years) (70,000)

Deferred gross profit for 12/31/15 intra-entity inventory (160,000 × 25%) (40,000)

Adjustments

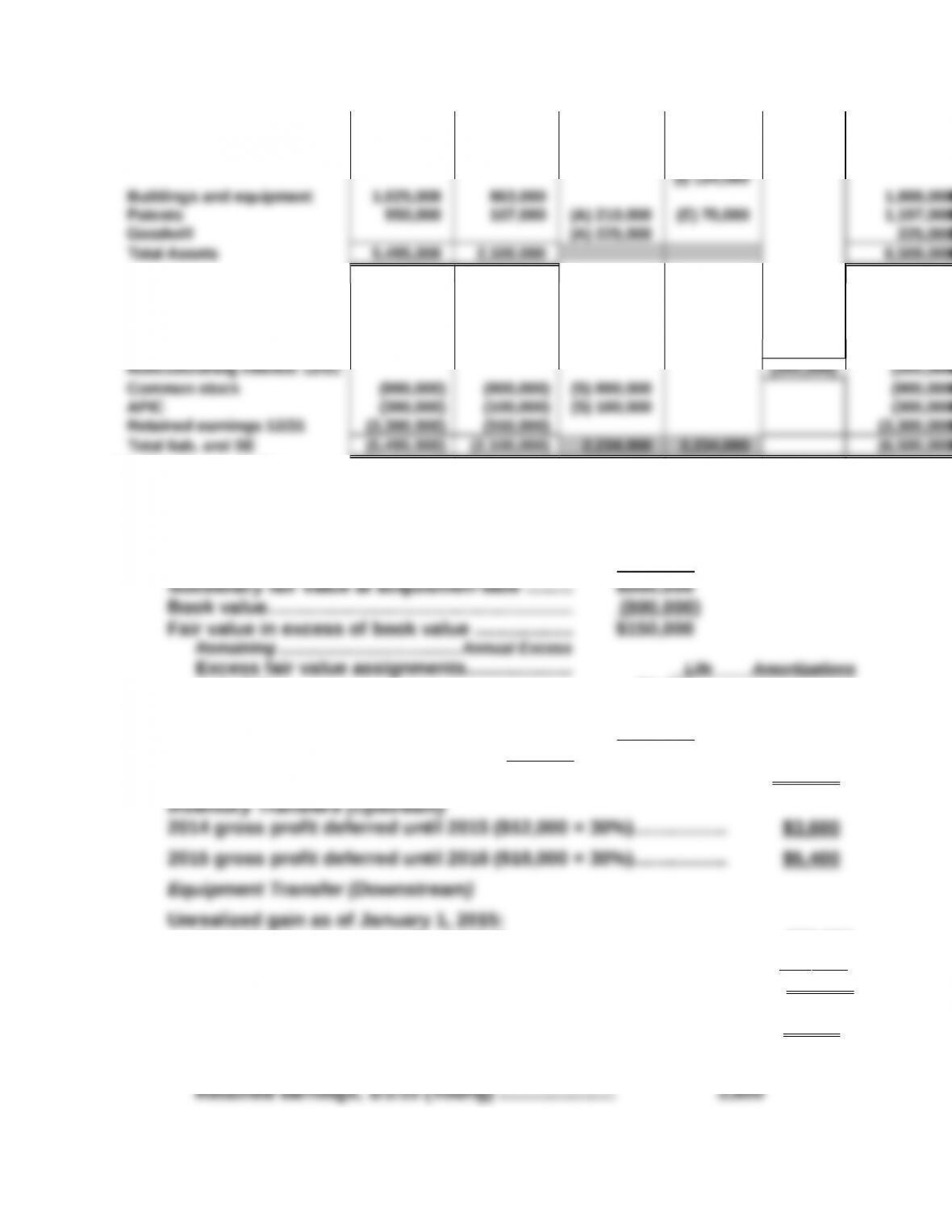

b. Plymouth Sander & Eliminations NCI Consolidated

Revenues (1,740,000) (950,000) (TI) 300,000 (2,390,000)

Cost of goods sold 820,000 500,000 (G) 40,000 (TI)300,000 1,025,000

(*G) 35,000

Depreciation expense 104,000 85,000 189,000

Consolidated net income (731,000)

to noncontrolling

interest (31,000) 31,000

to Plymouth Corp. (700,000)

Retained earnings 1/1 (2,800,000) (345,000) (S) 310,000 (2,800,000)

Cash 535,000 115,000 650,000

Accounts receivable 575,000 215,000 790,000

Inventory 990,000 800,000 (G) 40,000 1,750,000

Investment in Sander 1,420,000 (D) 20,000 (S)968,000

(A)348,000 0

Accounts payable (450,000) (200,000) (650,000)

Notes payable (545,000) (450,000) (995,000)

Noncontrolling interest 1/1 (S)242,000

(A) 87,000 (329,000)

33. (50 Minutes) (Prepare consolidation entries for a combination where upstream

inventory transfers have occurred as well as downstream equipment transfers.

Parent has applied initial value method)

Consideration transferred …………….………..….. $665,000

Noncontrolling interest fair value…………………. 285 ,000

to building…………………….………..………..…….. 50,000

5 yrs……………………………………………$10,000

to franchise agreements ………………….…..… 100 ,000

10 yrs…………………………………………. 10,000

-0- $20 ,000

Unrealized gain on transfer (1/1/14) ………………………..…………. $36,000

2014 excess depreciation ($36,000 ÷ 6 yrs.) …………..…..…..…. (6 ,000)

Unrealized gain January 1, 2015……………..………..………..…………… $30 ,000

Excess depreciation—2015 ($36,000 ÷ 6 yrs.) ……..……….…………. $6 ,000

Entry *G

Entry *TA

Retained earnings, 1/1/15 (Monica) ……………….. 30,000

33. (continued)

Entry *C

Investment in Young ………….…..….…..…..….... 123,480

Retained earnings, 1/1/15 (Monica) ..…..… 123,480

Because the parent uses the initial value method, its retained

earnings must be adjusted for the subsidiary’s increase in book

value less excess amortizations and upstream profits during 2013–

2014 as follows.

Removal of unrealized gross profit (Entry *G) ........ (3 ,600)

Realized retained earnings of Young,

December 31, 2014……….………..………..………..…… 626,400

Retained earnings at date of acquisition ………..…... (410 ,000)

Increase in retained earnings during 2013–2014..... 216,400

Entry S

Common stock (Young) ……….………..………..…….. 300,000

Additional paid-in capital (Young) …………….……. 90,000

Retained earnings, 1/1/15

(Young) (adjusted for *G) …………..……….…..… 626,400

Entry A

Franchise agreement…………..………..………..…..…. 80,000

Buildings ……….………..………..………..………..………. 30,000

excess amortizations.

33. (continued)

Entry I

Dividend income ………….………..…….…..…..…..….. 35,000

income under the initial value method.

Entry E

Depreciation expense………….………..………..……… 10,000

To recognize current year excess amortization expense.

Entry Tl

Sales ………..………..………..………….…..…..….…..….. 90,000

Cost of goods sold ……………..……………….…... 90,000

(computed above).

Entry ED

Accumulated depreciation …………..……………..…. 6,000

Depreciation expense ………………..….…..…..… 6,000

To remove current year depreciation on transferred item since its

historical cost has been fully depreciated.

Noncontrolling Interest’s Share of Consolidated Net Income

Reported net income of Young (given) ……………….…..….... $160,000

34. (35 Minutes) (Consolidation entries with upstream Inventory transfers and

downstream equipment transfers. Parent uses equity method)

Entry *G (Same as Entry *G in Problem 33.)

Entry *TA

Investment in Young ……………………..…………….... 30,000

Equipment ………….………..……….………..………..…… 14,000

Entry *C (No Entry *C is needed because equity method has been applied.)

Entry I

Investment income …………..…………..…..….…..….. 102,740

Investment in Young ………….…..….…..…..….... 102,740

To eliminate intra-entity income accrual.

Reported net income of Young (given) ……………..…..…..…..….… $160,000

Excess fair value amortization ……………..………..………..………….. (20,000)

Recognition of 2014 unrealized gross profit (Entry *G) …......... 3,600

Deferral of 2015 unrealized gross profit (Entry G) (upstream) (5 ,400)

Entry D

Investment in Young ……………………..…………….... 35,000

Dividends declared ………….………..……….…….. 35,000

To eliminate intra-entity dividend transfers.

Entry E (Same as Entry E in Problem 33.)