35. (Acquisition Method Consolidated Balances)

Adjustments

December 31, 2015 Paloma San Marco & Eliminations NCI Consolidated

Revenues (1,843,000) (675,000) (2,518,000)

Cost of goods sold 1,100,000 322,000 1,422,000

net income (437,000) (215,000)

Consolidated net income (450,500)

To noncontrolling interest (13,500) (13,500)

To Paloma Company (437,000)

Current Assets 1,204,000 430,000 1,634,000

Investment in San Marco 1,854,000 (D) 22,500 (S)769,500

(A)985,500 -0-

(I) 121,500

Customer base -0- -0- (A)720,000 (E) 80,000 640,000

Accounts Payable (485,000) (200,000) (685,000)

Notes Payable (542,000) (155,000) (697,000)

NCI in San Marco (S) 85,500

(A)109,500 (195,000)

(206,000) (206,000)

35. (Continued)

Controlling Noncontrolling

Interest Interest

Fair value at acquisition date $1,710,000 $190,000

Relative fair values of identifiable net assets

equally by $22,500 as follows:

Fair value of San Marco Company (1,710,000 + 167,500) $1,877,500

Carrying amount acquired 725,000

Excess fair value 1,152,500

to customer base 800,000

* NCI at beginning of year

Common stock-subsidiary $400,000

APIC-subsidiary 60,000

Retained earnings-subsidiary 1/1 395,000

Total $855,000

Controlling Noncontrolling

Interest Interest

Fair value at acquisition date $1,710,000 $167,500

Relative fair values of identifiable net assets

90% and 10% of $1,525,000 (acquisition date

36. (60 Minutes) (Consolidation worksheet and income statement with parent

using initial value method. Also consolidated balances with a control

premium paid by parent.)

a. Fair Value Allocation and Amortization

Consideration transferred by Holtz…….…...... $576,000

accounts based on fair value: life amortizations

Building……….…………………..………………….. 85,500

5 years………………..…………………….$17,100

Trademark …………….………………….…..….… 64 ,000

10 years……….………..…………………… 6,400

Change in subsidiary RE from 1/1/14 to 1/1/15........ $70,000

Excess amortization for 2014….………....................... 23,500

Adjusted subsidiary RE increase….………….............. $46,500

Percentage ownership by parent…........................... 80%

*C conversion entry………………………………………….... $37,200

of the noncontrolling interest for its share.

Entry I: Eliminates Intra-entity dividends declared by subsidiary and

recorded as income by parent.

Entry E: Recognizes amortization expense for current year.

Columnar entry—Recognizes net income attributable to noncontrolling

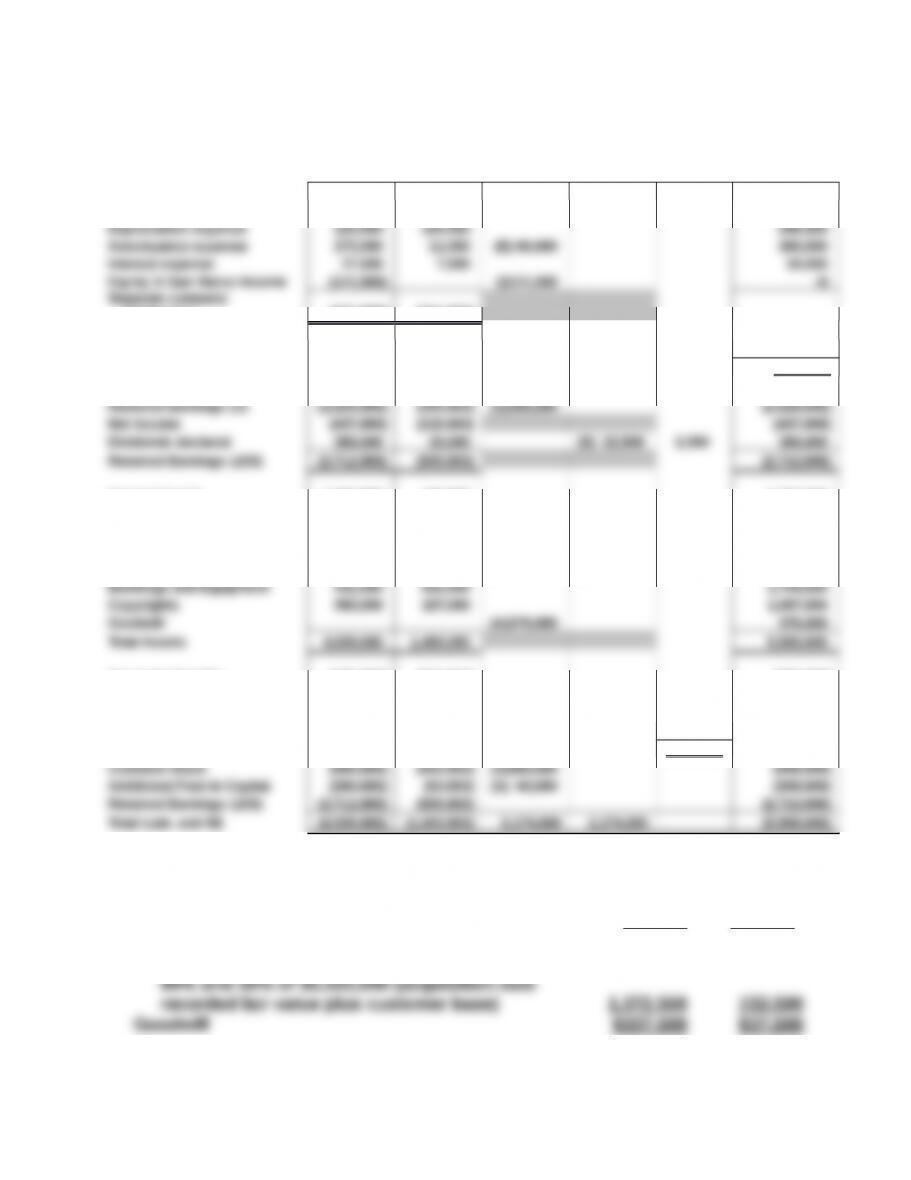

36. a. (continued) HOLTZ CORPORATION AND DEVINE, INC.

Consolidation Worksheet

For Year Ending December 31, 2015

Holtz Devine Consolidation

Entries Noncontrolling Consolidated

Accounts Corporation Inc. Debit Credit

Interest Totals

Sales (641,000) (399,000)

(1,040,000)

422,500

Dividend income (16 ,000) ___ _-0 – (I) 16,000

-0-

Separate company net income (186 ,000) (97 ,000)

NI attributable to Holtz Corp.

(228,800)

Retained earnings, 1/1 (762,000) (296,500) (S) 296,500 (*C)

37,200 (799,200)

Net income (above) (186,000) (97,000)

Current assets 121,000 120,500

241,500

Investment in Devine 576,000 -0- (*C) 37,200

(S)317,200 -0-

(A)296,000

244,000

Total assets 1 ,733,000 691 ,500

2,195,000

Liabilities (535,000) (218,000)

(753,000)

79,300

(A)

74,000 (153 ,300)

NCI in Devine, 12/31

(164,000) (164 ,000)

36. (continued)

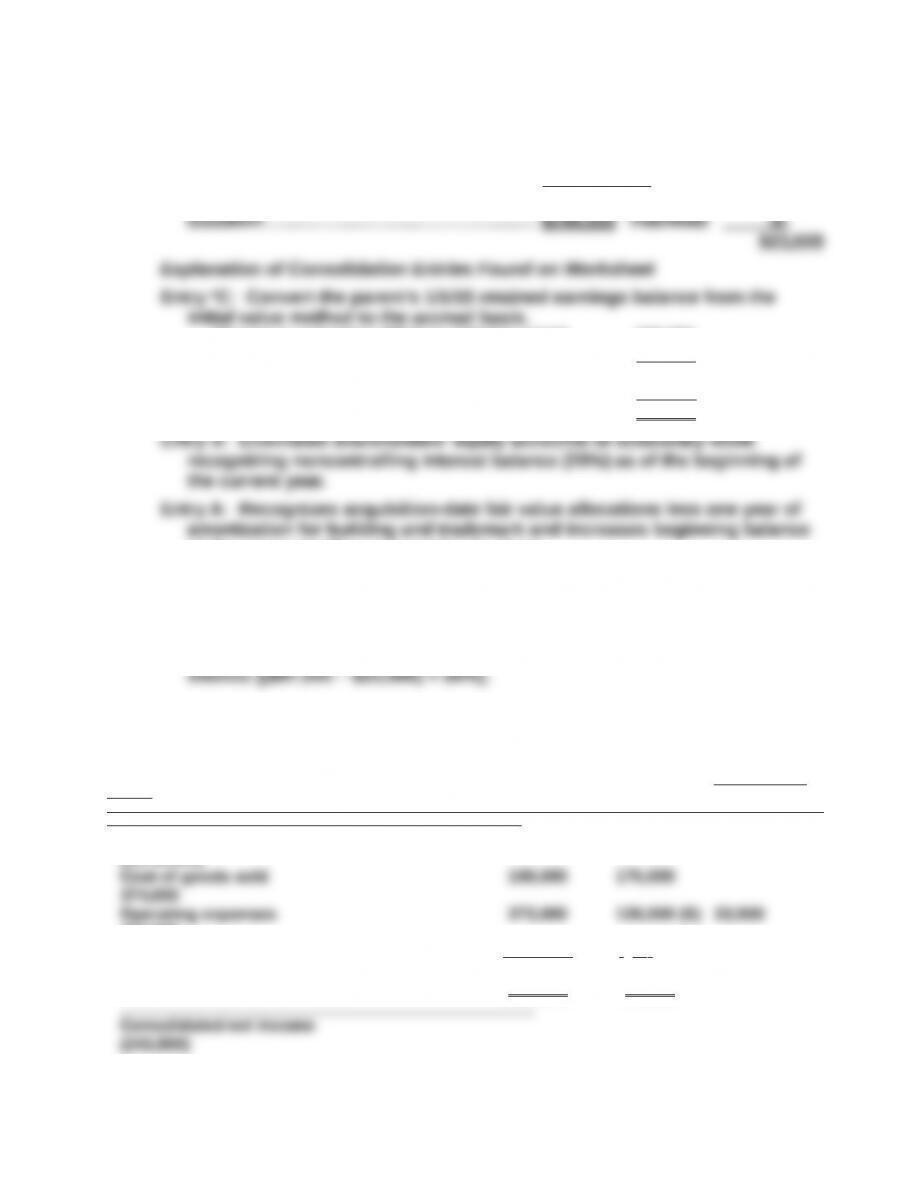

b. HOLTZ CORPORATION AND DEVINE, INC.

Consolidated Income Statement

For Year Ending December 31, 2015

Sales $1,040,000

To Holtz Corporation $228 ,800

c. Consideration transferred by Holtz for 80% of Devine $576,000

Noncontrolling interest fair value ($4.76 × 20,000 shares) 95 ,200

Devine fair value $671,200

Fair value of Devine’s underlying net assets 476 ,000

acquisition-date fair value:

(S) Common stock-Devine 100,000

Retained earnings- Devine 1/1 296,500

Investment in Devine 317,200

Noncontrolling interest 79,300

Investment in Devine 195,200

Controlling

Noncontrolling

Interest Interest

Fair value at acquisition date $576,000 $95,200

37. (40 Minutes) (Determine consolidated balances.)

Acquisition-date subsidiary fair value (given).... $1,003,400

Book value of subsidiary (given) ..….…..…..…..... (690 ,000)

Fair value in excess of book value .…..…............ $313,400

Allocations to specific accounts based on difference

313,400

Total………………………..…………………..….. -0-

Annual excess amortizations:

Buildings and equipment [$(24,000) ÷ 10 years] $(2,400)

Depreciation expense = $283,200 (add the two book values less $2,400

excess adjustment)

Amortization expense = $10,800 (add the two book values plus $4,700

excess adjustment)

Consolidated net income = $516,280 (revenues less expenses)

Net income attributable to noncontrolling interest = $44,280 ($226,000

reported subsidiary net income less $4,600 net excess amortization

expense multiplied by 20 percent outside ownership)

37. (continued)

Retained earnings, 12/31 = $1,487,000 (consolidated balance on 1/1 plus net

income to Padre Co. less Padre’s dividends declared) or simply the

parent’s RE because parent employs the equity method.

Total assets = $3,638,860

Accounts payable = $469,000 (add book values)

Notes payable = $700,900 (add the book values less $18,400 excess

allocation plus amortization)

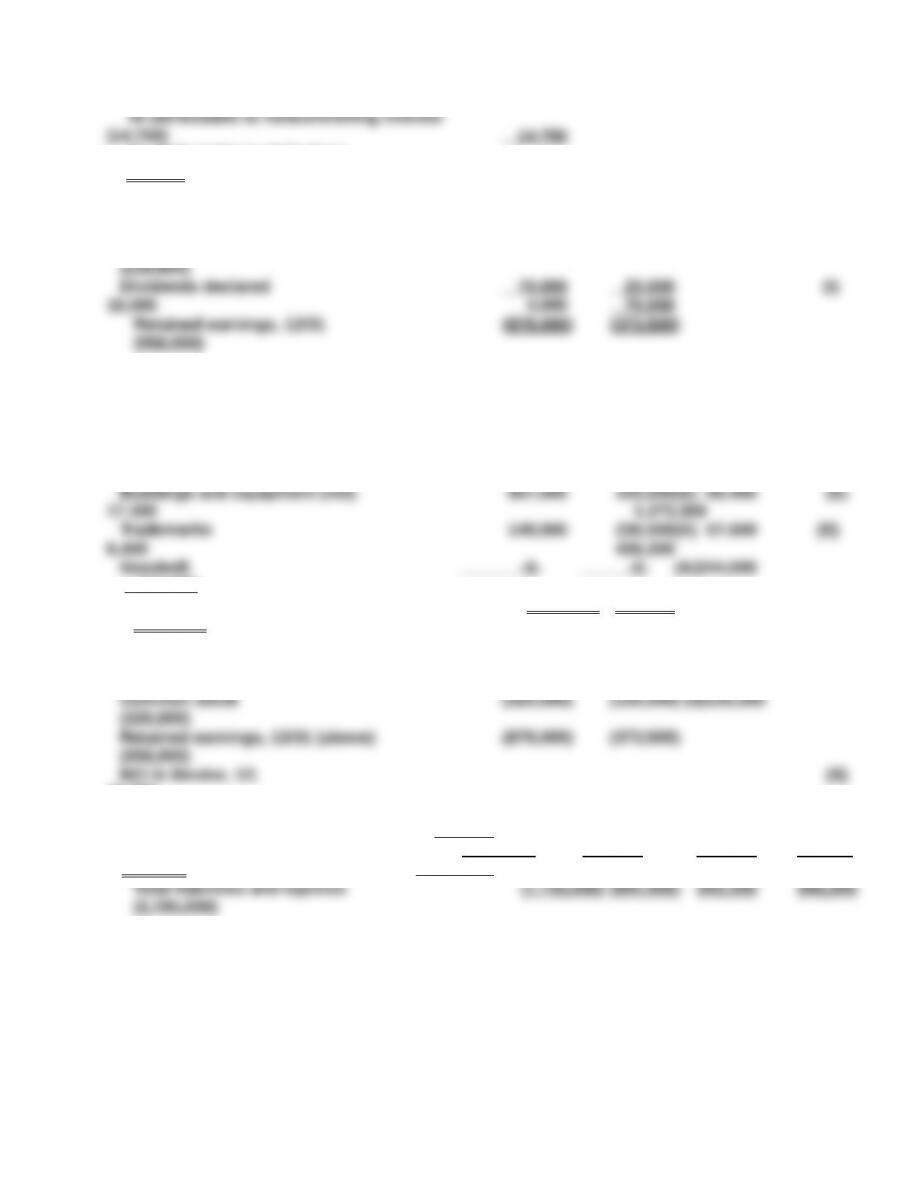

37. (continued) Acquisition Method

Consolidation Entries Noncontrolling Consolidated

Accounts Padre Sierra Debit Credit Interest Totals

Revenues…….……………....................... (1,394,980) (684,900) (2,079,880)

Cost of goods sold…………………......... 774,000 432,000 1,206,000

Depreciation expense…...................... 274,000 11,600 (E) 2,400 283,200

NI to noncontrolling interest........... (44,280) 44 ,280

NI to Padre Company ….................... (472 ,000)

Retained earnings 1/1 ........................ (1,275,000) (530,000) (S) 530,000 (1,275,000)

Net income (above) …......................... (472,000) (226,000) (472,000)

………………………………………..……… (A) 250,720 -0-

Land …………………............................... 360,000 65,000 (A) 225,000 650,000

Buildings and equipment (net).......... 909,000 275,400 (E) 2,400 (A) 24,000 1,162,800

Total assets …..…….……….............. 3 ,053,000 1 ,221,000 3 ,638,860

Common stock …….…......................... (300,000) (100,000) (S) 100,000 (300,000)

Additional paid-in capital….……......... (450,000) (60,000) (S) 60,000 (450,000)

Retained earnings 12/31....(above) … (1 ,487,000) (691 ,000) (1 ,487,000)

Total liab. and stockholders’ equity (3 ,053,000) (1 ,221,000)1,265,920 1,265,920 (3 ,638,860)

38. (55 Minutes) (Consolidated worksheet)

a. Consideration transferred by Adams $603,000

Book value of Barstow (CS + RE 12/31/13) (460 ,000)

Excess fair value over book value 210,000

Excess fair value assigned to specific Remaining Annual excess

accounts based on fair value life amortizations

Land $30,000 — —

Buildings (20,000) 10 years ($2,000)

Equipment 40,000 5 years 8,000

b. Because investment income is exactly 90 percent of Barstow’s reported

earnings, Adams apparently is applying the partial equity method.

c. d. Explanation of Consolidation Entries Found on Worksheet

Entry *C—Converts Adams’s financial records from the partial equity method

to the equity method by recognizing amortization for 2014. Total expense

was $15,000 but only 90 percent (or $13,500) applied to the parent.

Columnar Entry—Recognizes noncontrolling interest’s share of consolidated

net income as follows:

Net income attributable to noncontrolling interest (Columnar Entry)

Barstow reported net income ……………………..………..…..….…..…... $120,000

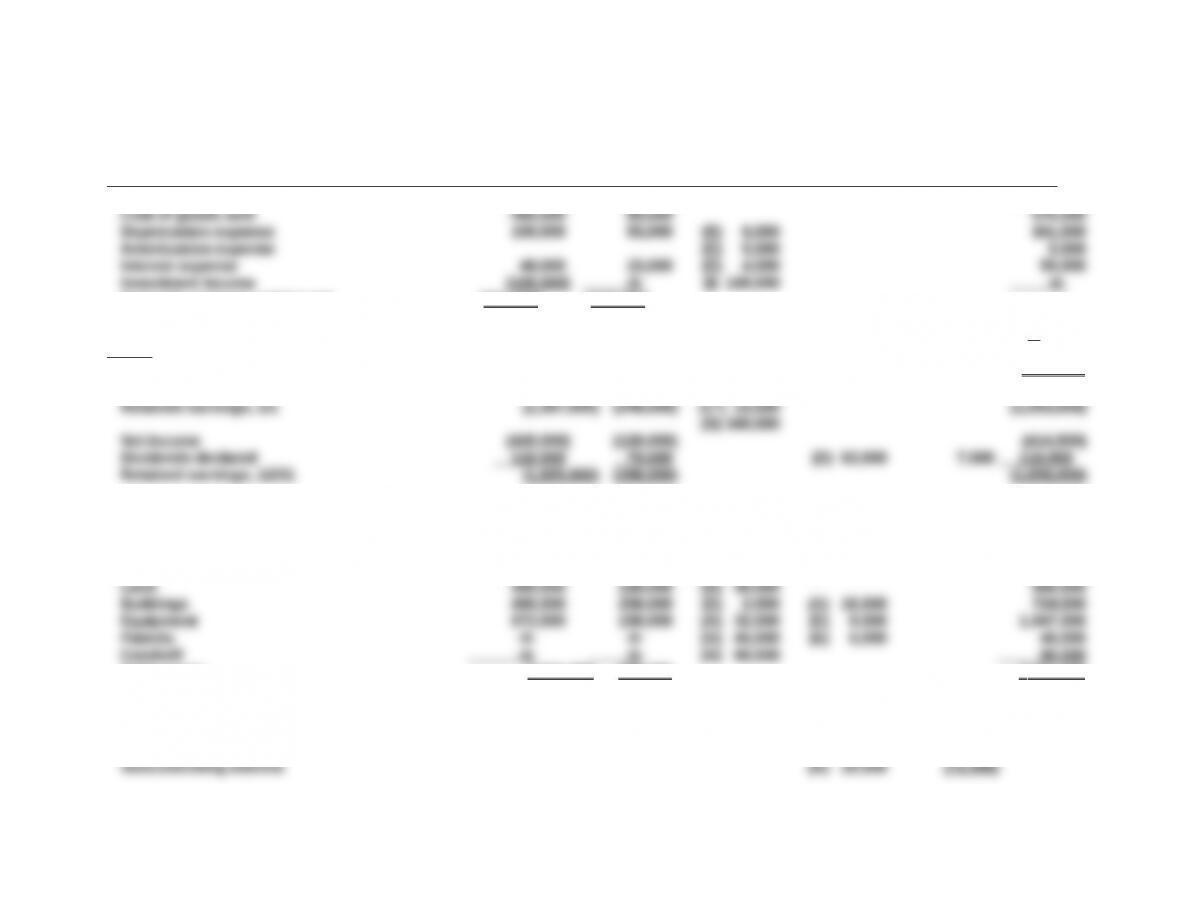

38. c. and d. (continued) ADAMS CORPORATION AND BARSTOW, INC.

Consolidation Worksheet-Acquisition Method

For Year Ending December 31, 2015 Noncontrolling Consolidated

Adams Corp. Barstow Inc. Debit Credit Interest Totals

Revenues (940,000) (280,000) (1,220,000)

Separate company net income (428,000) (120,000)

Consolidated net income (425,000)

NI to noncontrolling interest (10,500)

10,500

NI to Adams Corporation (414 ,500)

Current assets 610,000 250,000 860,000

Investment in Barstow 702,000 (D) 63,000 (*C) 13,500 -0-

(S) 468,000

(A) 175,500

(I) 108,000

Total assets 3 ,055,000 800 ,000 3 ,321,000

Notes payable (860,000) (230,000) (A) 16,000 (E) 4,000 (1,078,000)

Common stock (510,000) (180,000) (S) 180,000 (510,000)

Retained earnings, 12/31 (1,685,000) (390,000) (1,658,000)

(S) 52,000