25.(continued)

Entry E

Operating Expenses ………….………..………..………..….. 2,000

Equipment ………..………..………..………..………..…..….. 5,000

Franchise Contracts …………………..….…..….….….. 4,000

Cost of Goods Sold………….……….….…..….….….... 200,000

(To eliminate intra-entity inventory sales for the current year.)

Entry G

Cost of Goods Sold………….………..………..………….….. 18,000

Inventory……………………………..………..………….…...

Noncontrolling interest in Cuddy net income—common ......... $14 ,000

Noncontrolling Interest in Net Income of Wilson:

Reported operating income $130,000

Equity income of Cuddy ($70,000 × 40%)……………..….….…..…... 28,000

Excess amortization………….………..………..………..………..………….. (2,000)

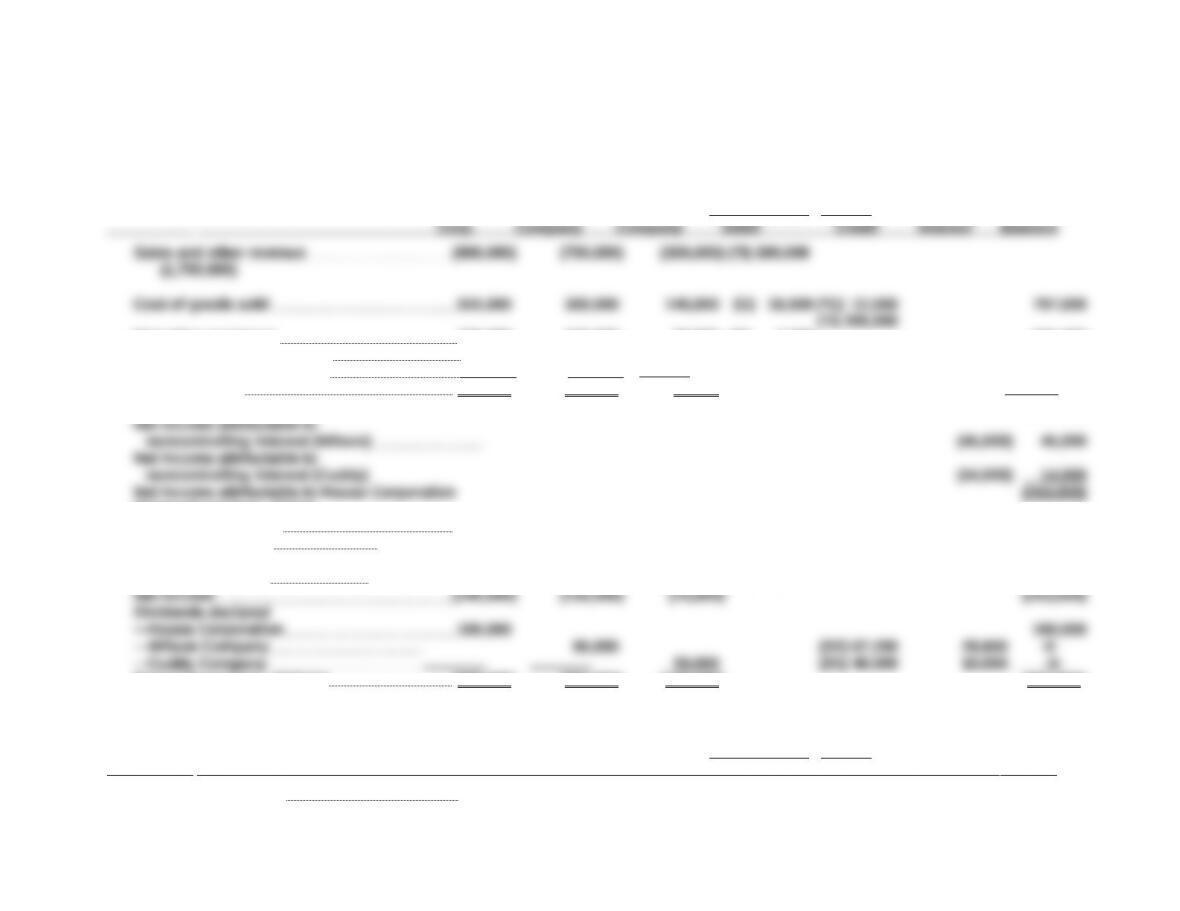

25. (continued)

HOUSE CORPORATION AND CONSOLIDATED SUBSIDIARIES

Consolidation Worksheet

December 31, 2014

Accounts House Wilson Cuddy Consolidation EntriesNoncontrollingConsolidated

Operating expenses 219,000 270,000 90,000 (E) 2,000 581,000

Income of Wilson Company (91,000) (I2) 91,000 -0-

Income of Cuddy Company (28 ,000) (28 ,000) (I1) 56,000 -0-

Net income (249 ,000) (158 ,000) (70 ,000)

Consolidated net income (322,000)

Retained earnings, 1/1/14:

—House Corporation (820,000) (*C) 11,200 (808,800)

—Wilson Company (590,000) (*G) 12,000 -0-

(S2)578,000

—Cuddy Company (150,000)(S1)150,000 -0-

Retained earnings, 12/31/14 (969 ,000) (652 ,000) (170 ,000) (971 ,800)

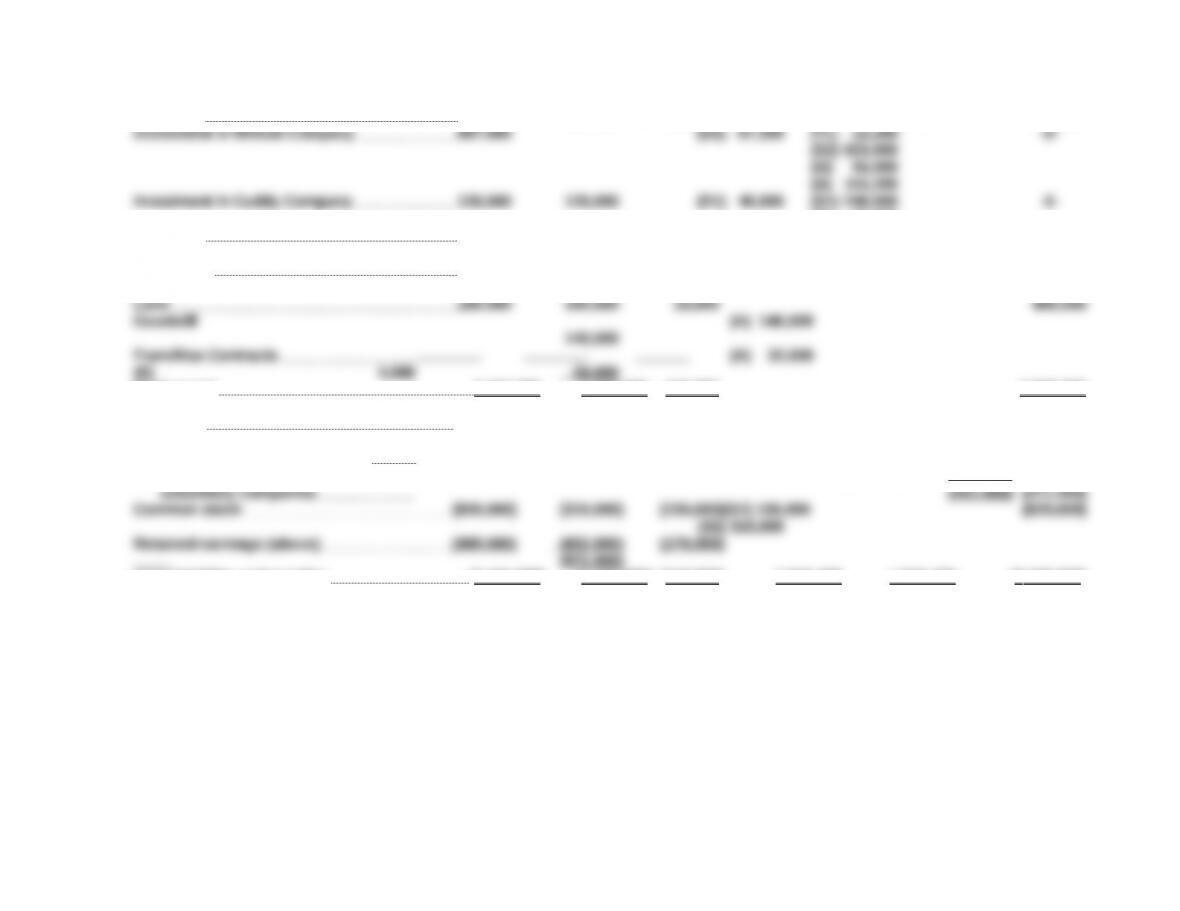

25. (continued)

Accounts House Wilson Cuddy Consolidation EntriesNoncontrollingConsolidated

Corp. Company Company Debit Credit Interest Balance

Cash and receivables 220,000 334,000 67,000 621,000

Inventory 390,200 320,000 103,000 (G) 18,000 795,200

(I1) 56,000

Buildings 385,000 320,000 144,000 (A) 54,000

(E) 3,000 900,000

Equipment 310,000 130,000 88,000 (E) 5,000

(A) 10,000 523,000

Total assets 2 ,421,000 1 ,532,000 418 ,000 3 ,503,200

Liabilities (632,000) (570,000) (98,000) (1,300,000)

Noncontrolling interest in Cuddy (S1) 60,000 (60,000)

Noncontrolling interest in Wilson (S2) 266,400

Noncontrolling interest in (A) 64,800 (331 ,200)

Total liabilities and equities (2 ,421,000) (1 ,532,000) (418 ,000) 1 ,916,400 1 ,916,400 (3 ,503,200)

Parentheses indicate a credit balance.

26. (20 Minutes) (Consolidation entries for a mutual holding business combination)

a. Acquisition Allocation and Amortization

Consideration transferred …………….………..………..…….. $420,000

Noncontrolling interest fair value ……………….….…..…... 280 ,000

Lowly’s business fair value……………………..….….…..…... 700,000

Investment in Lowly …………….………..………….….….... 117,000

Retained Earnings, 1/1/14 (Mighty) .…..….….….… 117,000

(To accrue income to parent during the previous years as measured by

increase in book value [$200,000 × 60%] and amortization expense of $3,000

[$5,000 × 60%] for the previous year.)

(To eliminate subsidiary stockholders’ equity accounts against investment

account and to recognize noncontrolling interest ownership.)

Entry S2

Treasury Stock ……………..………..…………………..……... 240,000

Investment in Mighty ………….……………..…..….….. 240,000

(To recognize unamortized portion of acquisition-date excess fair value.)

Entry E

Amortization Expense ………….…………………..………… 5,000

Trademarks ……………………..………..……………..…... 5,000

(To record trademarks amortization expense for 2014.)

27.(80 Minutes) (Prepare consolidation worksheet for a father-son-grandson

combination. Also asks about income taxes paid on both a separate

and a consolidated return)

a. Acquisition-Date Allocation and Amortization

The January 1, 2013 book values are determined by removing the 2013 income

from the January 1, 2014 book values (based on equity accounts).

Customer List……….………..…………………..………..…………. $ 50,000

Life …………………………..………..………..………..………..….….. 10 Years

Annual amortization ………….………..………….….….…..…... $ 5,000

Consideration transferred for Yarrow……………………….. $720,000

Noncontrolling interest fair value ……………….….…..…... 80,000

CONSOLIDATION ENTRIES

Entry *G

Retained Earnings, 1/1/14 (Stookey) ….…..….….….... 7,680

Cost of Goods Sold………….……….….…..….….….... 7,680

(To give effect to unrealized gross profit from 2013. Amount is calculated

based on normal 48% markup [found from Income Statement] multiplied by

$16,000 retained inventory [20% of $80,000])

Entry *C1

Investment in Stookey …………….…………….….….….… 85,856

Retained Earnings, 1/1/14 (Yarrow) ………….…….. 85,856

27.(continued)

Entry *C2

Investment in Yarrow ………………..………….….…..….… 217,670

Retained Earnings, 1/1/14 (Travers) …………..…... 217,670

(To recognize equity income accruing from Travers’ investment in Yarrow

$217,670 by the $3,600 [90% × $4,000] amortization applicable to 2013.)

Entry S1

Common Stock (Stookey) …………..………..…………….. 200,000

Retained Earnings, 1/1/14 (Stookey, as adjusted

by Entry *G) ………..………..……………….….….….…... 292,320

Entry S2

Common Stock (Yarrow) ……………….………..………..… 300,000

Retained Earnings, 1/1/14 (Yarrow, as adjusted

by Entry *C1) ……….………………..….….….…..….…... 685,856

Investment in Yarrow (90%) ………………………. 887,270

Customer List……….………..………………….…..….….…... 45,000

Investment in Stookey …………….………..…………... 36,000

Noncontrolling Interest in Stookey (20%) .......... 9,000

(To recognize January 1, 2014 unamortized portion of acquisition price

assigned to Stookey’s customer list.)

27. (continued)

Entry A2

Investment in Yarrow ………….………..……………..… 50,400

Noncontrolling Interest in Yarrow………..….…..…. 5,600

(To recognize January 1, 2014 unamortized portion of acquisition price

Entry E

Operating Expenses ………….………..…….…..….….….… 9,000

Entry Tl

Sales ………………..………..………..…………….….….…..….. 100,000

(To defer unrealized gross profit on ending inventory—$20,000 × 48%

markup.)

Noncontrolling Interest in Stookey’s Net Income

2014 Reported net income …………….………..………….…... $100,000

Customer list amortization ………….………….….…..….…... (5,000)

Noncontrolling Interest in Yarrow’s Net Income

2014 Reported net income …………….………..………….…... $200,000

Accrual of Stookey’s income (80% of $93,080

realized income [computed above]) …………….…..…. 74,464

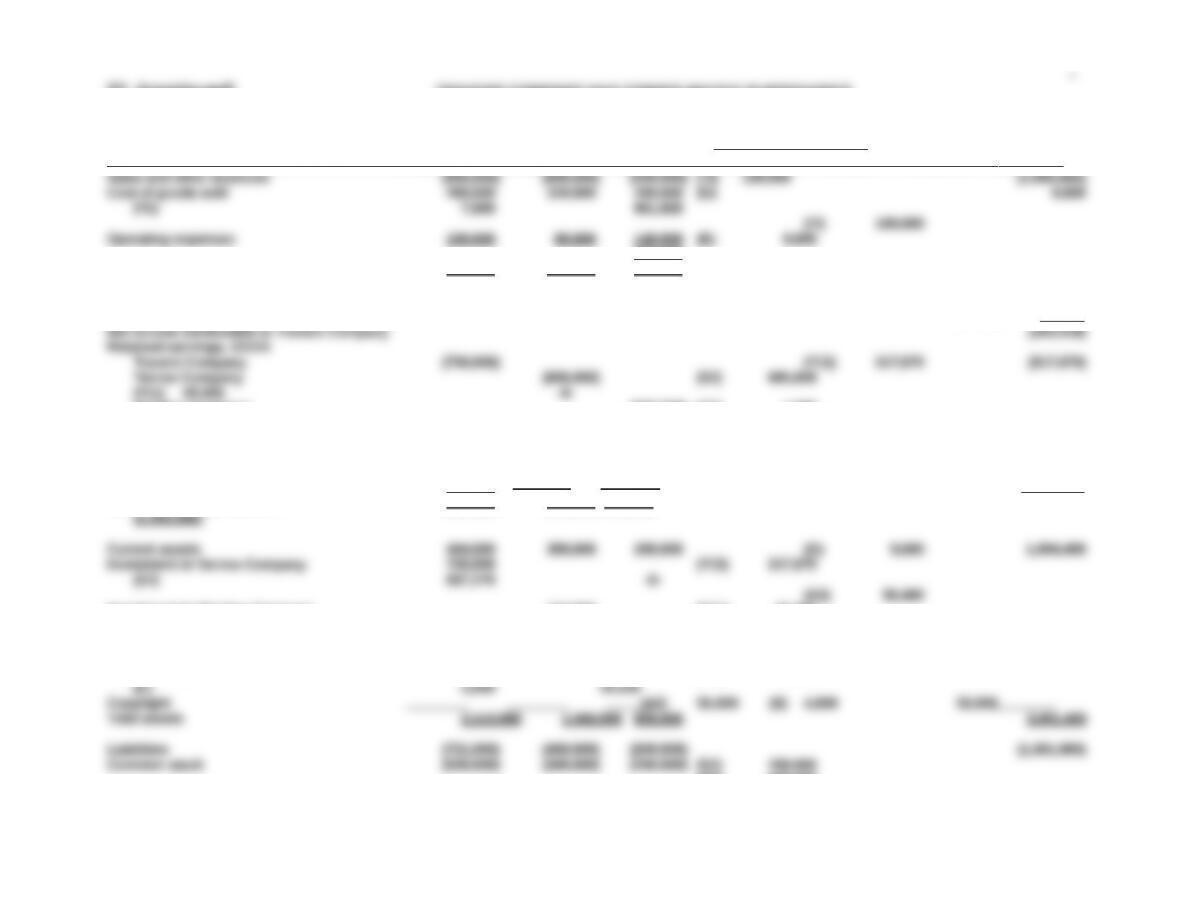

27. (continued) TRAVERS COMPANY AND CONSOLIDATED SUBSIDIARIES

Consolidation Worksheet

December 31, 2014

Travers Yarrow Stookey Consolidation EntriesNoncontrollingConsolidated

Accounts Company Company Company Debit Credit Interest Balances

329 ,000

Separate company net income (320 ,000) (200 ,000) (100 ,000)

Consolidated net income (609,080)

Net income attributable to NCI (Yarrow) (27,046) 27,046

Net income attributable to NCI (Stookey) (18,616) 18 ,616

Stookey Company (300,000) (*G) 7,680

-0-

(S1) 292,320

Net Income (above) (320,000) (200,000) (100,000) (563,418)

Dividends declared 128 ,000 128 ,000

Retained earnings, 12/31/14 (892 ,000) (800 ,000)(400,000)

Investment in Stookey Company 344,000 (*C1) 85,856

(S1) 393,856 -0-

(A1) 36,000

Land, buildings, & equipment (net) 949,000 836,000520,000 2,305,000

Customer list (A1) 45,000

(S2) 300,000

(500,000)

Retained earnings, 12/31/14 (above) (892,000) (800,000) (400,000) (S1) 98,464 (1,353,088)

NCI interest in Stookey, 1/1/14 (A1) 9,000 (107,464)

(S2) 98,586

27.(continued)

b. Travers’ reported pre-tax income ……………..………..………..………..……. $320,000

Yarrow’s reported pre-tax income ………..………..………….….…..….….… 200,000

Dividend income (none collected) ………………..………..…………….….…. -0-

c. Stookey’s reported pre-tax income …………………………..….….…..….…. $100,000

(Unrealized gains are not deferred on a separate

tax return.)

Tax rate …….………..………..………..………..………..…………….….….….…..…. 45%

Income tax payable ………….…………………..……………..…..….….….…..…. $45,000

d. (1) Because Yarrow owns 80% of Stookey’s stock, intra-entity dividends are

2014 Unrealized gross profit taxed in 2014………..…..….….….…..….…. $9,600

2013 Unrealized gross profit taxed previously in 2013….….….…....... (7 ,680)

Increase in taxable income …………..…………………..………..………………. $1,920

Tax rate …….………..………..………..………..………..…………….….….….…..…. 45%

Deterred income tax asset …………..………..………..………..………………... $ 864

Income tax expense 2014…………………..………..………..………..…..…. $274,086

Because a single rate is used, income tax expense can also be computed by

taking consolidated net income (prior to noncontrolling interest reduction) of

$609,080 (part a.) and multiplying by the 45% tax rate to obtain $274,086.

Income tax expense—current ………..…..….….…..….….… 274,086