26. (25 minutes) (Prepare journal entries for a partnership liquidation)

JOURNAL ENTRIES

a. Cash ………………..………..………..………..………………..…. 56,000

March, Capital (2/6 of loss) ……………………..………….. 6,000

April, Capital (3/6) …………..………..………..………….…... 9,000

May, Capital (1/6) ………..………..………….…..…..…..…... 3,000

Inventory ………..…………………..………..…………..….. 74,000

d. Cash ………………..………..………..………..………………..…. 45,000

Accounts Receivable ………….………..………..……… 45,000

e. Current Capital Share of Potential

Partner Adjusted Maximum Loss* Capital

March $16,500 2/6 x $77,000 = $25,667 $ (9,167)

*Maximum losses could be suffered on the remaining $39,000 in accounts

receivable and the $38,000 in land, building, and equipment.

Based on the above potential losses, March would have a deficit capital

balance of $9,167 which in turn has to be allocated to the two partners having

positive capital balances:

Potential Capital Share of Potential

Partner (above) March’s Deficit Capital

26. (continued)

As the above amounts represent safe capital balances, payments can be

presently made to these two partners.

April, Capital ………….………..…………………..…..…..…... 16,875

f. Cash (30%) …………………..………..……………..…..…..….. 11,700

March, Capital (2/6 of loss) ……………………..………….. 9,100

April, Capital (3/6)……………………..………..………….…... 13,650

May, Capital (1/6)…………………..…………….…..…..…..… 4,550

Accounts Receivable ………….………..………..……… 39,000

h. Liabilities ………..………..………..………………………….….. 21,000

Cash ………………..………..……………..…..…..…..…..… 21,000

i. Since $28,700 cash remains and each partner has a positive capital balance,

the money left can be distributed based on these ending totals.

27.(30 minutes) (Determine liquidation proceeds necessary to give partner a

specified amount; predistribution plan)

Answer: For Z to be able to pay his personal creditor $5,000 from the

distribution of partnership property, the partnership’s other assets must be

sold for at least $50,000.

$27,000 in cash above the current level must first be generated for creditors

and liquidation expenses. Based on the predistribution schedule below, the

A predistribution plan must be developed to generate this information:

W X Y Z

Beginning capital $ 60,000 $ 78,000 $ 40,000 $ 30,000

Assumed loss of $120,000 (see

Schedule 1) (5:3:1:1) (60 ,000) (36 ,000) (12 ,000) (12 ,000)

Schedule 1

Capital Balance/ Maximum Loss to

Partner Loss Allocation Be Absorbed

W $60,000/50% $120,000 (most vulnerable)

27. (continued)

Schedule 2

Capital Balance/ Maximum Loss to

Partner Loss Allocation Be Absorbed

X $42,000/(3/5) $ 70,000 (most vulnerable)

Schedule 3

Capital Balance/ Maximum Loss to

Partner Loss Allocation Be Absorbed

PREDISTRIBUTION PLAN

Current cash of $30,000 goes to creditors.

Next $27,000 generated goes to remaining creditors ($12,000) and to pay

liquidation expenses estimated at ($15,000).

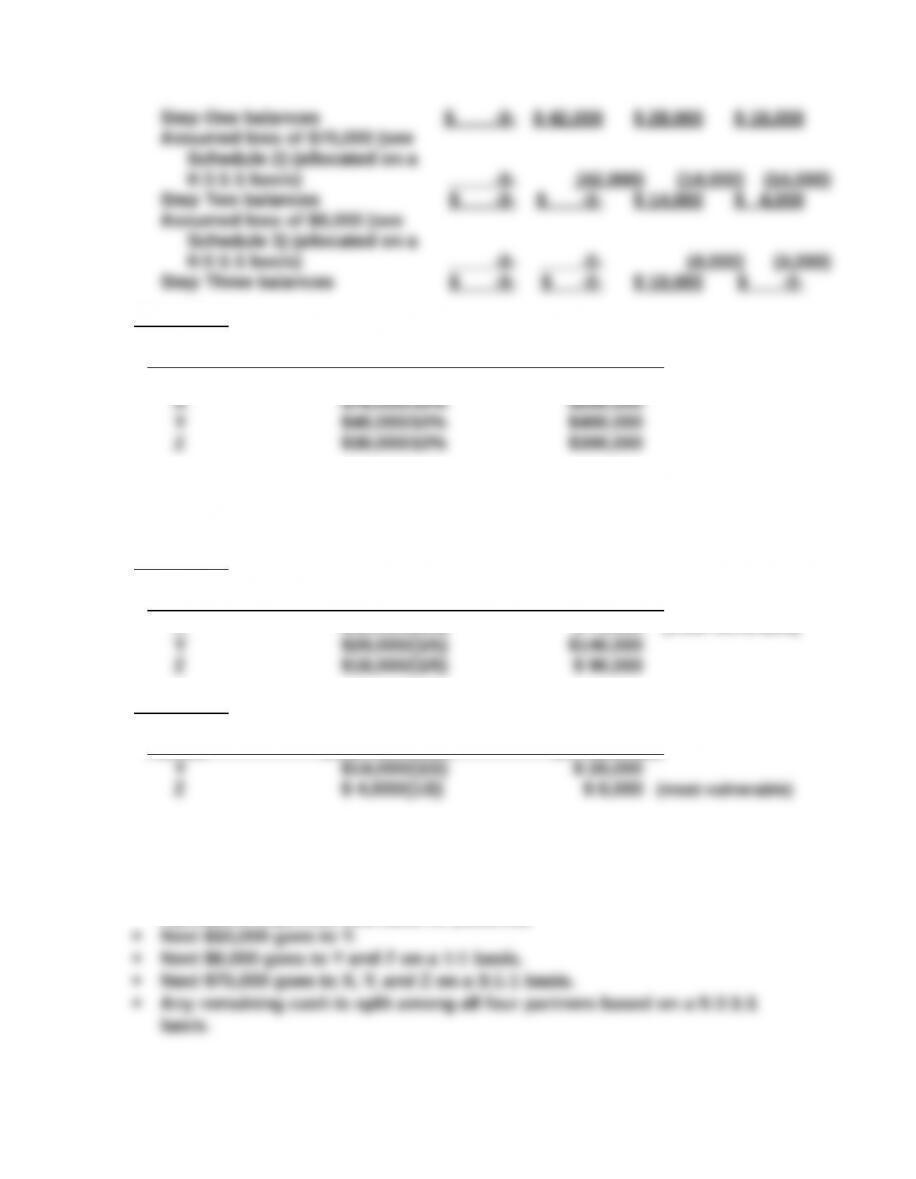

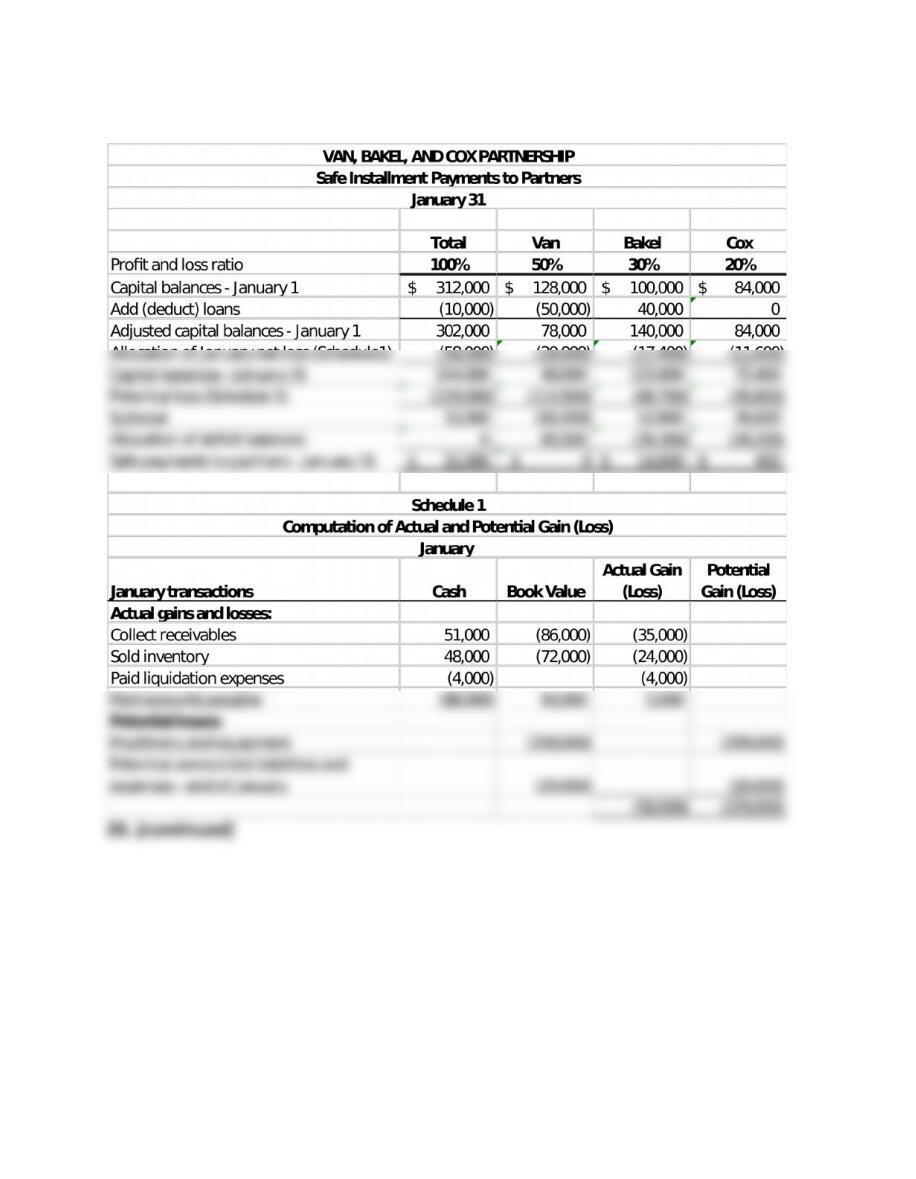

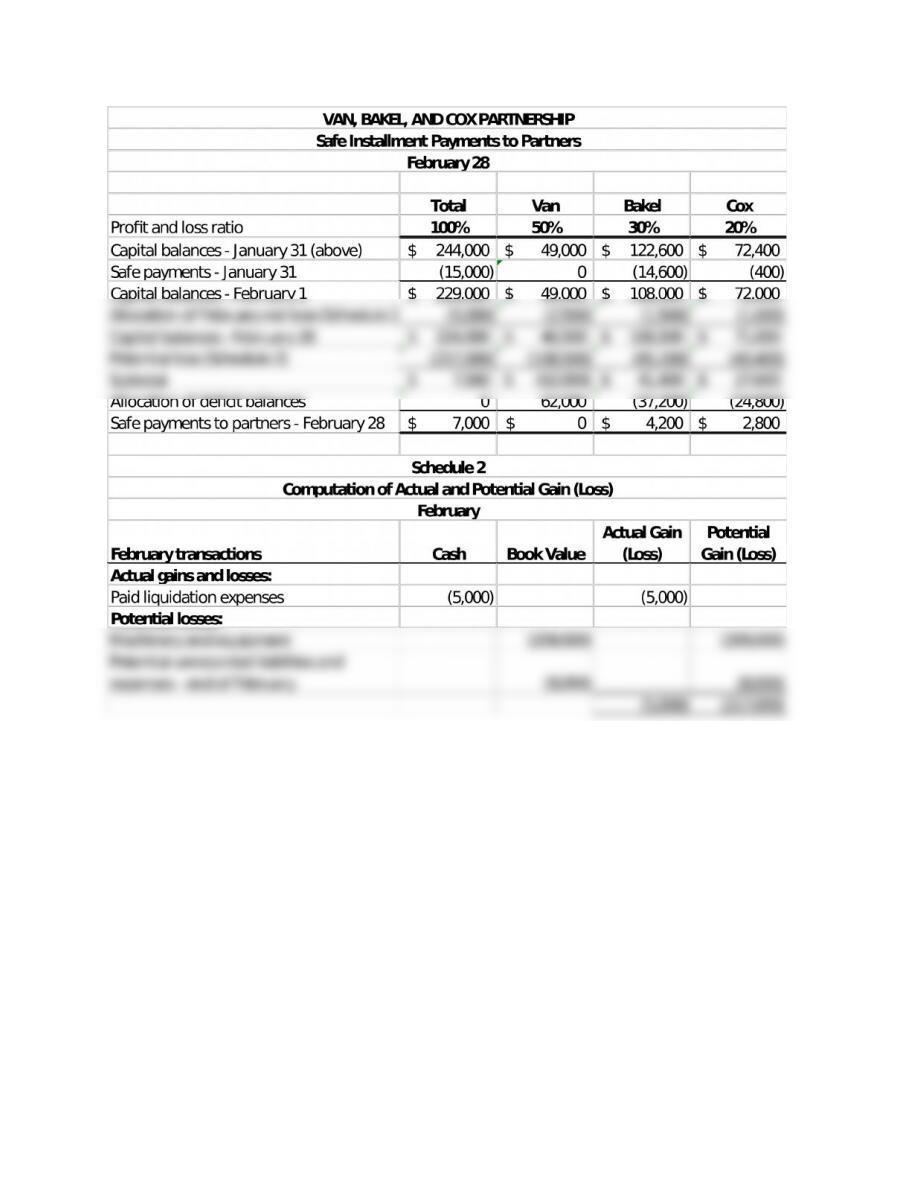

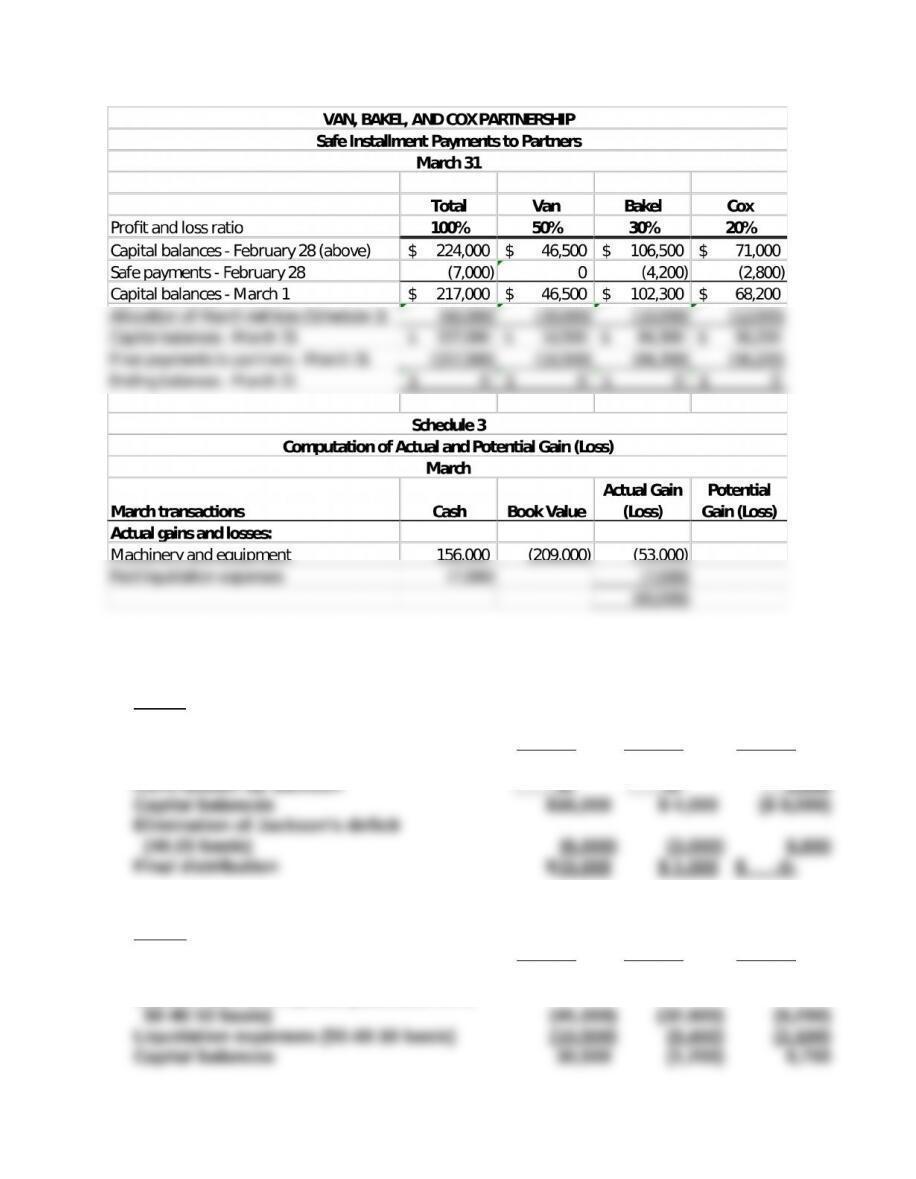

28. (35 minutes) (Determine monthly safe installment payments to partners)

28. (continued)

29. (35 minutes) (Determine cash distributions for four different partnership

liquidations; insolvent partners)

Part A Haynes,

Simon, Loan and Jackson,

Capital Capital Capital

Beginning balances $16,000 $ 4,000 ($12,000)

Contribution by Jackson – 0 – – 0 – 3 ,000

Hough, Luck,

Part B Loan and Loan and Cummings,

Capital Capital Capital

Beginning balances $82,000 $40,000 $20,000

$82,000 loss on disposal (allocated on a

Final distribution $29 ,500 $ – 0 – $ 9 ,500

Hough, Luck,

Part C Loan and Loan and Cummings,

Capital Capital Capital

Beginning balances $82,000 $40,000 $20,000

$82,000 loss on disposal (allocated on a

Allocation of Cummings’ deficit balance

(2:4 basis) (5 ,067) (10 ,133) 15 ,200

Capital balances $59,333 ($ 5,333) -0-

Allocation of Luck’s deficit balance (5 ,333) 5 ,333 – 0 –

Final distribution $54 ,000 $ – 0 – $ – 0 –

29. (continued)

Part D

Redmond,

Loan and Ledbetter, Watson, Sandridge,

Capital Capital Capital Capital

Beginning balances ($16,000) ($30,000) $ 3,000 $15,000

Allocation of Redmond’s

deficit balance (10:30:40

$32,000 contribution by

Ledbetter and $3,000 con-

tribution by Watson – 0 – 32,000 3,000 – 0 –

Final distribution* $ – 0 – $ – 0 – $ – 0 – $ 7,000

*Remaining $28,000 is used to pay liabilities.

30. (60 minutes) (Prepare a predistribution plan, a final statement of liquidation,

and journal entries for a partnership liquidation)

Part A Preparation of Predistribution Plan

Schedule 1

Maximum Loss

Capital Balance/ That Can

Partner Loss Allocation Be Absorbed

Frick $129,000/60% $215,000

Schedule 2

Maximum Loss

Capital Balance/ That Can

Partner Loss Allocation Be Absorbed

Schedule 3

Frick, Wilson, Clarke,

Capital Capital Capital

Beginning balances ……….….…..…..…..… $129,000 $35,000 $75,000

Loss of $175,000 assumed—Schedule 1

(allocated on a 60:20:20 basis) ........... (105 ,000) (35 ,000) (35 ,000)

Step One balances ………………..…..….….. 24,000 -0- 40,000

Loss of $32,000 assumed—Schedule 2

PREDISTRIBUTION PLAN

First, payment of liabilities and liquidation expenses must be assured.

Next $32,000 goes to Clarke.

30. (continued)

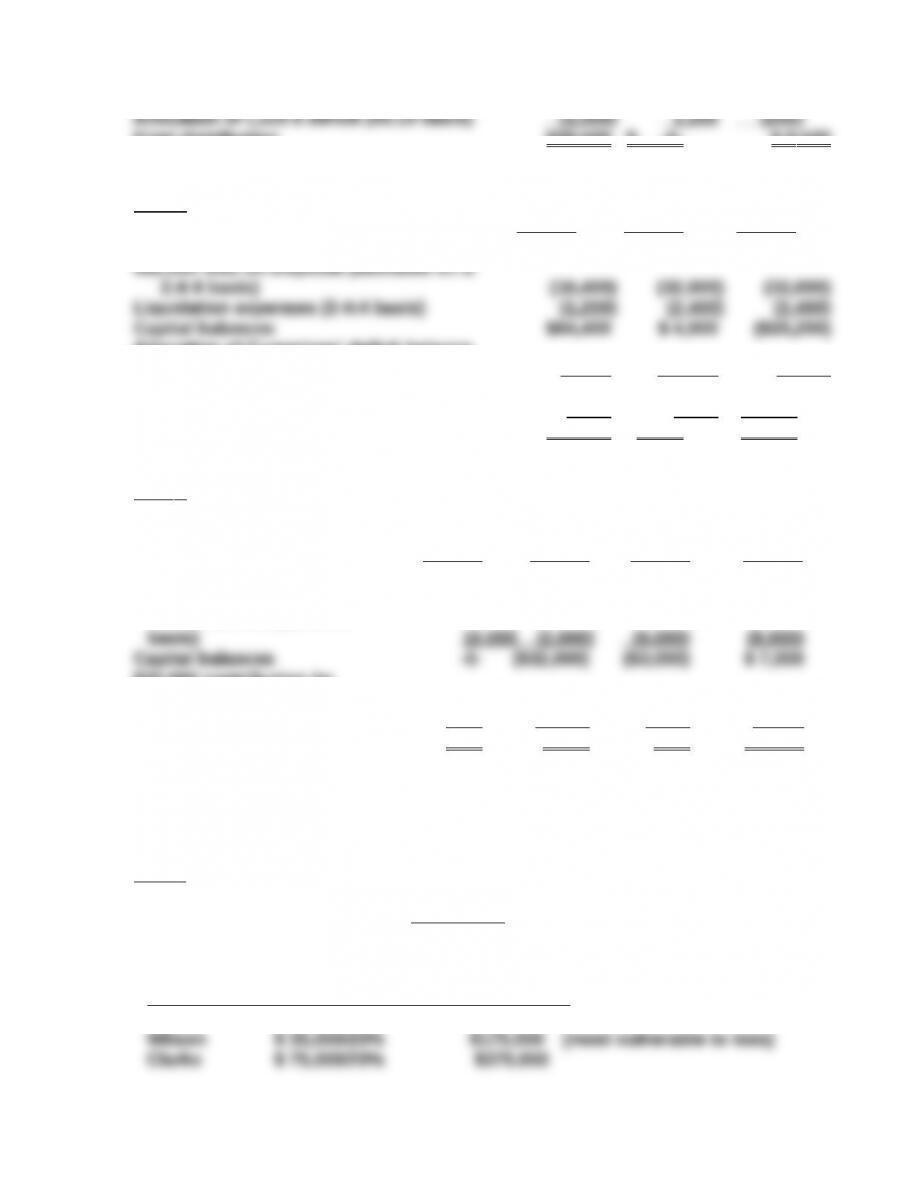

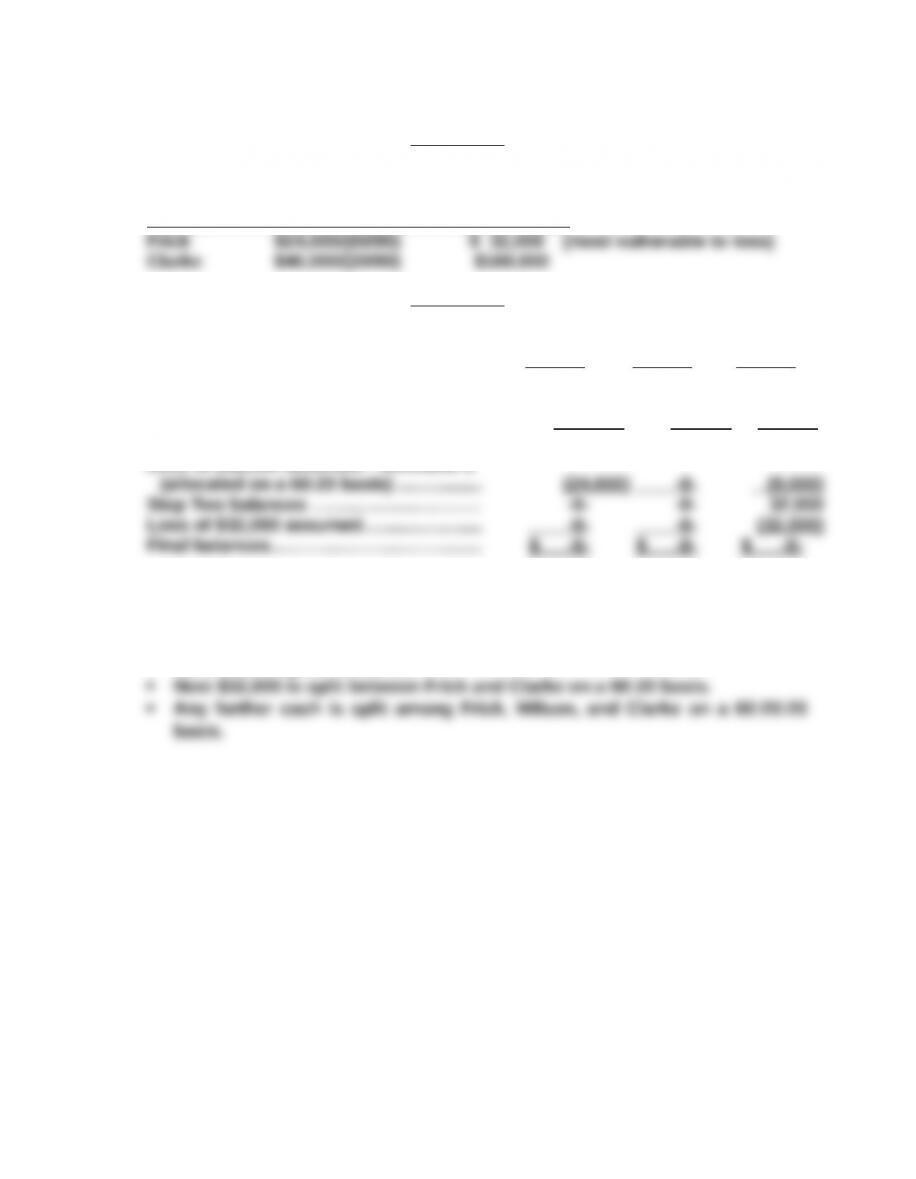

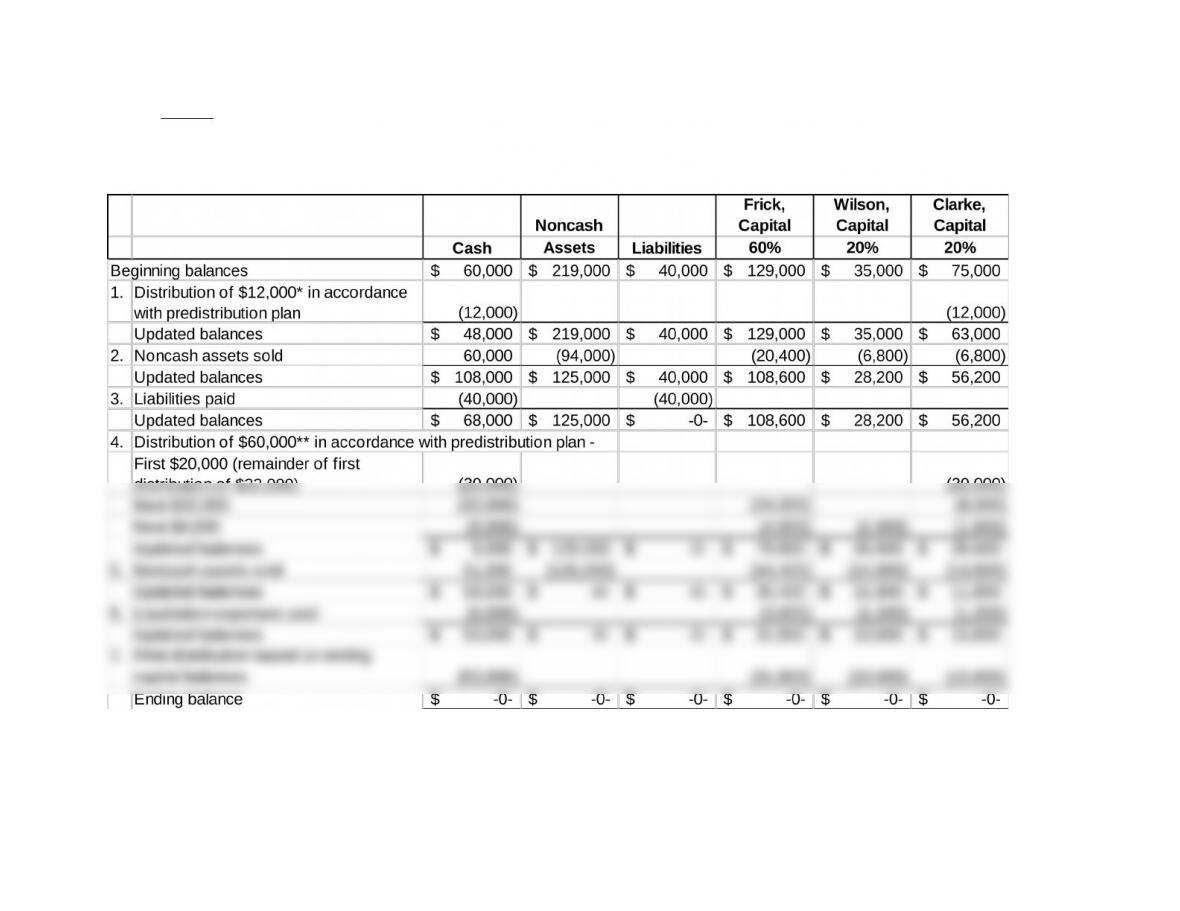

Part B Preparation of Final Statement of Partnership Liquidation

FRICK, WILSON, AND CLARKE

Statement of Partnership Liquidation

Final Balances

* $12,000 in cash is immediately available for distribution: Cash of $60,000 less

Liabilities of $40,000 and Estimated Liquidation Expenses of $8,000.

** $60,000 in cash is available for distribution: Cash of $68,000 less Estimated

Liquidation Expenses of $8,000.

30. (continued)

Part C Journal Entries

1. Clarke, Capital …………………………………………………………. 12,000

Cash ……………………………………………..……………… 12,000

Cash payments are made to partners in accordance

with predistribution plan.

2. Cash ……………………………………………………………………… 60,000

Frick, Capital (60% of $34,000 loss) …............................. 20,400

3. Liabilities……………………………………………………..…………. 40,000

Cash ……………………………………………..……………… 40,000

All liabilities are paid.

5. Cash ……………………………………………………………………..... 51,000

Frick, Capital (60% of $74,000 loss) …............................. 44,400

6. Frick, Capital …………………………………………….…………….. 3,600

Wilson, Capital …………………………………………….………….. 1,200

Clarke, Capital …………………………………………………………. 1,200

Cash ……………………………………………..……………… 6,000

Liquidation expenses are paid.

7. Frick, Capital …………………………………………….…………….. 31,800

Wilson, Capital …………………………………………….………….. 10,600