1) Mills Inc. had a receivable from a foreign customer that is due in the local currency

of the customer (stickles). On December 31, 2012, this receivable for §200,000 was

correctly included in Mills’ balance sheet at $132,000. When the receivable was

collected on February 15, 2013, the U.S. dollar equivalent was $144,000. In Mills’ 2013

consolidated income statement, how much should have been reported as a foreign

exchange gain?

A.$0

B.$36,000

C.$48,000

D.$10,000

E.$12,000

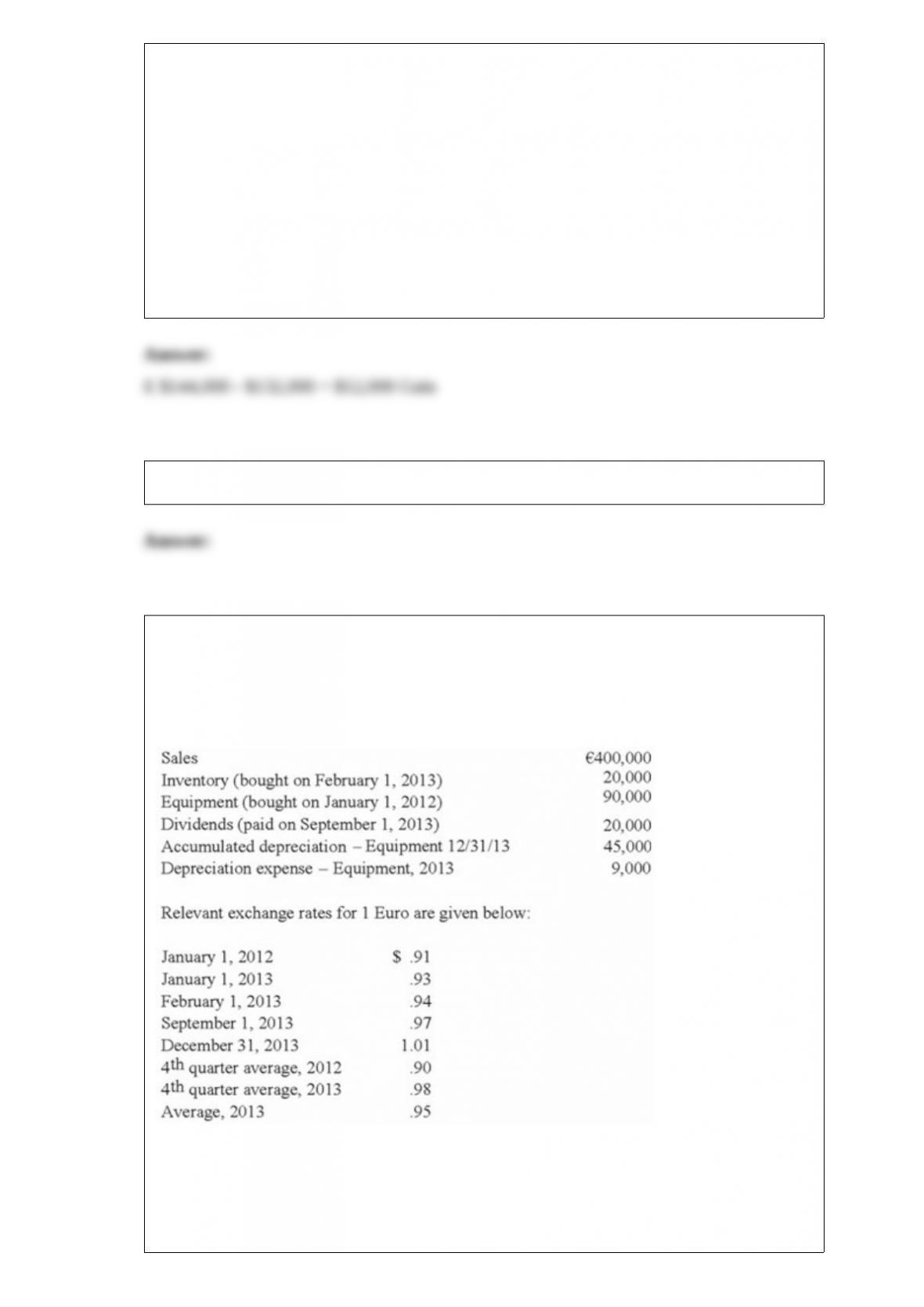

3) Quadros Inc., a Portuguese firm was acquired by a U.S. company on January 1,

2012. Selected account balances are available for the year ended December 31, 2013,

and are stated in Euro, the local currency.

Assume the functional currency is the U.S. Dollar; compute the U.S. balance sheet

amount for inventory, at cost, for 2013

A.$18,800

B.$19,600

C.$18,000

D.$20,200

E.$19,000

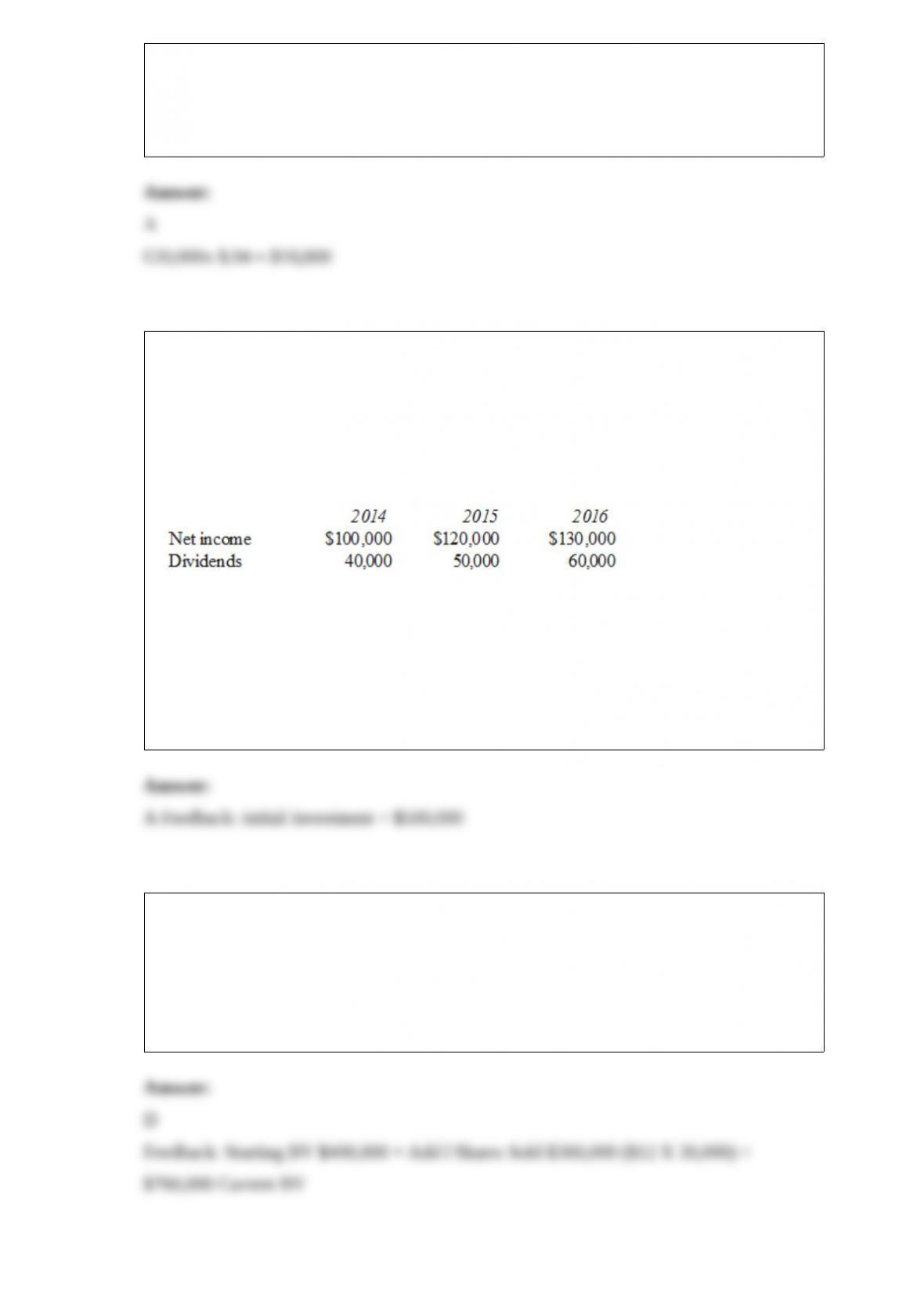

4) Pell Company acquires 80% of Demers Company for $500,000 on January 1, 2014.

Demers reported common stock of $300,000 and retained earnings of $210,000 on that

date. Equipment was undervalued by $30,000 and buildings were undervalued by

$40,000, each having a 10-year remaining life. Any excess consideration transferred

over fair value was attributed to goodwill with an indefinite life. Based on an annual

review, goodwill has not been impaired.

Demers earns income and pays dividends as follows:

Assume the INITIAL VALUE is applied.

Compute Pell’s investment in Demers at December 31, 2014.

A) $500,000.

B) $574,400.

C) $625,000.

D) $542,400.

E) $532,000.

5) What is the adjusted book value of Chase Company after the issuance of the shares?

A) $608,000.

B) $720,000.

C) $680,000.

D) $760,000.

E) $400,000.

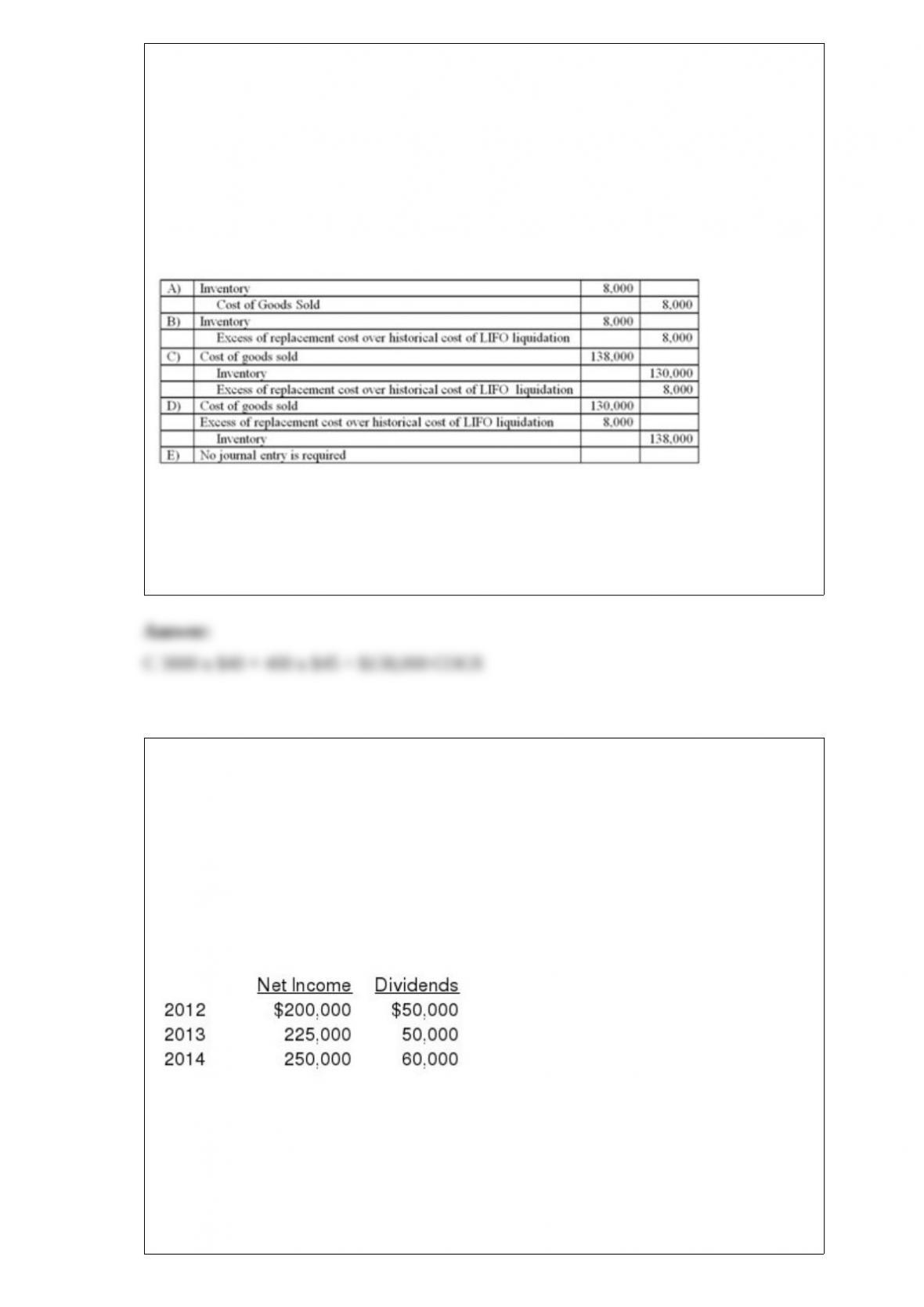

6) Cement Company, Inc. began the first quarter with 1,000 units of inventory costing

$25 per unit. During the first quarter, 3,000 units were purchased at a cost of $40 per

unit, and sales of 3,400 units at $65 per units were made. During the second quarter, the

company expects to replace the units of beginning inventory sold at a cost of $45 per

unit. Cement Company uses the LIFO method to account for inventory.

What is the correct journal entry to record cost of goods sold at the end of the first

quarter?

A.Option A

B.Option B

C.Option C

D.Option D

E.Option E

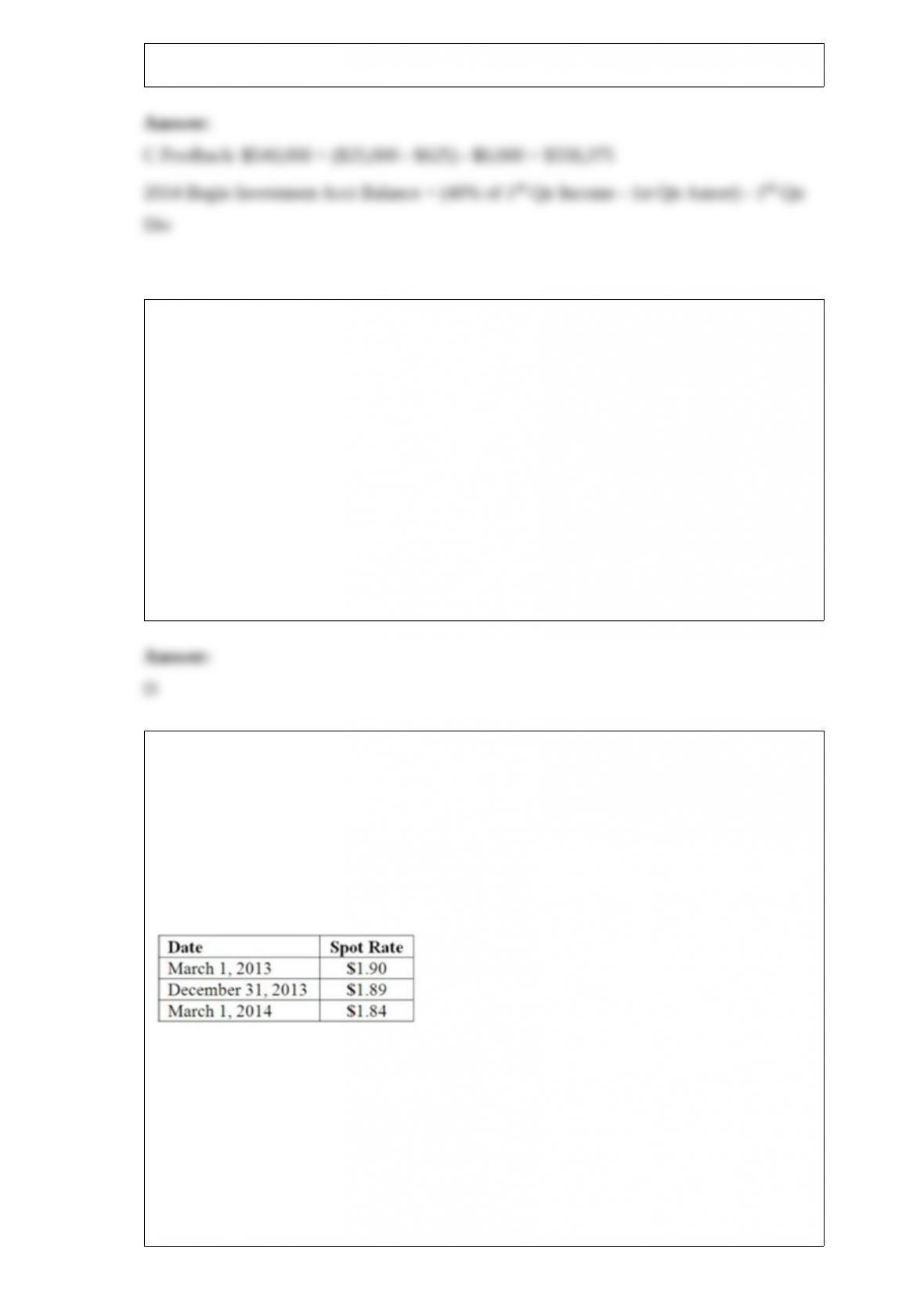

7) On January 1, 2012, Mehan, Incorporated purchased 15,000 shares of Cook

Company for $150,000 giving Mehan a 15% ownership of Cook. On January 1, 2013

Mehan purchased an additional 25,000 shares (25%) of Cook for $300,000. This last

purchase gave Mehan the ability to apply significant influence over Cook. The book

value of Cook on January 1, 2012, was $1,000,000. The book value of Cook on January

1, 2013, was $1,150,000. Any excess of cost over book value for this second transaction

is assigned to a database and amortized over five years.

Cook reports net income and dividends as follows. These amounts are assumed to have

occurred evenly throughout the years:

On April 1, 2014, just after its first dividend receipt, Mehan sells 10,000 shares of its

investment. What was the balance in the investment account at April 1, 2014 just before

the sale of shares?

A) $468,281.

B) $468,750.

C) $558,375.

D) $616,000.

E) $624,375.

8) White Company owns 60% of Cody Company. Separate tax returns are required. For

2012, White’s operating income (excluding taxes and any income from Cody) was

$300,000 while Cody reported a pretax income of $125,000. During the period, Cody

paid a total of $25,000 in cash dividends; $15,000 (60%) to White and $10,000 to the

non-controlling interest. White paid dividends of $180,000. The income tax rate for

both companies is 30%.

Compute the income tax payable by White for 2013.

A.$93,600.

B.$91,350.

C.$94,500.

D.$90,900.

E.$90,000.

9) On March 1, 2013, Mattie Company received an order to sell a machine to a

customer in England at a price of 200,000 British pounds. The machine was shipped

and payment was received on March 1, 2014. On March 1, 2013, Mattie purchased a

put option giving it the right to sell 200,000 British pounds on March 1, 2014 at a price

of $380,000. Mattie properly designates the option as a fair hedge of the pound firm

commitment. The option cost $2,000 and had a fair value of $2,200 on December 31,

2013. The following spot exchange rates apply:

Mattie’s incremental borrowing rate is 12 percent, and the present value factor for two

months at a 12 percent annual rate is .9803.

What was the net impact on Mattie’s 2013 income as a result of this fair value hedge of

a firm commitment?

A.$1,800.00 decrease.

B.$1,760.60 decrease.

C.$2,240.40 decrease.

D.$1,660.40 increase.

E. $2,240.60 increase.

10) Walsh Company sells inventory to its subsidiary, Fisher Company, at a profit during

2012. One-third of the inventory is sold by Walsh uses the equity method to account for

its investment in Fisher.

In the consolidation worksheet for 2012, which of the following choices would be a

debit entry to eliminate unrealized intra-entity gross profit with regard to the 2012

intra-entity sales?

A) Retained earnings.

B) Cost of goods sold.

C) Inventory.

D) Investment in Fisher Company.

E) Sales.

11) Strickland Company sells inventory to its parent, Carter Company, at a profit during

2012. One-third of the inventory is sold by Carter in 2012.

In the consolidation worksheet for 2013, assuming Carter uses the initial value methd of

accounting for its investment in Strickland, which of the following choices would be a

credit entry to eliminate unrealized intra-entity gross profit with regard to the 2012

intra-entity sales?

A) Retained earnings.

B) Cost of goods sold.

C) Inventory.

D) Investment in Strickland Company.

E) Sales.

12) On January 1, 2013, a subsidiary buys 12 percent of the outstanding voting stock of

its parent corporation. The payment of $400,000 exceeded book value of the acquired

shares by $80,000, attributable to a copyright with a 10-year useful life. During the

year, the parent reported operating income of $1,000,000 (excluding investment income

from the subsidiary), and paid $120,000 in dividends. If the treasury stock approach is

used, how is the Investment in Parent Stock reported in the consolidated balance sheet

at December 31, 2013?

A.Consolidated stockholders’ equity is reduced by $400,000.

B.Consolidated stockholders’ equity is reduced by $320,000.

C.Included in current assets.

D.Included in noncurrent assets.

E.There is no effect on the consolidated balance sheet, because the effects have been

eliminated.

13) On January 1, 2013, Payton Co. sold equipment to its subsidiary, Starker Corp., for

$115,000. The equipment had cost $125,000, and the balance in accumulated

depreciation was $45,000. The equipment had an estimated remaining useful life of

eight years and $0 salvage value. Both companies use straight-line depreciation. On

their separate 2013 income statements, Payton and Starker reported depreciation

expense of $84,000 and $60,000, respectively. The amount of depreciation expense on

the consolidated income statement for 2013 would have been

A) $144,000.

B) $148,375.

C) $109,000.

D) $134,000.

E) $139,625.

14) Pepe, Incorporated acquired 60% of Devin Company on January 1, 2012. On that

date Devin sold equipment to Pepe for $45,000. The equipment had a cost of $120,000

and accumulated depreciation of $66,000 with a remaining life of 9 years. Devin

reported net income of $300,000 and $325,000 for 2012 and 2013, respectively. Pepe

uses the equity method to account for its investment in Devin.

Compute the income from Devin reported on Pepe’s books for 2013.

A) $190,200.

B) $196,000.

C) $194,400.

D) $187,000.

E) $195,000.

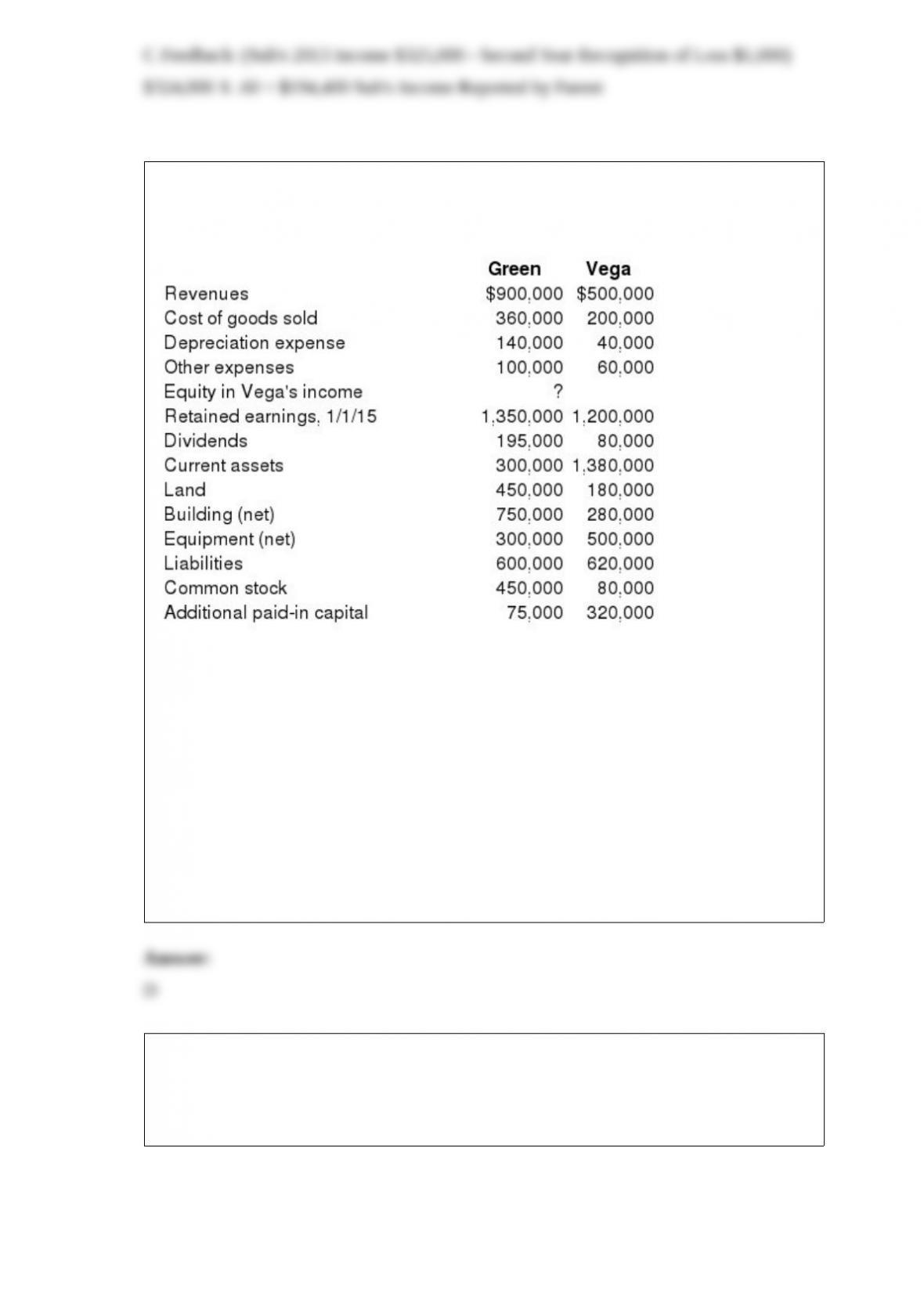

15) Following are selected accounts for Green Corporation and Vega Company as of

December 31, 2015. Several of Green’s accounts have been omitted.

Green acquired 100% of Vega on January 1, 2011, by issuing 10,500 shares of its $10

par value common stock with a fair value of $95 per share. On January 1, 2011, Vega’s

land was undervalued by $40,000, its buildings were overvalued by $30,000, and

equipment was undervalued by $80,000. The buildings have a 20-year life and the

equipment has a 10-year life. $50,000 was attributed to an unrecorded trademark with a

16-year remaining life. There was no goodwill associated with this investment.

Compute the December 31, 2015, consolidated total expenses.

A) $620,000.

B) $280,000.

C) $900,000.

D) $909,625.

E) $299,625.

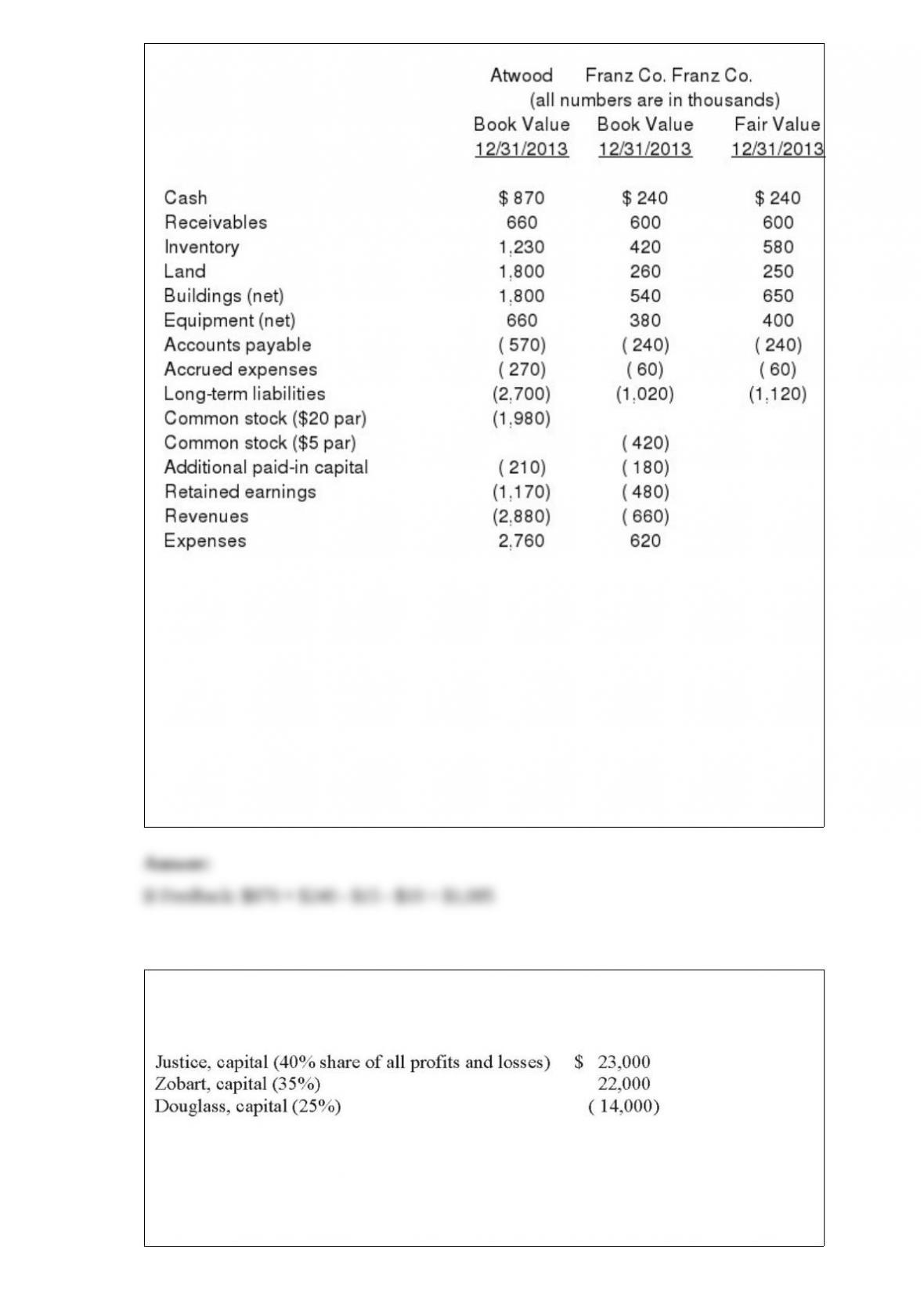

16) The financial balances for the Atwood Company and the Franz Company as of

December 31, 2013, are presented below. Also included are the fair values for Franz

Company’s net assets.

Note: Parenthesis indicate a credit balance

Assume an acquisition business combination took place at December 31, 2013. Atwood

issued 50 shares of its common stock with a fair value of $35 per share for all of the

outstanding common shares of Franz. Stock issuance costs of $15 (in thousands) and

direct costs of $10 (in thousands) were paid.

Compute consolidated cash at the completion of the acquisition.

A) $1,350.

B) $1,085.

C) $1,110.

D) $ 870.

E) $ 845.

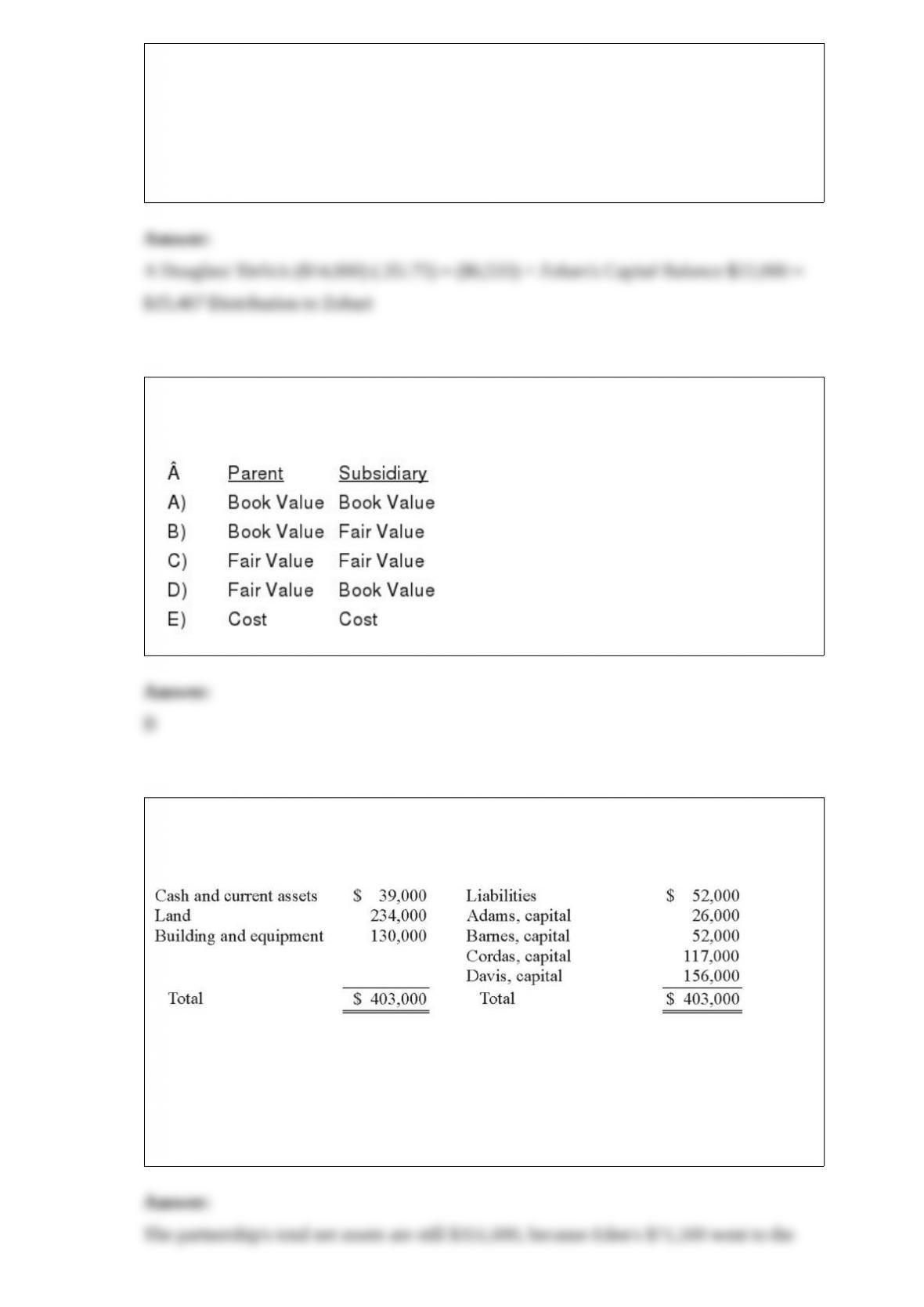

17) A local partnership was in the process of liquidating and reported the following

capital balances:

Douglass indicated that the $14,000 deficit would be covered by a forthcoming

contribution. However, the two remaining partners asked to receive the $31,000 that

was then in the cash account.

How much of this money should Zobart receive?

A.$15,467.

B.$14,467.

C.$17,333.

D.$15,633.

E.$15,867.

18) In an acquisition where control is achieved, how would the land accounts of the

parent and the land accounts of the subsidiary be combined?

19) The ABCD Partnership has the following balance sheet at January 1, 2012, prior to

the admission of new partner, Eden.

Eden acquired a 20% interest in the partnership by contributing a total of $71,500

directly to the other four partners. No goodwill is to be recorded. Profits and losses have

previously been split according to the following percentages: Adams, 15%, Barnes,

35%, Cordas, 30%, and Davis, 20%. After Eden made his investment, what were the

individual capital balances?

20) Norr and Caylor established a partnership on January 1, 2012. Norr invested cash of

$100,000 and Caylor invested $30,000 in cash and equipment with a book value of

$40,000 and fair value of $50,000. For both partners, the beginning capital balance was

to equal the initial investment. Norr and Caylor agreed to the following procedure for

sharing profits and losses:

– 12% interest on the yearly beginning capital balance

– $10 per hour of work that can be billed to the partnership’s clients

– the remainder divided in a 3:2 ratio

The Articles of Partnership specified that each partner should withdraw no more than

$1,000 per month.

For 2012, the partnership’s income was $70,000. Norr had 1,000 billable hours, and

Caylor worked 1,400 billable hours. In 2013, the partnership’s income was $24,000, and

Norr and Caylor worked 800 and 1,200 billable hours respectively. Each partner

withdrew $1,000 per month throughout 2012 and 2013.

Determine the amount of net income allocated to each partner for 2012.

21) During the most recent year, an estate generated income of $26,000:

The interest income was conveyed immediately to the beneficiary stated in the

decedent’s will. Dividends of $1,560 were given to the decedent’s church.

Prepare a schedule to show the amount of taxable income.

22) Fesler Inc. acquired all of the outstanding common stock of Pickett Company on

January 1, 2012. Annual amortization of $22,000 resulted from this transaction. On the

date of the acquisition, Fesler reported retained earnings of $520,000 while Pickett

reported a $240,000 balance for retained earnings. Fesler reported net income of

$100,000 in 2012 and $68,000 in 2013, and paid dividends of $25,000 in dividends

each year. Pickett reported net income of $24,000 in 2012 and $36,000 in 2013, and

paid dividends of $10,000 in dividends each year.

Assume that Fesler’s reported net income includes Equity in Subsidiary Income.

If the parent’s net income reflected use of the initial value method, what were the

consolidated retained earnings on December 31, 2013?

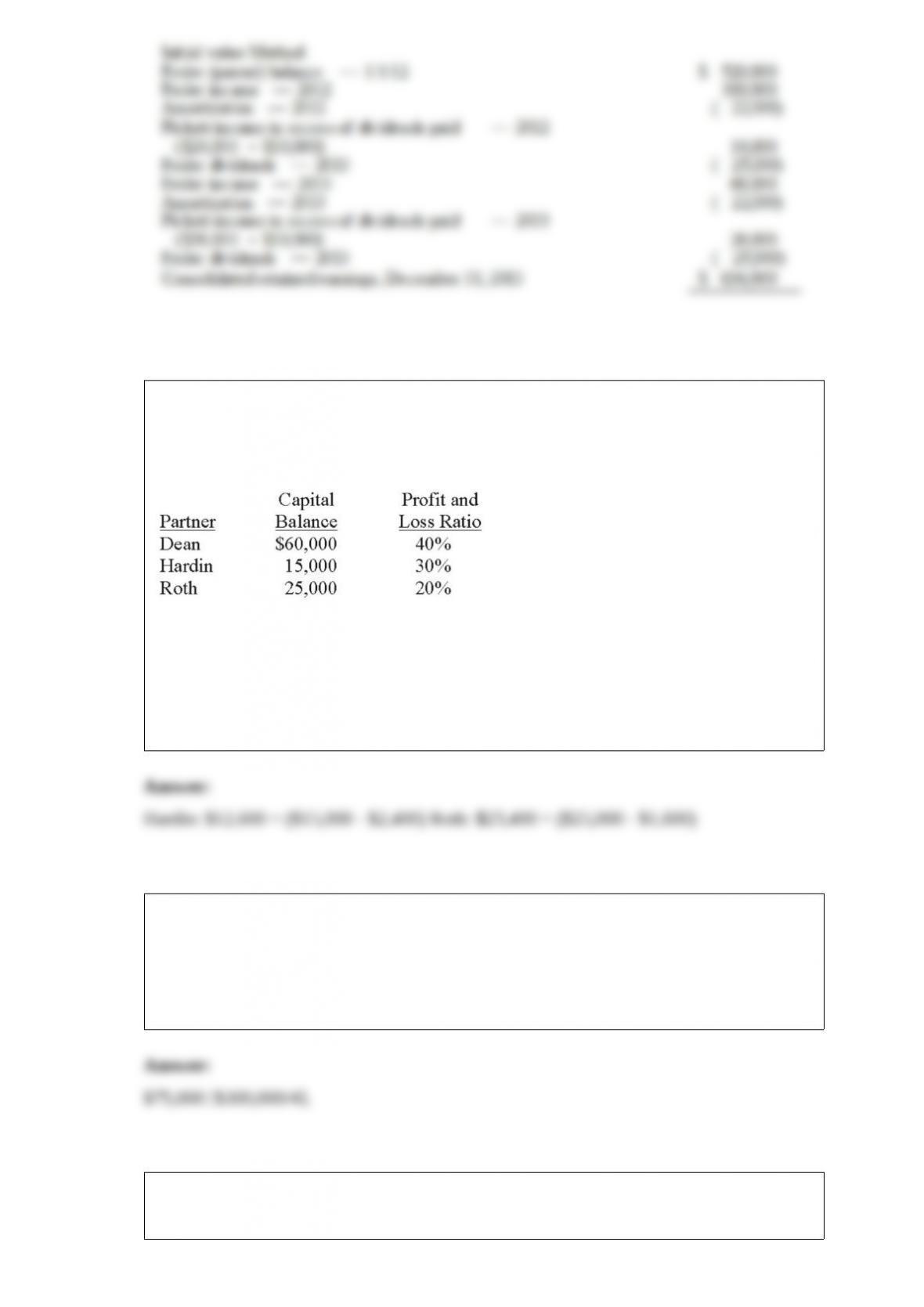

23) Assume the partnership of Dean, Hardin, and Roth has been in existence for a

number of years. Dean decides to withdraw from the partnership when the partners’

capital balances are as follows:

An appraisal of the business and its property estimates the fair value to be $100,000.

Dean has agreed to receive $64,000 in exchange for his partnership interest.

What are the remaining partners’ capital balances after Dean’s interest is dissolved,

assuming the bonus method is applied?

24) On February 23, 2013, Cleveland, Inc. paid property taxes of $300,000 for the

calendar year 2013

How much of this expense should be included in Cleveland’s net income for the quarter

ending March 31, 2013?

25) Hardin, Sutton, and Williams have operated a local business as a partnership for

several years. All profits and losses have been allocated in a 3:2:1 ratio, respectively.

Recently, Williams has undergone personal financial problems, and is insolvent. To

satisfy Williams’ creditors, the partnership has decided to liquidate.

The following balance sheet has been produced:

During the liquidation process, the following transactions take place:

– Noncash assets are sold for $116,000.

– Liquidation expenses of $12,000 are paid. No further expenses are expected.

– Safe capital distributions are made to the partners.

– Payment is made of all business liabilities.

– Any deficit capital balances are deemed to be uncollectible.

Develop a predistribution plan for this partnership, assuming $12,000 of liquidation

expenses are expected to be paid.

26) The executor of the Estate of Kate Tweed discovered the following assets (at fair

value):

The will of Kate Tweed had the following provisions:

– $195,000 in cash went to Victor Vickery.

– All shares of PepsiCo went to Duchess Doyle.

– The residence went to Louis Tweed.

– All other estate assets were to be liquidated with the resulting cash going to the Sacred

Church of Liberty, Missouri.

Funeral expenses of $26,000 were paid.

Prepare the journal entry to record the transaction.