24. C (Determine reportable segments under three tests)

Revenue Test

Combined segment revenues $32,750,000

10% criterion x 10%

Minimum $ 3,275,000

24. (continued)

Asset Test

Combined segment assets $67,500,000

10% criterion x 10%

25. D

26. B (Determine minimum number of reportable segments under 75% rule)

The test to verify that a sufficient number of industry segments is being

disclosed is based on revenues generated from unaffiliated customers.

27. C (Determine expense amounts to be recognized in interim period)

Depreciation $70,000 x 1/4 = $17,500

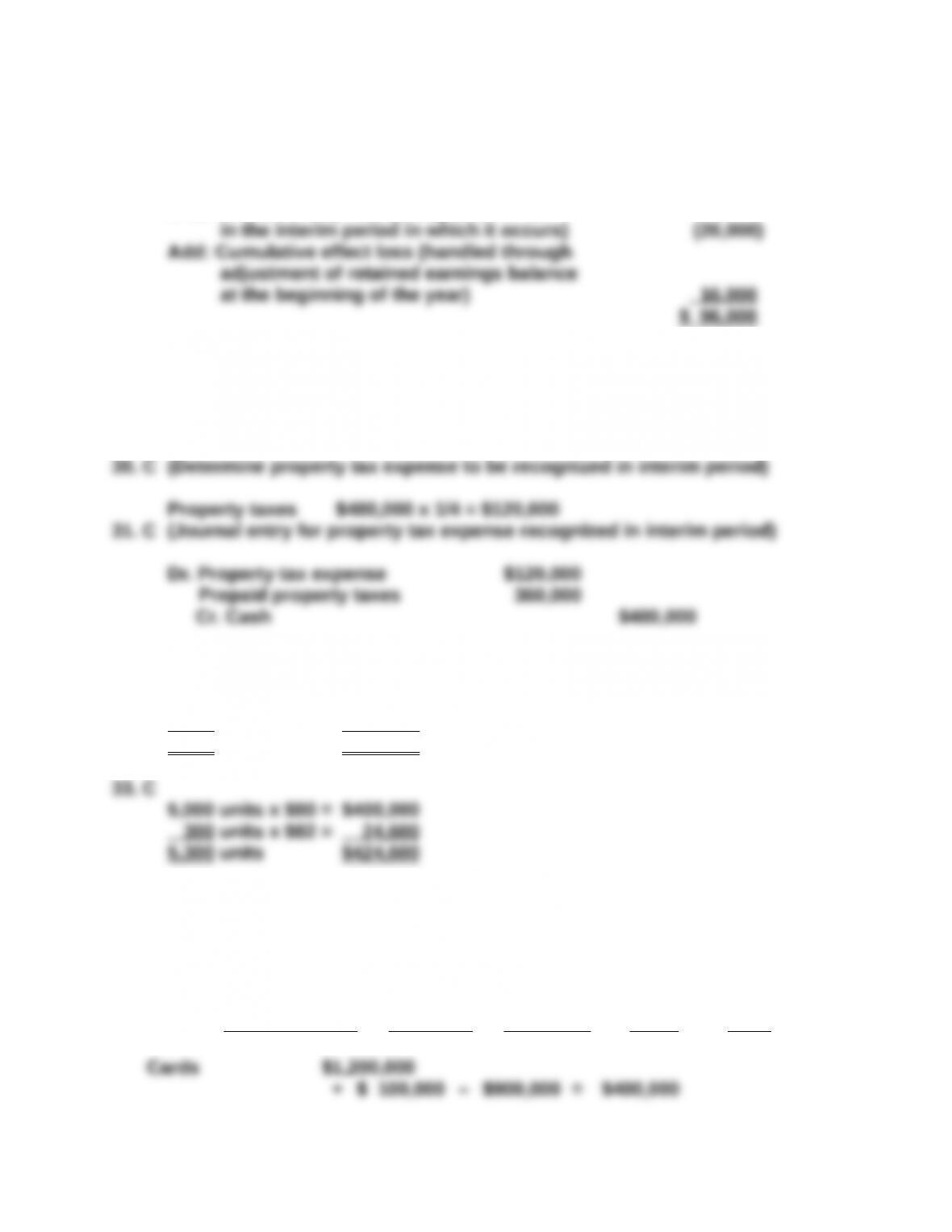

28. C (Determine net income to be reported in interim period)

Income as reported $100,000

Less: Extraordinary loss (recognized in full

29. C (Determine bonus expense to be recognized in interim period)

Bonus $1,000,000 x 1/4 = $250,000

32. A (Determine COGS in interim period under LIFO with LIFO liquidation)

5,000 units x $80 = $400,000

300 units x $50 = 15,000

5,300 units $415,000

34. (10 minutes) (Apply the Profit or Loss Test to Determine Reportable Operating

Segments)

Calculation of profit or loss.

Revenues Intersegment Operating

from Outsiders Transfers Expenses Profit Loss

35. (25 minutes) (Apply the Three Tests Necessary to Determine Reportable

Operating Segments)

Revenue Test (numbers in thousands)

Segment Revenues Percentage

Plastics $ 6,842 61.6% (reportable)

Metals 2,561 23.1% (reportable)

Profit or Loss Test (numbers in thousands)

Segment Revenues Expenses Profit Loss

Plastics $ 6,842 $ 4,290 $2,552 $ (reportable)

Metals 2,561 1,793 768 (reportable)

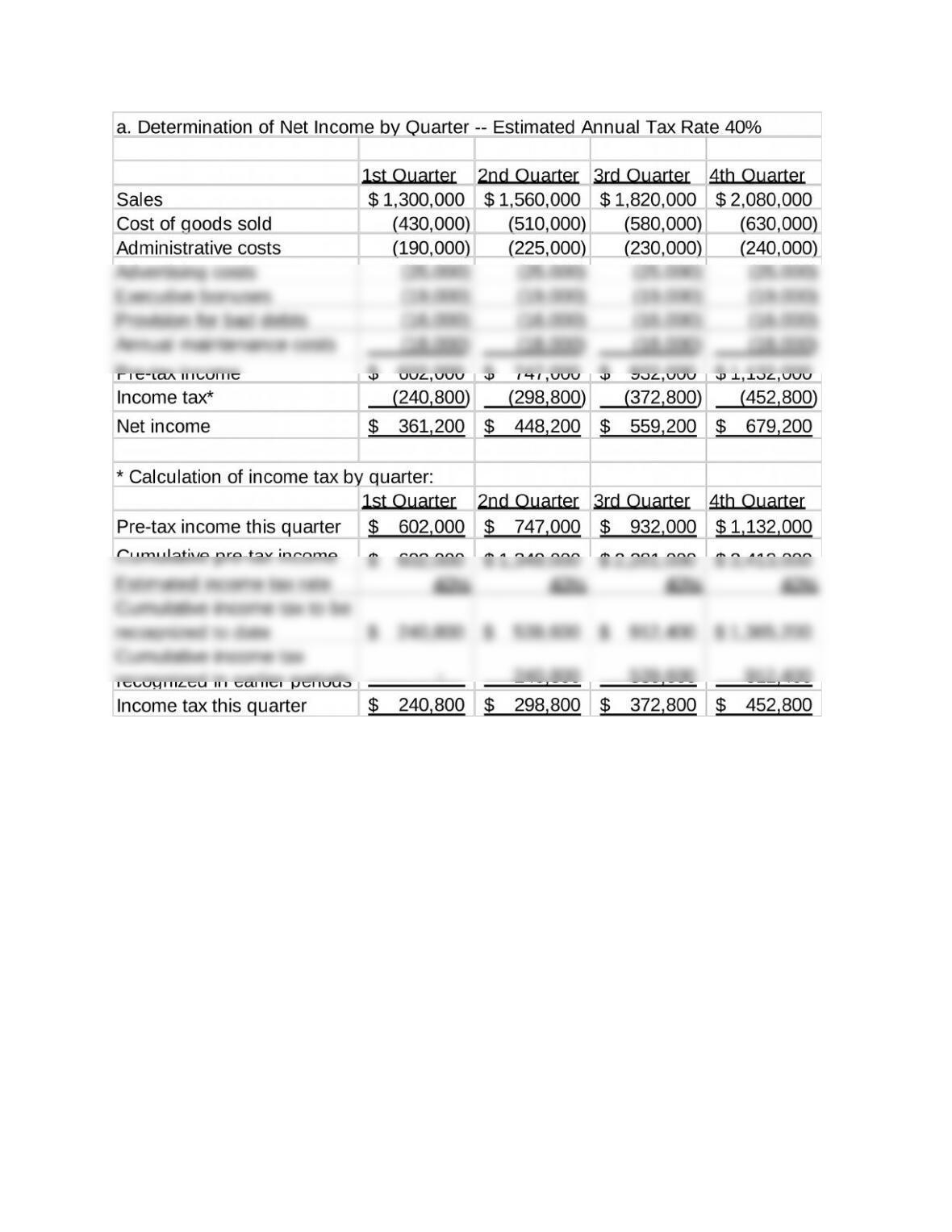

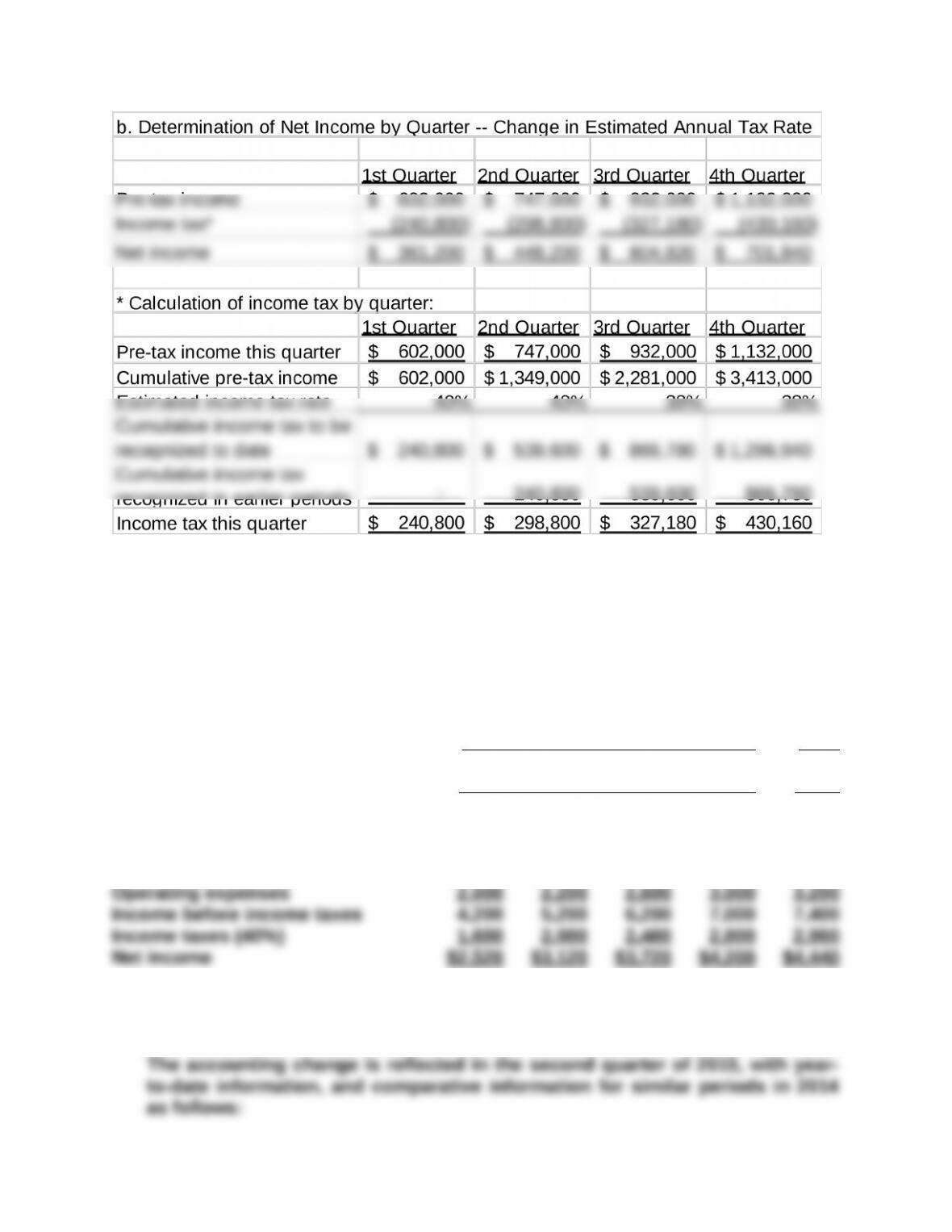

Asset Test (numbers in thousands)

Segment Assets Percentage

Plastics $1,588 21.4% (reportable)

Metals 3,599 48.4% (reportable)

three tests and therefore are reportable.

36. (20 minutes) (A Variety of Computational Questions about Operating Segment

and Major Customer Testing)

a. Total revenues for Fairfield (including intersegment revenues) amount to

$420,000.

b. Disclosure of operating segments is considered adequate only if the

separately reported segments have sales to unaffiliated customers that

disclosure of these three segments would be adequate.

c. Major customer disclosure is based on a level of sales to unaffiliated

d. This test is based on the greater (in absolute terms) of profits or losses. In

this problem, the total profit of Red, Blue, Green, and White ($1,971,000) is

37. (25 minutes) (Apply the three tests necessary to determine reportable

operating segments and determine whether a sufficient number of segments

is reported)

Revenue Test (numbers in thousands)

Segment Revenues Percentage

Books $ 205 9.3%

Finance 184 8.3%

Total $2,212 100.0%

Profit or Loss Test (numbers in thousands)

Segment Revenues Expenses Profit Loss

Books $ 205 $ 218 $ 13

Computers 936 899 $ 37 (reportable)

This test is based on the greater (in absolute amount) of total profit from

Asset Test (numbers in thousands)

Segment Assets Percentage

Books $ 206 6.1%

Computers 1,378 40.5% (reportable)

Total $3,398 100.0%

37. (continued)

Test for Sufficient Number of Segments Being Reported

Four of Mason’s segments (computers, maps, travel, and finance) meet at

least one of the tests carried out above. To determine whether a sufficient

number of segments is being reported, revenues from unaffiliated parties

segments.

Segment Sales to Outsiders

Computers $ 696

Maps 416

38. (15 minutes) (Apply materiality tests adopted by a company to determine

countries to be reported separately)

Revenue Test (sales to unaffiliated parties)

United States $4,610,000 80.3%

Spain 395,000 6.9%

Long-lived Asset Test

United States $1,894,000 83.7%

Spain 191,000 8.4%

None of the individual foreign countries meets either the revenue or long-

39. (20 minutes) (Allocate costs incurred in one quarter that benefit the entire year

and determine income tax expense

39. (continued)

40. (15 minutes) (Treatment of accounting change made in other than first interim

period)

Retrospective application of the FIFO method results in the following

restatements of income for 2014 and the first quarter of 2015:

2014 2015

1 st

Q. 2 nd

Q. 3 rd

Q. 4 th

Q. 1 st

Q.

Sales $10,000 $12,000 $14,000 $16,000 $18,000

Cost of goods sold (FIFO) 3,800 4,600 5,200 6,000 7,400

Net income in the second quarter of 2015 is $4,560 [$20,000 – 9,000 – 3,400 =

$7,600 – 3,040 (40%) = $4,560].

Three Months Ended Six Months Ended

June 30 June 30

2014 2015 2014 2015

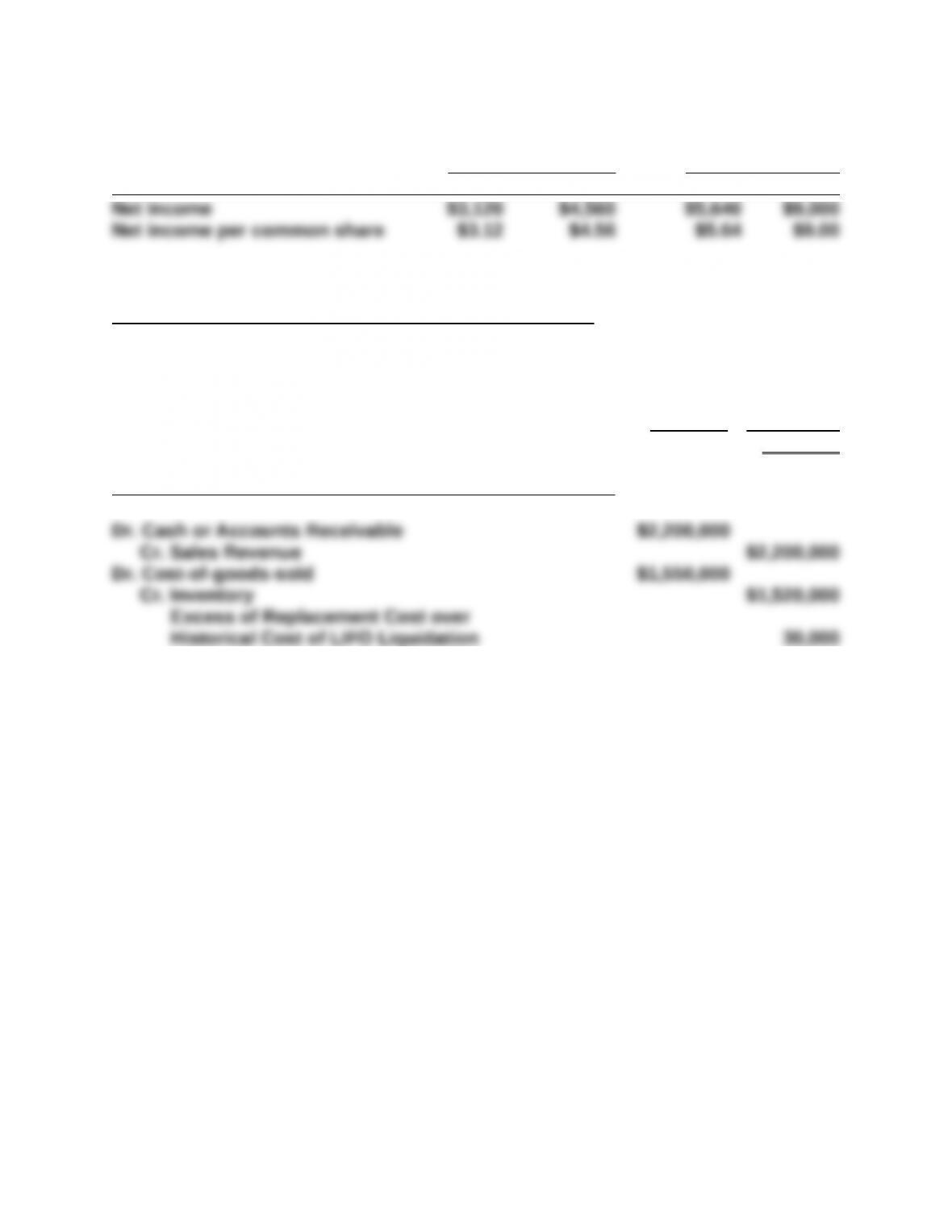

41. (10 minutes) (LIFO liquidation in interim report)

Determination of Cost-of-Goods-Sold and Gross Profit

Sales (110,000 units @ $20) $2,200,000

Cost-of-goods-sold

100,000 units @ $14 $1,400,000

10,000 units @ $15 (replacement cost) 150,000 1,550,000

Gross profit $650,000

Journal Entries to Record Sales and Cost-of-Goods-Sold

To record cost-of-goods-sold with a historical cost of $1,520,000 and an excess of

replacement cost over historical cost for beginning inventory liquidated of

$30,000 (($15 – $12) x 10,000 units).