36. (20 Minutes) (Consolidated balances three years after acquisition. Parent

has applied the equity method.)

a. Schedule 1—Acquisition-Date Fair Value Allocation and Amortization

Jasmine’s acquisition-date fair value $206,000

Excess fair value assigned to specific

accounts based on individual fair values Remaining Annual excess

life amortization

Equipment ………….………………. $54,400 8 yrs. $6,800

Buildings (overvalued) ........... (10 ,000) 20 yrs. (500)

Goodwill ………..……………..….… $21 ,600 indefinite -0 –

Total …..…………………………………. $6 ,300

Investment in Jasmine Company—12/31/15:

Jasmine’s acquisition-date fair value………………….….... $206,000

2013 Increase in book value of subsidiary …................ 40,000

36. (continued)

b. Equity in subsidiary earnings:

Income accrual………..…………………………………………….... $30,000

c. Consolidated net income:

Consolidated revenues (add book values) .…..….…...... $414,000

Consolidated expenses (add book values) ………………. (272,000)

d. Consolidated equipment:

Book values added together …………….……………………… $370,000

e. Consolidated buildings:

Book values added together …………….……………………… $288,000

f. Allocation of excess fair value to goodwill………….….... $21 ,600

g. Consolidated common stock…………….……………………… $290 ,000

The parent’s $290,000 balance appropriately shows the parent company

h. Consolidated retained earnings…………….………….…..…. $410 ,000

Tyler’s balance of $410,000 is equal to the consolidated total because

the equity method has been applied.

37. (35 minutes) (Consolidation with IPR&D, equity method)

a. Consideration transferred 1/1/14 $1,765,000

Increase in Salsa’s retained earnings to 1/1/15 150,000

37. (continued)

b. The IPR&D was abandoned in 2014 and the original asset was written off to

c. Picante and Subsidiary Salsa

Consolidated Worksheet

for the year ended December 31, 2015

12/31/15 12/31/15

Accounts Picante Salsa Adjustments Consolidated

Sales (3,500,000) (1,000,000) (4,500,000)

Cost of goods sold 1,600,000 630,000 2,230,000

Depreciation expense 540,000 160,000 (E) 7,000 707,000

Subsidiary income (203 ,000) (I) 203,000 – 0 –

Net Income (1 ,563,000) (210 ,000) (1 ,563,000)

Retained earnings 1/1/15 (3,000,000) (800,000) (S) 800,000 (3,000,000)

Inventory 900,000 580,000 1,480,000

Investment in Salsa 2,042,000 (D) 25,000 (S)1,800,000 -0-

(A) 64,000

(I) 203,000

Land 3,500,000 700,000 4,200,000

Common stock—Picante (5,150,000) (5,150,000)

Common stock—Salsa (1,000,000) (S)1,000,000

Retained earnings 12/31/15 (4 ,363,000) (985 ,000) (4 ,363,000)

(12 ,800,000) (3 ,185,000) 2 ,099,000 2 ,099,000 (14 ,000,000)

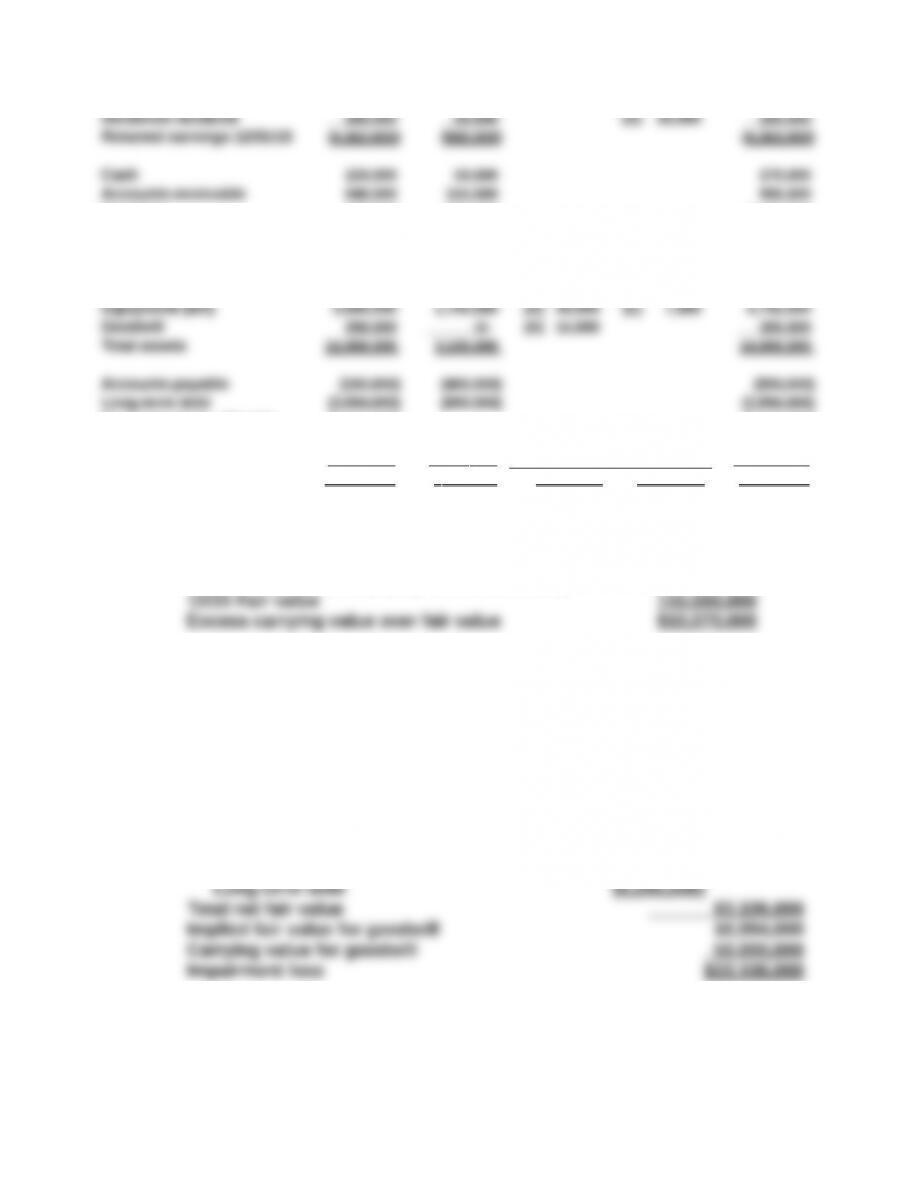

38. (55 minutes) (Goodwill impairment, consolidated balances, and worksheet)

a. Prine compares Lydia’s total fair value to its carrying value, as follows:

12/31 Carrying value (equity method balance) $120,070,000

Because fair value is less than carrying value, Prine is required to

further test whether goodwill is impaired.

b. 12/31 Fair value for Lydia $110,000,000

Fair values of assets and liabilities

Cash $109,000

Receivables (net) 897,000

Movie library 60,000,000

Broadcast licenses 20,000,000

Equipment 19,000,000

Current liabilities (650,000)

Journal Entry by Prine:

Goodwill impairment loss 33,106,000

Investment in Lydia Co. 33,106,000

c. Combined revenues $30,000,000

Combined expenses (including excess amortization) 22 ,200,000

Consolidated net loss $(25 ,306,000)

d. Consolidated goodwill = $50,000,000 – $33,106,000 = $16,894,000

e. Consolidated broadcast licenses = $350,000 + $14,014,000 = $14,364,000

The consolidated balance is the parent’s book value plus the fair value

of the subsidiary acquisition-date value adjusted for changes since

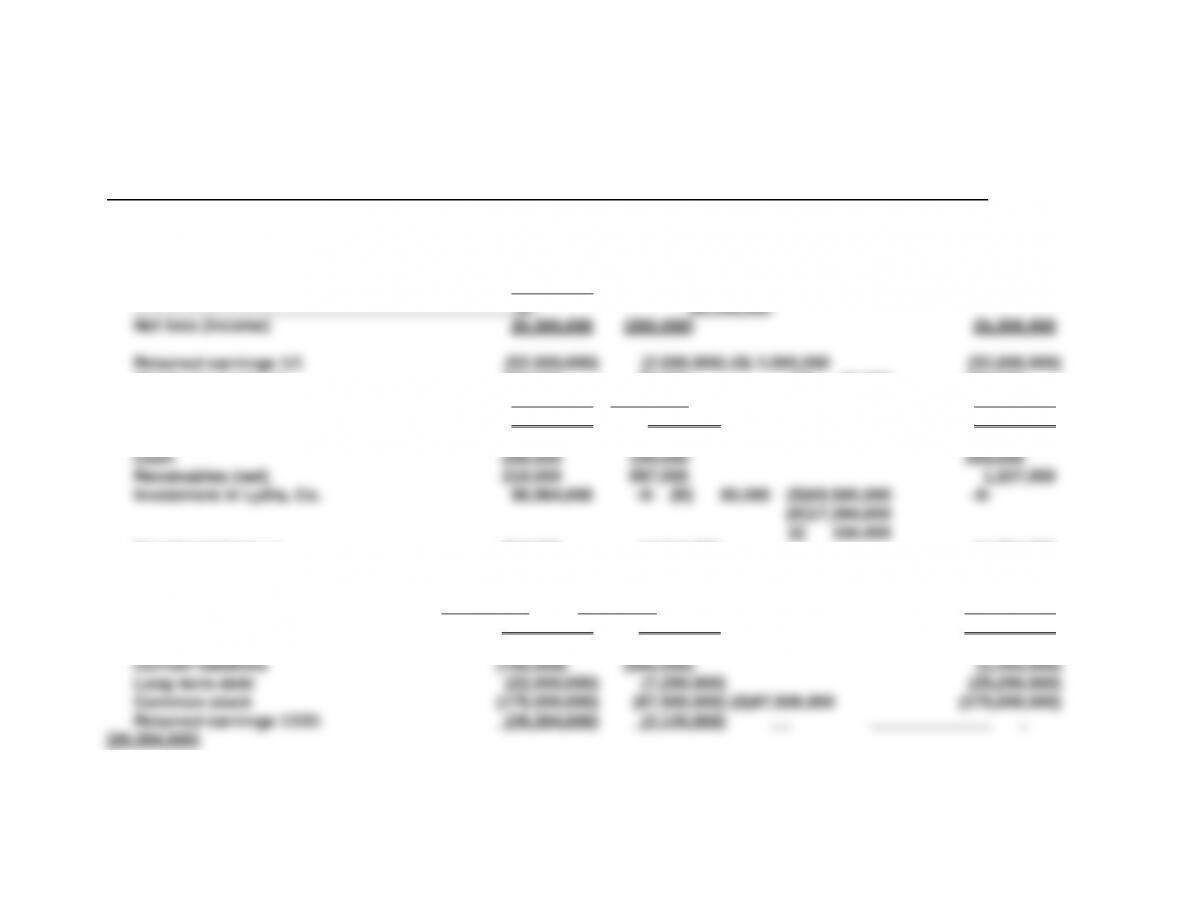

38. f. (continued) Prine and Lydia

Consolidated Worksheet

December 31

Adjusting Entries Consolidated

Accounts Prine, Inc. Lydia Co. Debit Credit Totals

Revenues (18,000,000) (12,000,000) (30,000,000)

Expenses 10,350,000 11,800,000(E) 50,000 22,200,000

Equity in Lydia earnings (150,000) -0- (I) 150,000 -0-

Impairment loss 33 ,106,000

-0 – 33,106,000

Dividends declared 300,000 80,000 (D) 80,000 300,000

Net loss (income) 25 ,306,000 (200 ,000) 25 ,306,000

Retained earnings 12/31 (26 ,394,000) (2 ,120,000) (26 ,394,000)

Broadcast licenses 350,000 14,014,000 14,364,000

Movie library 365,000 45,000,000 45,365,000

Equipment (net) 136,000,000 17,500,000(A) 500,000(E) 50,000 153,950,000

Goodwill -0- -0- (A)16,894,000 16 ,894,000

Total assets 224 ,149,000 77 ,520,000 232 ,049,000

Total liabilities and equity (224 ,149,000)(77,520,000)87,114,000 87 ,114,000

(232 ,049,000)

RESEARCH CASE SOLUTION

Jonas recognized several identifiable intangibles from its acquisition of

Innovation Plus. Jonas expresses the desire to expense these intangible assets

in the acquisition period.

1. Advise Jonas on the acceptability of its suggested immediate write-off.

2. Indicate the relevant factors to consider in allocating the values assigned to

identifiable intangibles acquired in a business combination.

The accounting for a recognized intangible asset is based on its useful life to

the reporting entity. An intangible asset with a finite useful life is amortized;

an intangible asset with an indefinite useful life is not amortized. The useful

life of an intangible asset to an entity is the period over which the asset is

expected to contribute directly or indirectly to the future cash flows of that

3. Jonas’ suggested treatment of goodwill is inappropriate. To ensure that

4. Per the FASB ASC (350-20-35-41):

For the purpose of testing goodwill for impairment, all goodwill acquired in a

business combination shall be assigned to one or more reporting units as of

the acquisition date. Goodwill shall be assigned to reporting units of the

MICROSOFT IMPAIRMENT ANALYSIS CASE SOLUTION

The following all can be found in Microsoft Corporation’s 2012 10-K annual report.

1. Microsoft’s OnOnline Services Division incurred a $6.193 billion goodwill

impairment loss assess on May 1, 2012

Online Services Division (“OSD”) develops and markets information and

content designed to help people simplify tasks and make more informed

2. Goodwill impairment appeared on the 2012 income statement and cash flow

statement as follows:

3. The impairment was the result of the OSD unit experiencing slower than

projected growth in search queries and search advertising revenue per query,

slower growth in display revenue, and changes in the timing and

implementation of certain initiatives designed to drive search and display

4. Microsoft’s Note 10 – Goodwill (page 64) states the following:

We tested goodwill for impairment as of May 1, 2012 at the reporting unit level

using a discounted cash flow methodology with a peer-based, risk-adjusted

weighted average cost of capital. We believe use of a discounted cash flow

approach is the most reliable indicator of the fair values of the businesses.

capital used to calculate the discounted cash flows of OSD in estimating the

fair value of the business. This business-specific risk factor reflects the

increased uncertainty in forecasting the future performance of OSD.

Because our annual test indicated that OSD’s carrying value exceeded its

estimated fair value, a second phase of the goodwill impairment test (“Step 2”)

was performed specific to OSD. Under Step 2, the fair value of all OSD assets

FASB ASC AND IASB RESEARCH CASE

1. GAAP prohibits reversal of impairment losses for goodwill. IFRS also

prohibits reversal of impairment losses for goodwill

2. Requirements for goodwill impairment differ under IFRS. Under IFRS, goodwill

impairment testing uses a one-step approach: The recoverable amount of the

CGU (cash-generating unit) or group of CGUs (i.e., the higher of its fair value

IAS 36 Impairment of Assets:

88. When, as described in paragraph 81, goodwill relates to a cash-generating

unit but has not been allocated to that unit, the unit shall be tested for

90. A cash-generating unit to which goodwill has been allocated shall be

tested for impairment annually, and whenever there is an indication that the

104. An impairment loss shall be recognised for a cash-generating unit (the

smallest group of cash-generating units to which goodwill or a corporate

asset has been allocated) if, and only if, the recoverable amount of the unit

(group of units) is less than the carrying amount of the unit (group of units).

The impairment loss shall be allocated to reduce the carrying amount of the

assets of the unit (group of units) in the following order:

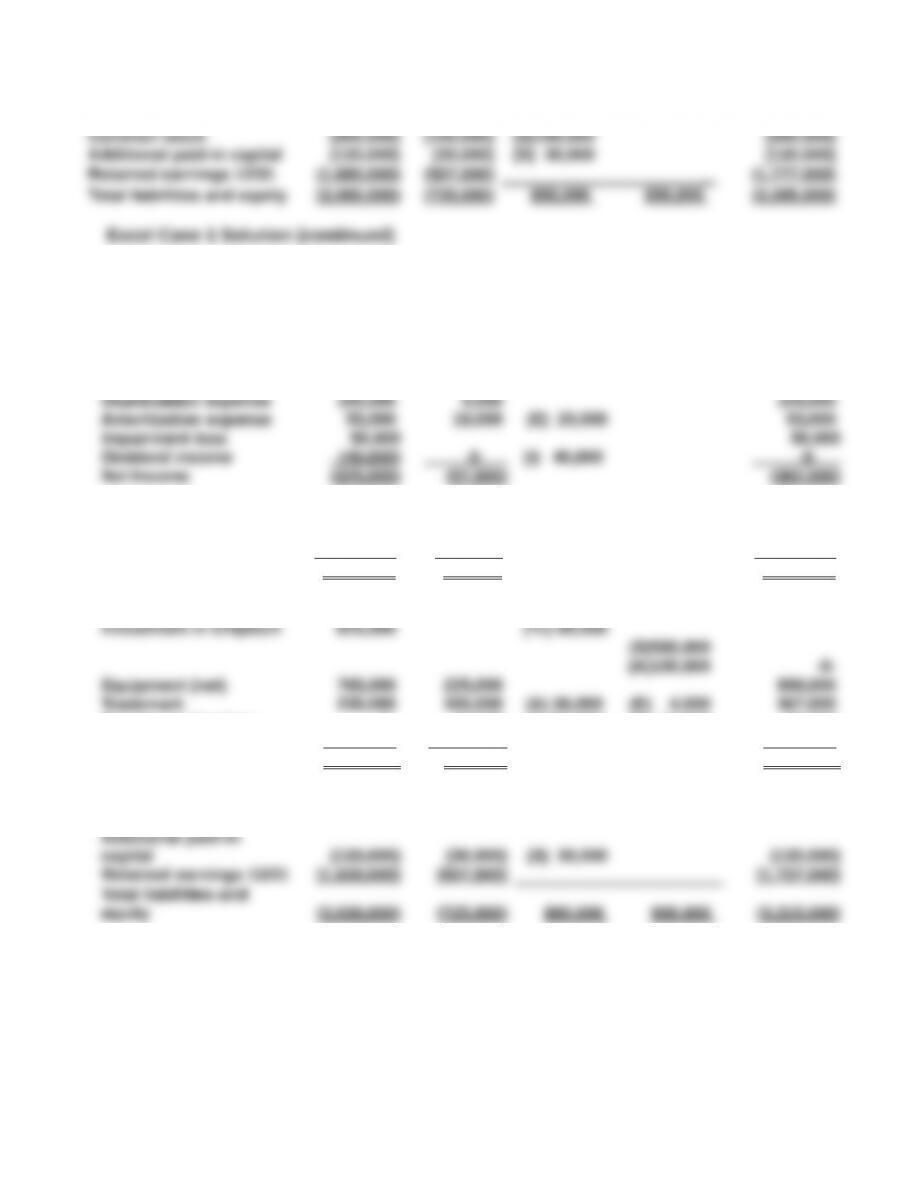

Excel Case 1 Solution

a. Innovus employs initial value method to account for ChipTech.

Innovus ChipTech Adjustments Consolidated

Net Income (375,000) (97,000) (412,000)

Retained earnings 1/1 (1,555,000) (450,000) (S)450,000 (*C) 60,000 (1,615,000)

Net income (375,000) (97,000) (412,000)

Dividends declared 250,000 40,000 (I) 40,000 250,000

Retained earnings 12/31 (1,680,000) (507,000) (1,777,000)

Trademark 235,000 100,000 (A) 36,000 (E) 4,000 367,000

Existing technology 0 45,000 (A) 64,000 (E) 16,000 93,000

Goodwill 450,000 -0- (A) 50,000 500,000

Total assets 3,080,000 725,000 3,265,000

Liabilities (780,000) (88,000) (868,000)

b. Innovus employs initial value method to account for ChipTech and goodwill is

impaired.

Innovus ChipTech Consolidated

Revenues (990,000) (210,000) (1,200,000)

Cost of good sold 500,000 90,000 590,000

Retained earnings 1/1 (1,555,000) (450,000) (S)450,000 (*C) 60,000 (1,615,000)

Net income (325,000) (97,000) (362,000)

Dividends declared 250,000 40,000 (I) 40,000 250,000

Retained earnings 12/31 (1,630,000) (507,000) (1,727,000)

Current assets 960,000 355,000 1,315,000

Existing technology -0- 45,000 (A )64,000 (E) 16,000 93,000

Goodwill 450,000 -0- 450,000

Total assets 3,030,000 725,000 3,215,000

Liabilities (780,000) (88,000) (868,000)

Common stock (500,000) (100,000) (S)100,000 (500,000)

Alternatively, the goodwill impairment loss could have been recognized as an

adjustment on the worksheet.

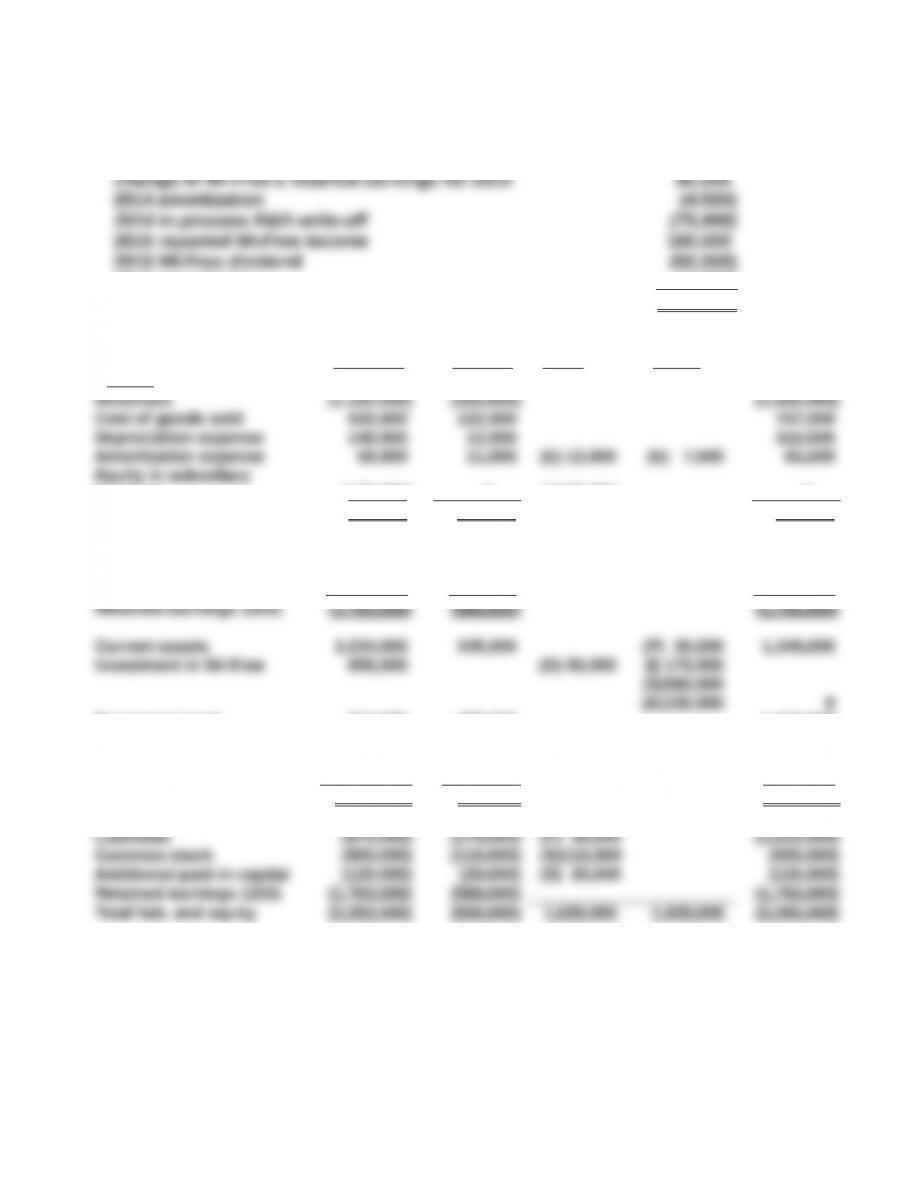

Excel Case 2 Solution

Part a: Investment in Wi-Free account balance 12/31/15

Wi-Free’s acquisition-date fair value $730,000

2015 amortization (4 ,500)

Balance 12/31/15 $856 ,000

Part b: Consolidation Entries Consolidated

Hi-Speed Wi-Free Debit Credit

Totals

earnings (175,500) -0- (I)175,500 -0-

Net Income (460,500) (180,000) (460,500)

Retained earnings 1/1 (1,552,500) (450,000) (S)450,000 (1,552,500)

Net income (460,500) (180,000) (460,500)

Dividends declared 250,000 50,000 (D) 50,000 250,000

Equipment (net) 713,000 305,000 1,018,000

Computer software 650,000 130,000 (E) 7,500 (A) 22,500 765,000

Internet domain name 0 100,000 (A)108,000 (E) 12,000 196,000

Goodwill -0- -0- (A) 65,000 65,000

Total assets 3,253,000 880,000 3,393,000