25. (15 minutes) (Determine the amounts at which foreign currency balances are

reported on a foreign subsidiary’s trial balance and in the parent’s

consolidated financial statements)

a. Remeasurement of Swiss franc (CHF) balances into Israeli shekels (ILS)

to report on the Israeli subsidary’s trial balance.

December 31, 2015 CHF Exchange Rate ILS*

Interest expense 25,000 x 3.95 A = 98,750

b. Translation of remeasured Swiss franc (CHF) balances into U.S. dollars

(USD) to report in the U.S. parent’s consolidated financial statements.

December 31, 2015 ILS Exchange Rate USD**

Interest expense 98,750 x 0.27 A = 26,662.50

statements

26. (30 minutes) (Prepare financial statements for a foreign subsidiary and then

translate them into U.S. dollars)

Fenwicke Company Subsidiary

Income Statement

LCU U.S. Dollars

Rent revenue 60,000 x $1.90 A = $114,000

Interest expense (10,000) x $1.90 A = (19,000)

* Repair expense is the only expense not incurred evenly throughout the

year.

Statement of Retained Earnings

LCU U.S. Dollars

Retained earnings, 1/1 –0- -0-

Net income 32,000 (above) $61,000

Balance Sheet

Cash 41,000x $1.80 C = $ 73,800

Accounts receivable 10,000x $1.80 C = 18,000

Building 140,000x $1.80 C = 252,000

Accumulated depreciation (14 ,000)x $1.80 C = (25 ,200)

Total assets 177 ,000 $318 ,600

Interest payable 10,000x $1.80 C = $ 18,000

Total liabilities and equities 177 ,000 $318 ,600

Computation of Translation Adjustment

Beginning net assets -0- -0-

Increase in net assets:

Issued common stock 40,000 x $2.00 = $ 80,000

Net income 32,000 (above) 61,000

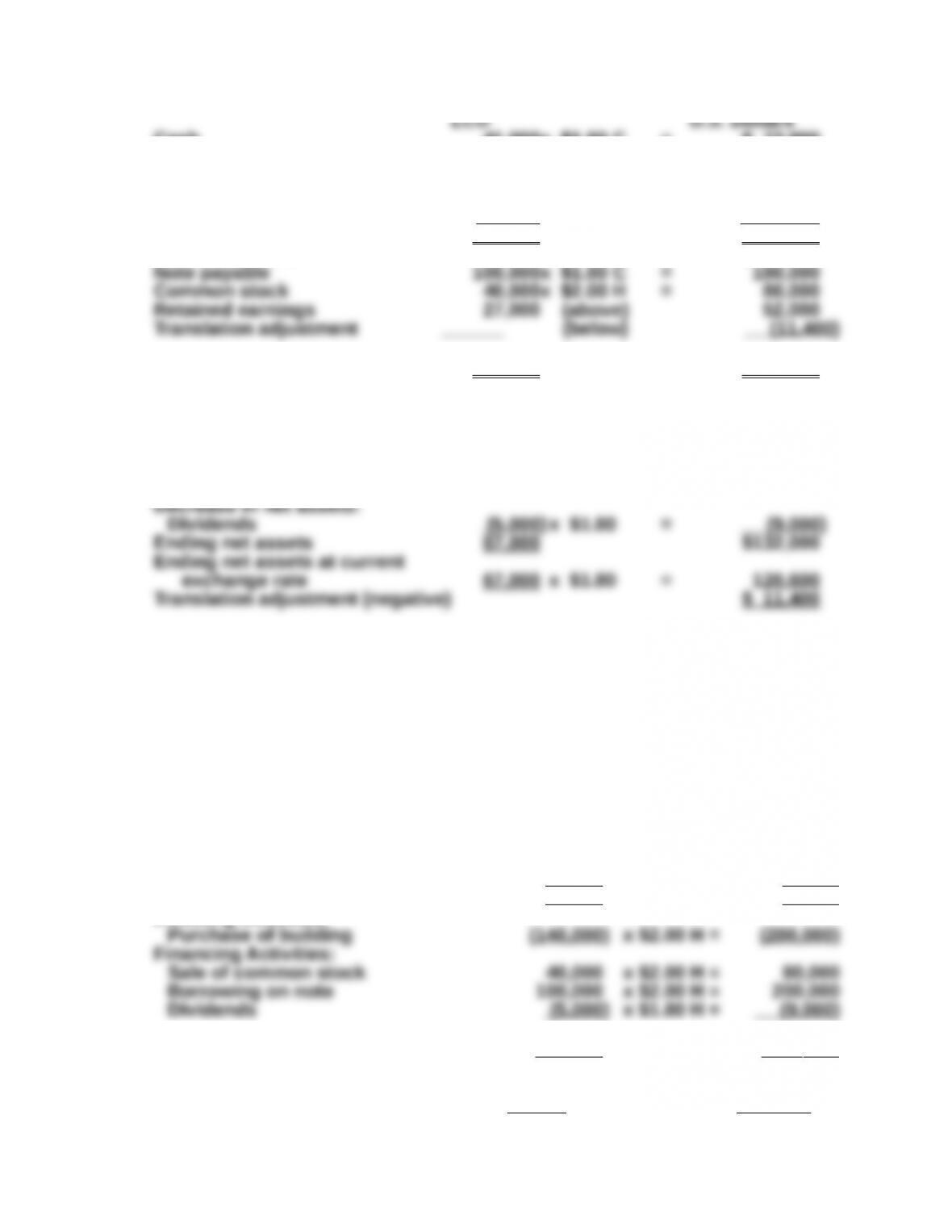

27. (30 minutes) (Prepare a statement of cash flows for a foreign subsidiary and then translate

it into U.S. dollars)

Fenwicke Company Subsidiary

Statement of Cash Flows

LCU U.S. Dollars

Operating Activities:

Net income 32,000 (from prob 26)

plus: depreciation 14,000 x $1.90 A = 26,600

less: increase in accounts receivable (10,000) x $1.90 A = (19,000)

plus: increase in interest payable 10 ,000 x $1.90 A = 19 ,000

Cash flow from operations 46 ,000 87 ,600

Investing Activities:

135 ,000 271 ,000

Increase in cash 41,000 78,600

Effect of exchange rate change on cash (4,800)

Cash, 1/1 -0- -0-

Cash, 12/31 41 ,000 x $1.80 C = $ 73 ,800

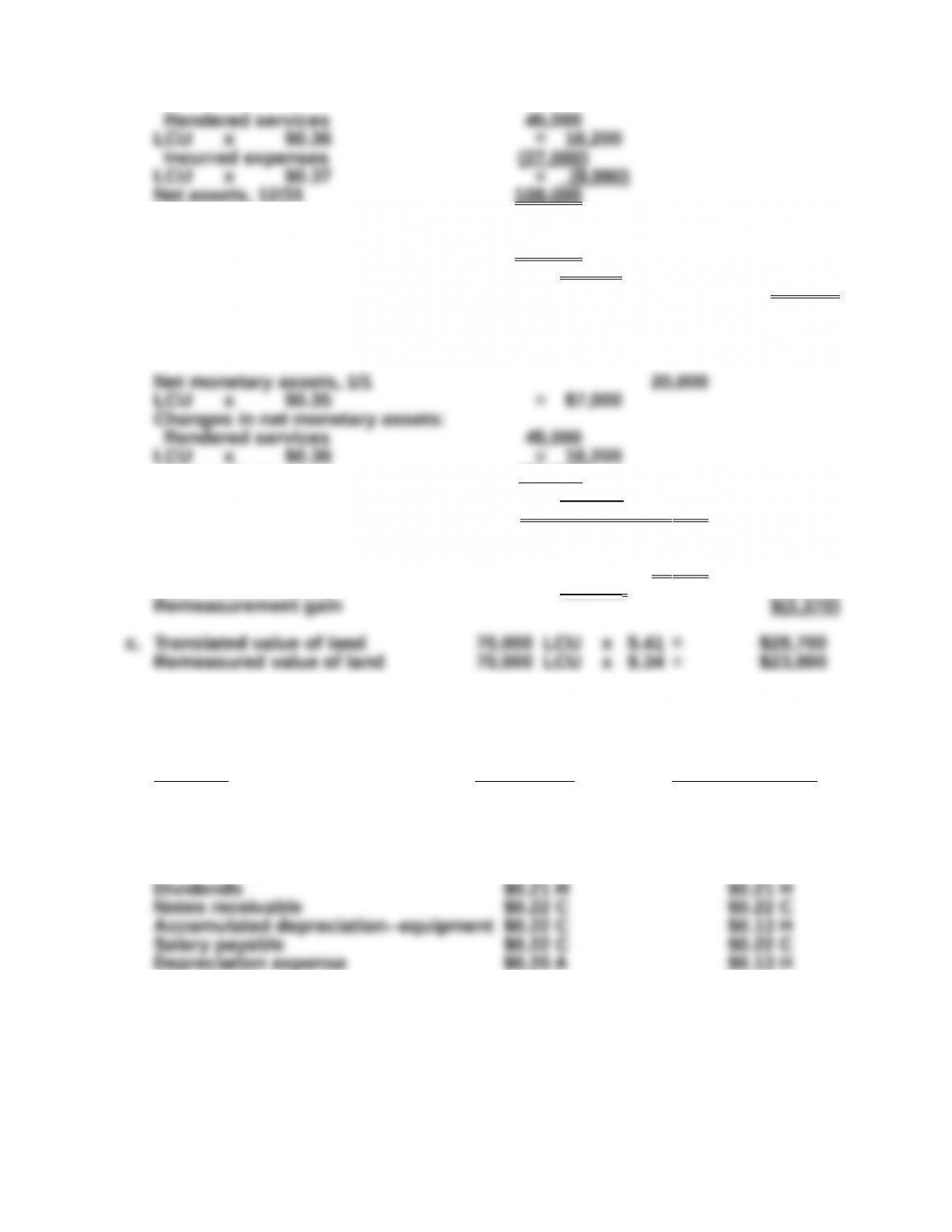

28. (25 minutes) (Compute translation adjustment and remeasurement gain/loss)

a. Translation—only changes in net assets have an impact on the computation of the

translation adjustment.

Net asset balance 1/1 KM30,000 x $.32 = $ 9,600

Increases in net assets (income):

Net asset balance 12/31

at current exchange rate KM31 ,000 x $.42 = (13 ,020)

Translation adjustment—positive $(3 ,340)

b. Remeasurement—only changes in net monetary assets and liabilities have an

impact on the computation of the remeasurement gain.

Beginning net monetary

liability position KM (3,000) x $.32 = $ ( 960)

Decreases in monetary assets:

Bought inventory 10/1 (12,000) x $.39 = (4,680)

Bought land 11/1 (4,000) x $.40 = (1,600)

Note: The purchase of land on account did not result in a decrease in

monetary assets, rather an increase in monetary liabilities. Payment on the

note payable and collection of accounts receivable do not affect the net

monetary liability position.

29. (20 minutes) (Compute translation adjustment and remeasurement gain/loss)

a. The translation adjustment is based on changes in the net assets of the

subsidiary.

Net assets, 1/1 90,000

LCU x $0.35 = $31,500

Changes in net assets:

LCU $37,710

Net assets, 12/31 at

current exchange rate 108 ,000

LCU x $0.41 = 44,280

Translation adjustment (positive) $(6 ,570)

b. The remeasurement gain or loss is based on changes in the net monetary

assets of the subsidiary.

Incurred expenses (27 ,000)

LCU x $0.37 = (9,990)

Net monetary assets, 12/31 38 ,000

LCU $13,210

Net monetary assets, 12/31 at

current exchange rate 38 ,000

LCU x $0.41 = 15,580

30. (10 minutes) (Determine the appropriate exchange rate under the current rate

method [translation] and temporal method [remeasurement])

(a) Current Rate Method (b) Temporal Method

Account Translation Remeasurement

Sales $0.20 A $0.20 A

Inventory $0.22 C $0.19 H

Equipment $0.22 C $0.13 H

Rent expense $0.20 A $0.20 A

C = current exchange rate, A = average exchange rate, H = Historical

exchange rate

31. (30 minutes) (Determine translation adjustment; prepare journal entries for forward

contract hedge of balance sheet exposure; determine amount to be reported in accumulated

other comprehensive income)

a. Net assets, 1/1 (132,000 – 54,000) 78,000 kitesx $0.80 = $62,400

Change in net assets:

Net assets, 12/31 94 ,000 kites $74,720

Net assets at current

exchange rate, 12/31 94 ,000 kitesx $0.75 = 70 ,500

Translation adjustment (negative) $ 4 ,220

b. Forward contract journal entries

10/1 No entry

12/31 Forward Contract…………..………………… 2,000

Translation Adjustment (positive). . 2,000

(To record the change in the value of the forward contract as

an adjustment to the translation adjustment)

Foreign Currency (kites)……….…….. 150,000

Forward Contract……….…….…….….. 2,000

(To record delivery of 200,000 kites, receipt of $152,000, and

close the forward contract account.)

$2,000).

32. (45 minutes) (Translation and remeasurement of foreign subsidiary trial

balance)

a. Translation of Subsidiary Trial Balance

Debits Credits

Cash…………………………………. 8,000 KQ x 1.62$12,960

Accounts Receivable…………….. 9,000 KQ x 1.62 14,580

Notes Payable…………………….. 5,000 KQ x 1.62 8,100

Common Stock…………………… 10,000 KQ x 1.71 17,100

Dividends……….…………………. 4,000 KQ x 1.66 6,640

Sales………………………………… 25,000 KQ x 1.64 41,000

Salary Expense…………………… 5,000 KQ x 1.64 8,200

Depreciation Expense…………… 600 KQ x 1.64 984

$72,032 $72,032

Calculation of Translation Adjustment

Net assets, 1/1………………………….. -0- -0-

Increase in net assets:

Common stock issued………………. 10,000 KQx 1.71 $17,100

Sales……………………………………. 25,000 KQx 1.64 41,000

Decrease in net assets:

Net assets, 12/31………………………. 16 ,400* KQ $27,516

Net assets, 12/31 at

current exchange rate……………. 16 ,400 KQx 1.62 26 ,568

Translation adjustment (negative) $ 948

* This amount can be verified as ending assets (24,400 KQ) minus ending

liabilities (8,000 KQ) – net assets, 12/31 = 16,400 KQ.

32. (continued)

b. Remeasurement of Subsidiary Trial Balance

Debits Credits

Cash 8,000 KQ x 1.62 $12,960

Accounts Receivable 9,000 KQ x 1.62 14,580

Notes Payable 5,000 KQ x 1.62 8,100

Common Stock 10,000 KQ x 1.71 17,100

Dividends 4,000 KQ x 1.66 6,640

Sales 25,000 KQ x 1.64 41,000

Salary Expense 5,000 KQ x 1.64 8,200

Depreciation Expense 600 KQ x 1.71 1,026

Calculation of Remeasurement Loss

Net monetary assets, 1/1 -0- -0-

Increase in net monetary assets:

Common stock issued 10,000

KQ x 1.71 $17,100

Sales 25,000

Dividends (4,000) KQ x 1.66

(6,640)

Salary expense (5,000) KQ x 1.64

(8,200)

Miscellaneous expense (9 ,000) KQ x 1.64 (14 ,760)

* This amount can be verified as ending assets (17,000 KQ) minus ending

liabilities (8,000 KQ) – net assets, 12/31 = 9,000 KQ.

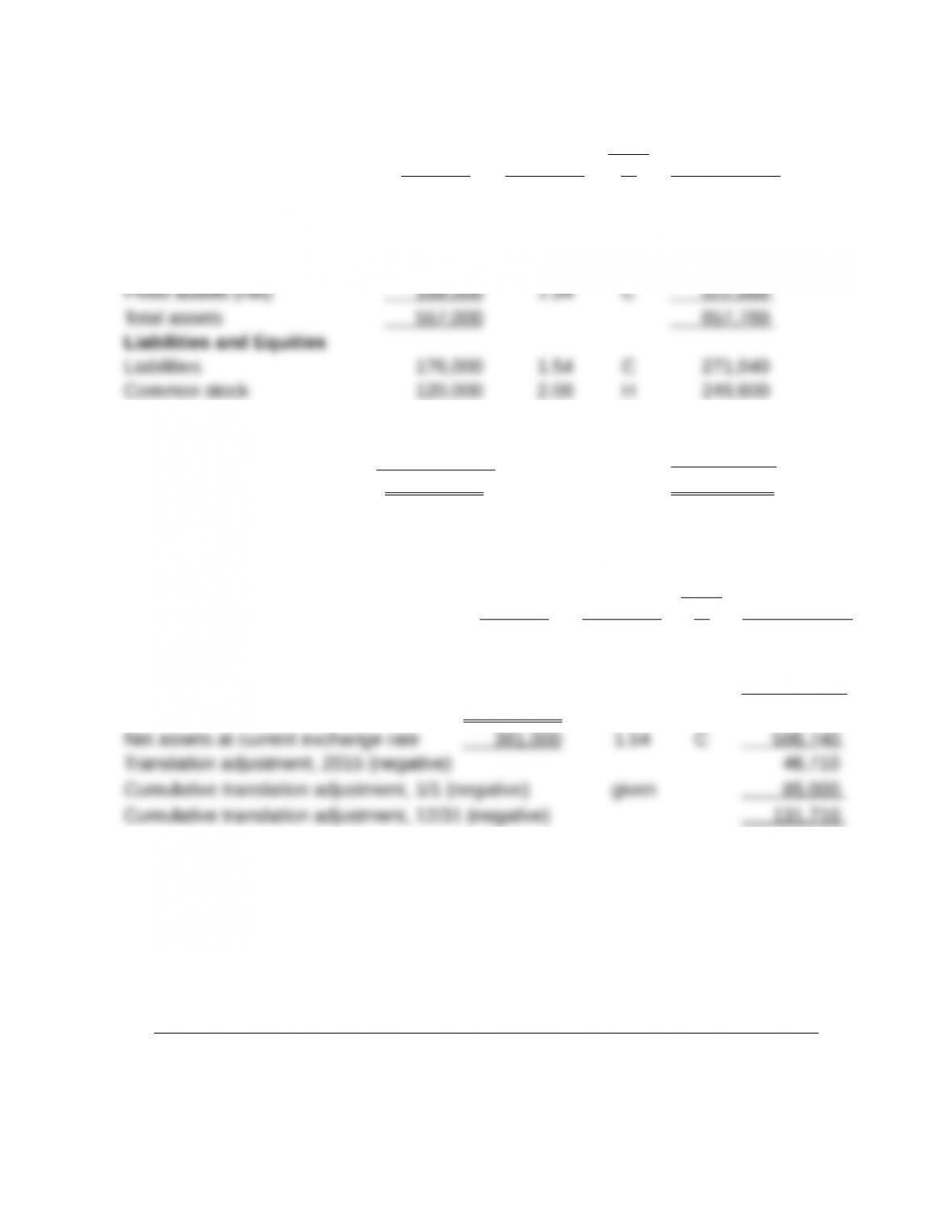

33. (30 minutes) (Translate financial statements of a foreign subsidiary)

LIVINGSTON COMPANY

Income Statement

For the Year Ending December 31, 2015

Goghs Ex Rate

Cod

e U.S. Dollars

Sales 270,000 1.59 A 429,300

Cost of goods sold (155,000) 1.59 A (246,450)

Net income 71,000 114,190

Statement of Retained Earnings

For the Year Ending December 31, 2015

Goghs Ex Rate

Cod

e U.S. Dollars

Retained earnings, 1/1 216,000 given 395,000

Balance Sheet

December 31, 2015

Goghs Ex Rate

Cod

e U.S. Dollars

Assets

Cash 44,000 1.54 C 67,760

Receivables 116,000 1.54 C 178,640

Inventory 58,000 1.54 C 89,320

Retained earnings, 12/31 261,000

abov

e 467,330

Translation adjustment (131,710)

Total liabilities and equities 557,000 856,260

33. (continued)

Calculation of Translation Adjustment:

Goghs Ex Rate

Cod

e U.S. Dollars

Net assets, 1/1 336,000 1.67 BOY 561,120

Net income 71,000 above 114,190

Dividends (26,000) above (41,860)

Net assets, 12/31 381,000 633,450

Code: A = average; C = current; H = historical; BOY = beginning of year

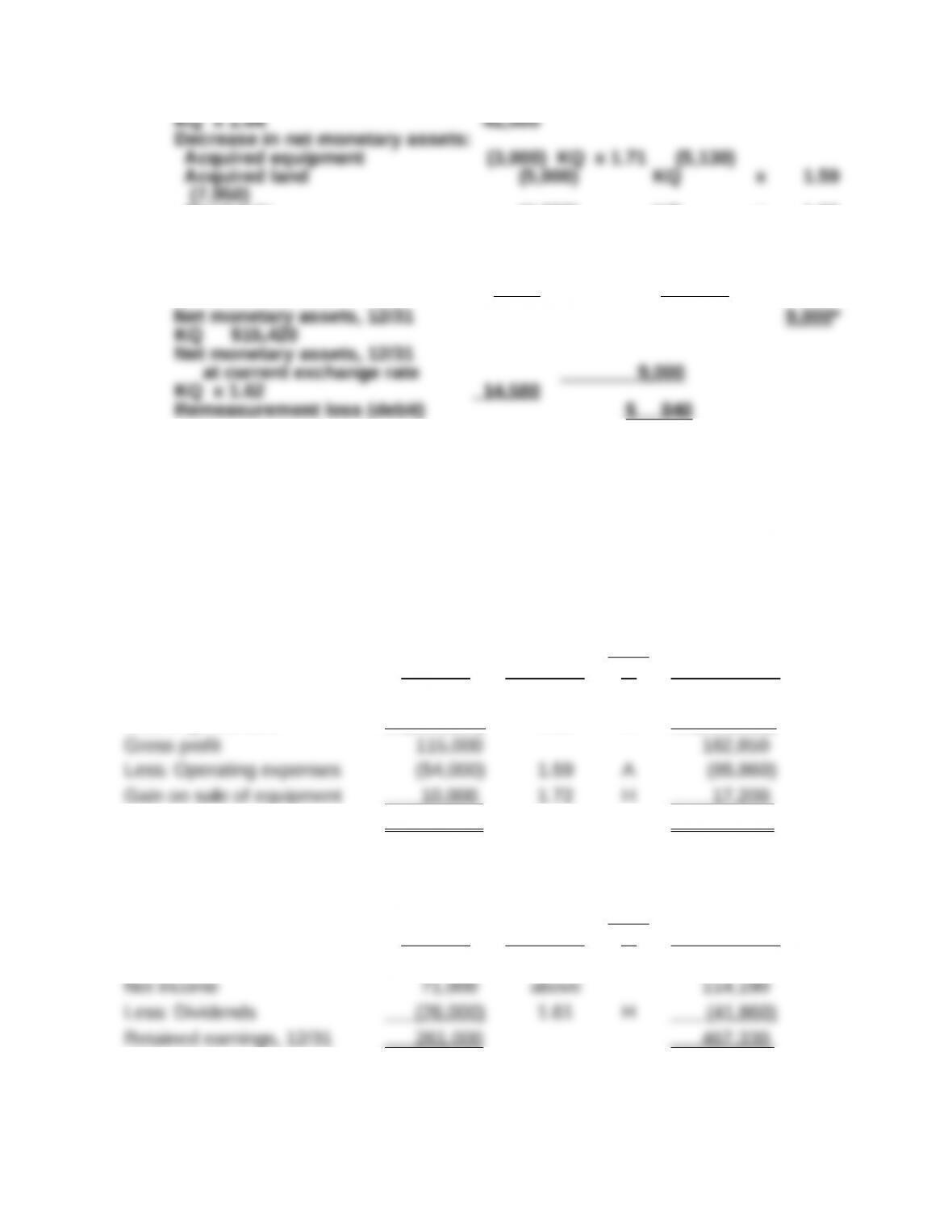

34. (35 minutes) (Compute remeasurement gain/loss and translation adjustment)

a. Remeasurement Gain or Loss

Exchange

KR Rate US$

Net monetary assets, 1/1/15* 35,000

x $3.00 = $105,000

Increases in net monetary assets:

Issued Common Stock (4/1/15) 13,000

x $3.10 = 40,300

Sold Building** (7/1/15) 10,000

x $3.30 = 33,000

Sales (2015) 162,000

x $3.20 = 518,400

Decreases in net monetary assets:

Purchased Equipment (4/1/15) (64,000)

Salary Expense (2015) (45,000)

x $3.20 = (144,000)

Utilities Expense (2015) (7 ,000)

x $3.20 = (22,400)

Net monetary assets, 12/31/15 25 ,500

$69,300

Net monetary assets, 12/31/15 at

* Net monetary assets: (Cash + Accounts Receivable) – (Account Payable +

Bonds Payable)

** Cash proceeds from the sale of the building of KR10,000 is determined by

adding the Book value of the building sold of KR1,500 and the Gain on

sale of building of KR 8,500.

b. Translation Adjustment

Exchange

KR Rate US$

Net assets, 1/1/15* 124,000

x $3.00 = $372,000

Increases in net monetary assets:

Decreases in net monetary assets:

Paid Dividends (10/1/15) (57,000)

x $3.40 = (193,800)

Depreciation expense (2015) (40,000)

x $3.20 =(128,000)

Rent Expense (2015) (21,500)

x $3.20 = (68,800)

Net monetary assets, 12/31/15 at

current exchange rate 137 ,000

x $3.50 = 479,500

Translation adjustment (credit) $ (77 ,750)

* Net assets: Common stock + Retained earnings

** Selling a building at a gain of KR 8,500 increases net assets by that

amount.

35. (90 minutes) (Remeasure non-functional currency accounts into foreign

functional currency and then translate foreign functional currency financial

statements into U.S. dollars)

a. Remeasurement of Mexican Operations

Canadian Dollars

Pesos Debit Credit

Accounts payable 49,000

17,150

Accumulated depreciation 19,000

4,750

Building and equipment 40,000

6,900

Inventory (ending

—income statement) 28,000

9,520

Inventory (ending—balance sheet) 28,000

9,520

Purchases 68,000

Sales 124,000

42,160

Main o(ce 30,000

given 7,530

Remeasurement loss Schedule One 10

Schedule One—Remeasurement Loss Pesos Canadian Dollars

Net monetary liabilities, 1/1/15* (16,000)x .32 (5,120)

Increases in net monetary assets

Net monetary assets, 12/31/15** 31 ,000 10,860

Net monetary assets, 12/31/15 at

current exchange rate 31 ,000x .35 10 ,850

Remeasurement loss 10

* Net monetary liabilities, 1/1/15, can be determined by first determining the

net monetary assets at 12/31/15 and then backing out the changes in