Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

CHAPTER 10

TRANSLATION OF FOREIGN

CURRENCY FINANCIAL STATEMENTS

Chapter Outline

I. In today's global economy, many companies have invested in operations in foreign

countries.

A. In preparing consolidated financial statements on a worldwide basis, the foreign

currency accounts prepared by foreign operations must be restated into the parent

company's reporting currency.

B. There are two major issues related to the translation of foreign currency financial

statements.

1. Which method should be used?

2. How should the resulting translation adjustment be reported on the consolidated

financial statements?

C. Translation methods differ on the basis of which accounts are translated at the current

exchange rate and which are translated at a historical exchange rate. Translating

accounts at the current exchange rate creates a translation adjustment.

D. Historically, accountants have experimented with a number of different translation

methods. The dominant methods currently in use are the temporal method and the

current rate method.

E. Translation adjustments can be either (1) reported as a gain or loss in income or (2)

deferred in the stockholders' equity section of the balance sheet.

II. The primary objective of the temporal method is to maintain the underlying valuation method

used by the foreign entity to account for its assets and liabilities.

A. Assets and liabilities carried at current or future value are translated at the current

exchange rate. Assets and liabilities carried at cost and stockholders' equity items are

translated at a historical exchange rate.

B. By translating some assets at the current exchange rate and others at historical rates the

temporal method distorts financial ratios calculated in the foreign currency.

C. Most income statement items are translated at average-for-the-period rates. However,

cost-of-goods-sold, depreciation, and amortization expense are translated at relevant

historical exchange rates.

D. Balance sheet exposure under the temporal method is defined as cash, marketable

securities, and receivables minus total liabilities. A net liability exposure often exists.

1. When a liability balance sheet exposure exists, depreciation of the foreign currency

results in a positive translation adjustment (gain) and appreciation of the foreign

currency results in a negative translation adjustment (loss).

2. Reporting a translation loss when the foreign currency appreciates is thought to be

inconsistent with economic reality.

III. With the current rate method, the net investment in a foreign operation is considered to be

exposed to foreign exchange risk.

A. Assets and liabilities are translated at the current exchange rate; equity is translated at

historical rates.

B. Translating assets which are carried at cost using the current exchange rate results in a

translated value which is not readily interpretable; it is neither a current value nor a

historical cost.

C. However, translating all assets at the current rate does maintain underlying ratios and

relationships that exist in the foreign currency statements.

D. Revenues and expenses which occur evenly throughout the period are translated at the

average-for-the-period exchange rate. Income items, such as gains and losses, which

are the result of a discrete event, are translated at the actual exchange rate on the date

of occurrence.

E. Balance sheet exposure under the current rate method is equal to the foreign entity's net

assets (stockholders' equity).

1. Appreciation in the foreign currency results in a positive translation adjustment

(gain); depreciation results in a negative translation adjustment (loss).

IV. FASB Accounting Standards Codification Topic 830, Foreign Currency Matters, (FASB ASC

830) provides guidelines for the translation of foreign currency financial statements by U.S.-

based multinational corporations. The appropriate translation method and disposition of

translation adjustment depends upon the functional currency of the foreign entity.

A. The functional currency is the primary currency of the foreign entity's operating

environment. It can be either the U.S. dollar or a foreign currency.

1. U.S. GAAP lists six indicators that are to be used in determining an entity's functional

currency. There are no guidelines as to how these indicators are to be weighted.

B. If a foreign currency is the functional currency, the foreign entity's financial statements

are "translated" using the current rate method and the resulting translation adjustment is

reported as a separate component of equity. The average-for-the-period exchange rate

is used to translate the foreign entity's income statement.

1. Upon the sale or liquidation of a specific foreign entity, the cumulative translation

adjustment related to that entity is taken to income as an adjustment to the gain or

loss on sale or liquidation.

C. If the U.S. dollar is the functional currency, foreign currency financial statements are

"remeasured" using the temporal method with "remeasurement" gains and losses

reported in operating income.

D. If a foreign entity operates in a highly inflationary economy (cumulative three-year

inflation greater than 100%), its financial statements are remeasured into U.S. dollars

using the temporal method and remeasurement gains and losses are reported in

income.

V. Some companies hedge the balance sheet exposures of their foreign entities so as to avoid

adverse effects on income and/or stockholders' equity.

A. FASB Accounting Standards Codification Topic 815, Derivatives and Hedging (FASB

ASC 815) refers to this as a hedge of a net investment in a foreign operation and

stipulates that gains and losses on hedging instruments used in this manner should be

treated in the same fashion as the translation adjustment (remeasurement gain/loss)

being hedged.

B. The paradox of hedging balance sheet exposure is that by avoiding a translation

adjustment (remeasurement gain/loss), realized foreign exchange gains and losses can

arise.

Answer to Discussion Question: How Do We Report This?

This case represents the ongoing debate as to the proper reporting of foreign currency

balances. Southwestern has invested the equivalent of $30,000 (150,000 vilseks) in each of

three assets. The relative value of the vilsek has now changed. Thus, 150,000 vilseks now can

be converted into $34,500. However, the subsidiary does not have vilseks--only land, inventory,

Conversely, the current rate method requires that each of the three assets be reported at

$34,500 based on the current exchange rate. As the controller indicates, though, $34,500 was

not the original cost expended by Southwestern. In addition, using the current rate means that

As a classroom exercise or written assignment, students could be required to select a reported

value for each of the three assets and then defend their position. What figure is actually the

fairest representation of each of the three assets? What figure is the best conveyor of

information to an outside party? There is no single best answer to these questions. The

The temporal and current rate methods of translation differ primarily with regard to the exchange

rate used to translate those assets that are reported at historical cost--inventories, prepaids,

Answers to Questions

1. The two major issues related to the translation of foreign currency financial statements are:

(a) which method should be used and (b) where should the resulting translation adjustment

be reported in the consolidated financial statements. The first issue relates to determining

2. Balance sheet exposure arises when a foreign currency balance is translated at the current

exchange rate. By translating at the current exchange rate, the foreign currency item in

essence is being revalued in U.S. dollar terms on the consolidated financial statements.

3. Although balance sheet exposure does not result in cash inflows and outflows, it does

nevertheless affect amounts reported in consolidated financial statements. If the foreign

currency is the functional currency, translation adjustments will be reported in stockholders’

equity. If translation adjustments are negative and therefore reduce total stockholders’

share.

The paradox in hedging balance sheet exposure is that, by agreeing to receive or deliver

foreign currency in the future under a forward contract, a transaction exposure is created.

4. The gains and losses arising from financial instruments used to hedge balance sheet

exposure are treated in a similar manner as the item the hedge is intended to cover. If the

5. The major concept underlying the temporal method is that the translation process should

result in a set of translated U.S. dollar financial statements as if the foreign subsidiary’s

transactions had actually been carried out using U.S. dollars. To achieve this objective,

assets carried at historical cost and stockholders’ equity are translated at historical

exchange rates; assets carried at current value and liabilities (carried at current value) are

investment.

6. The Retained Earnings balance is created by a multitude of transactions: all revenues,

expenses, gains, losses, and dividends since the company’s inception. Identifying each

7. The major differences relate to non-monetary assets carried at historical cost and related

expenses, i.e., inventory and cost of goods sold; property, plant, and equipment and

8. The functional currency is the currency of the subsidiary’s primary economic environment. It

is usually identified as the currency in which the company generates and expends cash.

9. The foreign subsidiary's net asset position in foreign currency at the beginning of the period

is first determined. Changes in net assets are determined to explain the net asset balance

in foreign currency at the end of the period. The beginning net asset position and changes

in net assets are translated at appropriate exchange rates and the ending net asset position

in dollars is determined.

10. One theory mentioned by the FASB identifies the translation adjustment as a measure of

unrealized increases and decreases that have occurred in the value of the foreign subsidiary

11. Translation is required when a foreign currency is the functional currency. Remeasurement

is required in two situations:

a. The U.S. dollar is the functional currency.

12. The temporal method must be used to remeasure the financial statements of operations in

highly inflationary countries. One reason for mandating the use of the temporal method is

13. Differences exist between IFRS and U.S. GAAP with regard to (a) the hierarchy of factors

used to determine the functional currency and (b) the method used to translate the financial

statements of a subsidiary located in a hyperinflationary country.

IAS 21 establishes primary factors and other factors to be considered in determining an

no adjustment for inflation in this situation.

Answers to Problems

1. C (Definition of functional currency)

4. B (Determine appropriate translation method and resulting translation

adjustment)

5. A (Translation process (current rate method) – asset and related expense)

All asset accounts are translated at current rates.

8. A (Remeasurement process (temporal method) – inventory)

9. A (Remeasurement process (temporal method) – cost of goods sold)

10. D (Translation process (current rate method) – marketable securities and

inventory)

The foreign currency is the functional currency, so a translation is

appropriate. All assets are translated at the current exchange rate of $.19.

13. C (Calculation of translation adjustment)

Beginning net assets, 1/1………….. P20,000 x $.15 = $ 3,000

Increase in net assets:

Net income.................................. 10,000 x $.19 = 1 ,900

14. C (Concepts underlying current rate and temporal methods)

by the foreign subsidiary.

15. A (Calculation of remeasurement gain/loss)

Beginning net monetary assets, 1/1 P100,000 x $.16 = $16,000

Increases in net monetary assets:

Sale of inventory......................... 50,000 x $.20 = 10,000

Decreases in net monetary assets:

16. C (Remeasurement process (temporal method))

17. B (Determine appropriate translation method and treatment of translation

adjustment)

losses reported in income.

18. B (Translation process (current rate method) – wages expense and wages

payable)

19. C (Treatment of gains and losses on hedges of net investments)

21. (10 minutes) (Specify appropriate exchange rates for the translation of

foreign currency financial statements under the current rate method)

Sales—use actual (historical) rate at time of recording. Sales often occur

evenly throughout the year so that an average rate is acceptable. However, if

sales are more prevalent at a particular time during the year, historical rates

should be used.

change rate at the balance sheet date.

21. (continued)

22. (5 minutes) Determine Translated Values under the Current Rate Method

As a translation, both the asset (inventory) and the liability (accounts

payable) utilize the current exchange rate at the balance sheet date

(December 31). Thus, the translated values are as follows:

23. (10 minutes) (Determine appropriate exchange rates under the current rate

method [translation] and temporal method [remeasurement])

Translation Remeasurement

Accounts payable $.16 C $.16 C

Accounts receivable $.16 C $.16 C

Accumulated depreciation $.16 C $.26 H

Dividends (10/1) $.20 H $.20 H

Notes payable $.16 C $.16 C

Patents (net) $.16 C $.25 H

* C = current rate, H = historical rate, A = average rate

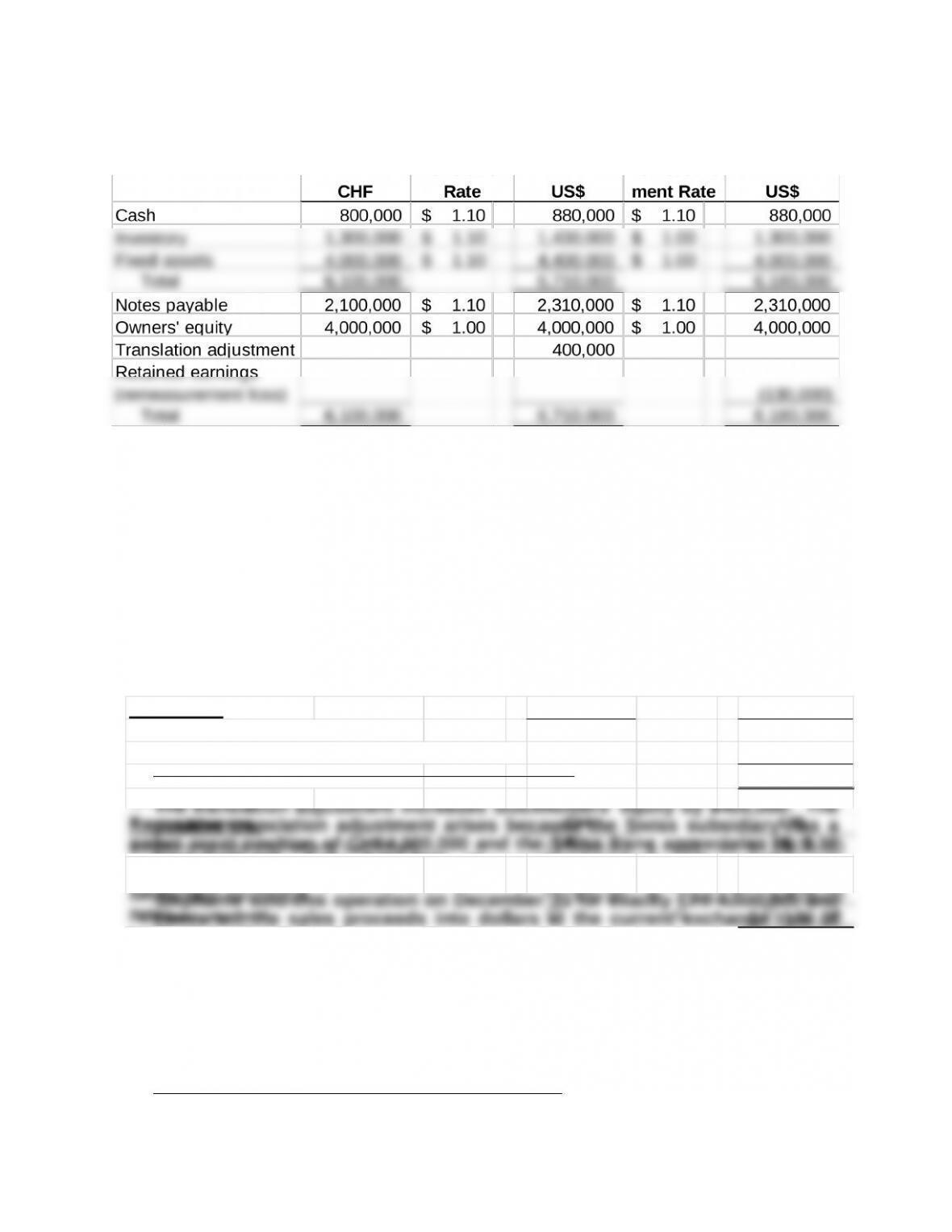

24. (20 minutes) (Calculate translation adjustment and remeasurement gain/loss

and explain their economic relevance)

Translatio

n

CH

F

US

$

Beginning net assets,

12/18

4,000,0

00

1.0

0

$

H 4,000,0

00

$

Ending net assets, 12/31 at current

exchange rate

4,000,0

00

1.1

0

$

C 4,400,0

00

Translation adjustment

(positive)

(400,00

0)

$

loss

0

The translation adjustment and remeasurement gain/loss can be determined

as the plug figure that keeps the dollar balance sheet in balance:

Alternatively, the translation adjustment and remeasurement loss can be

calculated by analyzing the subsidiary’s balance sheet exposure:

Economic Relevance of Translation Adjustment

$1.10 per Swiss franc.

24. (continued)

Economic Relevance of Remeasurement Loss

The remeasurement loss arises because the Swiss subsidiary has a net

monetary liability position of CHF1,300,000 (Cash of CHF800,000 less Notes

payable of CHF2,100,000) and the Swiss franc has appreciated by $.10