38. (90 minutes) Remeasure the foreign currency transactions of a foreign

subsidiary into the subsidiary’s functional currency and then translate the

subsidiary’s trial balance into the parent’s reporting currency

a.

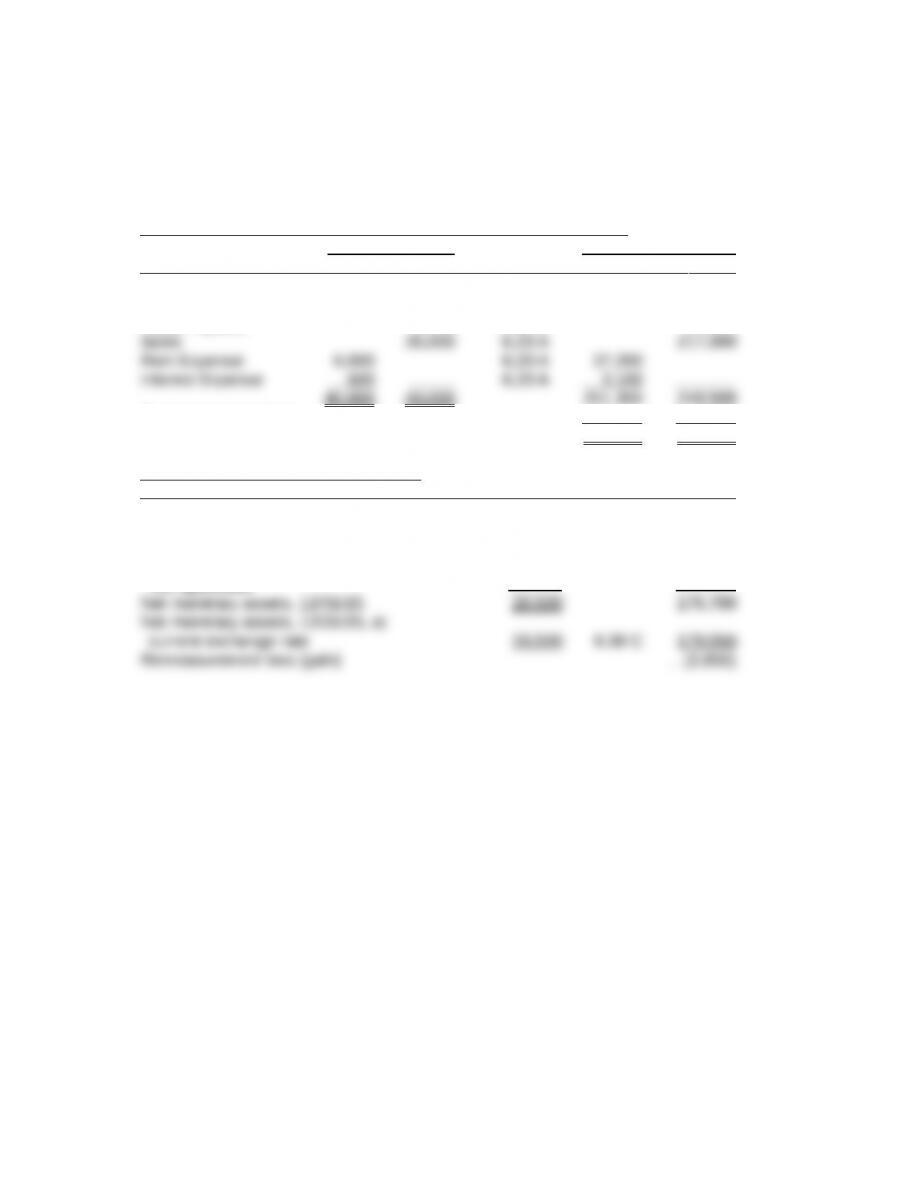

Remeasurement of BRL Trial Balance into Mexican Pesos MXN

BRL MXN

Debit Credit Rate Debit Credit

Cash 5,500 6.30 C 34,650

Accounts Receivable 28,000 6.30 C 176,400

Notes Payable 5,000 6.30 C 31,500

Remeasurement Gain 2,850

Total 251,350 251,350

Calculation of Remeasurement Gain

BRL Rate MXN

Net monetary asset balance, 1/1/15 0

Increase in net monetary items:

Income (sales less rent and interest) 28,500 6.20 A 176,700

Decrease in net monetary items:

Not applicable

38. (continued)

Calculation of Cumulative Translation Adjustment

MXN Rate USD

Net asset balance, 1/1/15 14,500,000 0.080 H 1,160,000.00

Increase in net assets:

Net assets, 12/31/15, at

current exchange rate 14,679,550 0.072 C 1,056,927.60

Translation adjustment, 2015 (debit) 120,538.65

Cumulative translation adjustment, 1/1/2015 (debit) Given 39,572.50

Cumulative translation adjustment, 12/31/2015 (debit) 160,111.15

Chapter 10 Develop Your Skills

Research Case 1—Foreign Currency Translation and Hedging Activities

The responses to this assignment will depend upon the company selected by the student for

analysis. It is unlikely that the company selected will disclose the amount of any

remeasurement gains and losses. The amount of translation adjustment reported in

negative translation adjustment indicates the opposite.

Research Case 2—Foreign Currency Translation Disclosures in the Computer Industry

The responses to requirements in this case will depend upon the annual

reports used by students to complete the case. The solution provided here

is based upon 2011 annual reports.

a. In 2011, in addition to providing information related to foreign currency

translation and hedging activities in its Form 10-K under 1A. Risk Factors,

p. 14, IBM also provided information in its Annual Report on these

activities in the following locations:

i. Management Discussion, under Currency Rate Fluctuations, p. 61.

In its Form 10-K for the year ended February 3, 2012 (Fiscal 2012), Dell

provided information related to foreign currency translation and hedging

activities in the following locations:

i. Item 1A. Risk Factors, p. 16, 17, 19.

Research Case 2 (continued)

b. IBM’s foreign operations do not have a predominant functional currency.

The company indicates that it operates in multiple functional currencies

(AR, p. 96). The majority of Dell’s foreign operations have the U.S. dollar

Dell’s foreign operations, on the other hand, are remeasured into dollars

using the temporal method with remeasurement gains and losses

c. From the Consolidated Statement of Comprehensive Income (AR, p. 71), it

can be seen that IBM reported translation adjustments as follows over the

period 2009-2011:

2009: positive $1,675 million

2010: positive $712 million

2011: negative $693 million

The negative sign of the translation adjustment in 2011 indicates that, on

average, the foreign currency functional currencies of IBM’s foreign

operations decreased in value against the U.S. dollar in that year. The

Dell reported foreign currency translation adjustments in Consolidated

Statements of Stockholders’ Equity as follows:

Fiscal 2010: negative $29 million

Fiscal 2011: positive $79 million

Fiscal 2012: negative $74 million

Research Case 2 (continued)

d. In Note D. Financial Instruments, under Foreign Exchange Risk, IBM

indicates that a significant portion of the company’s foreign currency

denominated debt is designated as a hedge of its foreign currency

e. The response to this requirement will vary from student to student. Much

Accounting Standards Case 1—More than One Functional Currency

This case requires students to search the authoritative literature to determine

how the functional currency should be determined for a foreign entity that

has more than one distinct and separable operation.

Source of guidance: FASB ASC 830-10-55-6 Foreign Currency Matters;

Overall; Implementation Guidance and Illustrations: The Functional Currency

ASC 830-10-55-6 states: “In some instances, a foreign entity might have more

than one distinct and separable operation. For example, a foreign entity might

have one operation that sells parent-entity-produced products and another

This guidance indicates that the functional currency should be determined

separately for each distinct and separable operation of a single foreign entity.

Accounting Standards Case 2—Change in Functional Currency

This case requires students to search the authoritative literature to determine

how an entity should handle a change in foreign currency from the foreign

currency to the U.S. dollar. Specific questions are:

Source of guidance: FASB ASC 830-10-45-10 Foreign Currency Matters;

General; Other Presentation Matters; Functional Currency Changes from

Foreign Currency to Reporting Currency

ASC 830-10-45-10 states: “If the functional currency changes from a foreign

currency to the reporting currency, translation adjustments for prior periods

In essence, the authoritative guidance indicates that the change in functional currency from the Canadian dollar to the U.S. dollar should

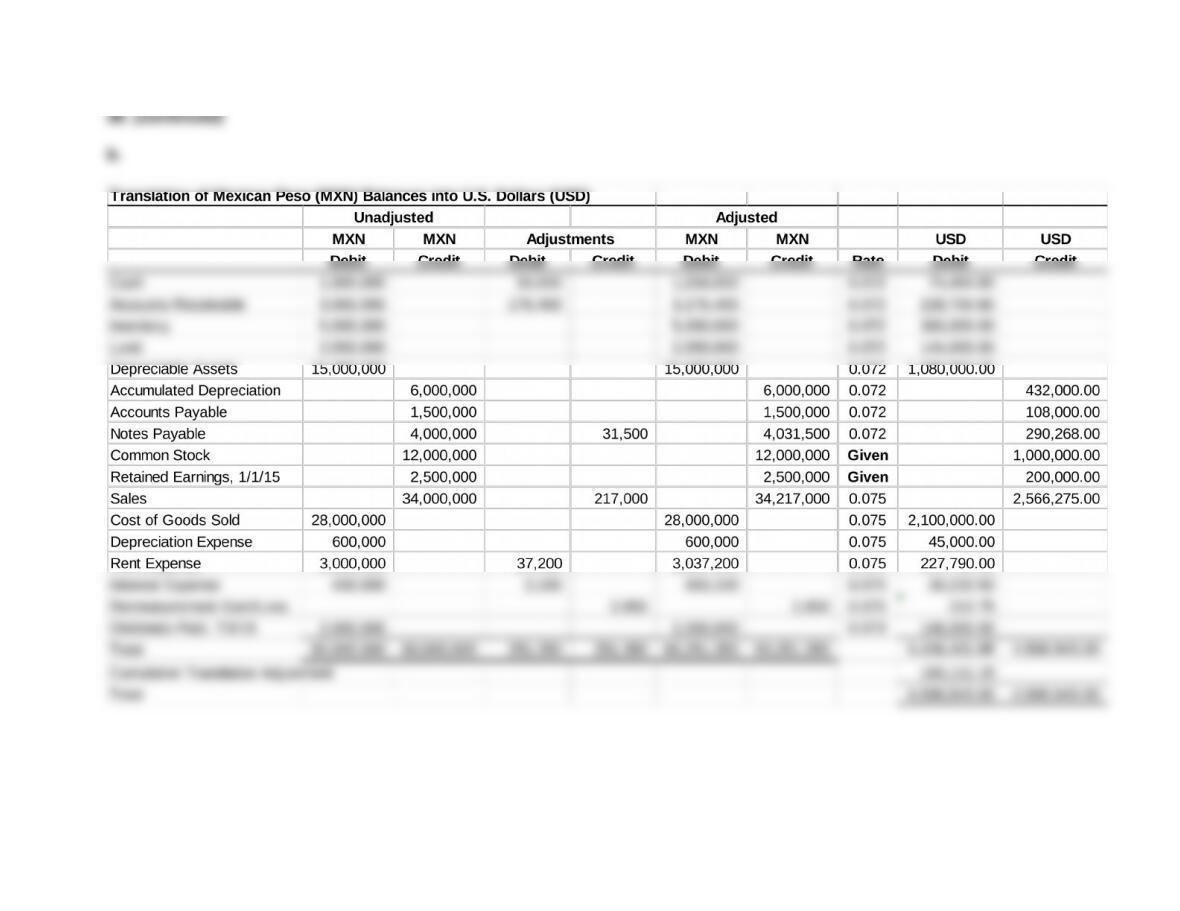

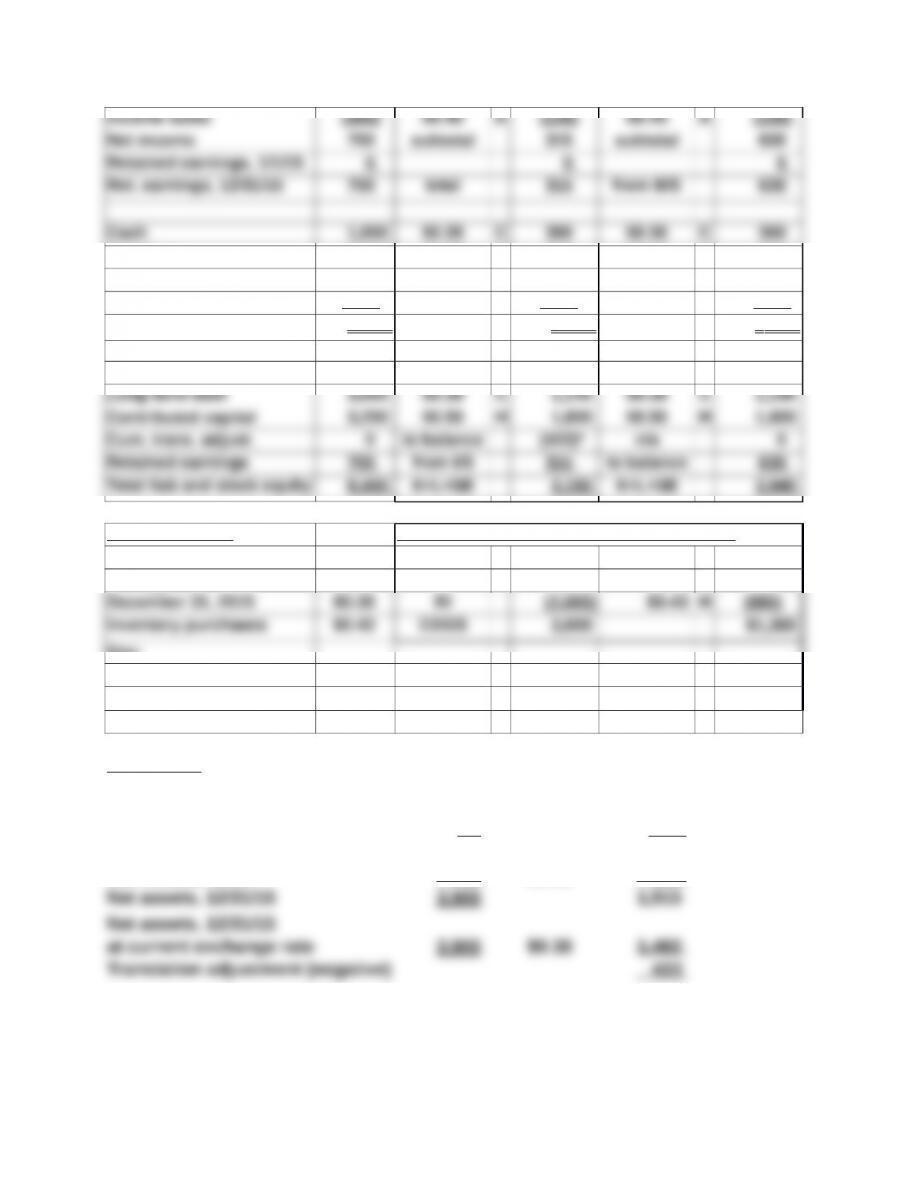

Excel Case—Translating Foreign Currency Financial Statements

a.b. Spreadsheet for the translation (current rate method) and remeasurement

(temporal method) of the FC financial statements of Charles Edward

Company’s foreign subsidiary.

Current Rate Method Temporal Method

December 31, 2015 FC Rate USD Rate USD

Sales 5,000 $0.45 A $2,250 $0.45 A $2,250

Cost of goods sold (3 ,000) $0.45 A (1 ,350) calculation (1 ,360)

Gross profit 2,000 subtotal 900 subtotal 890

Inventory 2,000 $0.38 C 760 $0.43 H 860

Fixed assets 6,000 $0.38 C 2,280 $0.50 H 3,000

Less: accum/deprec (600 ) $0.38 C (228 ) $0.50 H (300 )

Total assets 8 ,400 total 3 ,192 total 3 ,940

Current liabilities 1,500 $0.38 C 570 $0.38 C 570

Exchange Rates Temporal method—COGS (on a FIFO basis)

January 1-31, 2015 $0.50 BI 1,000 $0.50 H $500

Average 2015 $0.45 P 4,000 $0.43 H 1,720

Key:

Average Exchange Rate A

Current Exchange Rate C

Historical Exchange Rate H

Excel Case (continued)

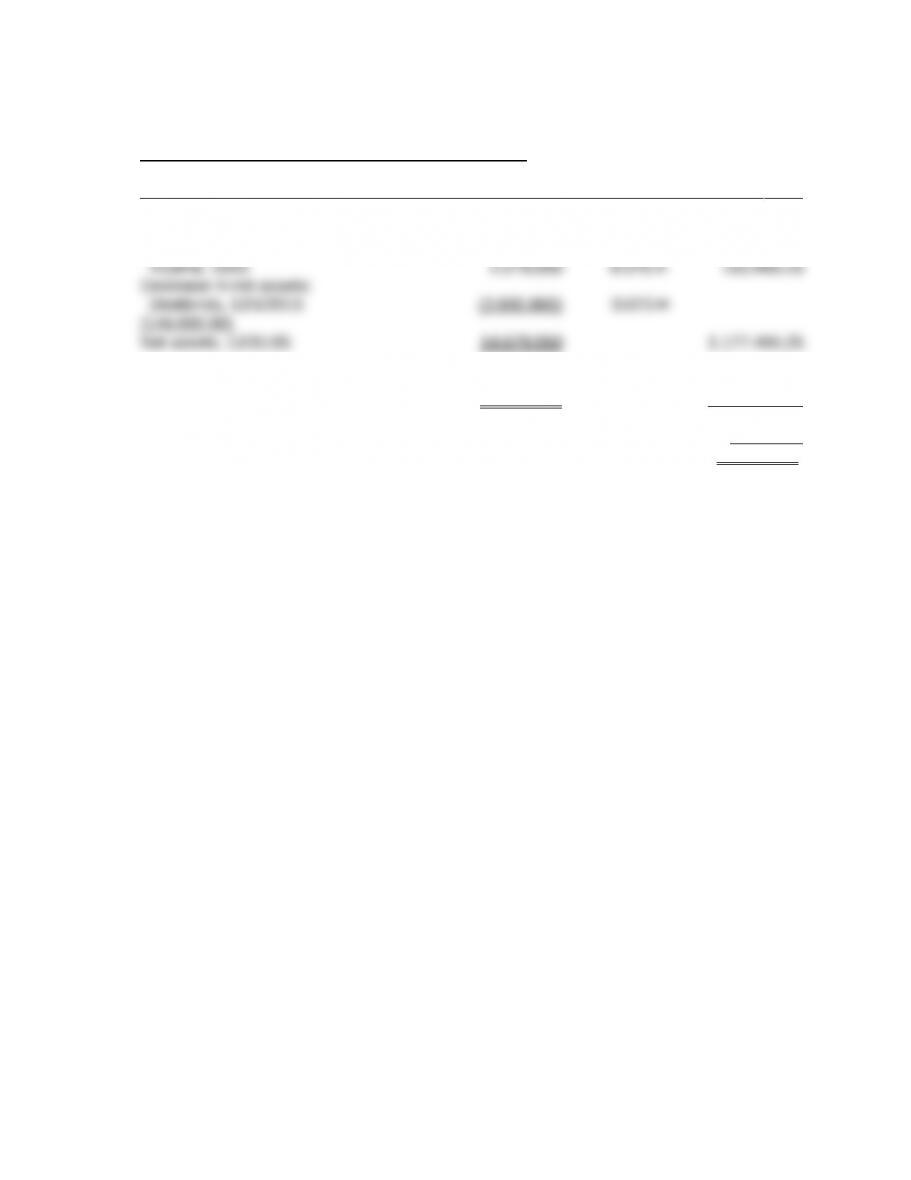

*Computation of Translation Adjustment

FC USD

Net assets, 1/1/15 3,200 $0.50 1,600

Net income, 2015 700 $0.45 315

c. With the FC as functional currency, the U.S. dollar net income reflected in the

consolidated income statement is $315. If the U.S. dollar were the functional

currency, the amount would be twice as much—$630. The amount of total

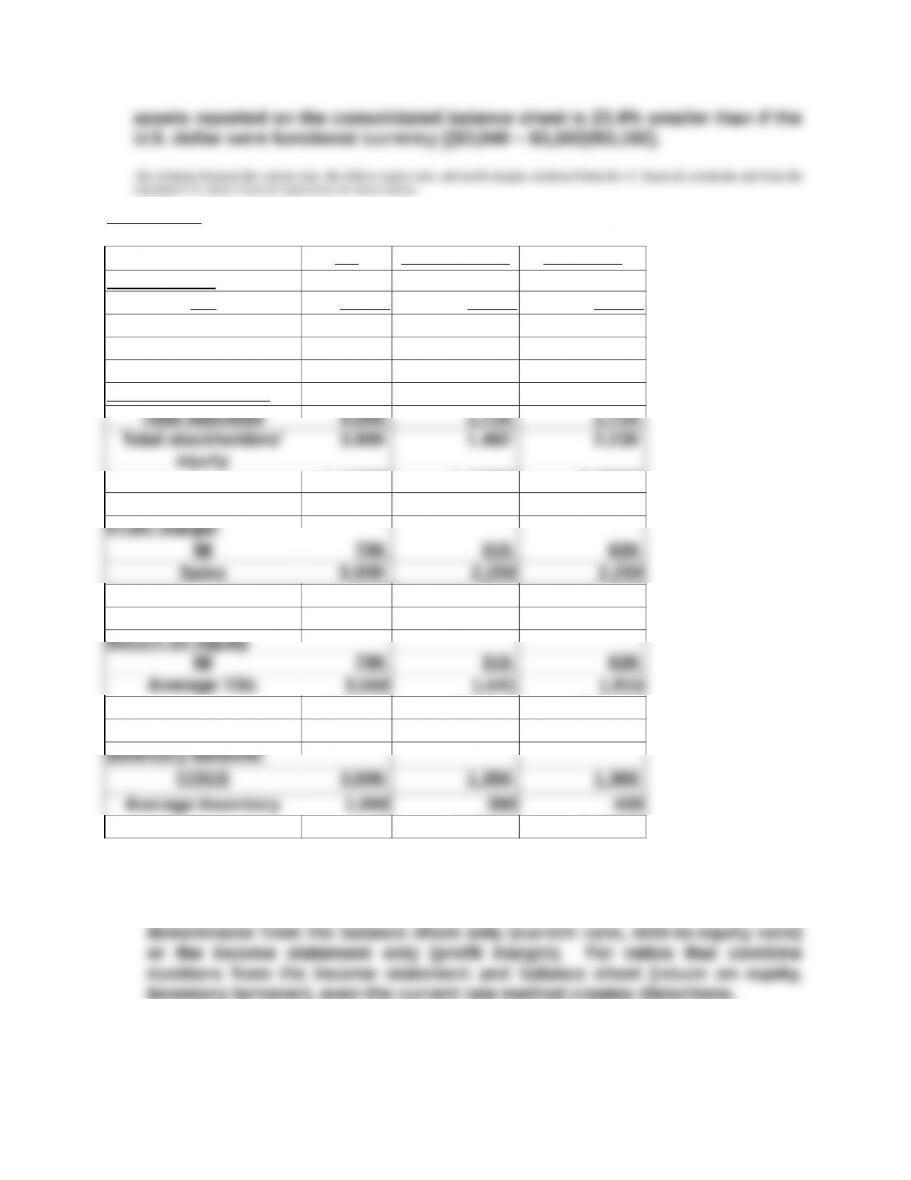

Excel Case (continued)

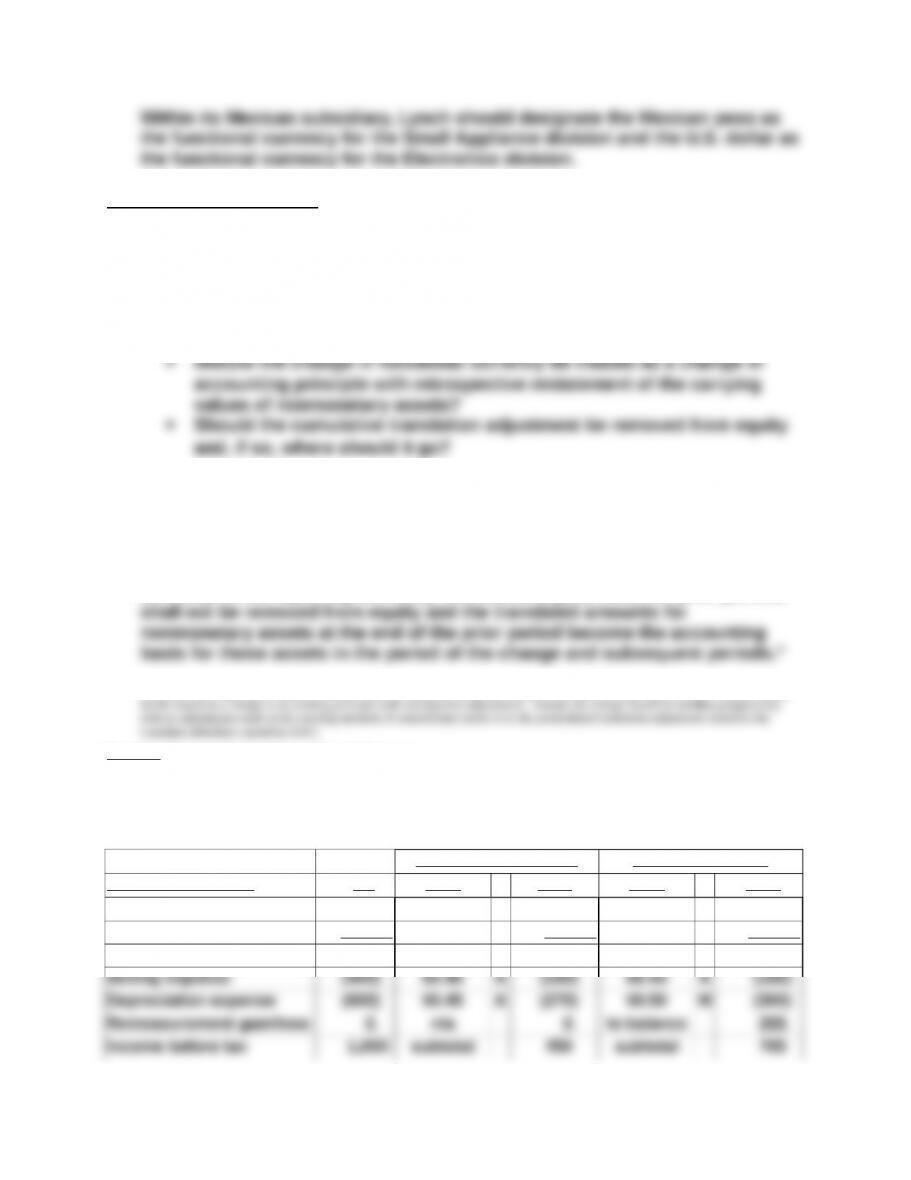

FC Current Rate Temporal

Current ratio

CA 3,000 1,140 1,240

CL 1,500 570 570

2.0 2.0 2.1754

Debt to equity ratio

equity

1.15385 1.15385 0.76682

0.14 0.14 0.28

0.19718 0.20441 0.32898

3 3.55263 3.16279

These results show that the temporal method distorts all ratios as calculated

from the original foreign currency financial statements. The current rate

method maintains all ratios that use numbers in the numerator and

inventory turnover), even the current rate method creates distortions.

The U.S. dollar amounts reported under the temporal method for inventory

and fixed assets reflect the equivalent U.S. dollar cost of those assets as if

Excel Case (continued)

The U.S. dollar amounts reported under the current rate method for inventory

and fixed assets reflect neither the equivalent U.S. dollar cost of those

assets nor their U.S. dollar current value. By multiplying the FC historical

Excel and Analysis Case—Parker Inc. and Suffolk PLC

This assignment requires translation of foreign currency financial

statements under three different sets of assumptions regarding changes in

Part I—Appreciating Foreign Currency

Relevant exchange rates: January 1, 2014 $1.60

2014 Average $1.62