26. (45 Minutes) (P&L allocations and admission of a new partner)

a. The interest factor was probably inserted to reward Hugh for contributing

$50,000 more to the partnership than Jacobs. The salary allowance gives

b. The drawings show the assets removed by a partner during a period of

time. A salary allowance is added to each partner’s capital for the year

(usually in recognition of work done) and is a component of net income

c. Hugh, drawings …………..……………….……………..…..… 7,500

Repair expense ………………………..…..….….….….... 7,500

(To reclassify payment made to repair personal residence.)

(To close drawings accounts for 2014.)

Revenues ………..………..……….………..……….………..….. 175,000

Expenses (adjusted by first entry) …………..….…. 138,500

Income summary ……………………..…..….….…..…... 36,500

(To close revenue and expense accounts for 2014.)

(To close net income to partners’ capital–see allocation plan shown below.)

Allocation of Income Hugh Jacobs

Interest (10% of beginning balance) $ 15,000

$ 10,000

Salary allowances 5,000

25,000

Remaining income (loss):

Net income $ 36,500

26. (continued)

d. Total capital (original balances of $250,000 plus 2014

net income less drawings) …………..……………..…. $256,000

Investment by Thomas ………….……….…..….….….…... 64,000

Total capital after investment ……………….…………….. $320,000

Ownership portion acquired by Thomas .….….…..... 15%

Bonus to Jacobs (60%) ………….………..……….………… $9,600

Cash ……..……….………..……….………..……….………….… 64,000

Thomas, capital (20% of total capital) ................ 48,000

Hugh, capital ………………….…….…..….….…..….…... 6,400

Jacobs, capital ………………….……………….….….….. 9,600

27. (40 Minutes) (Reporting a change in the composition of a partnership)

a. Exact amount of investment can only be computed algebraically:

E Investment = 25% (Original Capital + E Investment)

E Investment = $90,000

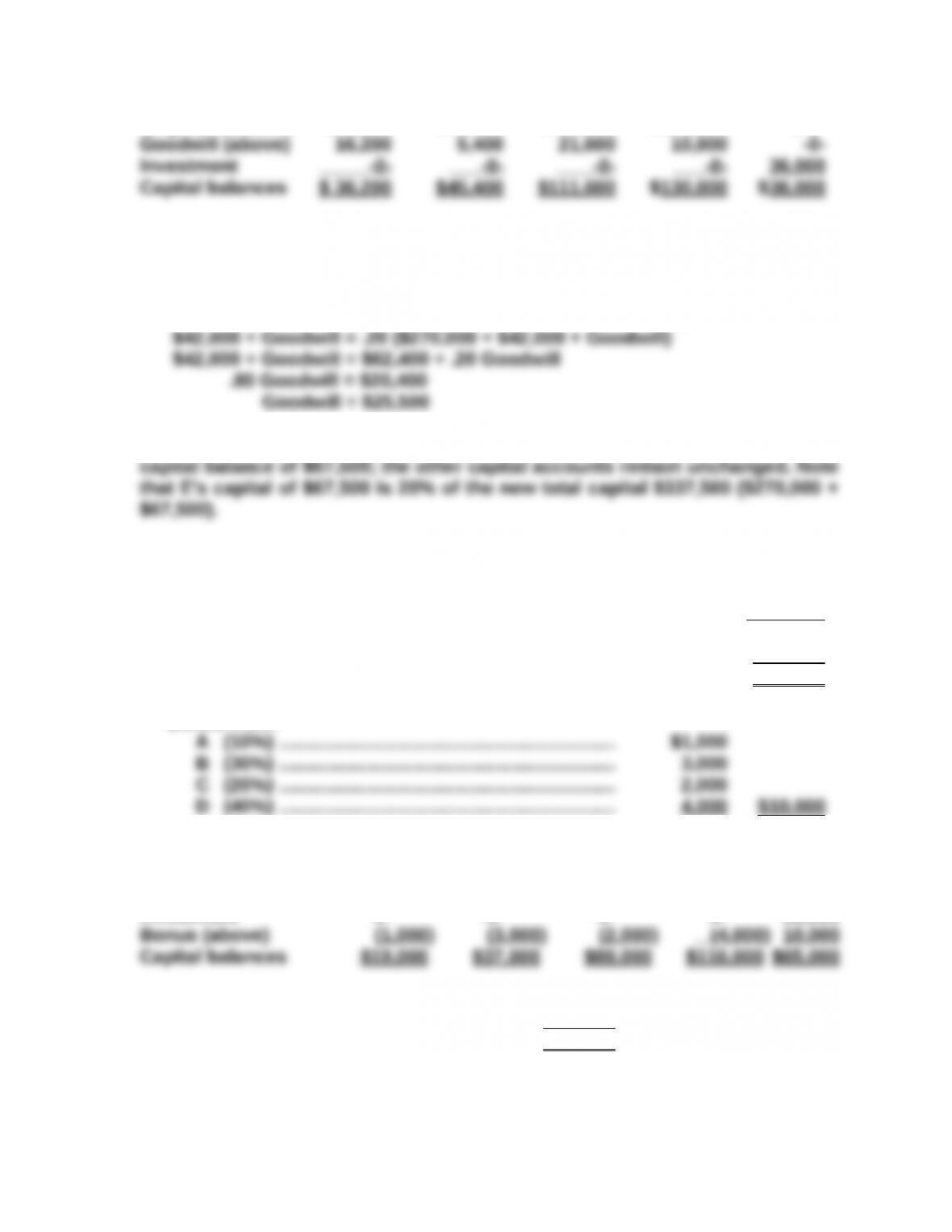

b. Implied value of partnership ($36,000 ÷ 10%).......... $360,000

Allocation of Goodwill:

A (30%) ……….……….………..……….……….…..….….. $16,200

B (10%) ……….……….………..……….……….…..….….. 5,400

CAPITAL BALANCES

ABCDE

Original balances $20,000 $40,000 $ 90,000 $120,000 $-0-

c. Because E’s investment of $42,000 is less than 20% of the resulting capital

($312,000). E is apparently bringing some other attribute to the partnership

(goodwill) that must be computed:

E Investment = 20% (Original Capital + E Investment)

E’s investment is, therefore, $42,000 in cash and $25,500 in goodwill for a total

27.(continued)

d. Total capital after investment ($270,000 + $55,000) $325,000

Amount acquired by E …………..……….…..….….…..….. 20%

E’s capital balance ………………………….….…..….….….. $ 65,000

E’s payment ………………….…………….….….…..….….….. 55,000

Bonus being given to E …………….…..….…..….….….… $ 10,000

Bonus from:

CAPITAL BALANCES

ABCDE

Original balances $20,000 $40,000 $90,000 $120,000 $-0-

Investment -0- -0- -0- -0- 55,000

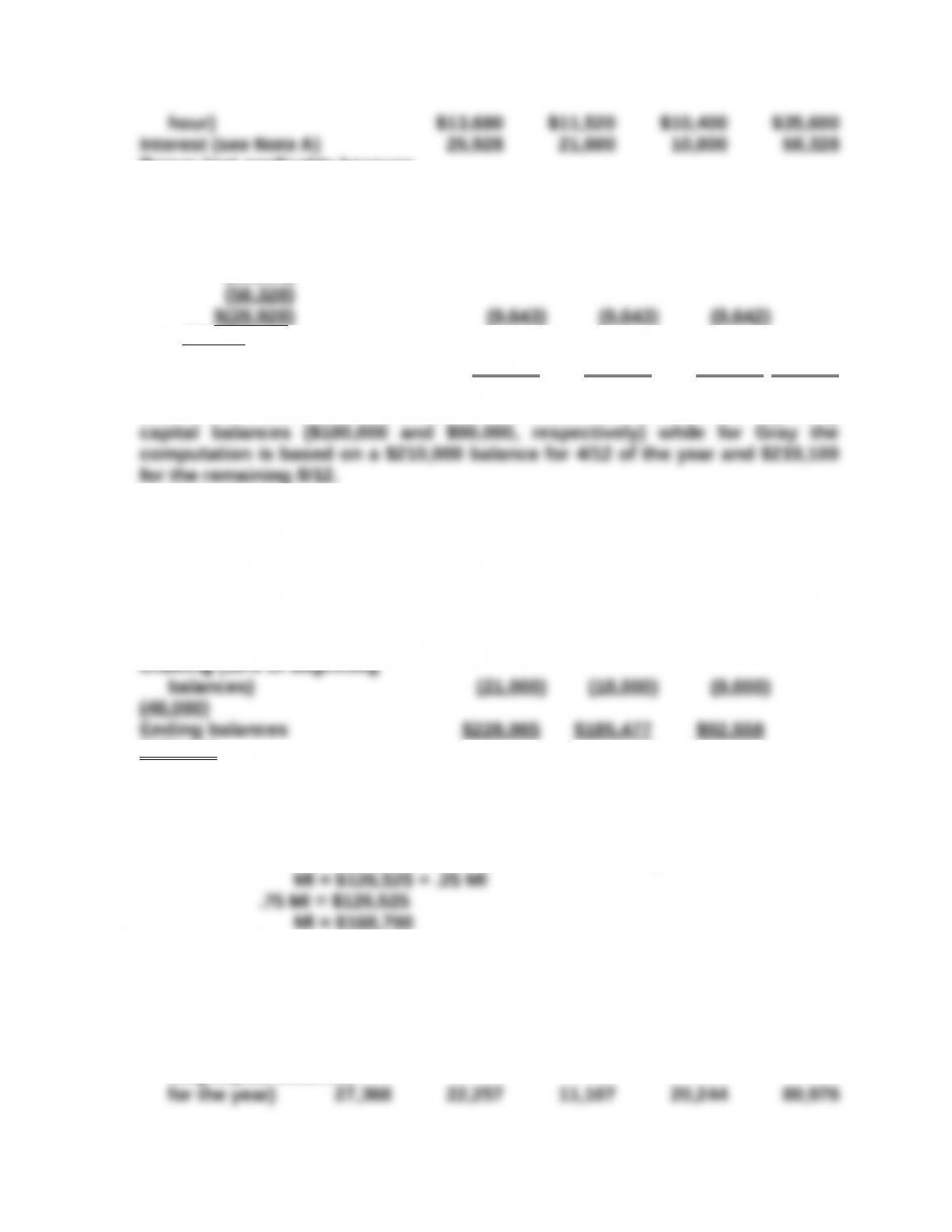

e. C’s capital balance $ 90,000

C’s collection (125%) 112,500

Bonus being paid to C $ 22,500

Bonus from:

A (1/3) $7,500

CAPITAL BALANCES

A B C D

Original balances ….….......... $20,000 $40,000 $ 90,000 $120,000

28.(55 Minutes) (Allocation of income to the partners and determination of capital

balances)

ALLOCATION OF INCOME—2013

Boswell Johnson Total

Salary (8 months) ….….….….. $8,000 $-0- $ 8,000

STATEMENT OF PARTNERS’ CAPITAL—DECEMBER 31, 2013

Boswell Johnson Total

Beginning Balances ($114,000

Invested capital split evenly—

market value used for assets) $57,000 $57,000 $114,000

WALPOLE INVESTMENT JANUARY 1, 2014

Walpole’s $54,000 investment increases total capital to $179,000. Walpole is

ALLOCATION OF INCOME—2014

Boswell Johnson Walpole Total

Salary ……….……….…………….. $12,000 $-0- $24,000 $36,000

Remaining $8,000 loss ($28,000 –

STATEMENT OF PARTNERS’ CAPITAL—DECEMBER 31, 2014

Boswell Johnson Walpole Total

Beginning balances ............. $66,200 $58,800 $ -0- $125,000

Walpole’s contribution ……… (7,040) (10,560) 71,600 54,000

Ending balances ............. $65 ,200 $39 ,400 $82 ,400 $187 ,000

28.(continued)

ADMISSION OF POPE—JANUARY 1, 2015

Pope’s payment was made directly to the partners. Therefore, neither goodwill

nor a bonus need be recognized. Instead, 10% of each capital balance shown

above will be reclassified to Pope. The journal entry would be as follows:

ALLOCATION OF INCOME—2015

Boswell Johnson Walpole Pope Total

Salary $12,000 $-0- $24,000 $9,600 $45,600

STATEMENT OF PARTNERSHIP CAPITAL—DECEMBER 31, 2015

Boswell Johnson Walpole Pope Total

Beginning balances $65,200 $39,400 $82,400 $-0– $187,000

Admission of Pope (6,520) (3,940) (8,240) 18,700 -0-

Allocation of income

$209,000

29. (60 Minutes) (Allocate income and prepare a statement of partners’ capital)

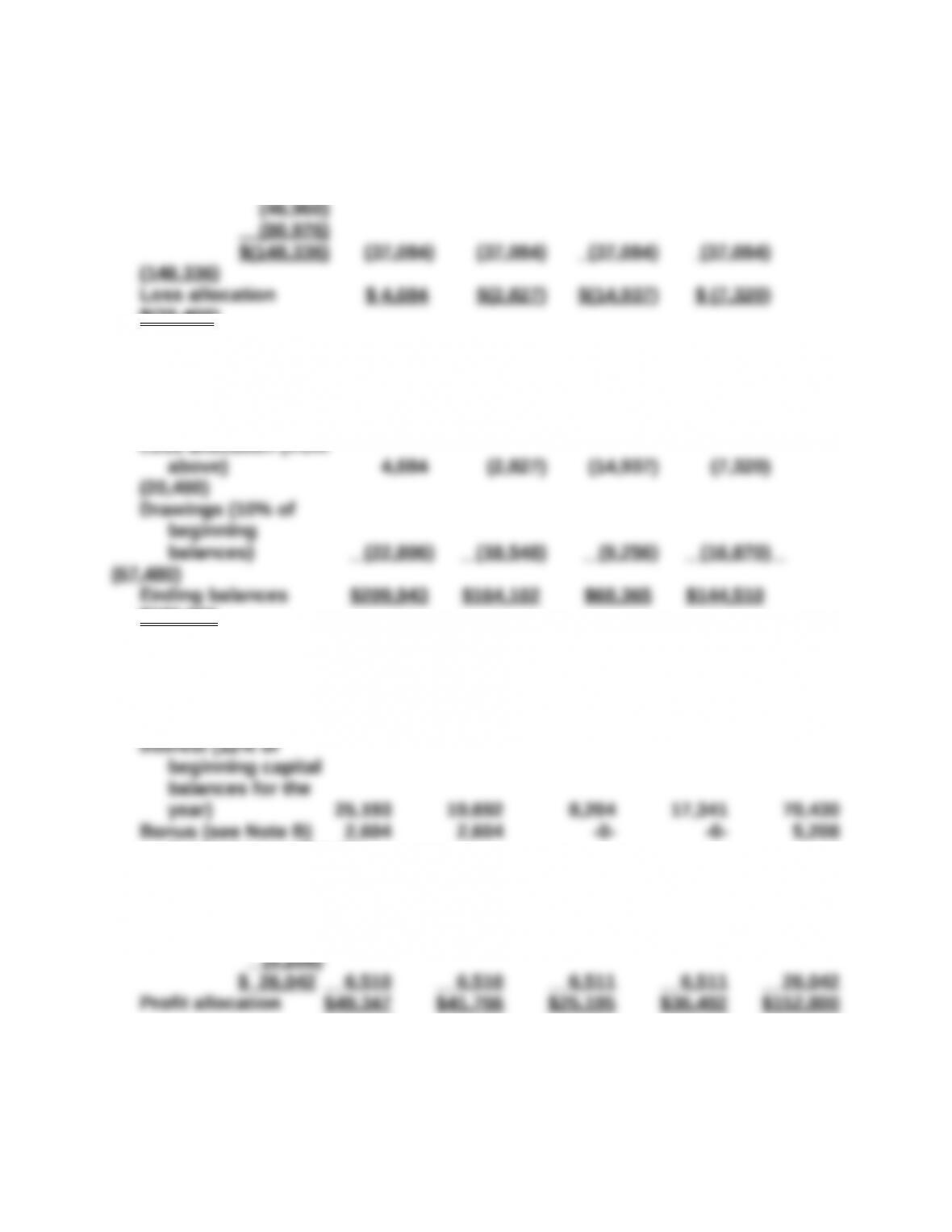

a. Income Allocation—2013

Gray Stone Lawson Totals

Salary allowance ($8 per billable

Bonus (not applicable because

salary and interest would

necessitate a negative bonus) -0- -0- -0- -0-

Remaining loss (split evenly):

$ 65,000

(35,600)

(28,928)

Profit allocation $29 ,965 $23 ,477 $11 ,558 $65 ,000

Note A: Interest for Stone and Lawson is calculated at 12% of their beginning

Capital Account Balances—1/1/13 – 12/31/13

Gray Stone Lawson Totals

Beginning contributions $210,000 $180,000 $90,000

$480,000

Added Investment 9,100 -0- -0- 9,100

Profit allocation (from above) 29,965 23,477 11,558 65,000

$506,100

Prior to developing the information for 2014, a computation of Monet’s

investment must be made:

Monet’s Investment = 25% ($506,100 + Monet’s Investment)

29. a. (continued)

Income Allocation—2014

Gray Stone Lawson Monet Totals

Salary allowance ($8

per billable hour) $14,400 $ 12,000 $ 11,040 $ 9,520 $ 46,960

Interest (12% of begin-

ning capital balances

Bonus (not applicable) -0- -0- -0- -0- -0-

Remaining loss (split

evenly):

$ (20,400)

$(20,400)

Capital Account Balances 1/1/14 – 12/31/14

Gray Stone Lawson Monet Totals

Beginning balances $228,065 $185,477 $92,558 $168,700

$674,800

Loss allocation (from

$586,920

Income Allocation—2015

Gray Stone Lawson Monet Totals

Salary allowance ($8

per billable hour) $15,040 $12,960 $10,480 $12,640 $ 51,120

Remaining profit split

evenly:

$152,800

(51,120)

(70,430)

29.a. (continued)

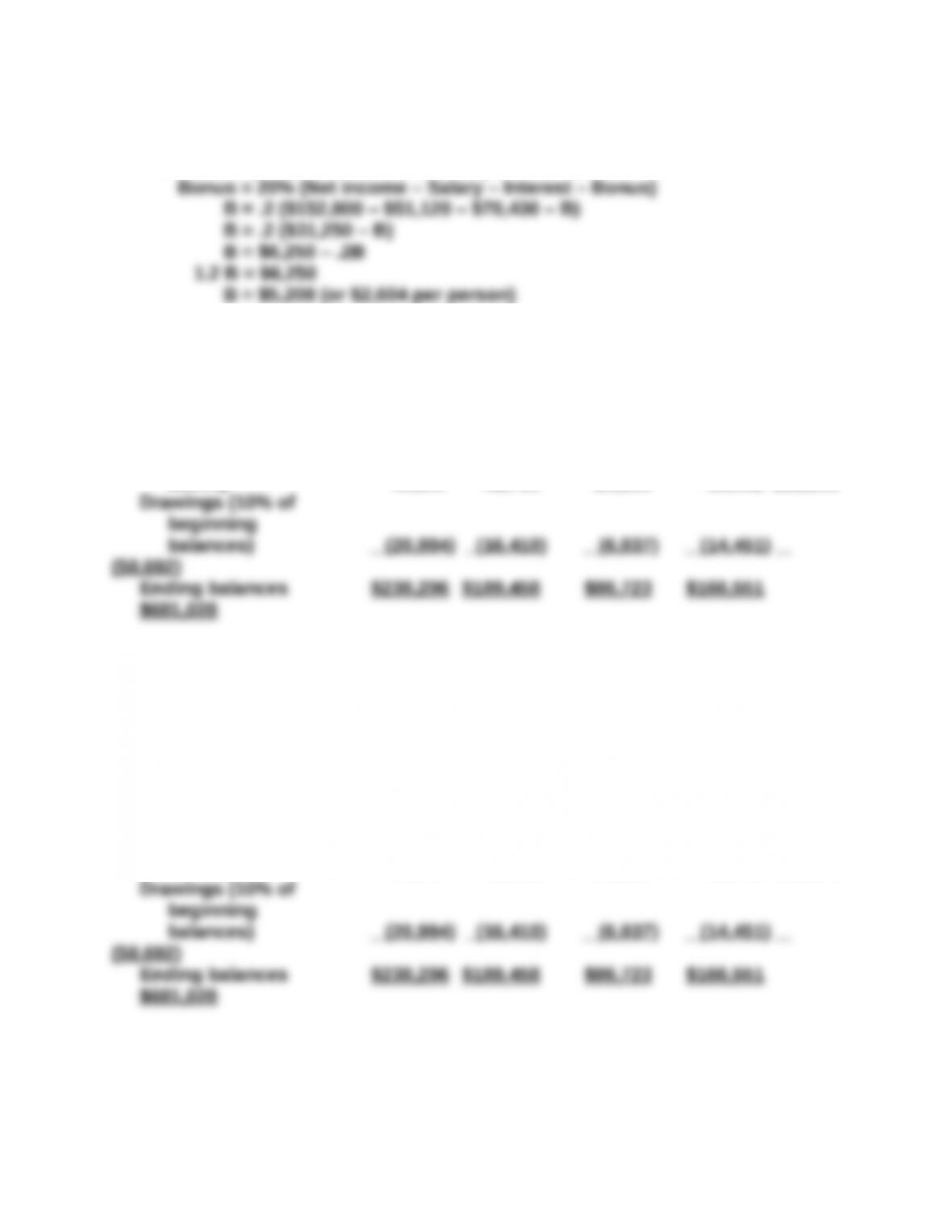

Note B: The bonus to Gray and Stone can only be derived algebraically.

Because each of the two partners is entitled to 10% of net income as defined,

the total bonus is 20% and can be computed as follows:

Capital Account Balances 1/1/15 – 12/31/15

Gray Stone Lawson Monet Totals

Beginning balances $209,943 $164,102 $68,365 $144,510

$586,920

Profit allocation (from

above) 49,347 41,766 25,195 36,492 152,800

b.

GRAY, STONE, LAWSON, and MONET

Statement of Partners’ Capital

For Year Ending December 31, 2015

Gray Stone Lawson Monet Totals

Beginning balances $209,943 $164,102 $68,365 $144,510

$586,920

Profit allocation (from

above) 49,347 41,766 25,195 36,492 152,800

30.(40 Minutes) (Recording admission and retirement of partners using both the

bonus and goodwill methods)

a. Porthos, capital ………….………..…..….….…..….….….…. 35,000

b. Goodwill …….………..……….………..……….…..….….… 50,000

Athos, capital (50%) ………………….………..………… 25,000

(To record goodwill based on $250,000 implied value of partnership [$25,000

÷ 10%]. Because current capital is only $200,000 [the $25,000 goes directly

to the partners], goodwill of $50,000 has to be recorded and allocated using

profit and loss ratio.)

Athos, capital (10% of balance) …………..….….….…... 10,500

c. Cash ……..……….………..……….………..……….………….… 30,000

D’Artagnan, capital (10% of total capital).….….... 23,000

Athos, capital (50% of excess payment) ............ 3,500

$7,000 payment being recorded as a bonus to the original partners.)

d. Cash ……..……….………..……….………..……….………….… 30,000

Goodwill ………..……….………..……………….….…..….…... 70,000

D’Artagnan, capital …………………….…..….….….….. 30,000

Athos, capital (50% of goodwill) ……………….…… 35,000

Porthos, capital (30% of goodwill) ..….….…..…... 21,000

partners.)

30. (continued)

e. Cash ……………….………..……….………..……….………….… 12,222

Goodwill . ………….……….………..………….…..….….….…. 10,000

D’Artagnan, capital …………………….…..….….….….. 22,222

To record investment by D’Artagnan. The implied value of the investment as

a whole would be only $122,220 ($12,222 ÷ 10%). Because the capital

balances are well in excess of this figure, D’Artagnan is apparently bringing

some other factor (goodwill) into the partnership. This goodwill can be

computed as follows:

f. Goodwill …….………..……….………..…..….….…..….….….. 80,000

Athos, capital (50%) ………….……….………..………… 40,000

Porthos, capital (30%) ………………..….….….…..….. 24,000