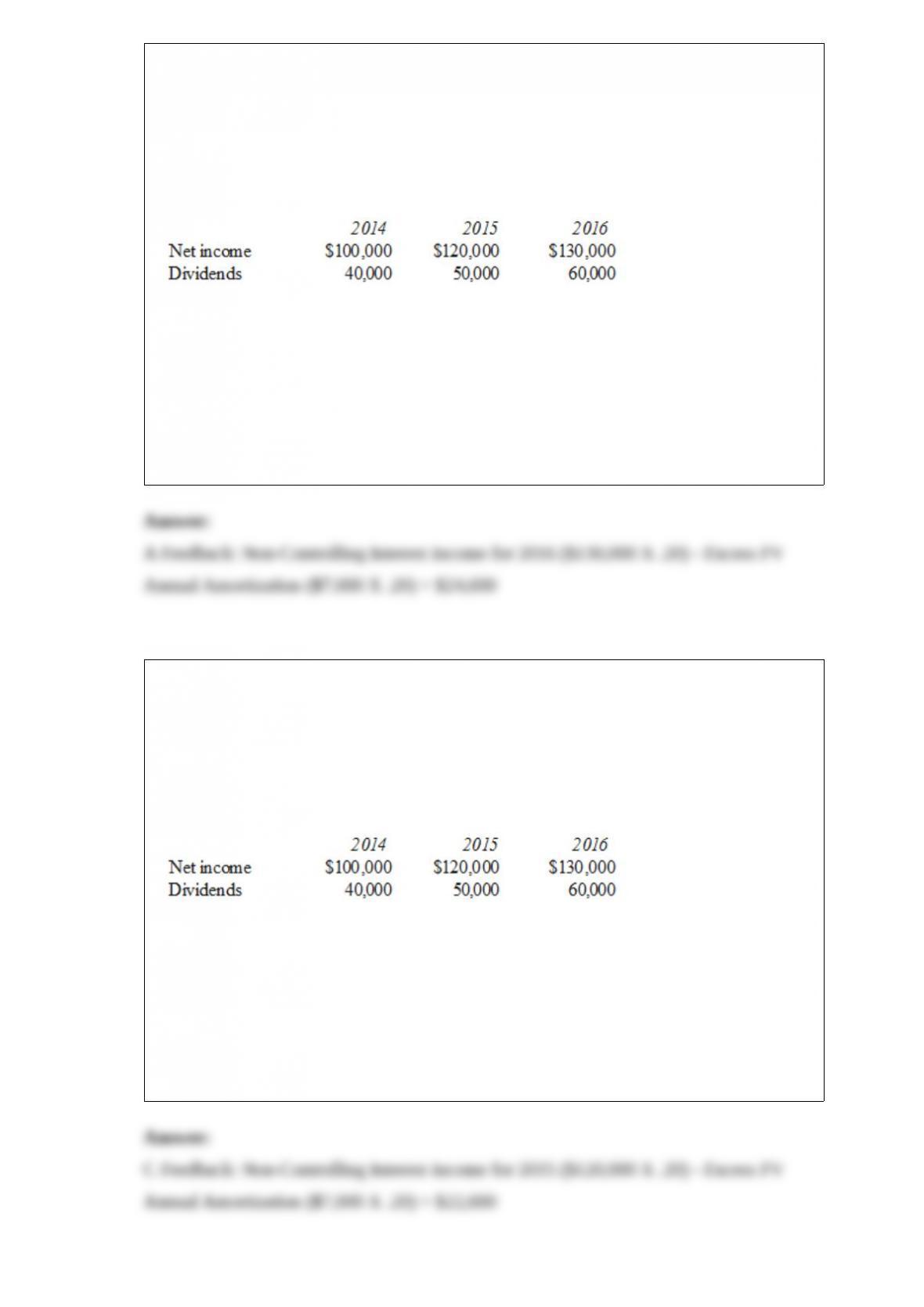

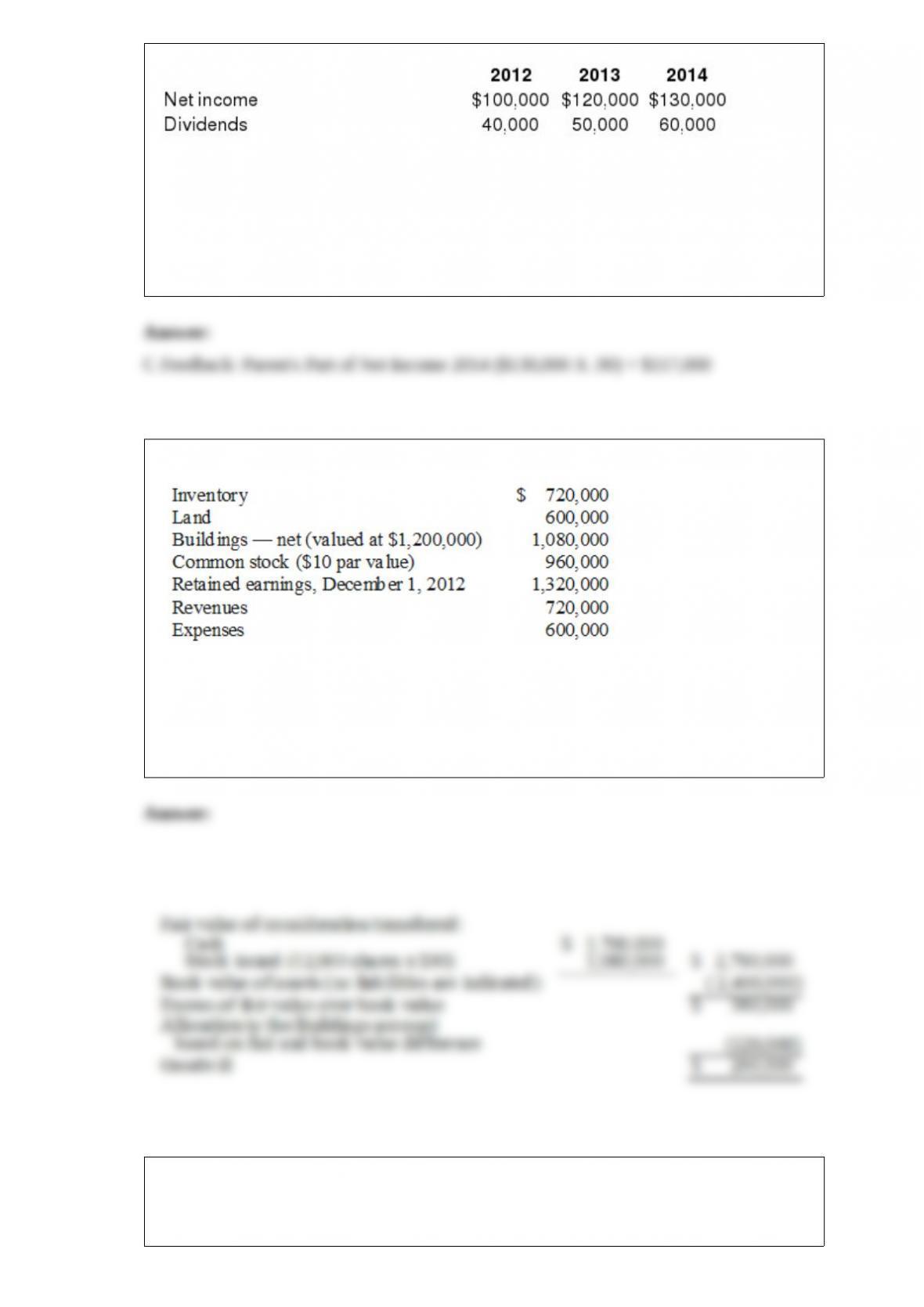

1) Pell Company acquires 80% of Demers Company for $500,000 on January 1, 2014.

Demers reported common stock of $300,000 and retained earnings of $210,000 on that

date. Equipment was undervalued by $30,000 and buildings were undervalued by

$40,000, each having a 10-year remaining life. Any excess consideration transferred

over fair value was attributed to goodwill with an indefinite life. Based on an annual

review, goodwill has not been impaired.

Demers earns income and pays dividends as follows:

Assume the INITIAL VALUE is applied.

Compute the non-controlling interest in the net income of Demers at December 31,

2016.

A) $24,600.

B) $14,000.

C) $26,000.

D) $20,400.

E) $12,600.

2) Pell Company acquires 80% of Demers Company for $500,000 on January 1, 2014.

Demers reported common stock of $300,000 and retained earnings of $210,000 on that

date. Equipment was undervalued by $30,000 and buildings were undervalued by

$40,000, each having a 10-year remaining life. Any excess consideration transferred

over fair value was attributed to goodwill with an indefinite life. Based on an annual

review, goodwill has not been impaired.

Demers earns income and pays dividends as follows:

Assume the INITIAL VALUE is applied.

Compute the non-controlling interest in the net income of Demers at December 31,

2015.

A) $18,400.

B) $14,000.

C) $22,600.

D) $24,000.

E) $12,600.

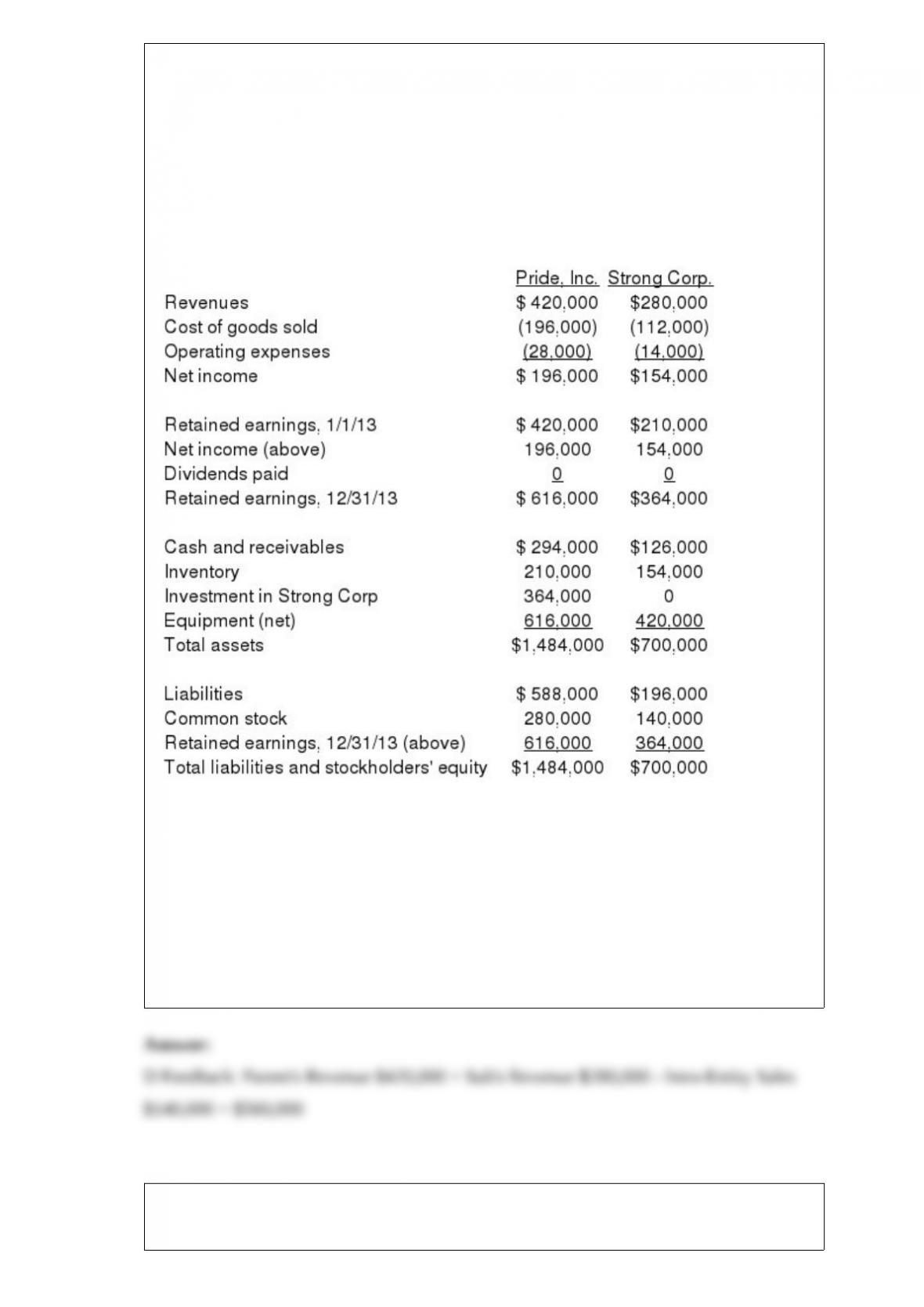

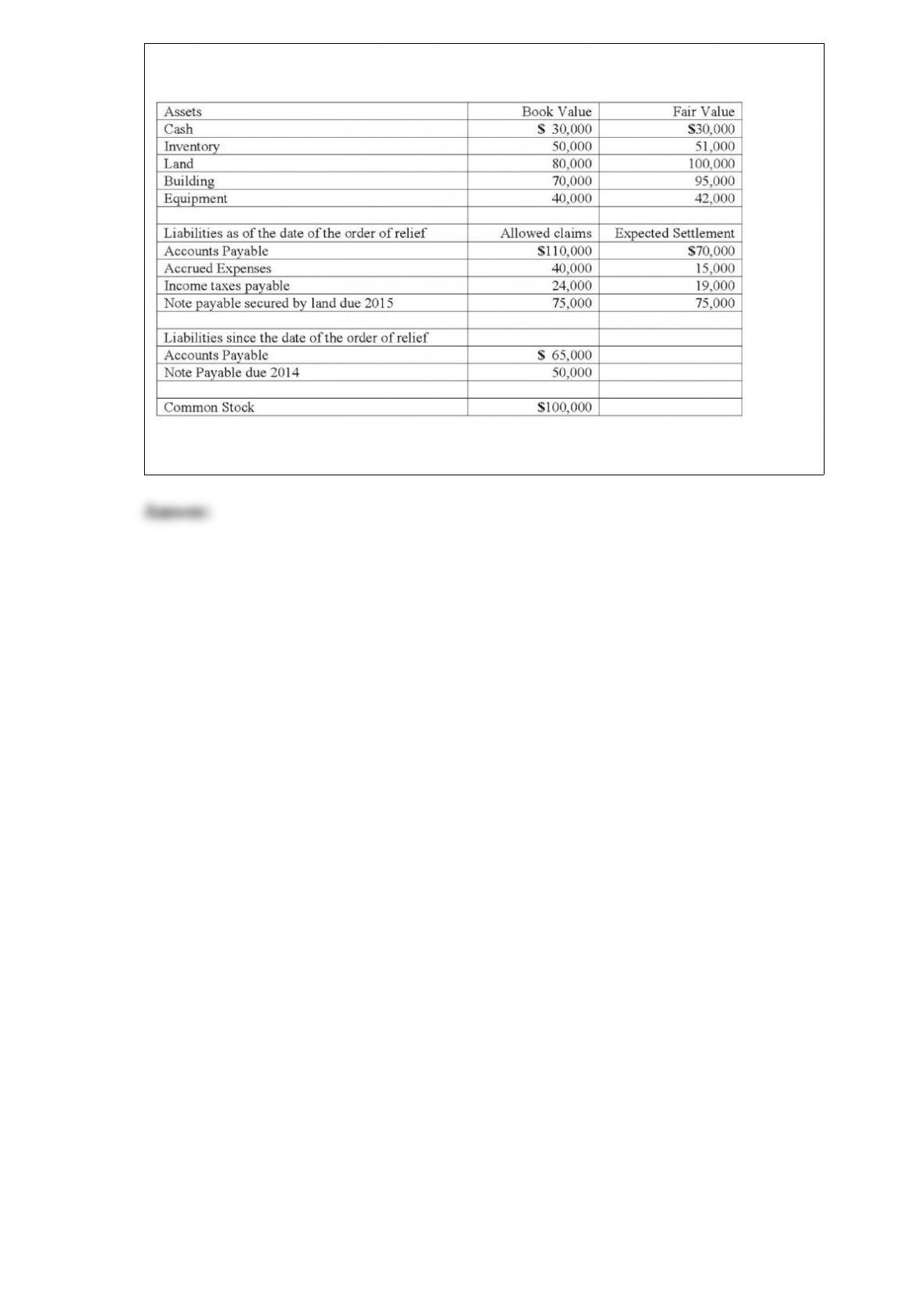

3) On January 1, 2013, Pride, Inc. acquired 80% of the outstanding voting common

stock of Strong Corp. for $364,000. There is no active market for Strong’s stock. Of this

payment, $28,000 was allocated to equipment (with a five-year life) that had been

undervalued on Strong’s books by $35,000. Any remaining excess was attributable to

goodwill which has not been impaired.

As of December 31, 2013, before preparing the consolidated worksheet, the financial

statements appeared as follows:

During 2013, Pride bought inventory for $112,000 and sold it to Strong for $140,000.

Only half of this purchase had been paid for by Strong by the end of the year. 60% of

these goods were still in the company’s possession on December 31, 2013. What is the

total of consolidated revenues?

A) $700,000.

B) $644,000.

C) $588,000.

D) $560,000.

E) $840,000.

4) Acker Inc. bought 40% of Howell Co. on January 1, 2012 for $576,000. The equity

method of accounting was used. The book value and fair value of the net assets of

Howell on that date were $1,440,000. Acker began supplying inventory to Howell as

follows:

Howell reported net income of $100,000 in 2012 and $120,000 in 2013 while paying

$40,000 in dividends each year.

What is the amount of unrealized intra-entity inventory profit to be deferred on

December 31, 2013?

A) $ 1,600.

B) $ 8,000.

C) $15,000.

D) $20,000.

E) $40,000

5) On January 1, 2013, a subsidiary buys 8 percent of the outstanding voting stock of its

parent corporation. The payment of $350,000 exceeded book value of the acquired

shares by $50,000, attributable to a copyright with a 10-year useful life. During the

year, the parent reported operating income of $675,000 (excluding investment income

from the subsidiary), and paid $100,000 in dividends. If the treasury stock approach is

used, how is the Investment in Parent Stock reported in the consolidated balance sheet

at December 31, 2013?

A.Included in current assets.

B.Included in noncurrent assets.

C.Consolidated stockholders’ equity is reduced by $350,000.

D.Consolidated stockholders’ equity is reduced by $300,000.

E.There is no effect on the consolidated balance sheet, because the effects have been

eliminated.

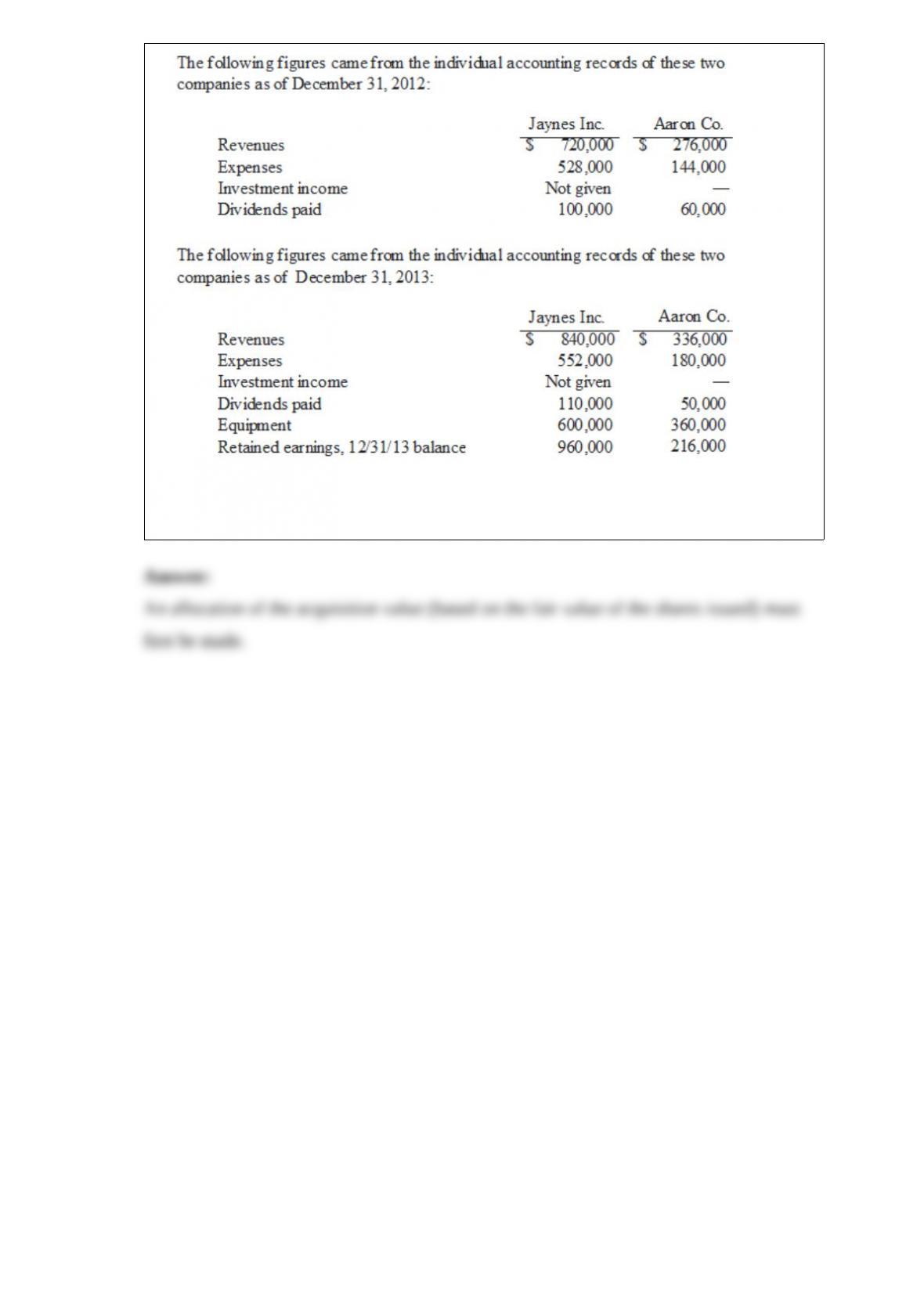

6) Jaynes Inc. acquired all of Aaron Co.’s common stock on January 1, 2012, by issuing

11,000 shares of $1 par value common stock. Jaynes’ shares had a $17 per share fair

value. On that date, Aaron reported a net book value of $120,000. However, its

equipment (with a five-year remaining life) was undervalued by $6,000 in the

company’s accounting records. Any excess of consideration transferred over fair value

of assets and liabilities is assigned to an unrecorded patent to be amortized over ten

years.

What balance would Jaynes’ Investment in Aaron Co. account have shown on

December 31, 2012, when the equity method was applied for this acquisition?

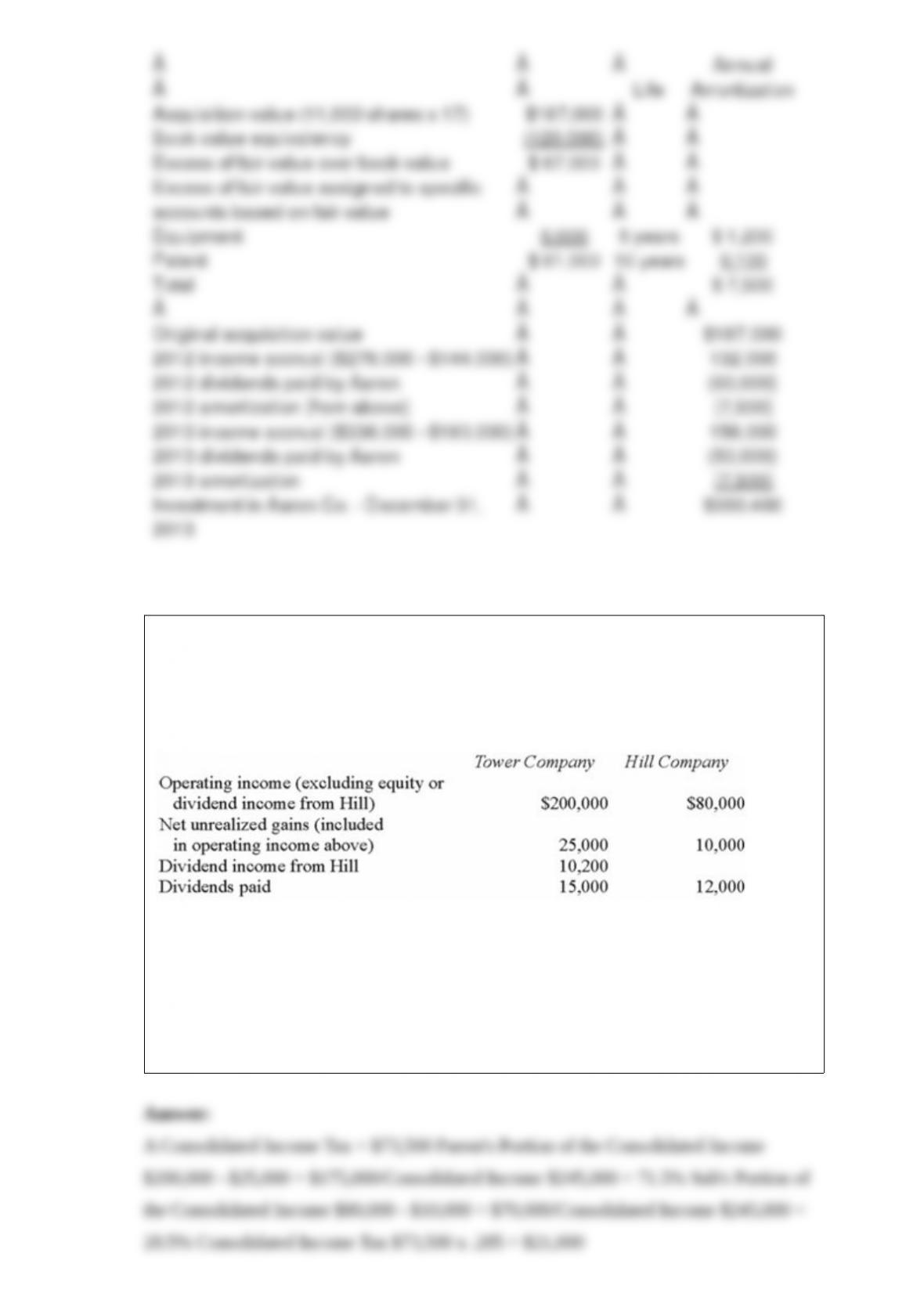

7) Tower Company owns 85% of Hill Company. The two companies engaged in several

intra-entity transactions. Each company’s operating and dividend income for the current

time period follow, as well as the effects of unrealized gains. No income tax accruals

have been recognized within these totals. The tax rate for each company is 30%.

Using percentage allocation method, how much income tax expense is assigned to Hill?

A.$21,000.

B.$24,000.

C.$20,400.

D.$17,400.

E.$0.

10) On June 1, CamCo received a signed agreement to sell inventory for x500,000. The

sale would take place in 90 days. CamCo immediately signed a 90-day forward contract

to sell the yen as soon as they are received. The spot rate on June 1 was x1 = $.004167,

and the 90-day forward rate was x1 = $.00427. At what amount would CamCo record

the Forward Contract on June 1?

A.$2,083

B.$0

C.$2,110

D.$2,532

E.$2,135

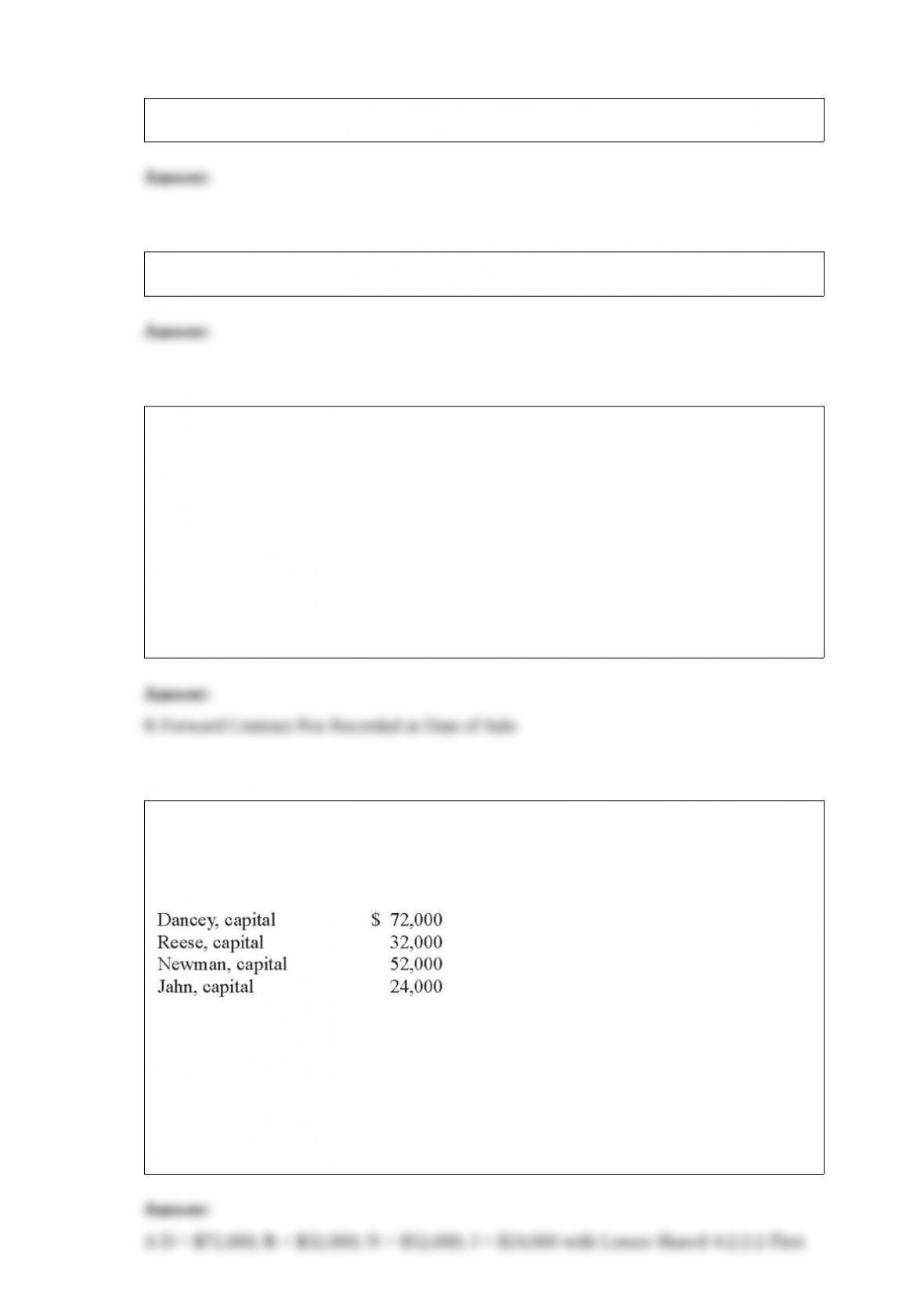

11) Dancey, Reese, Newman, and Jahn were partners who shared profits and losses on a

4:2:2:2 basis, respectively. They were beginning to liquidate their business. At the start

of the process, capital balances were as follows:

Which one of the following statements is true for a predistribution plan?

A.The first available $16,000 would go to Newman.

B.The first available $20,000 would go to Dancey.

C.The first available $8,000 would go to Jahn.

D.The first available $8,000 would go to Newman.

E.The first available $4,000 would go to Jahn.

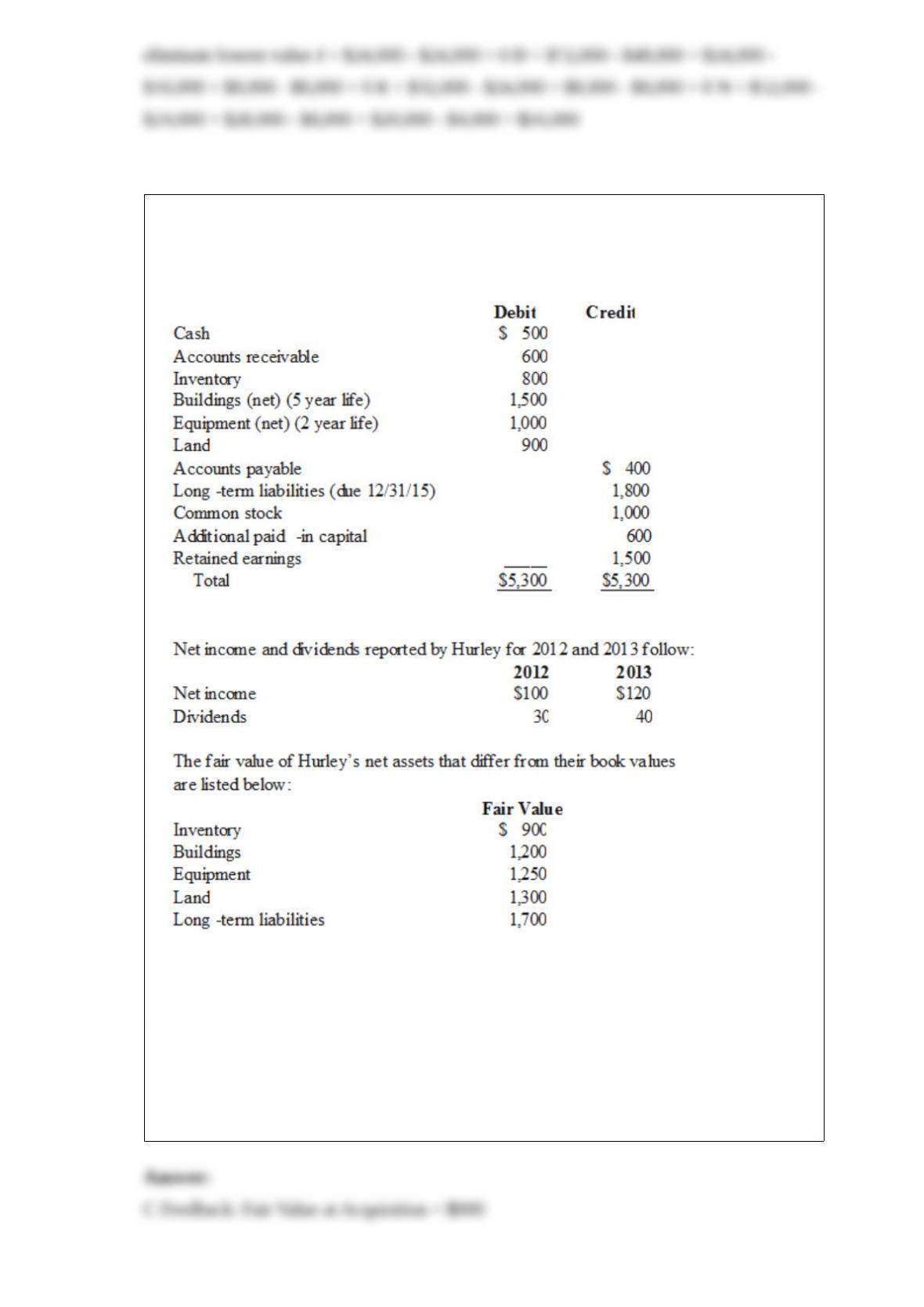

12) Perry Company acquires 100% of the stock of Hurley Corporation on January 1,

2012, for $3,800 cash. As of that date Hurley has the following trial balance;

Compute

the amount of Hurley’s inventory that would be reported in a January 1, 2012,

consolidated balance sheet.

A) $800.

B) $100.

C) $900.

D) $150.

E) $ 0.

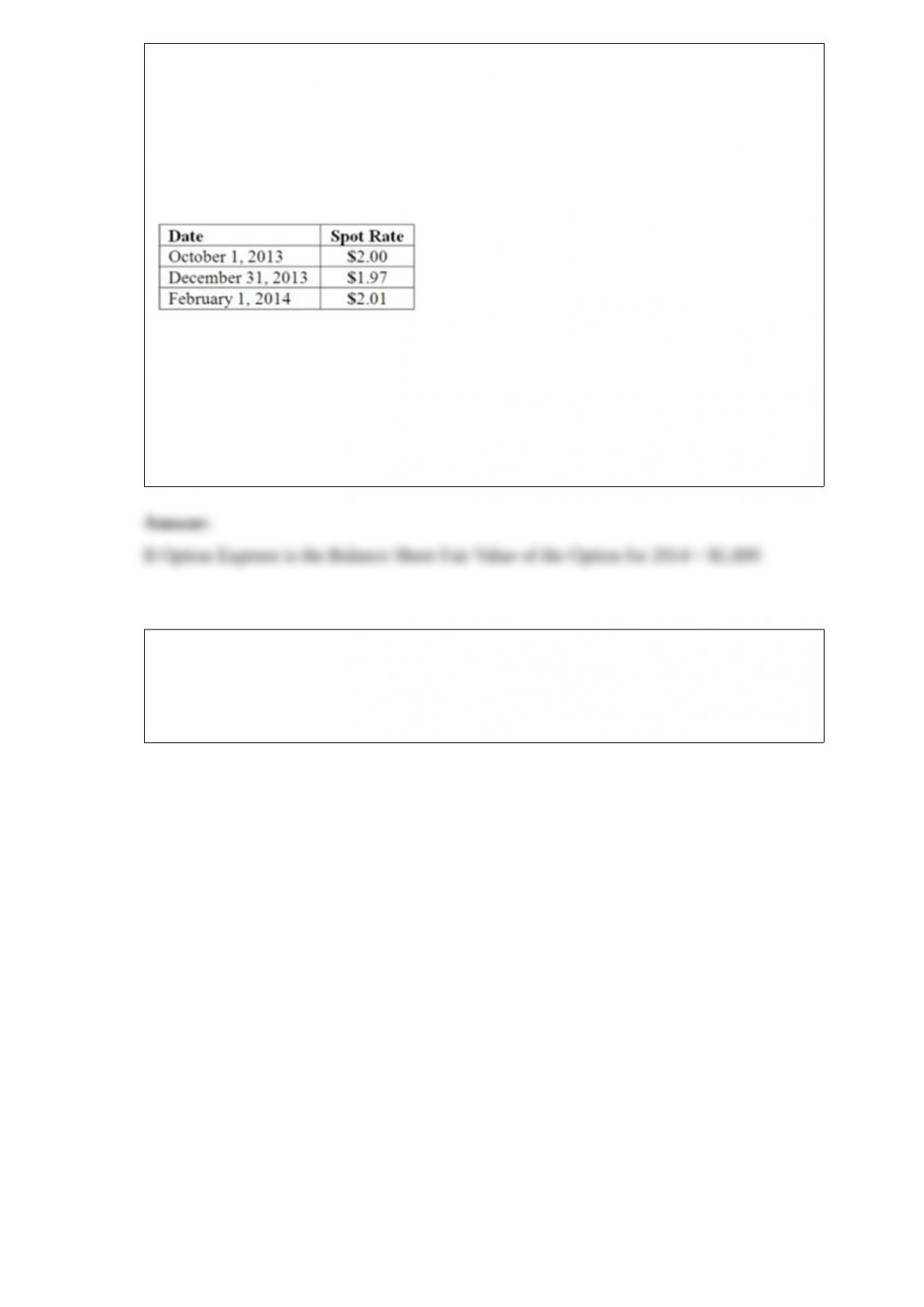

13) On October 1, 2013, Eagle Company forecasts the purchase of inventory from a

British supplier on February 1, 2014, at a price of 100,000 British pounds. On October

1, 2013, Eagle pays $1,800 for a three-month call option on 100,000 pounds with a

strike price of $2.00 per pound. The option is considered to be a cash flow hedge of a

forecasted foreign currency transaction. On December 31, 2013, the option has a fair

value of $1,600. The following spot exchange rates apply:

What is the amount of option expense for 2014 from these transactions?

A.$1,000

B.$1,600

C.$2,500

D.$2,600

E.$0

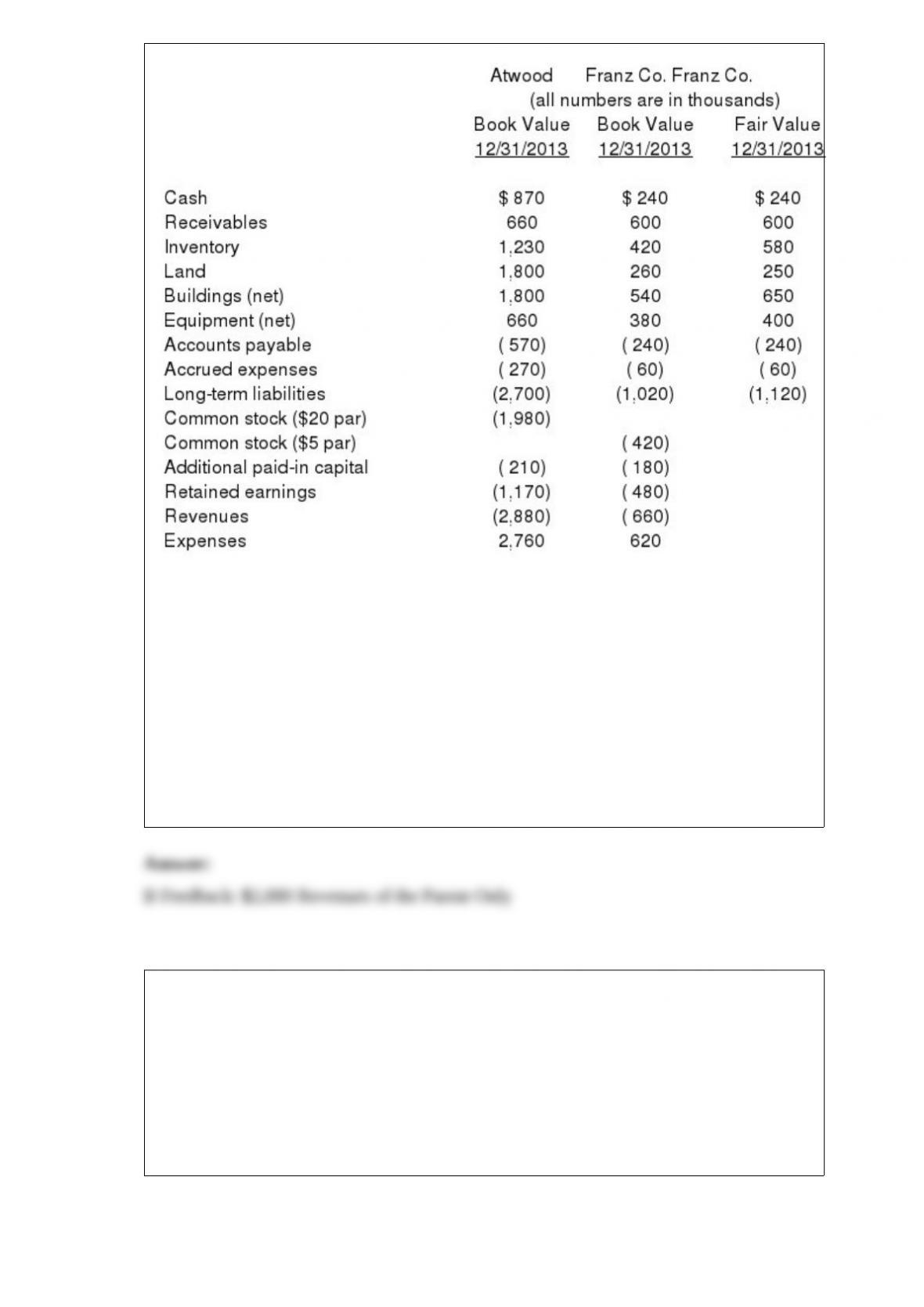

14) The financial balances for the Atwood Company and the Franz Company as of

December 31, 2013, are presented below. Also included are the fair values for Franz

Company’s net assets.

Note: Parenthesis indicate a credit balance

Assume an acquisition business combination took place at December 31, 2013. Atwood

issued 50 shares of its common stock with a fair value of $35 per share for all of the

outstanding common shares of Franz. Stock issuance costs of $15 (in thousands) and

direct costs of $10 (in thousands) were paid.

Compute consolidated revenues at the date of the acquisition.

A) $3,540.

B) $2,880.

C) $1,170.

D) $1,650.

E) $4,050.

15) Wilson owned equipment with an estimated life of 10 years when it was acquired

for an original cost of $80,000. The equipment had a book value of $50,000 at January

1, 2012. On January 1, 2012, Wilson realized that the useful life of the equipment was

longer than originally anticipated, at ten remaining years.

On April 1, 2012 Simon Company, a 90% owned subsidiary of Wilson Company,

bought the equipment from Wilson for $68,250 and for depreciation purposes used the

estimated remaining life as of that date. The following data are available pertaining to

Simon’s income and dividends:

Compute Wilson’s share of income from Simon for consolidation for 2014.

A) $118,825.

B) $115,000.

C) $117,000.

D) $119,000.

E) $118,800.

16) Salem Co. had the following account balances as of December 1, 2012:

Bellington Inc.

transferred $1.7 million in cash and 12,000 shares of its newly issued $30 par value

common stock (valued at $90 per share) to acquire all of Salem’s outstanding common

stock.

Determine the balance for Goodwill that would be included in a December 1, 2012,

consolidation.

17) Candice Company is currently going through bankruptcy reorganization. The

accountant has determined the following balances of the accounts at December 31,

2013.

Prepare the balance sheet for Candice Company. Retained earnings will need to be

calculated.

19) Fargus Corporation owned 51% of the voting common stock of Sanatee, Inc. The

parent’s interest was acquired several years ago on the date that the subsidiary was

formed. Consequently, no goodwill or other allocation was recorded in connection with

the acquisition price.

On January 1, 2012, Sanatee sold $1,400,000 in ten-year bonds to the public at 108. The

bonds pay a 10% interest rate every December 31. Fargus acquired 40% of these bonds

on January 1, 2014, for 95% of the face value. Both companies utilized the straight-line

method of amortization.

What consolidation entry would be recorded in connection with these intra-entity bonds

on December 31, 2016?

20) On January 1, 2013, Wakefield City purchased $40,000 office supplies. During the

year $35,000 of these supplies were used.

Required:

Record the journal entries for these transactions using the consumption method.

(Disregard the encumbrance entries.)

21) Hampton Company is trying to decide whether to seek liquidation or

reorganization. Hampton has provided the following balance sheet:

Additional information is as follows:

– The investments are currently worth $13,000.

– It is estimated that $32,000 of the accounts receivable are collectible.

– The inventory can be sold for $74,000.

– The prepaid expenses and the intangible assets have no net realizable value.

– The land and building are currently valued at $250,000.

– The equipment can be sold for $60,000.

– Administrative expenses (not yet recorded) are estimated to be $12,500.

– Accrued expenses include $17,000 of salaries payable ($11,000 to one employee and

$3,000 each to two other employees).

– Accrued expenses include $7,000 of unpaid payroll taxes.

What is the payout percentage to unsecured creditors? (Round the percentage to a

whole number and two decimal places.)

22) Skipen Corp. had the following stockholders’ equity accounts:

The preferred stock was participating and is therefore considered to be equity. Vestin

Corp. acquired 90% of this common stock for $2,250,000 and 70% of the preferred

stock for $1,120,000. All of the subsidiary’s assets and liabilities were determined to

have fair values equal to their book values except for land which is undervalued by

$130,000. Required:

What amount was attributed to goodwill on the date of acquisition?

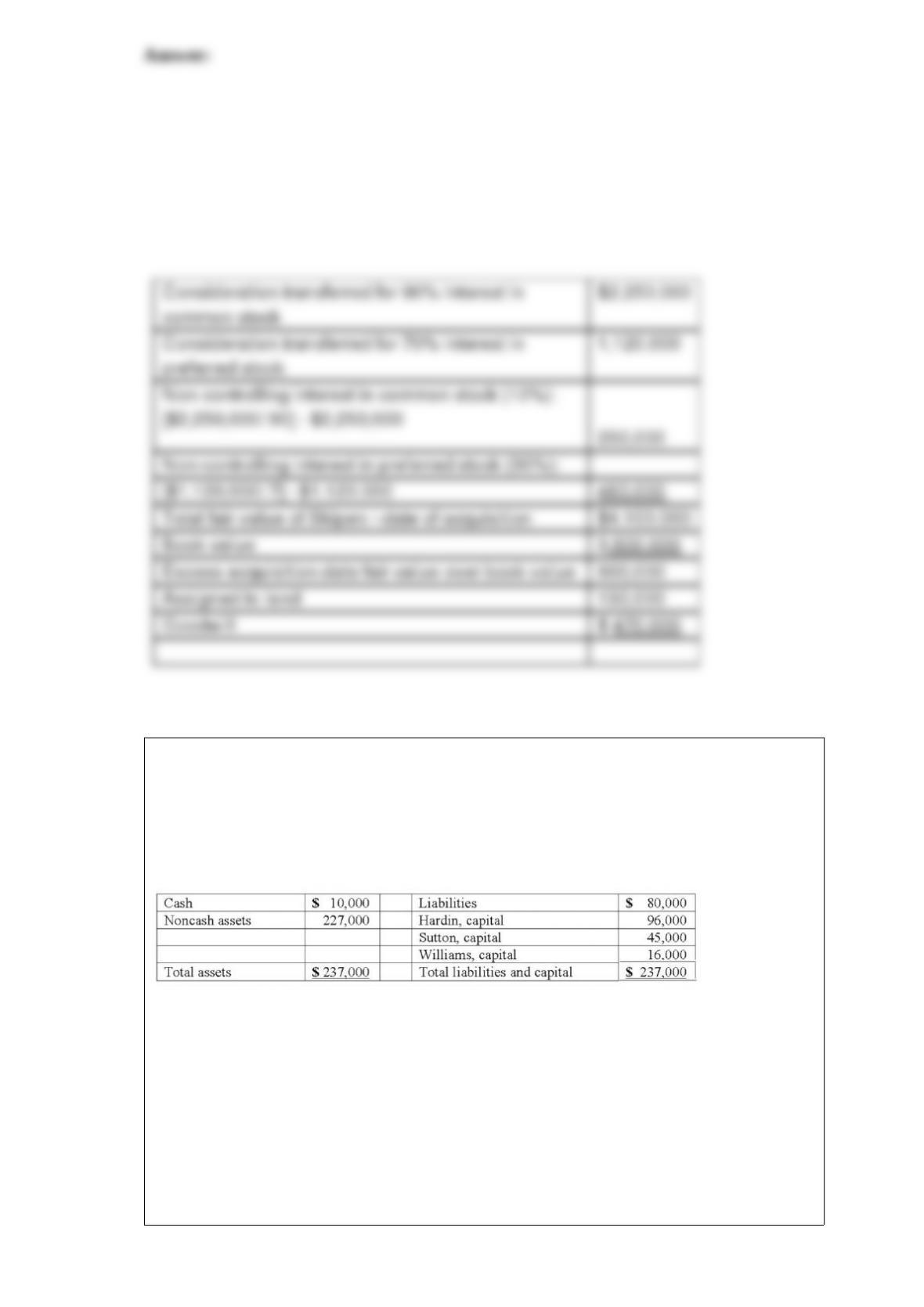

23) Hardin, Sutton, and Williams have operated a local business as a partnership for

several years. All profits and losses have been allocated in a 3:2:1 ratio, respectively.

Recently, Williams has undergone personal financial problems, and is insolvent. To

satisfy Williams’ creditors, the partnership has decided to liquidate.

The following balance sheet has been produced:

During the liquidation process, the following transactions take place:

– Noncash assets are sold for $116,000.

– Liquidation expenses of $12,000 are paid. No further expenses are expected.

– Safe capital distributions are made to the partners.

– Payment is made of all business liabilities.

– Any deficit capital balances are deemed to be uncollectible.

Prepare journal entries to record the actual liquidation transactions.

24) Jones, Marge, and Tate LLP decided to dissolve and liquidate the partnership on

September 30, 2013. After realization of a portion of the noncash assets, the capital

account balances were Jones $50,000; Marge $40,000; and Tate $15,000. Cash of

$35,000 and other assets with a carrying amount of $100,000 were on hand. Creditors’

claims totaled $30,000. Jones, Marge, and Tate shared net income and losses in a 2:1:1

ratio, respectively.

Prepare a working paper to compute the amount of cash that may be paid to creditors

and to partners at this time, assuming that no partner is solvent.

25) The City of Kamen collected $17,000 from parking meters that must be transferred

to the county government.