Develop Your Skills

Research Case 1—Segment Reporting (60 minutes)

This assignment requires the student to select a company and find the note on

operating segments in that company’s annual report. The responses to this

assignment will depend upon the company selected by the student for analysis.

Research Case 2—Interim Reporting (60 minutes)

This assignment requires students to select a company, find the most recent

quarterly report for that company, and then determine whether the company

provides the minimum disclosure required as listed in the text. The responses

to this assignment will depend upon the company selected by the student for

analysis.

Research Case 3—Operating Segments (60 minutes)

This assignment requires students to find the note on operating segments in

each company’s annual report, determine three items of information (answer

three questions) from those notes, and prepare a written summary of their

findings. The primary objective of this requirement is to help students develop

their ability to present such findings in a written format. In answering these

questions, students will become familiar with the different formats and

terminology used by companies in providing operating segment information. The

answers to these questions will change depending upon the most recent annual

report available on the company’s website. The following general observations

indicate how these questions might be answered.

1. The two most important operating segments in terms of percentage of total

revenues.

The answer to this question is determined by calculating the ratio “segment

products/services.

2. The two operating segments with the largest growth in revenues.

This question is answered by calculating the ratio “(current year segment

3. The two most profitable operating segments in terms of profit margin.

This question is answered by calculating the ratio “segment profit/segment

revenues” for each segment of each company (again using revenues from

sales to external customers if separately reported). Segment profit goes

After reviewing the information provided by each of these companies in its

segment note, instructors might wish to add additional questions to this

assignment. For example, do these companies use generally accepted

accounting principles in preparing segment information? Does each company

provide a reconciliation to consolidated totals?

Research Case 4—Comparability of Geographic Area Information (60 minutes)

This assignment requires students to find the note on geographic areas in each

company’s annual report and then prepare a report describing the comparability

of this information. In preparing this assignment, students will see the different

formats used by companies in providing this information, and the different levels

assignment.

Geographic Areas Reported by Four Pharmaceutical Companies

Bristol-Myers Squibb Eli Lilly Merck Pfizer

U.S. U.S. U.S. U.S.

Europe Europe – –

– – E/ME/A –

– – – Developed Europe

Japan, Asia Pacific, and

Canada – – –

– Japan Japan –

Latin America, Middle East,

and Africa – – –

Emerging Markets – – Emerging Markets

– – – Developed Rest of World

Other Other Other –

The only geographic area that can be directly compared across these four

pharmaceutical companies is the United States. Bristol-Myers Squibb provides

somewhat more detailed information than the other companies. Only Eli Lilly and

Merck report an individual country (Japan) other than the U.S. Issues that could

geographic areas, focusing on developed vs. emerging markets.

Evaluation Case—Operating Segment Disclosures (60 minutes)

1. Two questions must be considered in evaluating CHIC’s operating segment

disclosures: (a) have reportable operating segments been appropriately

determined, e.g., is it appropriate to combine the Helicopters and Ships divisions

into one segment designated as Other, and (b) are the disclosures provided for

each segment in compliance with FASB ASC Topic 280, Segment Reporting?

With respect to question (a), ASC 280 allows (but does not require) segments to be

combined if they have essentially the same business activities in essentially the

same economic environments. In determining whether business activities and

environments are similar, management must consider these aggregation criteria:

5. If applicable, the nature of the regulatory environment.

Segments must be similar in each and every one of these areas to be combined.

The facts of this case indicate that the types of customers and method used to

distribute products differ across the four divisions, and each division must

comply with industry-specific regulations. Thus, the Helicopters and Ships

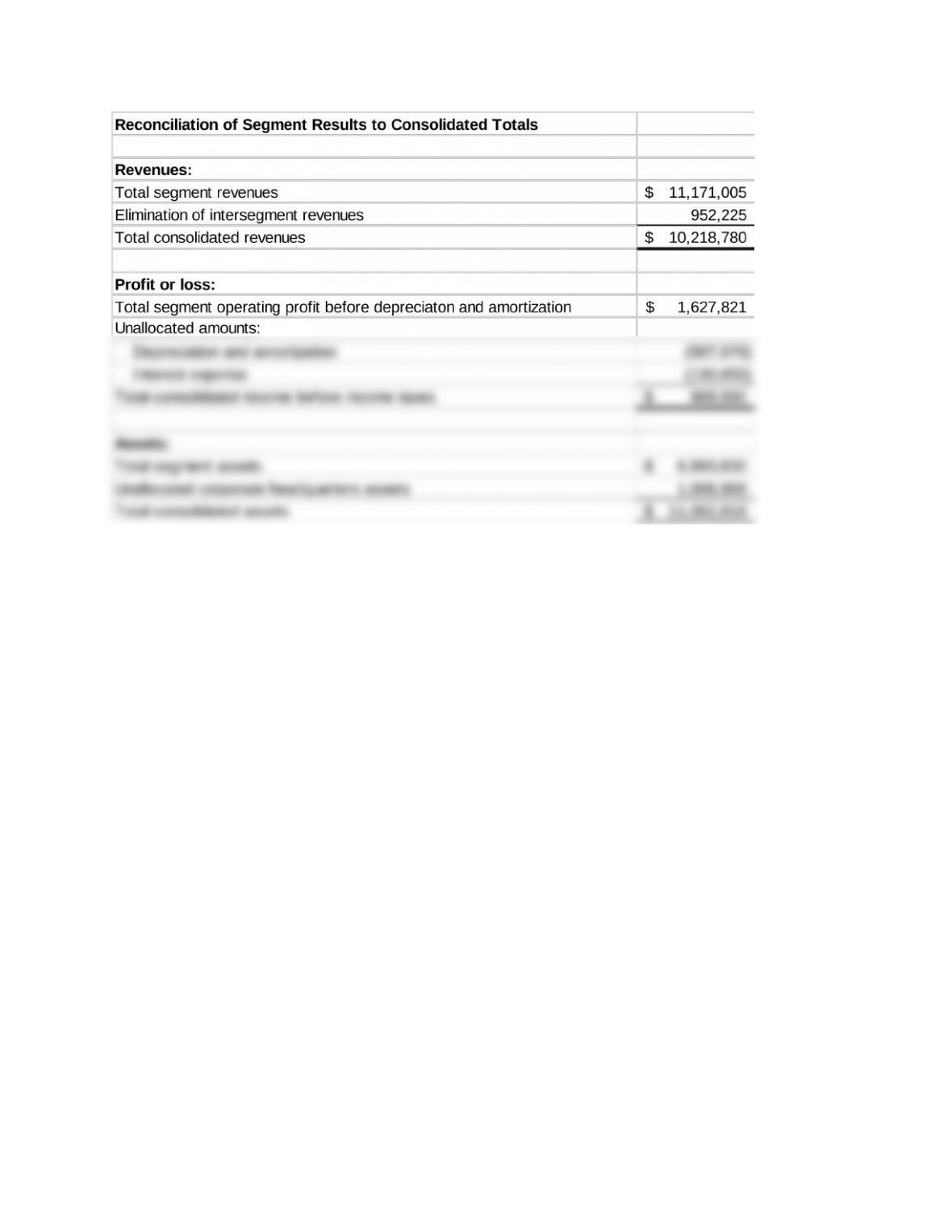

Revenue test: Total segment revenues are $11,171,005; thus, any segment with

more than $1,117,100 in sales is separately reportable.

Automobiles, Trucks, and Helicopters meet this threshold.

Profit (loss) test: Total segment profits of $ 1,686,700 ($881,292 + $456,530 +

$348,878) exceed total segment losses of $58,879, thus any segment with profit or

loss greater than $168,670 is separately reportable.

Automobiles, Trucks, and Helicopters meet this threshold.

with ASC 280.

With respect to question (b), Note X. Operating Segments prepared by CHIC’s

accountant fails to disclose information for the Helicopters and Ships segments

separately. Note X. also fails to separately disclose revenues from sales to

2. The disclosures required under ASC 280 could be provided in the following

manner:

Accounting Standards Case 1 —Segment Reporting (15 minutes)

Source of guidance: FASB ASC 280-10-55-2: Segment Reporting; Overall;

Implementation Guidance and Illustrations; Operating Segments – Equity

Method Investees

ASC 280-10-55-2 states “An equity method investee could be considered an

operating segment, if, under the specific facts and circumstances being

considered, it meets the definition of an operating segment, even though the

investor has no control over the performance of the investee.”

Thus, in response to the questions asked in the case:

Accounting Standards Case 2—Interim Reporting (15 minutes)

Source of guidance: FASB ASC 270-10-50-6: Interim Reporting; Overall;

Disclosure; Contingencies

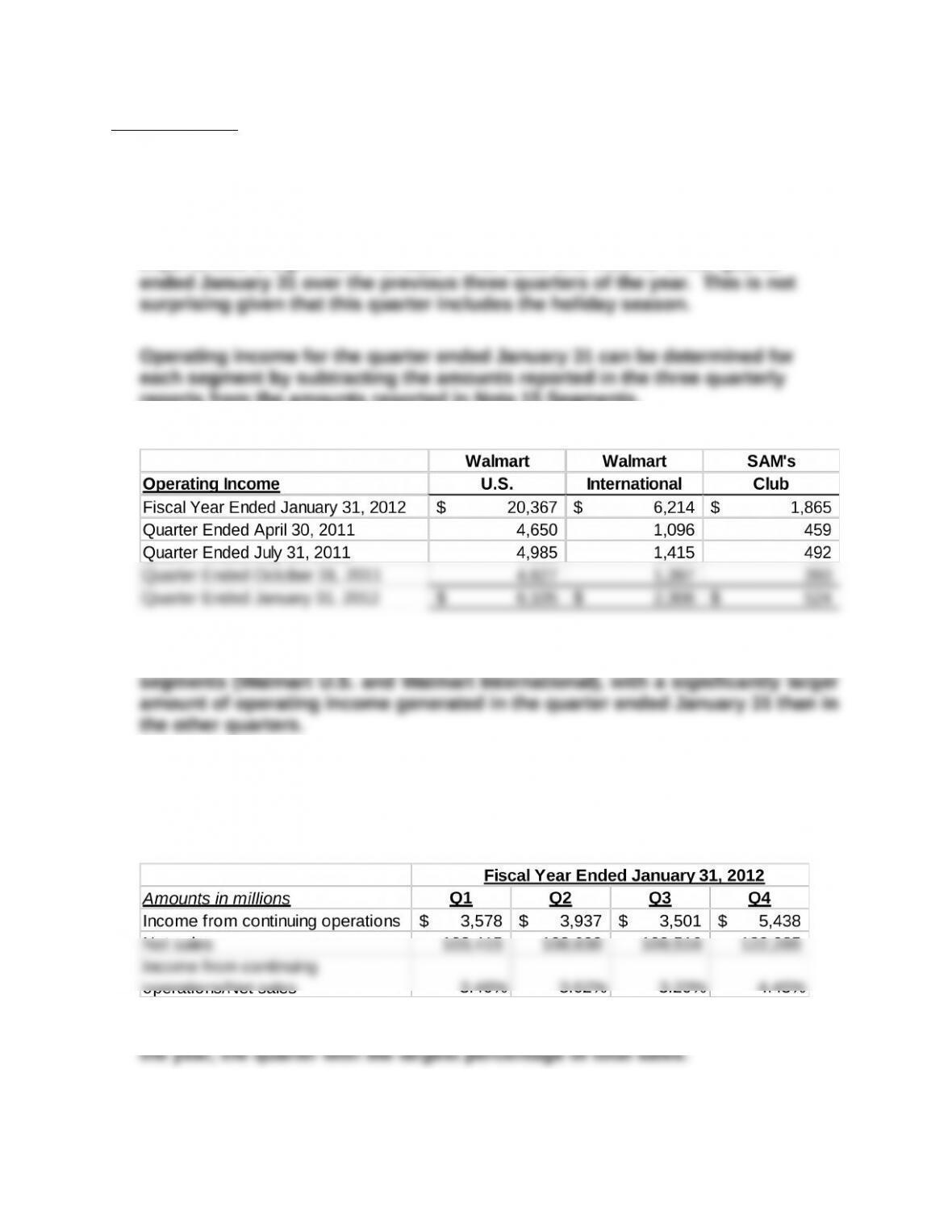

Analysis Case—Walmart Interim and Segment Reporting (60 minutes)

1. Assess the seasonal nature of Walmart’s sales and income for the company

as a whole and by operating segment.

The excerpt from Note 17 Quarterly Financial Data shows that Walmart

experienced a significant increase in net sales and income in the quarter

reports from the amounts reported in Note 15 Segments.

These results show the seasonal nature of the company’s two largest

2. Assess Walmart’s profitability by quarter and by segment.

Note 17 can be used to assess profitability in terms of profit margin (Income

from continuing operations/Net sales) by quarter.

These results indicate that profit margins are highest in the fourth quarter of

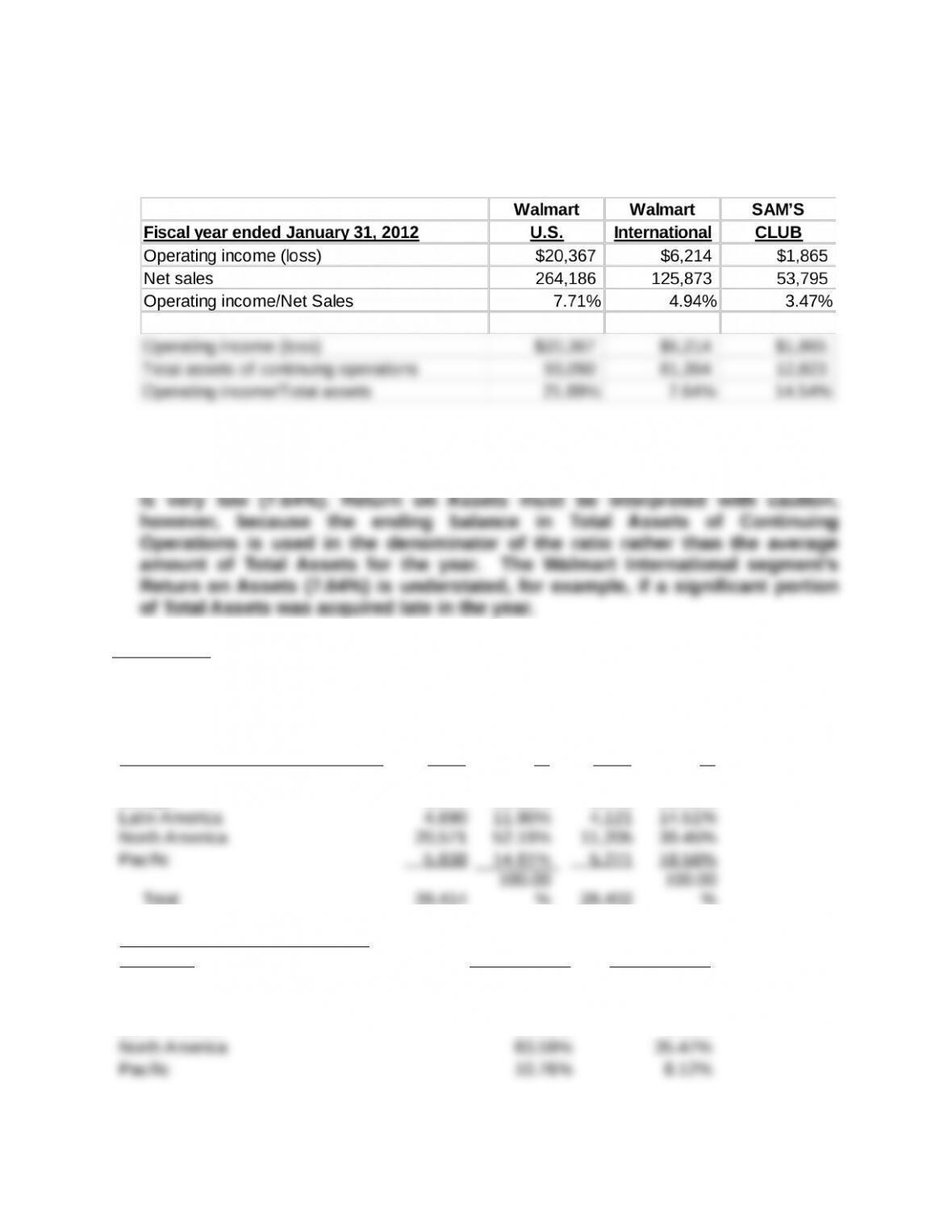

Note 15 can be used to assess profitability in terms of operating profit margin

(Operating income/Net sales) and return on assets (Operating income/Total

assets of continuing operations) by segment.

These results indicate that Walmart U.S. by far is the most profitable segment

for Walmart Stores, Inc. Although the Walmart International segment has a

reasonable Operating Profit Margin (4.94%), that segment’s Return on Assets

Excel Case—Coca-Cola Geographic Segment Information (60 minutes)

1. The ratios required to be calculated for the Coca-Cola Company are as

follows:

Percentage of total net revenues 2011 % 2010 %

Eurasia & Africa 2,841 7.21% 2,556 9.00%

Europe 5,474 13.89% 5,249 18.48%

Total 39,414

% 28,402

%

Percentage growth in total net

revenues 2010 to 2011 2009 to 2010

Eurasia & Africa 11.15% 16.34%

Europe 4.29% 0.88%

Latin America 13.81% 6.16%

Operating income as a percentage of

total net revenues (profit margin) 2011 2010

Eurasia & Africa 38.40% 38.34%

Europe 56.45% 56.70%

2. There is no right or wrong answer to this question. Students could argue that

Latin America and Europe would be the areas of the world in which to expand

because profit margin is highest in these areas. There would seem to be more

3. There is a great deal of non-accounting information that one would need to

determine a specific region of the world in which to focus expansion. For

example, one might need to gather information to answer the following

questions:

Is there a sufficiently large population with enough disposable income to

be able to purchase the company’s products?