1) A company sells a building to a bank in 2013 at a gain of $100,000 and immediately

leases the building back for period of five years. The lease is accounted for as an

operating lease. The building was originally purchased for $200,000 and currently had a

book value of $50,000 at the date of the sale.

What amount should be recognized as a gain in 2013 using IFRS?

A.$20,000.

B.$50,000.

C.$100,000.

D.$150,000.

E.$200,000.

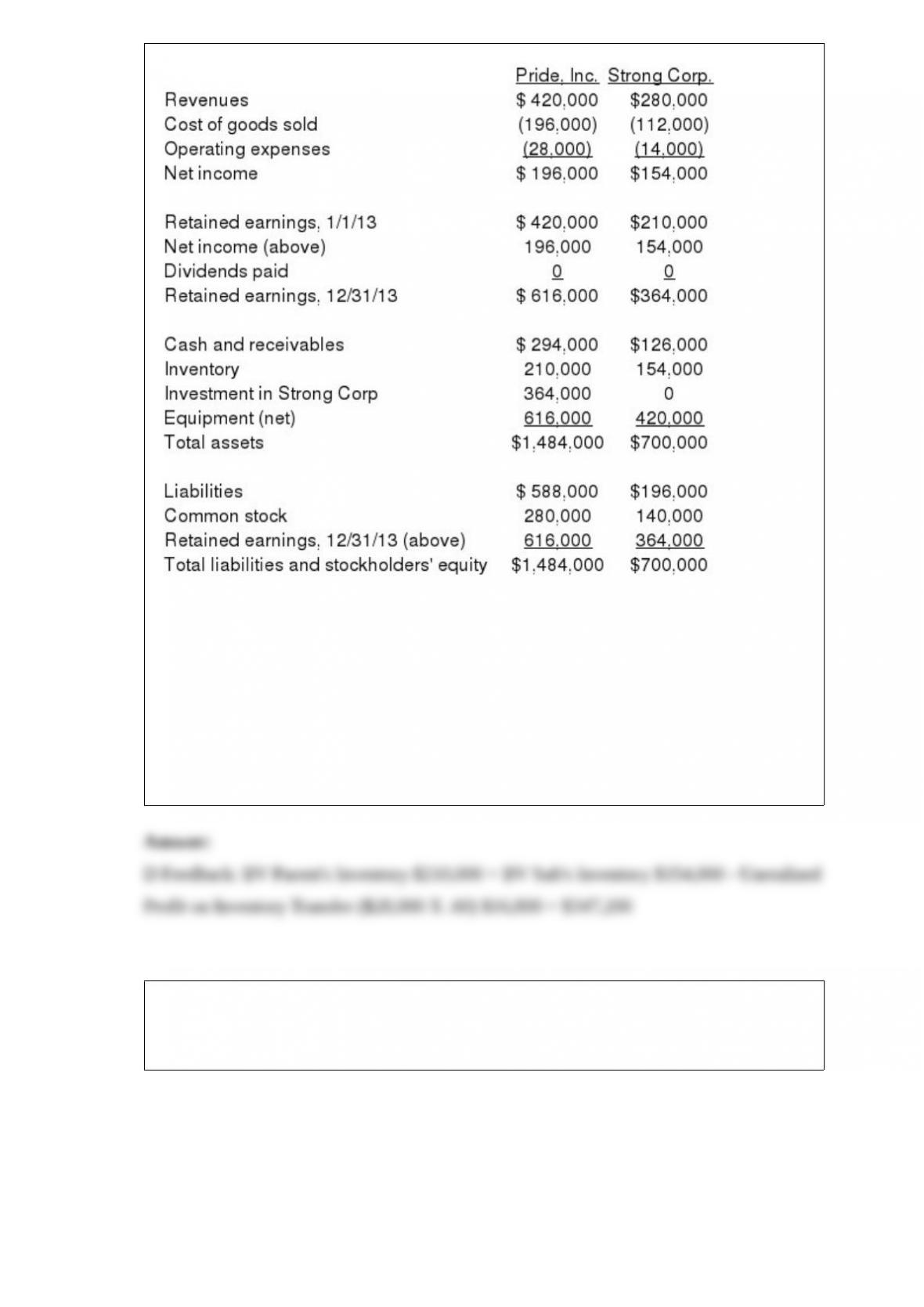

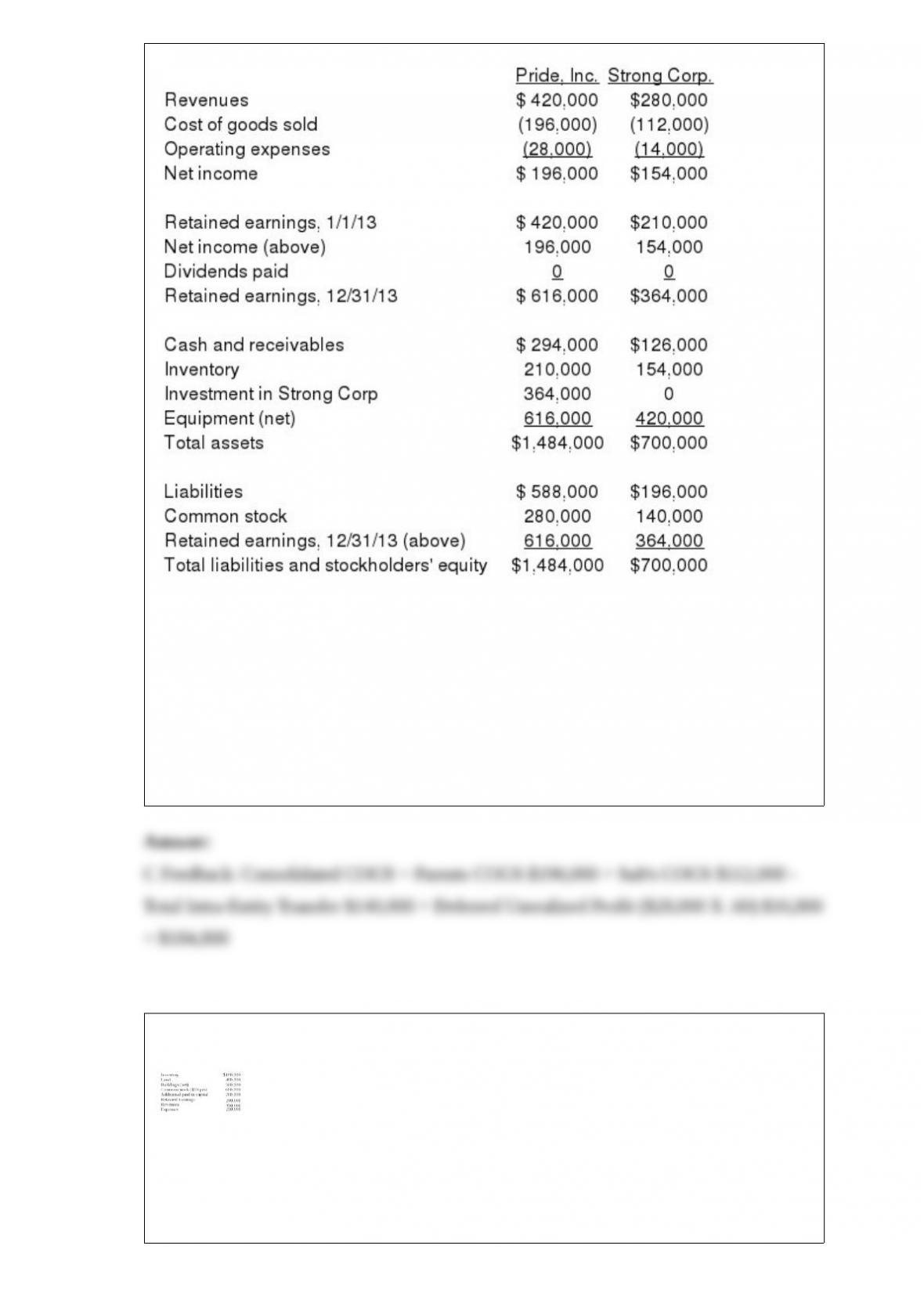

2) On January 1, 2013, Pride, Inc. acquired 80% of the outstanding voting common

stock of Strong Corp. for $364,000. There is no active market for Strong’s stock. Of this

payment, $28,000 was allocated to equipment (with a five-year life) that had been

undervalued on Strong’s books by $35,000. Any remaining excess was attributable to

goodwill which has not been impaired.

As of December 31, 2013, before preparing the consolidated worksheet, the financial

statements appeared as follows:

During 2013, Pride bought inventory for $112,000 and sold it to Strong for $140,000.

Only half of this purchase had been paid for by Strong by the end of the year. 60% of

these goods were still in the company’s possession on December 31, 2013. What is the

consolidated total for inventory at December 31, 2013?

A) $336,000.

B) $280,000.

C) $364,000.

D) $347,200.

E) $349,300.

3) Dean Hardware, Inc. is comprised of five operating segments. Information about

each of these segments is as follows (in thousands):

What is the total amount of revenues in applying the revenue test?

A.$794

B.$808

C.$892

D.$906

E.$934

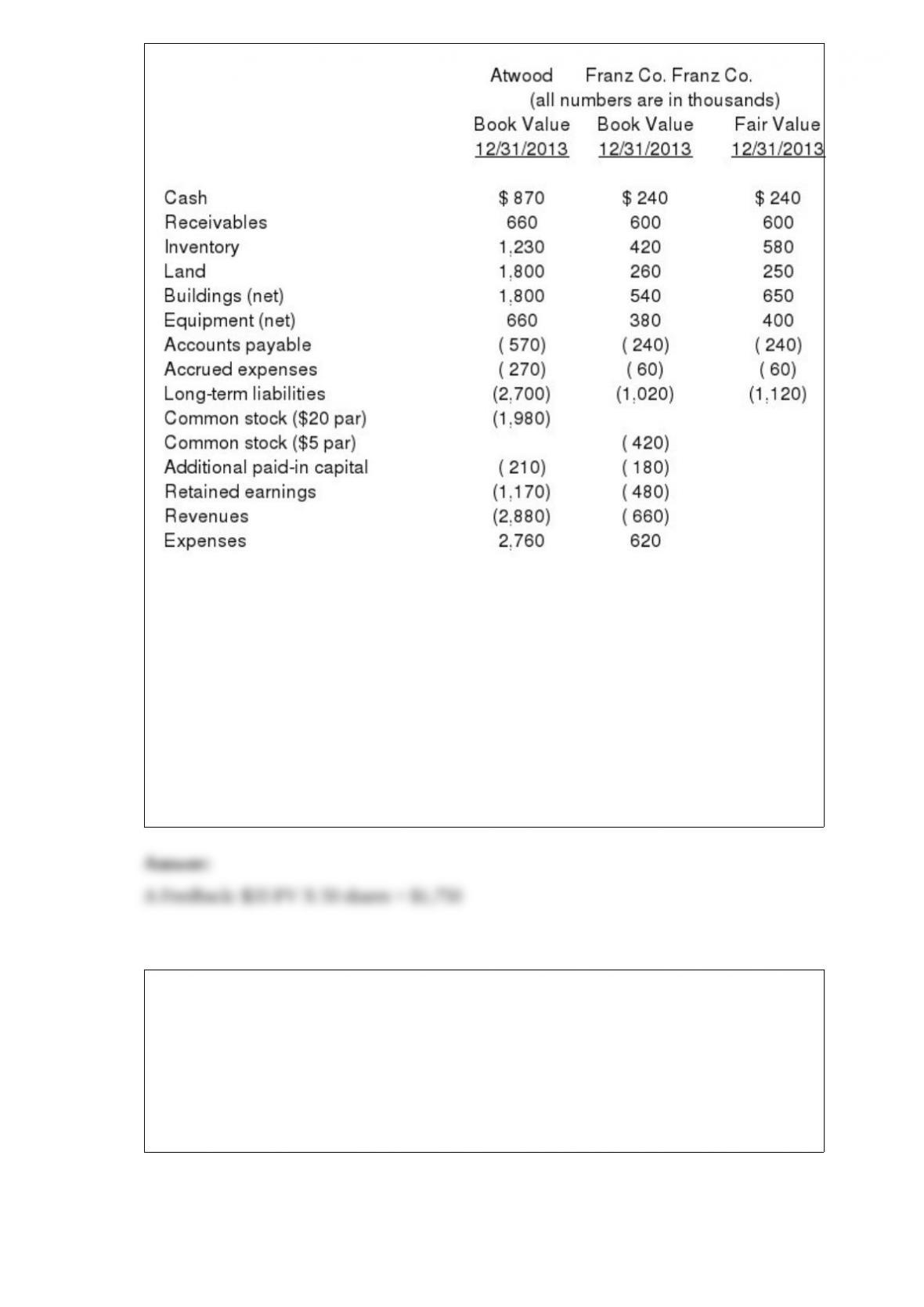

4) The financial balances for the Atwood Company and the Franz Company as of

December 31, 2013, are presented below. Also included are the fair values for Franz

Company’s net assets.

Note: Parenthesis indicate a credit balance

Assume an acquisition business combination took place at December 31, 2013. Atwood

issued 50 shares of its common stock with a fair value of $35 per share for all of the

outstanding common shares of Franz. Stock issuance costs of $15 (in thousands) and

direct costs of $10 (in thousands) were paid.

Compute the investment to be recorded at date of acquisition.

A) $1,750.

B) $1,760.

C) $1,775.

D) $1,300.

E) $1,120.

5) On January 1, 2013, Pride, Inc. acquired 80% of the outstanding voting common

stock of Strong Corp. for $364,000. There is no active market for Strong’s stock. Of this

payment, $28,000 was allocated to equipment (with a five-year life) that had been

undervalued on Strong’s books by $35,000. Any remaining excess was attributable to

goodwill which has not been impaired.

As of December 31, 2013, before preparing the consolidated worksheet, the financial

statements appeared as follows:

During 2013, Pride bought inventory for $112,000 and sold it to Strong for $140,000.

Only half of this purchase had been paid for by Strong by the end of the year. 60% of

these goods were still in the company’s possession on December 31, 2013. What is the

total of consolidated cost of goods sold?

A) $196,000.

B) $212,800.

C) $184,800.

D) $203,000.

E) $168,000.

6) Carnes has the following account balances as of May 1, 2012 before an acquisition

transaction takes place.

The fair value of Carnes’ Land and Buildings are $650,000 and $550,000, respectively.

On May 1, 2012, Riley Company issues 30,000 shares of its $10 par value ($25 fair

value) common stock in exchange for all of the shares of Carnes’ common stock. Riley

paid $10,000 for costs to issue the new shares of stock. Before the acquisition, Riley

has $700,000 in its common stock account and $300,000 in its additional paid-in capital

account.

At the date of acquisition, by how much does Riley’s additional paid-in capital increase

or decrease?

A) $ 0.

B) $440,000 increase.

C) $450,000 increase.

D) $640,000 increase.

E) $650,000 decrease.