Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

30. (65 Minutes) (Consolidated totals and worksheet five years after

acquisition. Parent uses equity method. Includes goodwill impairment.)

a. Acquisition-date fair value allocations (given) Remaining Annual excess

life

amortizations

Land $90,000 -- --

earnings) less $5,000 in amortization expense computed above.

b.

Revenues = $1,535,000 (both balances are added together)

Cost of goods sold = $640,000 (both balances are added)

Depreciation expense = $307,000 (both balances are added along with

excess equipment depreciation)

subsidiary's dividends are intra-entity)

Retained earnings, 12/31/15 = $1,695,000 (the parent’s balance at

beginning of the year plus consolidated net income less consolidated

dividends declared)

Equipment = $959,000 (both book balances are added plus the

30. b. (continued)

Goodwill = $60,000 (represents the original acquisition-date

allocation)

Total assets = $3,143,000 (summation of all consolidated assets)

b. Worksheet is presented on following page.

c. If all goodwill from the Small investment was determined to be impaired,

Giant would make the following journal entry on its books:

Investment in Small 60,000

After this entry, the worksheet process would no longer require an

30. c. (continued)

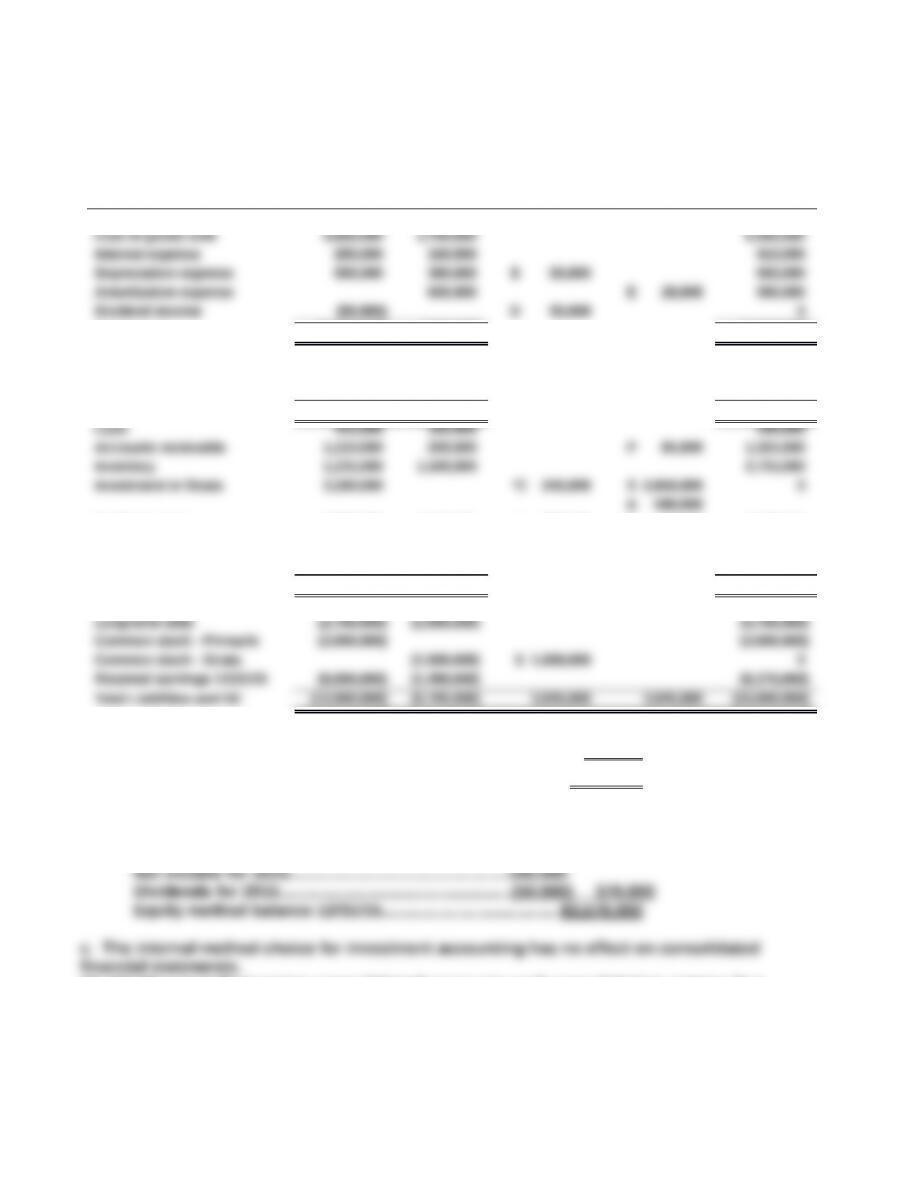

GIANT COMPANY AND SMALL COMPANY

Consolidation Worksheet

For Year Ending December 31, 2015

Consolidation Entries Consolidated

Accounts Giant Small Debit Credit Totals

Revenues............................................................. (1,175,000) (360,000) (1,535,000)

Cost of goods sold.............................................. 550,000 90,000 640,000

Depreciation expense......................................... 172,000 130,000(E) 5,000 307,000

Net income (above)............................................. (588,000) (140,000) (588,000)

Dividends declared............................................. 310 ,000 110 ,000 (D) 110,000 310 ,000

Retained earnings 12/31............................... (1 ,695,000) (650 ,000) (1 ,695,000)

Buildings (net)..................................................... 304,000 419,000 723,000

Equipment (net)................................................... 648,000 286,000(A) 30,000 (E) 5,000 959,000

Goodwill............................................................... -0- -0- (A) 60,000 60 ,000

Total assets.................................................... 2 ,785,000 1 ,188,000 3 ,143,000

Liabilities.............................................................. (840,000) (368,000)(P) 10,000 (1,198,000)

31. (45 Minutes) (Consolidated totals and worksheet two years after acquisition.

Parent uses initial value method. Includes question comparing initial value

and equity methods).

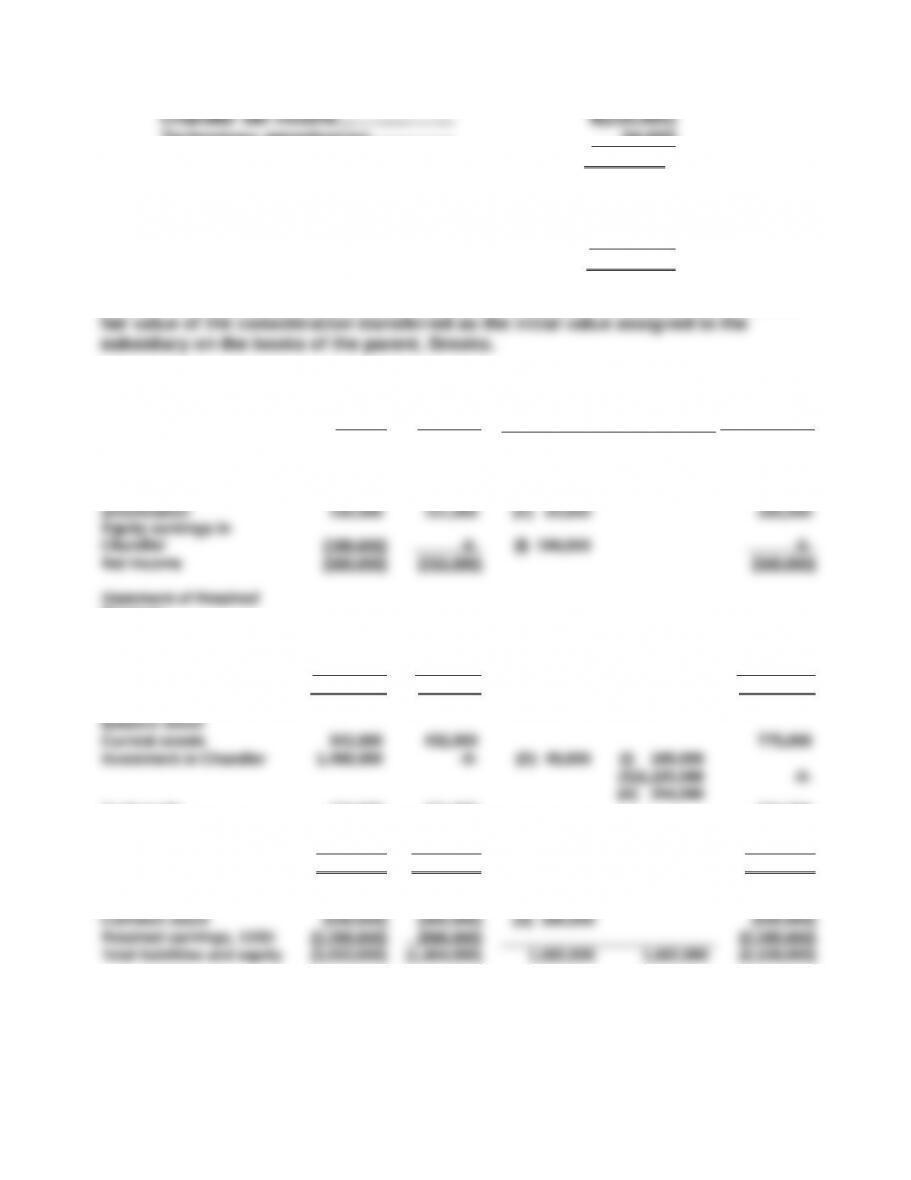

a. 12/31/2015 Pinnacle Strata Adjustments and Eliminations Consolidated

Sales (7,000,000) (3,000,000) (10,000,000)

Net Income (1,560,000) (190,000) (1,690,000)

Retained earnings 1/1/15 (5,000,000) (1,350,000) S 1,350,000 *C 240,000 (5,240,000)

Net income (1,560,000) (190,000) (1,690,000)

Dividends declared 560,000 50,000 D 50,000 560,000

Retained earnings 12/31/15 (6,000,000) (1,490,000) (6,370,000)

Buildings (net) 5,572,000 2,040,000 A 270,000 E 30,000 7,852,000

Licensing agreements 1,800,000 E 20,000 A 80,000 1,740,000

Goodwill 350,000 A 400,000 750,000

Total Assets 12,000,000 5,705,000 15,000,000

Accounts payable (300,000) (715,000) P 85,000 (930,000)

b. Subsidiary income (190,000 – 10,000).......................................$180,000

1/1/15 retained earnings (5,000,000 + 240,000).....................$5,240,000

Investment in Strata:

Initial value basis ..............................................................$3,200,000

Conversion to equity as of 1/1/15.........................240,000

32.(30 Minutes) (Determine consolidated accounts and consolidation entries five

years after acquisition. Parent applies equity method.)

a. Fair value allocation and annual amortization

Remaining Annual excess

Allocation life amortizations

CONSOLIDATED TOTALS

Revenues = $850,000 (add the two book values)

Cost of goods sold = $380,000 (the accounts of both companies are added

together)

Depreciation expense = $179,000 (the accounts are added and include the

excess depreciation net adjustment of $9,000)

b. The method used by the parent is only important in determining the parent's

separate account balances (which are given here or are not needed) or

consolidation worksheet entries (which are not required in a.)

32. (continued)

c. Consolidation entry S

Common stock (Hill) ............................. 40,000

Additional paid-in capital (Hill) ............ 160,000

Retained earnings 1/1 .......................... 600,000

Customer list (net) ................................ 80,000

Buildings (net) ................................. 18,000

Investment in Hill ............................ 94,000

(To recognize unamortized allocation balances as of beginning of

current year)

of $14,000 for the year)

Consolidation entry D

Investment in Hill .................................. 40,000

Dividends declared ......................... 40,000

(To remove Intra-entity dividend declarations)

Customer list.................................... 5,000

(To recognize excess acquisition-date fair-value amortizations for

the period)

33. (30 Minutes) (Determine parent company and consolidated account

balances for a bargain purchase combination. Parent applies equity

method)

a. Acquisition-date fair value allocation and annual excess amortization

Consideration transferred ............. $1,183,000

Technology amortization................. 34,000

Equity earnings in Chandler........... $(199,000)

Fair value of net assets at acquisition-date $1,309,000

Equity earnings from Chandler...... 199,000

Dividends declared.......................... (40,000)

Investment in Chandler 12/31/15.... $1,468,000

Because a bargain purchase occurred, Chandler’s net asset fair value replaces the

33 continued (part b.)

Income Statement Brooks Chandler Adj. & Elim. Consolidated

Revenues (640,000) (587,000) (1,227,000)

Cost of goods sold 255,000 203,000 458,000

Gain on bargain purchase (126,000) -0- (126,000)

Depreciation and

Earnings

Retained earnings, 1/1 (1,835,000) (805,000) (S) 805,000 (1,835,000)

Net income (above) (560,000) (233,000) (560,000)

Dividends declared 100,000 40,000 (D) 40,000 100,000

Retained earnings, 12/31 (2,295,000) (998,000) (2,295,000)

Trademarks 134,000 221,000 355,000

Patented technology 395,000 410,000 (A) 204,000 (E) 34,000 975,000

Equipment 693,000 341,000 1,034,000

Total assets 3,033,000 1,404,000 3,139,000

Liabilities (203,000) (106,000) (309,000)

34. (35 minutes) (Contingent performance obligation and worksheet adjustments

for equity and initial value methods.)

a. Investment in Wolfpack, Inc. 500,000

Contingent performance obligation 35,000

Cash 465,000

b.

Cash 50,000

c. Equity Method

Common stock- Wolfpack 200,000

Retained earnings-Wolfpack 180,000

Investment in Wolfpack 380,000

Investment in Wolfpack 35,000

Dividends declared 35,000

Amortization expense 10,000

Royalty agreements 10,000

d. Initial Value Method

34. (continued)

Royalty agreements 90,000

35. (45 Minutes) (Prepare consolidation worksheet five years after acquisition.

Parent applies equity method. Includes question on push-down accounting.)

a. Allocation of Acquisition-Date Fair Value and Determination of

Amortization:

Storm’s acquisition-date fair value ..................... $140,000

Excess assigned to specific accounts: Remaining Annual excess

life amortizations

.......................................................Land $10,000 –

–

Equipment .................................. 5,000 5 yrs. $1,000

The equity in subsidiary earnings reflects the equity method. The initial

value method would have recorded $40,000 (100% of dividend declared)

b. Explanation of Consolidation Entries Found on Worksheet

Entry S—Eliminates stockholders' equity accounts of the subsidiary as

of the beginning of the current year.

Entry A—Recognizes remaining unamortized allocation from

acquisition-date fair value adjustments. As of the beginning of the

current year, equipment and formula have undergone four years of

amortization.

35. (continued) Palm and Subsidiary Consolidated Worksheet for year ended December 31, 2015

Consolidation Entries Consolidated

Accounts Palm Co. Storm Co. Debit Credit Totals

Income Statement

Revenues.......................................................... (485,000) (190,000) (675,000)

Statement of Retained Earnings

Retained earnings 1/1...................................... (659,000) (98,000)(S) 98,000 (659,000)

Net income (above).......................................... (261,000) (68,000) (261,000)

Dividends declared.......................................... 175 ,500 40 ,000 (D) 40,000 175 ,500

Retained earnings 12/31............................. (744 ,500) (126 ,000) (744 ,500)

Land ............................................................... 427,500 58,000(A) 10,000 495,500

Buildings and equipment (net)........................ 713,000 161,000(A) 1,000 (E) 1,000 874,000

Formula............................................................. -0- -0- (A) 16,000 (E) 1,000 15 ,000

Total assets................................................. 1 ,624,500 294 ,000 1 ,727,500

Current liabilities.............................................. (110,000) (19,000) (129,000)

Parentheses indicate a credit balance.

35. (continued)

c. If push-down accounting had been applied, the acquisition-date fair

value allocations to land ($10,000), equipment ($5,000), and formula

($20,000) would have been entered into the subsidiary's balances with