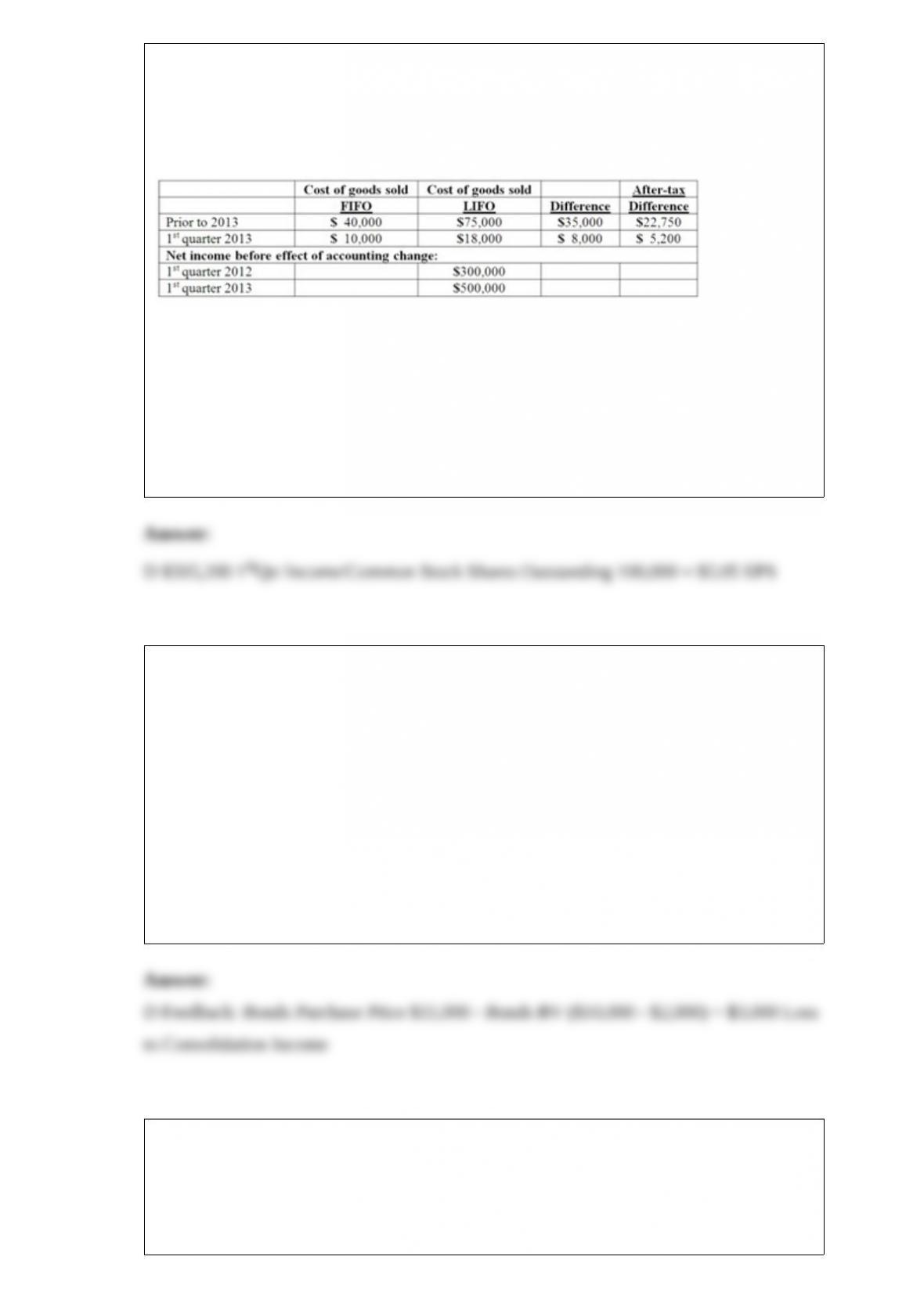

1) Baker Corporation changed from the LIFO method to the FIFO method for inventory

valuation during 2013. Baker has an effective income tax rate of 30 percent and

100,000 shares of common stock issued and outstanding. The following additional

information is available:

Assuming Baker makes the change in the first quarter of 2013, compute net income per

common share.

A.$4.92

B.$4.95

C.$5.00

D.$5.05

E.$5.28

2) Stevens Company has had bonds payable of $10,000 outstanding for several years.

On January 1, 2013, when there was an unamortized discount of $2,000 and a

remaining life of 5 years, its 80% owned subsidiary, Matthews Company, purchased the

bonds in the open market for $11,000. The bonds pay 6% interest annually on

December 31. The companies use the straight-line method to amortize interest revenue

and expense. Compute the consolidated gain or loss on a consolidated income statement

for 2013.

A) $1,000 gain.

B) $1,000 loss.

C) $2,000 loss.

D) $3,000 loss.

E) $3,000 gain.

3) On January 1, 2012, Dawson, Incorporated, paid $100,000 for a 30% interest in

Sacco Corporation. This investee had assets with a book value of $550,000 and

liabilities of $300,000. A patent held by Sacco having a book value of $10,000 was

actually worth $40,000 with a six year remaining life. Any goodwill associated with this

acquisition is considered to have an indefinite life. During 2012, Sacco reported income

of $50,000 and paid dividends of $20,000 while in 2013 it reported income of $75,000

and dividends of $30,000. Assume Dawson has the ability to significantly influence the

operations of Sacco.

The amount allocated to goodwill at January 1, 2012, is

A) $25,000.

B) $13,000

C) $ 9,000.

D) $16,000.

E) $10,000.

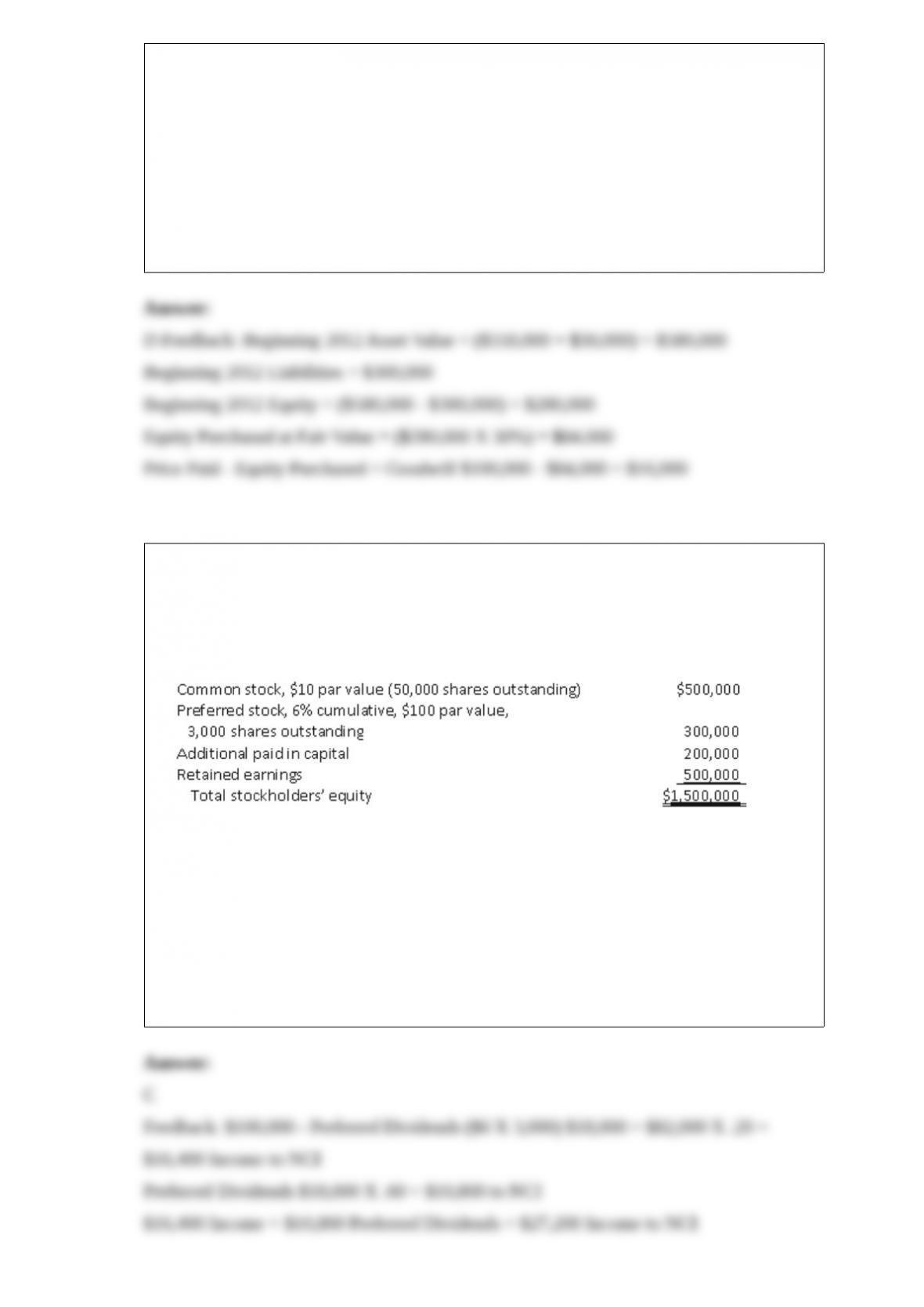

4) On January 1, 2013, Nichols Company acquired 80% of Smith Company’s common

stock and 40% of its non-voting, cumulative preferred stock. The consideration

transferred by Nichols was $1,200,000 for the common and $124,000 for the preferred.

Any excess acquisition-date fair value over book value is considered goodwill. The

capital structure of Smith immediately prior to the acquisition is:

If Smith’s net income is $100,000 in the year following the acquisition,

A) the portion allocated to the common stock (residual amount) is $92,800.

B) $10,800 preferred stock dividend will be subtracted from net income attributed to

common stock in arriving at non-controlling interest in subsidiary income.

C) the non-controlling interest balance will be $27,200.

D) the preferred stock dividend will be ignored in non-controlling interest in subsidiary

net income because Nichols owns the non-controlling interest of preferred stock.

E) the non-controlling interest in subsidiary net income is $30,800.

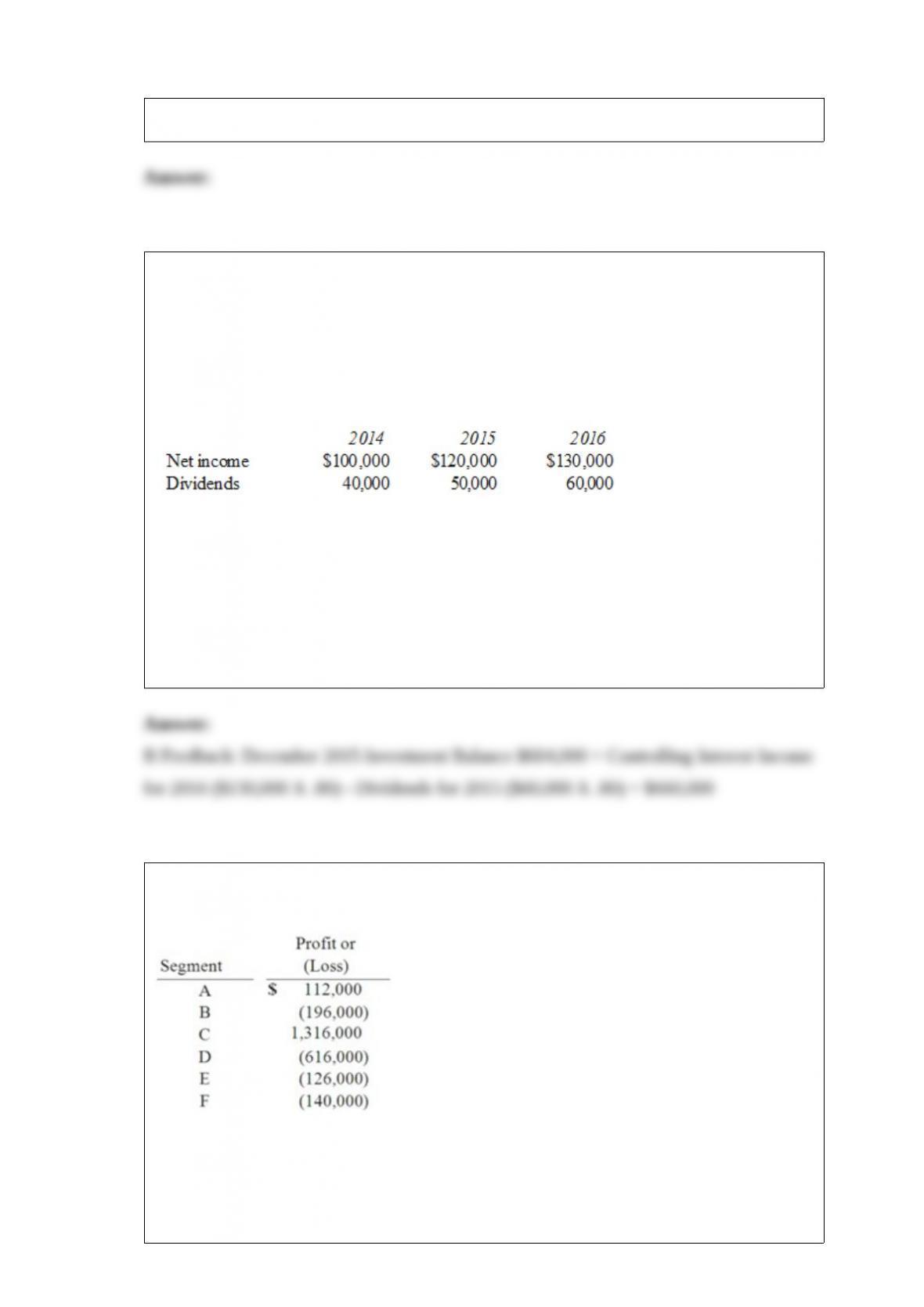

6) Pell Company acquires 80% of Demers Company for $500,000 on January 1, 2014.

Demers reported common stock of $300,000 and retained earnings of $210,000 on that

date. Equipment was undervalued by $30,000 and buildings were undervalued by

$40,000, each having a 10-year remaining life. Any excess consideration transferred

over fair value was attributed to goodwill with an indefinite life. Based on an annual

review, goodwill has not been impaired.

Demers earns income and pays dividends as follows:

Assume the PARTIAL EQUITY method is applied.

Compute Pell’s investment in Demers at December 31, 2016.

A) $780,000.

B) $660,000.

C) $785,000.

D) $676,000.

E) $620,000.

7) Kurves Corp. had six different operating segments reporting the following operating

profit and loss figures:

Which one of the following statements is true?

A.Segment A is a reportable segment based on this test.

B.Segment B is not a reportable segment based on this test.

C.Segment E is a reportable segment based on this test.

D.Segment C is not a reportable segment based on this test.

E.Segment D is a reportable segment based on this test.

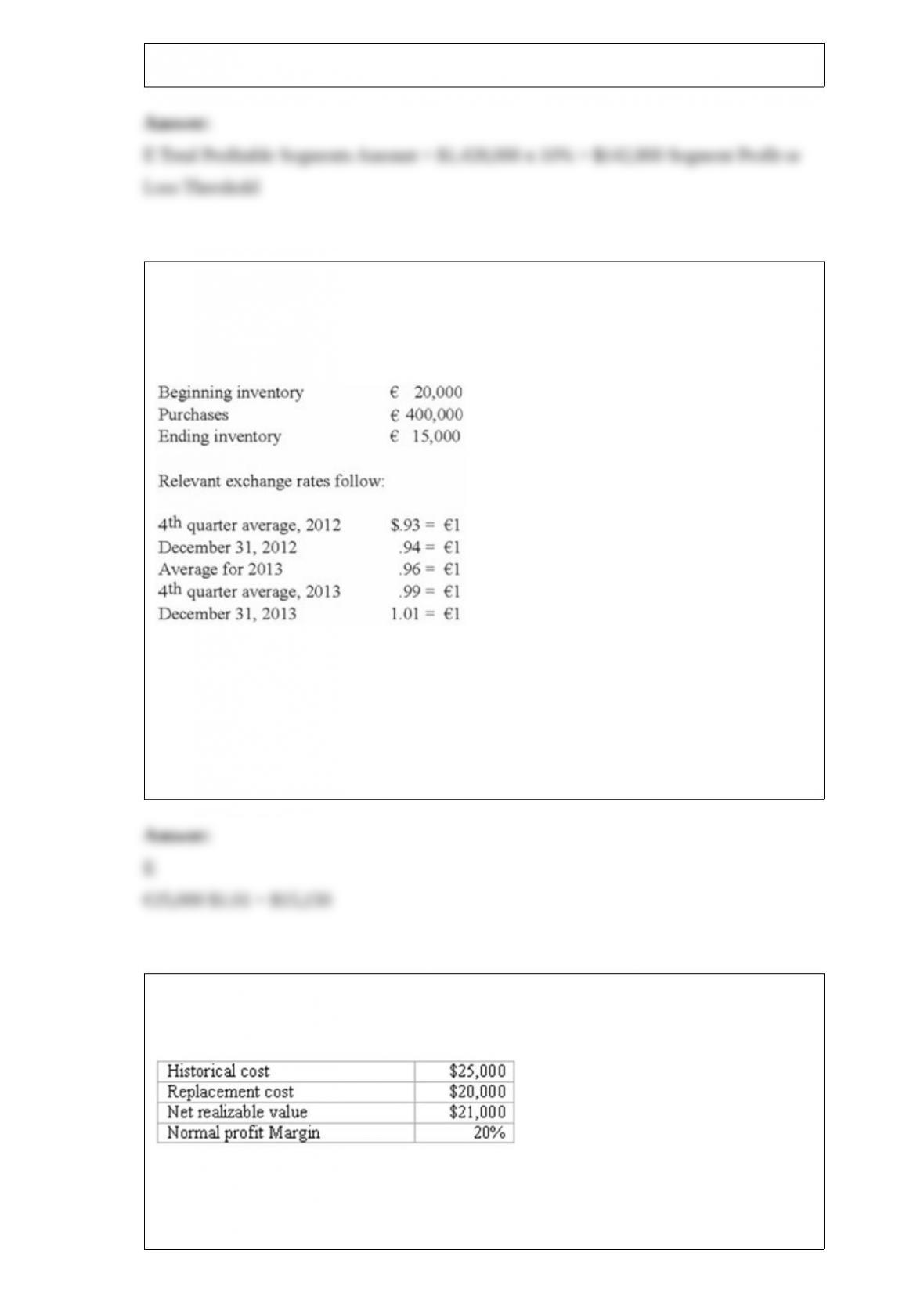

8) Esposito is an Italian subsidiary of a U.S. company.

Esposito’s ending inventory is valued at the average cost for the last quarter of the year.

The following account balances are available for Esposito for 2013:

Compute ending inventory for 2013 under the current rate method.

A.$13,950

B.$14,100

C.$14,400

D.$14,850

E.$15,150

9) The following information pertains to inventory held by a company at December 31,

2013.

What amount of inventory should be reported under IFRS?

A.$25,000

B.$21,000

C.$20,000

D.$4,000

E.$5,000

10) Femur Co. acquired 70% of the voting common stock of Harbor Corp. on January

1, 2014. During 2014, Harbor had revenues of $2,500,000 and expenses of $2,000,000.

The amortization of excess cost allocations totaled $60,000 in 2014. The

non-controlling interest’s share of the earnings of Harbor Corp. is calculated to be

A) $132,000.

B) $150,000.

C) $168,000.

D) $160,000.

E) $0.

11) Acker Inc. bought 40% of Howell Co. on January 1, 2012 for $576,000. The equity

method of accounting was used. The book value and fair value of the net assets of

Howell on that date were $1,440,000. Acker began supplying inventory to Howell as

follows:

Howell reported net income of $100,000 in 2012 and $120,000 in 2013 while paying

$40,000 in dividends each year.

What is the amount of unrealized intra-entity inventory profit to be deferred on

December 31, 2012?

A) $ 1,600.

B) $ 4,000.

C) $ 8,000.

D) $15,000.

E) $20,000.

12) Strickland Company sells inventory to its parent, Carter Company, at a profit during

2012. One-third of the inventory is sold by Carter in 2012.

In the consolidation worksheet for 2012, which of the following choices would be a

credit entry to eliminate the intra-entity transfer of inventory?

A) Retained earnings.

B) Cost of goods sold.

C) Inventory.

D) Investment in Strickland Company.

E) Sales.

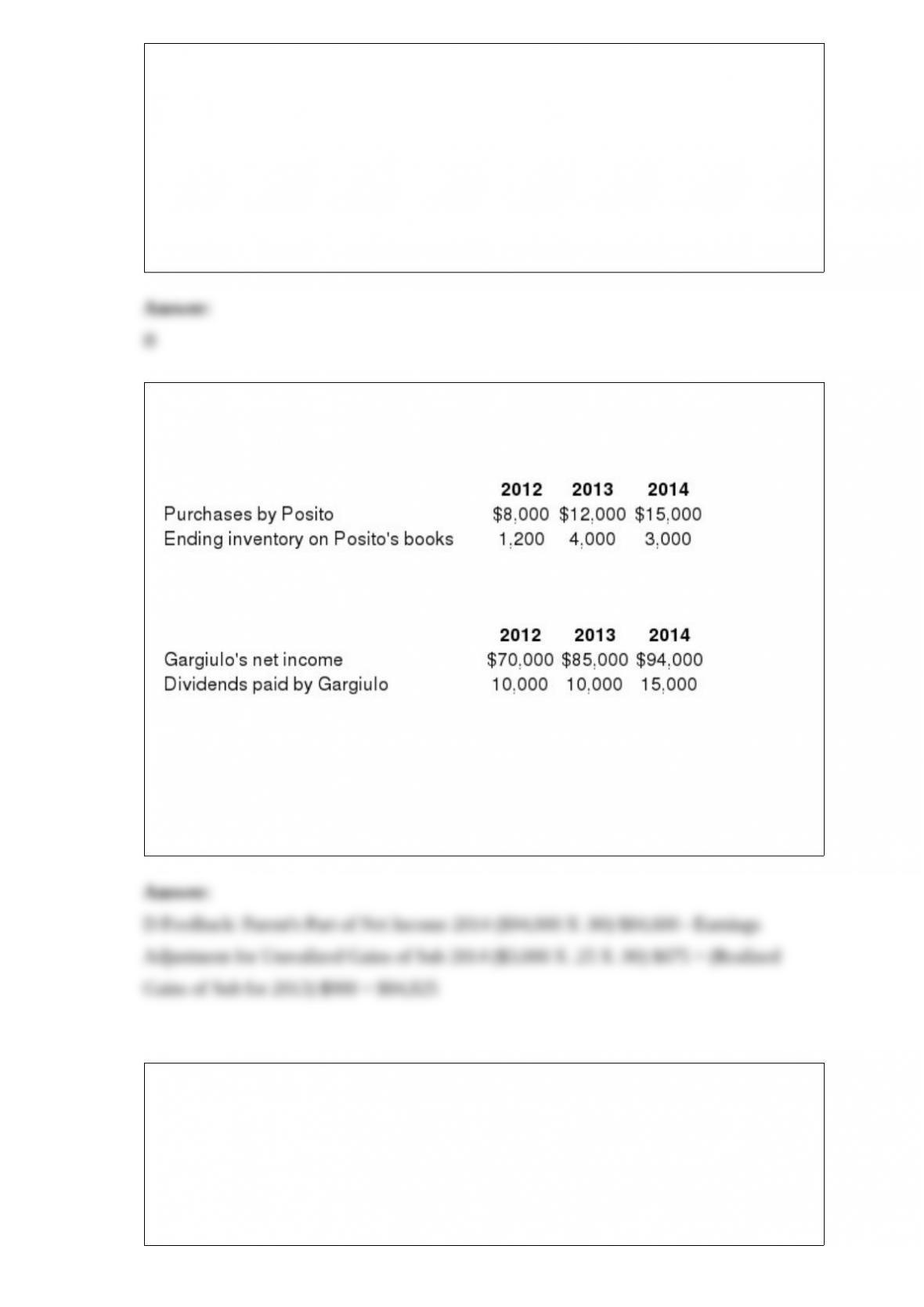

13) Gargiulo Company, a 90% owned subsidiary of Posito Corporation, sells inventory

to Posito at a 25% profit on selling price. The following data are available pertaining to

intra-entity purchases. Gargiulo was acquired on January 1, 2012.

Assume the equity method is used. The following data are available pertaining to

Gargiulo’s income and dividends.

Compute the equity in earnings of Gargiulo reported on Posito’s books for 2014.

A) $84,600.

B) $84,375.

C) $83,925.

D) $84,825.

E) $84,850.

14) Hoyt Corporation agreed to the following terms in order to acquire the net assets of

Brown Company on January 1, 2013:

(1) To issue 400 shares of common stock ($10 par) with a fair value of $45 per share.

(2) To assume Brown’s liabilities which have a fair value of $1,500.

On the date of acquisition, the consideration transferred for Hoyt’s acquisition of Brown

would be

A) $18,000.

B) $16,500.

C) $20,000.

D) $18,500.

E) $19,500.

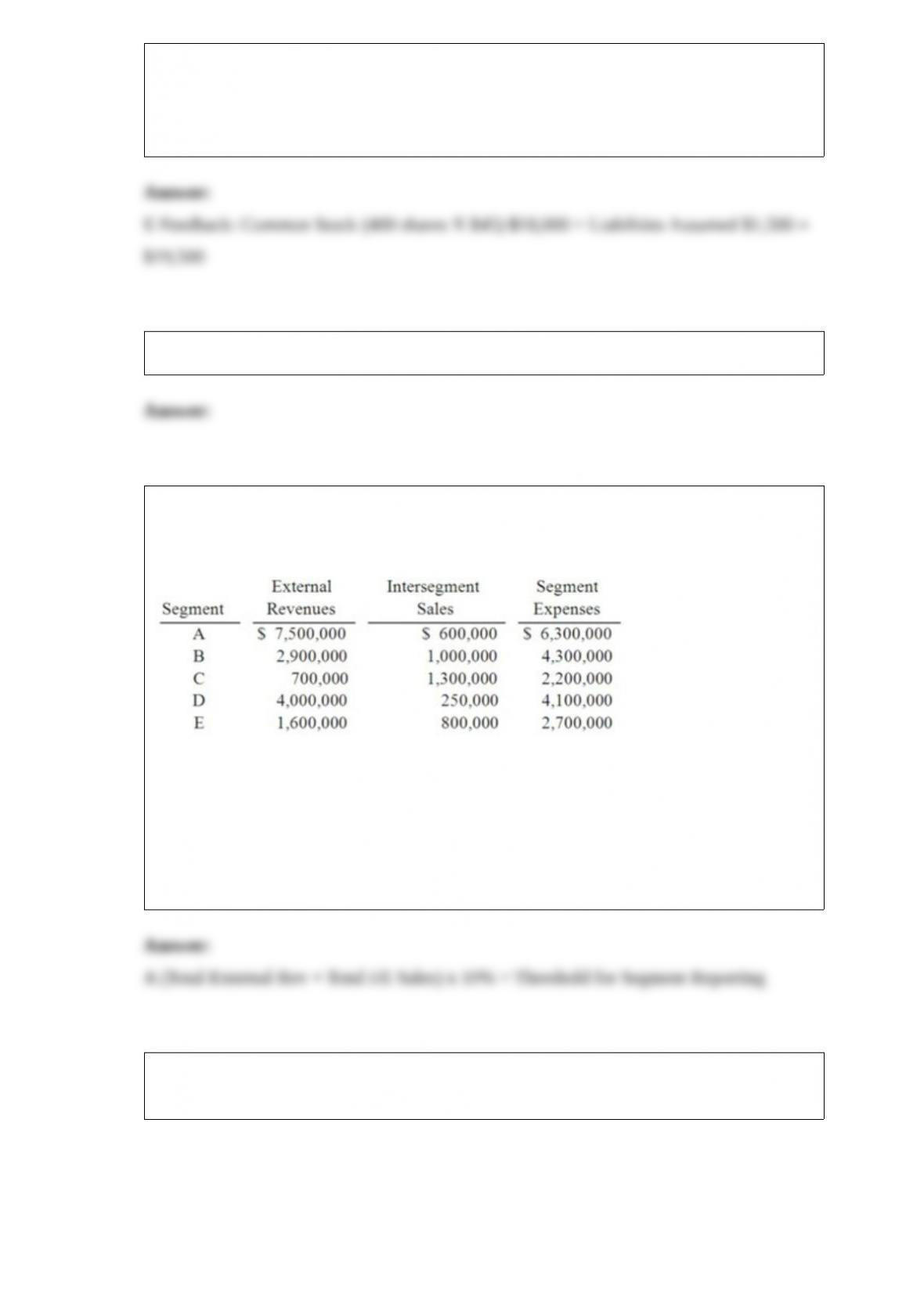

16) Natarajan, Inc. had the following operating segments, with the indicated amounts of

segment revenues and segment expenses:

According to the revenue test, which segments would require disaggregation?

A.A, B, D, and E.

B.A and B.

C.B and C.

D.A, B, and D.

E.C, D, and E.

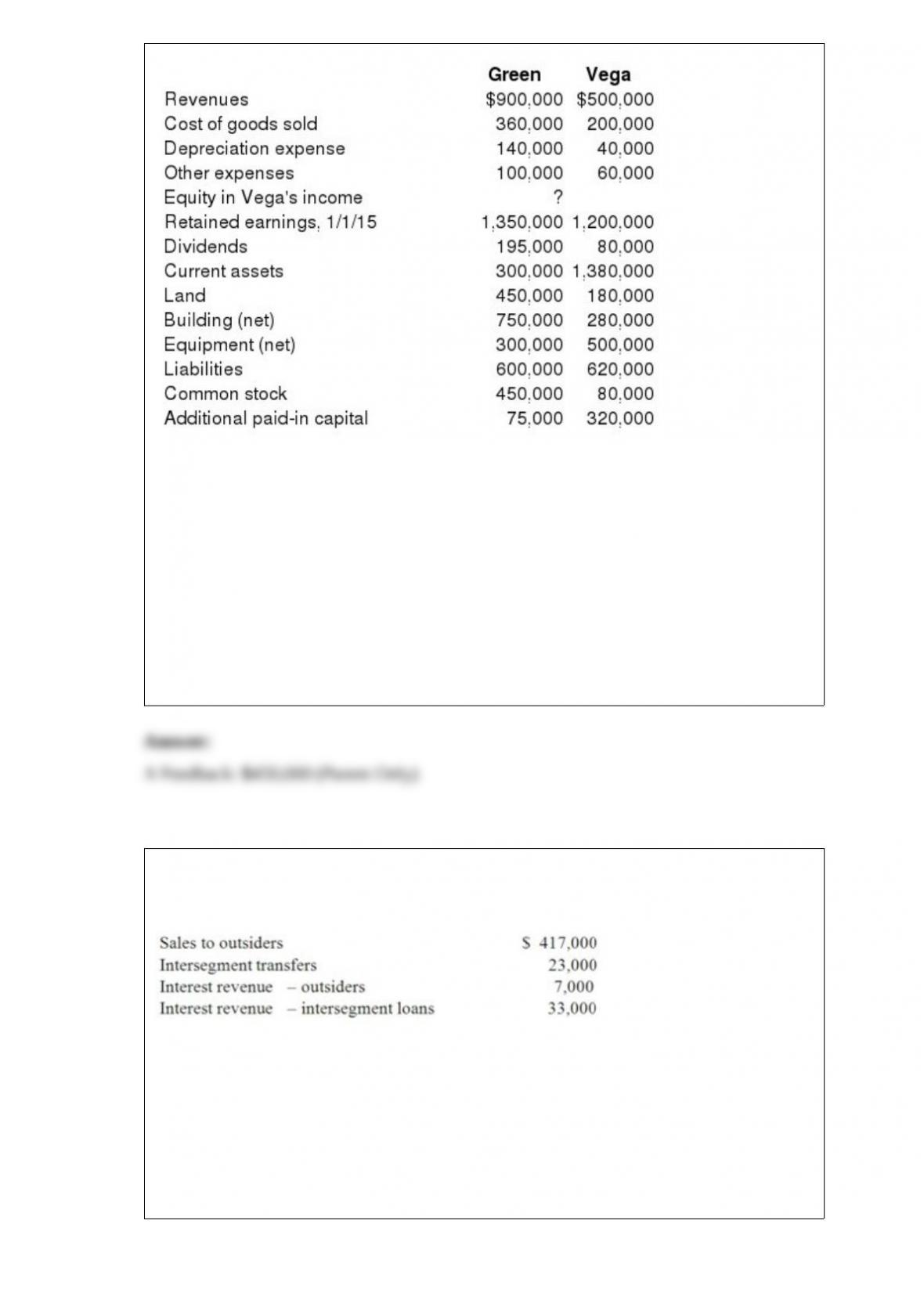

17) Following are selected accounts for Green Corporation and Vega Company as of

December 31, 2015. Several of Green’s accounts have been omitted.

Green acquired 100% of Vega on January 1, 2011, by issuing 10,500 shares of its $10

par value common stock with a fair value of $95 per share. On January 1, 2011, Vega’s

land was undervalued by $40,000, its buildings were overvalued by $30,000, and

equipment was undervalued by $80,000. The buildings have a 20-year life and the

equipment has a 10-year life. $50,000 was attributed to an unrecorded trademark with a

16-year remaining life. There was no goodwill associated with this investment.Compute

the December 31, 2015, consolidated common stock. A) $450,000.

B) $530,000.

C) $555,000.

D) $635,000.

E) $525,000.

18) The hardware operating segment of Bloom Corporation has the following revenues

for the year ended December 31, 2013:

For purposes of the revenue test, what amount will be used as total revenues of the

hardware operating segment?

A.$417,000

B.$440,000

C.$424,000

D.$460,000

E.$480,000

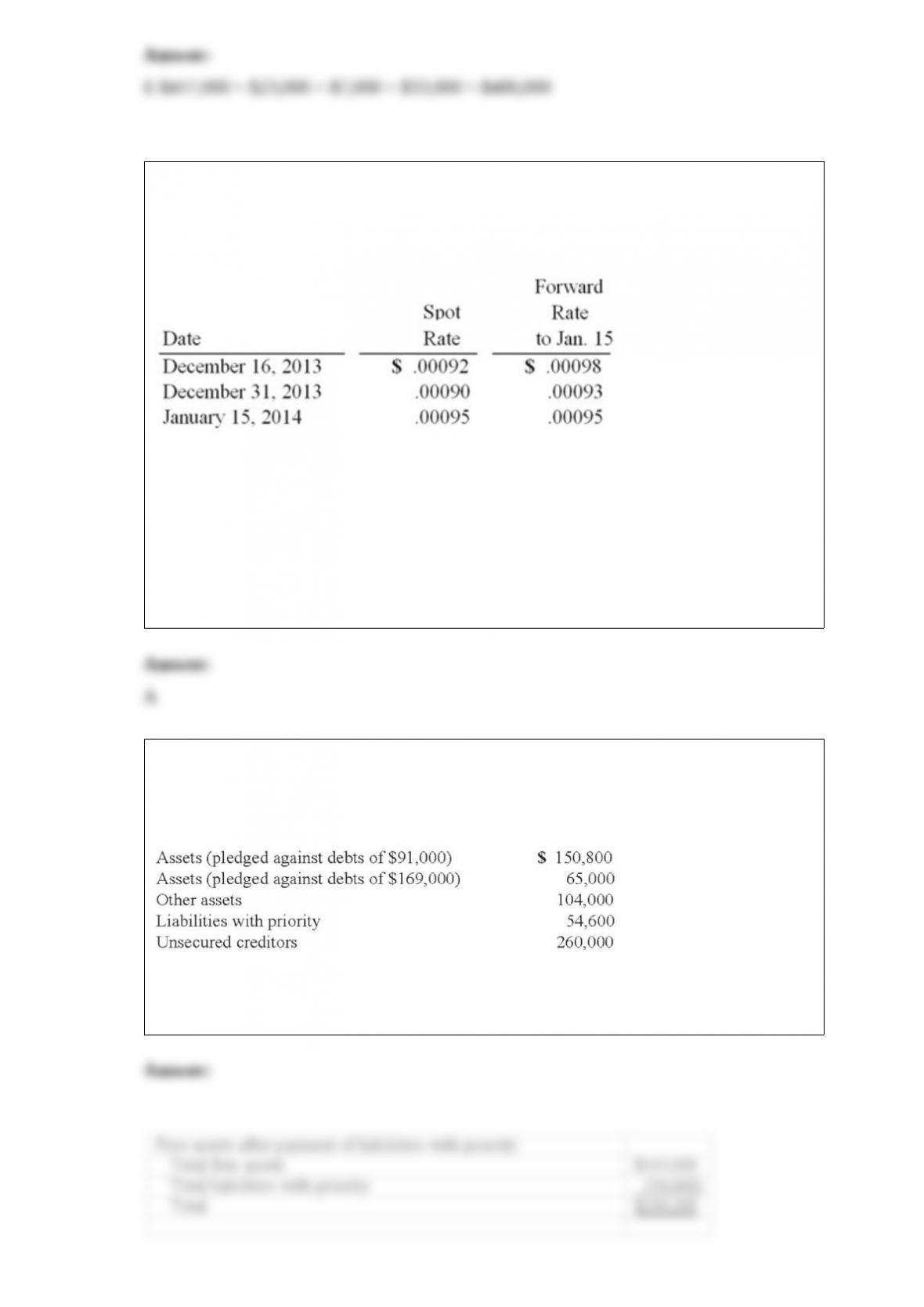

19) Car Corp. (a U.S.-based company) sold parts to a Korean customer on December

16, 2013, with payment of 10 million Korean won to be received on January 15, 20 The

following exchange rates applied:

Assuming a forward contract was entered into, how would the forward contract be

reflected on Car’s December 31, 2013 balance sheet?

A.Forward contract (asset).

B.Forward contract (liability).

C.Foreign currency (asset).

D.Foreign currency (liability).

E.Foreign exchange (liability).

20) Bazley Co. had severe financial difficulties and was considering the possibility of

filing a bankruptcy petition. At that time, the company had the following assets (stated

at net realizable value) and liabilities.

Assets that are available for unsecured creditors after payment of liabilities with priority

are calculated to be what amount?

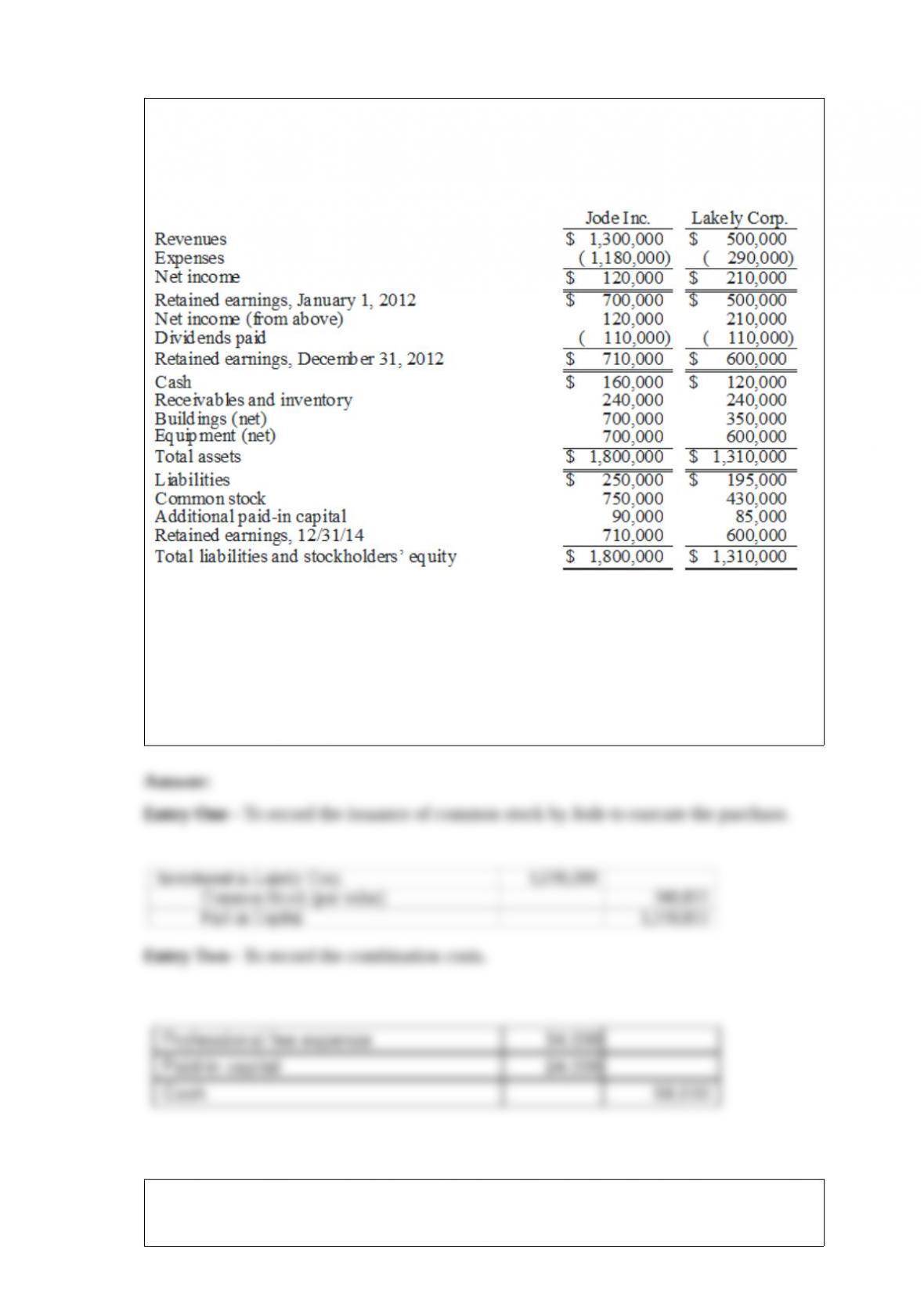

21) The financial statements for Jode Inc. and Lakely Corp., just prior to their

combination, for the year ending December 31, 2012, follow. Lakely’s buildings were

undervalued on its financial records by $60,000.

On December 31, 2012, Jode issued 54,000 new shares of its $10 par value stock in

exchange for all the outstanding shares of Lakely. Jode’s shares had a fair value on that

date of $35 per share. Jode paid $34,000 to an investment bank for assisting in the

arrangements. Jode also paid $24,000 in stock issuance costs to effect the acquisition of

Lakely. Lakely will retain its incorporation. Prepare the journal entries to record (1) the

issuance of stock by Jode and (2) the payment of the combination costs.

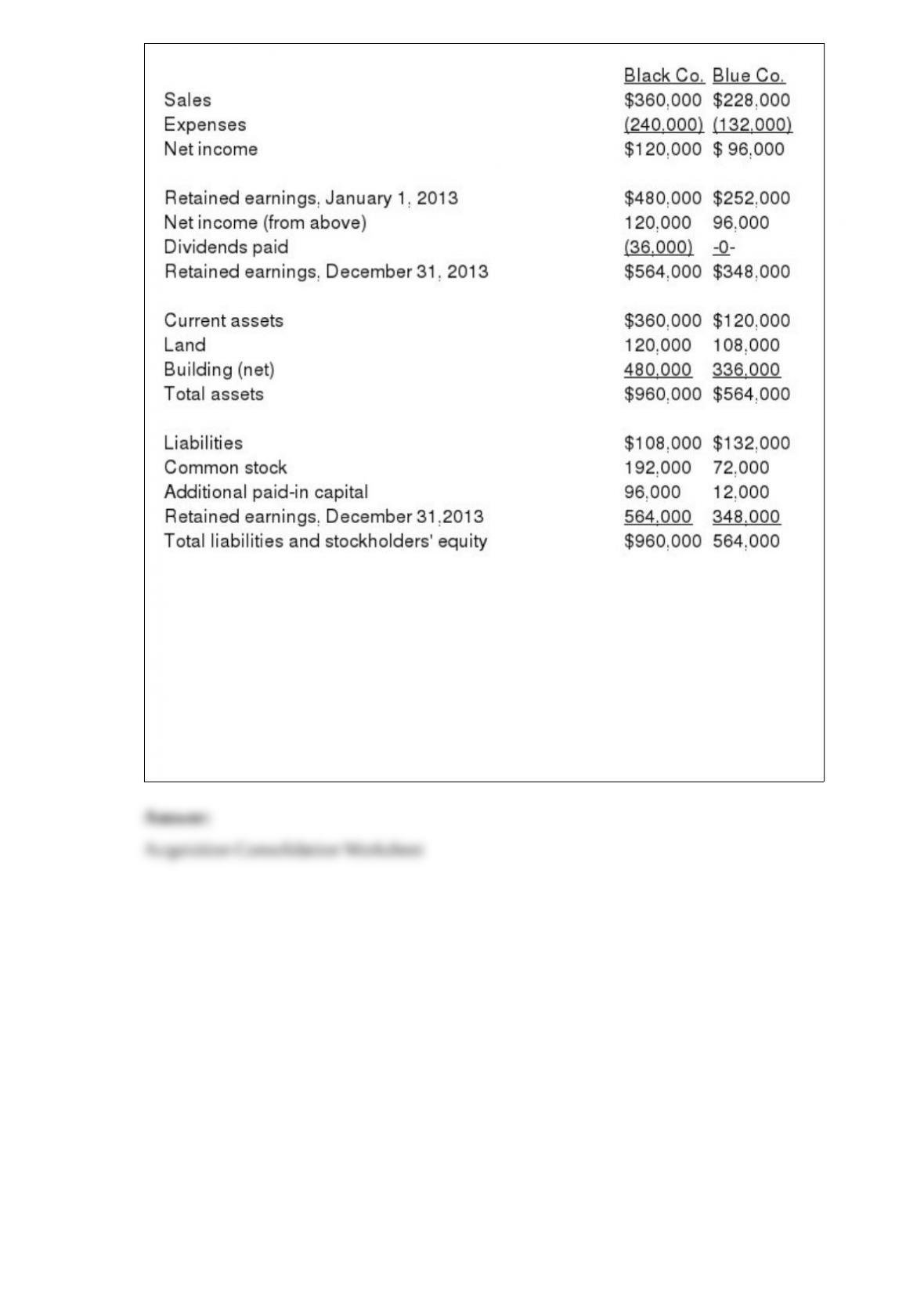

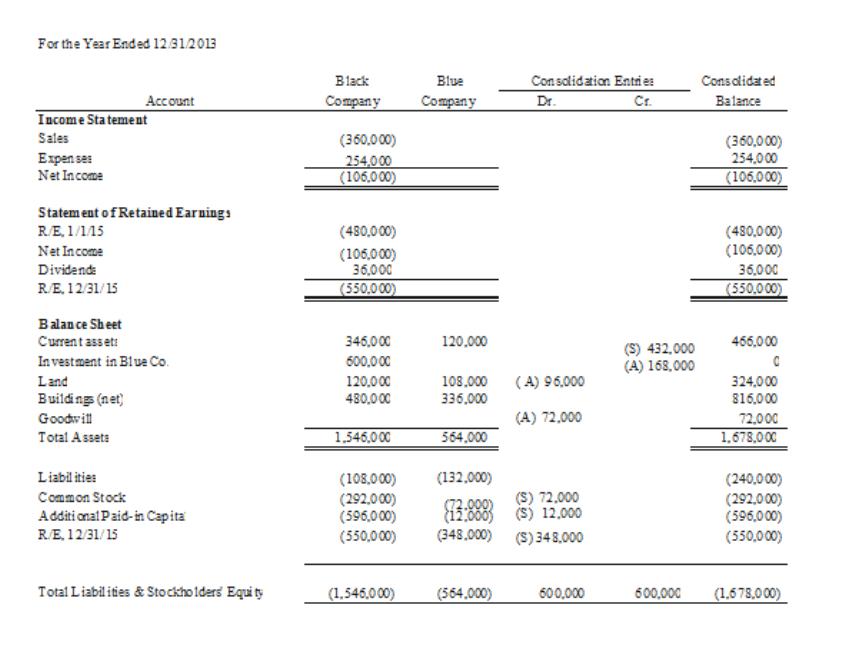

22) The following are preliminary financial statements for Black Co. and Blue Co. for

the year ending December 31, 2013 prior to Black’s acquisition of Blue.

On December 31, 2013 (subsequent to the preceding statements), Black exchanged

10,000 shares of its $10 par value common stock for all of the outstanding shares of

Blue. Black’s stock on that date has a fair value of $60 per share. Black was willing to

issue 10,000 shares of stock because Blue’s land was appraised at $204,000. Black also

paid $14,000 to several attorneys and accountants who assisted in creating this

combination. Required:

Assuming that these two companies retained their separate legal identities, prepare a

consolidation worksheet as of December 31, 2013 after the acquisition transaction is

completed.

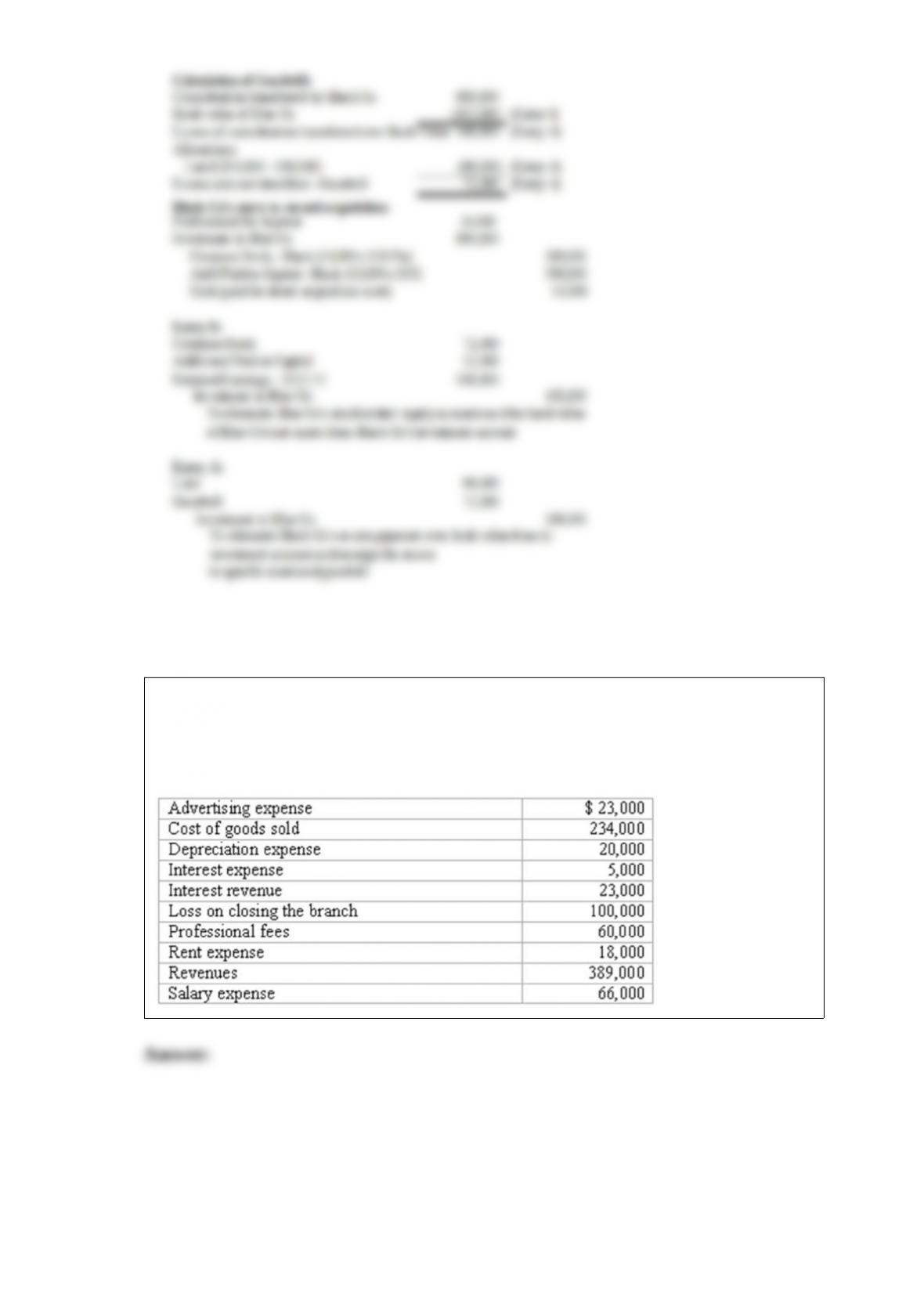

23) Berry Company is going through Chapter 11 bankruptcy reorganization. Prepare the

income statement for the calendar year 2013 using the following information. The

effective tax rate is 20%.

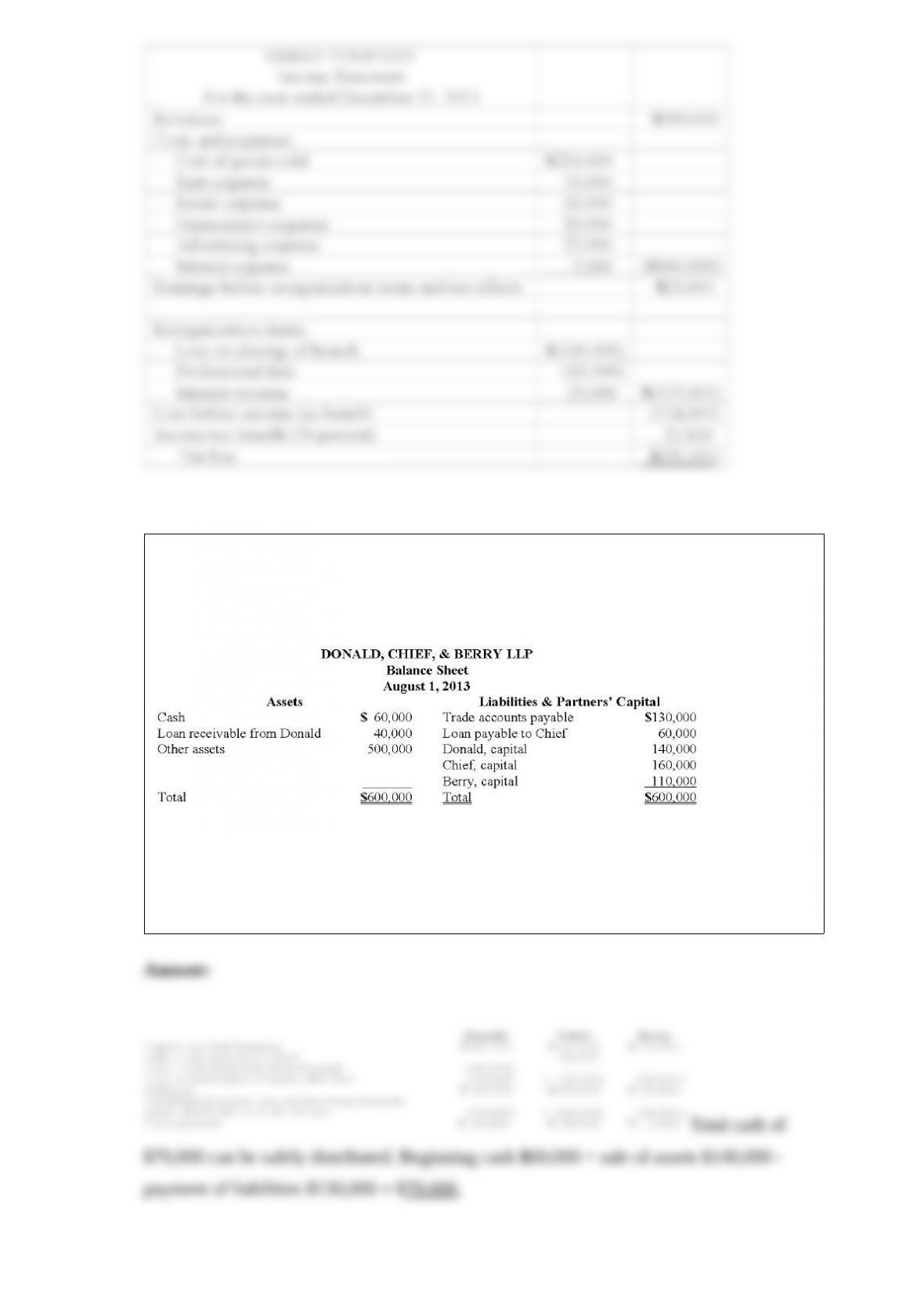

24) The partners of Donald, Chief & Berry LLP decided to liquidate on August 1, 2013.

The balance sheet of the partnership is as follows, with the profit and loss ratio of 25%,

45%, and 30%, respectively.

The disposal of Other Assets with a carrying amount of $200,000 realized $140,000,

and all available cash was distributed.

Prepare the schedule to compute the cash payments to the partners.

25) Jull Corp. owned 80% of Solaver Co. Solaver paid $250,000 for 10% of Jull’s

common stock. In 2013, Jull and Solaver reported operating income (not including

income from the investment) of $300,000 and $80,000, respectively. Jull and Solaver

paid dividends of $120,000 and $50,000, respectively.

Under the treasury stock approach, what is Jull’s controlling interest in Solaver Co.’s net

income?

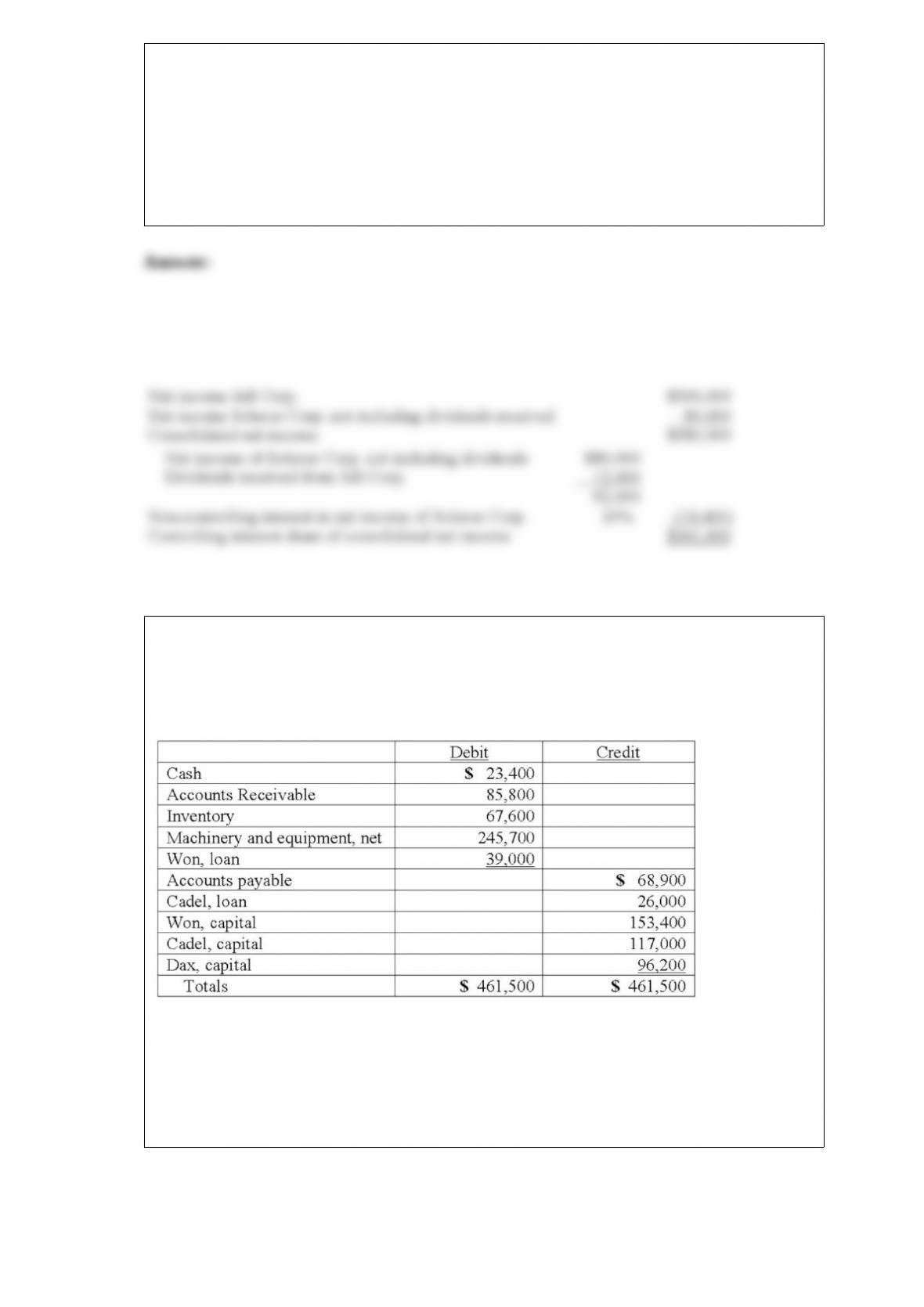

26) On January 1, 2013, the partners of Won, Cadel, and Dax (who shared profits and

losses in the ratio of 5:3:2, respectively) decided to liquidate their partnership. The trial

balance at this date was as follows:

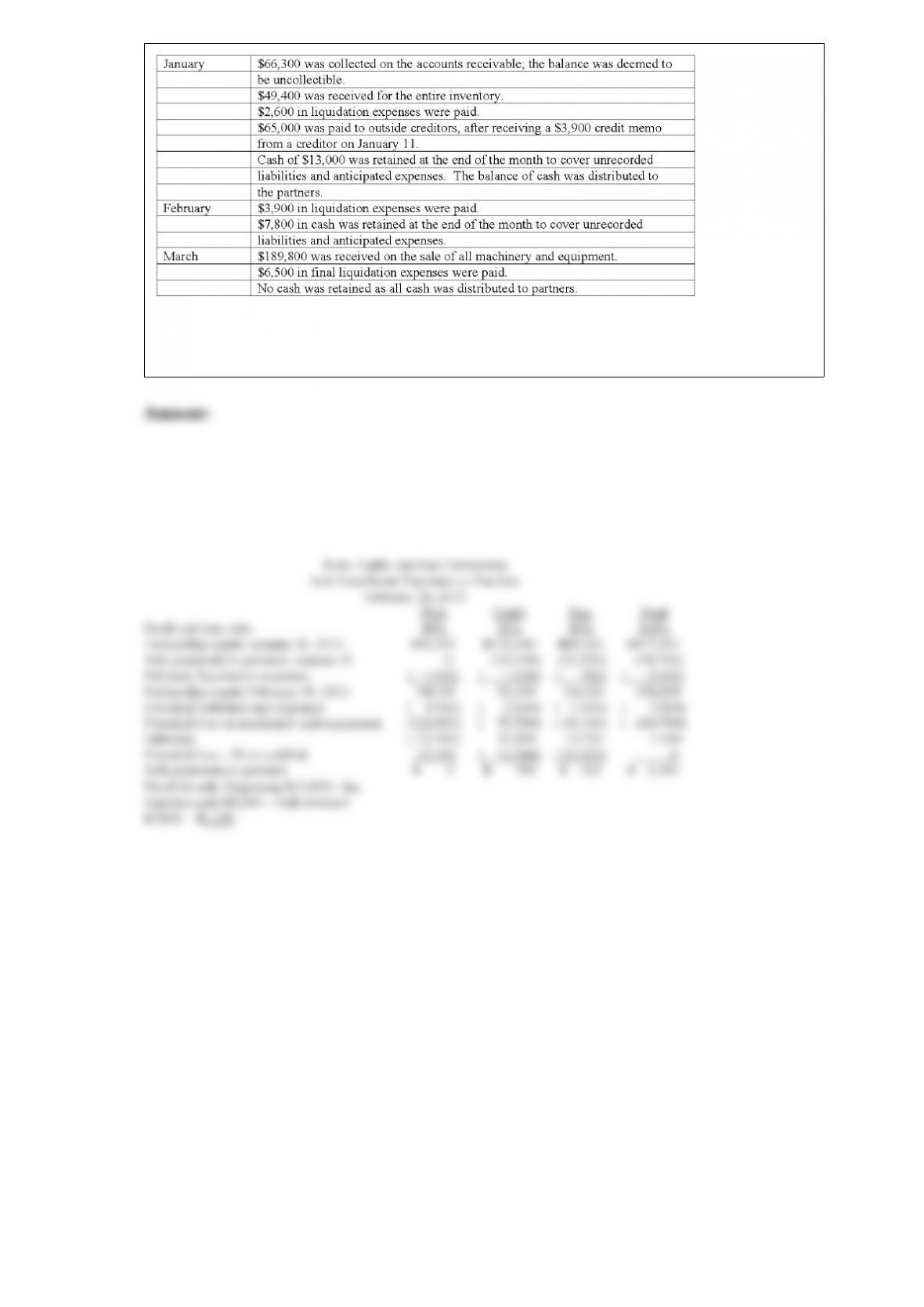

The partners planned a program of piecemeal conversion of the business assets to

minimize liquidation losses. All available cash, less an amount retained to provide for

future expenses, was to be distributed to the partners at the end of each month. A

summary of liquidation transactions follows:

Prepare a schedule to calculate the safe installment payments to be made to the partners

at the end of February.