42. (continued)

University of Danville

Statement of Activities

Unrestricted Temporarily Permanently Total

Net Restricted Restricted

Assets Net Assets Net Assets

Revenues and Gains

-Tuition 1,200,000

Contributions

-Cash and Other

Assets 707,000 300,000 1,007,000

-Services 80,000 80,000

Total Revenues, Gains,

Operating Expenses

-Salaries 390,000 390,000

-Depreciation 32,000 32,000

-Utilities and Other

Expenses 212,000 212,000

Total Expenses 634,000 634,000

43.(30 Minutes) (Series of questions about private not-for-profit entities)

a. Many private non-for-profit entities depend heavily on gifts and grants from

outside parties. An earning process is not present in connection with such

conveyances. Asset inflows are simply created by donations. Such amounts

b. A statement of functional expenses is required to be included in the financial

statements of voluntary health or welfare entities and is permitted for all other

private not-for-profits. This statement enables readers to determine the

c. Some charities (Goodwill Industries and the Salvation Army, for example)

d. A not-for-profit entity may receive gifts (or unconditional promises to give)

from outside parties that (1) must be expended for a particular purpose or (2)

cannot be expended until a particular point in the future. Because the

organization does not have free use of these assets, they are included within

are included within the “Permanently Restricted Net Assets.”

e. Donated services are extremely common in the operation of many not-for-

profit entities. Literally thousands of individuals solicit funds for entities such

as the Heart Fund, Salvation Army, and March of Dimes. In addition,

individuals often voluntarily fill positions of responsibility throughout many of

f. Prior to 1987, the costs of direct mailings and other solicitations for

support were recorded by private not-for-profit entities as fundraising

expenses even if educational materials were included. In that year, this

requirement was modified so that an allocation of the joint costs could be

made between educational expenses (a program service cost) and fundraising

(a supporting service cost). Some entities took advantage of this rule.

g. Donated materials are normally reported as assets at their fair value

accompanied by an increase in unrestricted net assets (see answer [c]

above). However, the recording of art works, historical treasures, museum

44. (25 Minutes) (Determine impact of various transactions on a private college.)

(1)—False. The January 1, Year 1, restriction is an internal action and, therefore,

causes no changes in the amount of unrestricted net assets. Such changes can

only be created by external donors.

is made immediately at the time of proper expenditure. Spending of the board-

designated $1.9 million does not change the amount of net unrestricted assets—

just the composition.

(5)—False. Depreciation expense is appropriate for all long-lived assets with a

finite life regardless of the policy of the school. A time restriction indicates when

any related donations for this project are released from restriction.

(10)—False. Based on the information given, both the contributed support and

the expense must be reported. “Might” implies an option which is not available

for this type of donation. If a donated service meets the criteria, it is reported.

45. (30 Minutes) (Determine changes in net asset balances for several different

types of transactions)

Part (1)

–Unrestricted Net Assets – No net change. When the $22,000 in designated

funds is spent as designated, a reclassification of that amount is made into

Unrestricted Net Assets. At that time, though, a faculty salary expense of the

Part (2)

–Unrestricted Net Assets – No net change. Because of the restriction on the

use of the machine for this period of time, the $200,000 gift is initially reported as

an increase in Temporarily Restricted Net Assets. At the end of the year, the

asset balance will be reduced by $20,000 in depreciation. Thus, a $20,000

Part (3)

–Unrestricted Net Assets – Category increases by $1.6 million. The tuition

revenue of $2 milion is reduced by the $700,000 in financial aid for a net increase

of $1.3 million. However, because $300,000 of previously restricted net assets

46. (65 Minutes) (Prepare financial statements for a private not-for-profit entity.)

a. Entries for this not-for-profit entity are presented below. The numbers in

parenthesis indicate account totals at that point in time. This method is used

as an easy way to monitor account balances.

Contributions receivable……………..…..…... 20,000 (220,000)

Contributed support—unrestricted

net assets…………..…………..……………… 180,000 (180,000)

Salary expense……….……………………….…... 90,000 ( 90,000)

Cash ………..…………..…………………………….. 12,000 (302,000)

Contributed support—temporarily restricted 12,000 ( 12,000)

(To record gift to go to a specified beneficiary.

Entity records this contribution because it

holds variance powers.)

Reclassification – unrestricted net

assets………..………………………….….….… 50,000 ( 65,000)

(To record reclassification of restricted

amount properly spent.)

46. (continued)

Investment revenue—unrestricted net assets 30,000 ( 30,000)

(Income is earned on permanently restricted

net assets but use of the income is unrestricted.)

Rent expense……………………………………..… 12,000 ( 12,000)

Advertising expense ……………………….…... 15,000 ( 15,000)

(Although pledge is unrestricted, it will not

be collected for five years and, therefore,

the proceeds are viewed as temporarily

restricted.)

Contributions receivable……………..…..…... 6,000 (275,000)

Contributed support—interest–temporarily

restricted net assets ……………..….…. 6,000 ( 6,000)

46. (continued)

Based on the final balances computed above, the following statements can be

prepared.

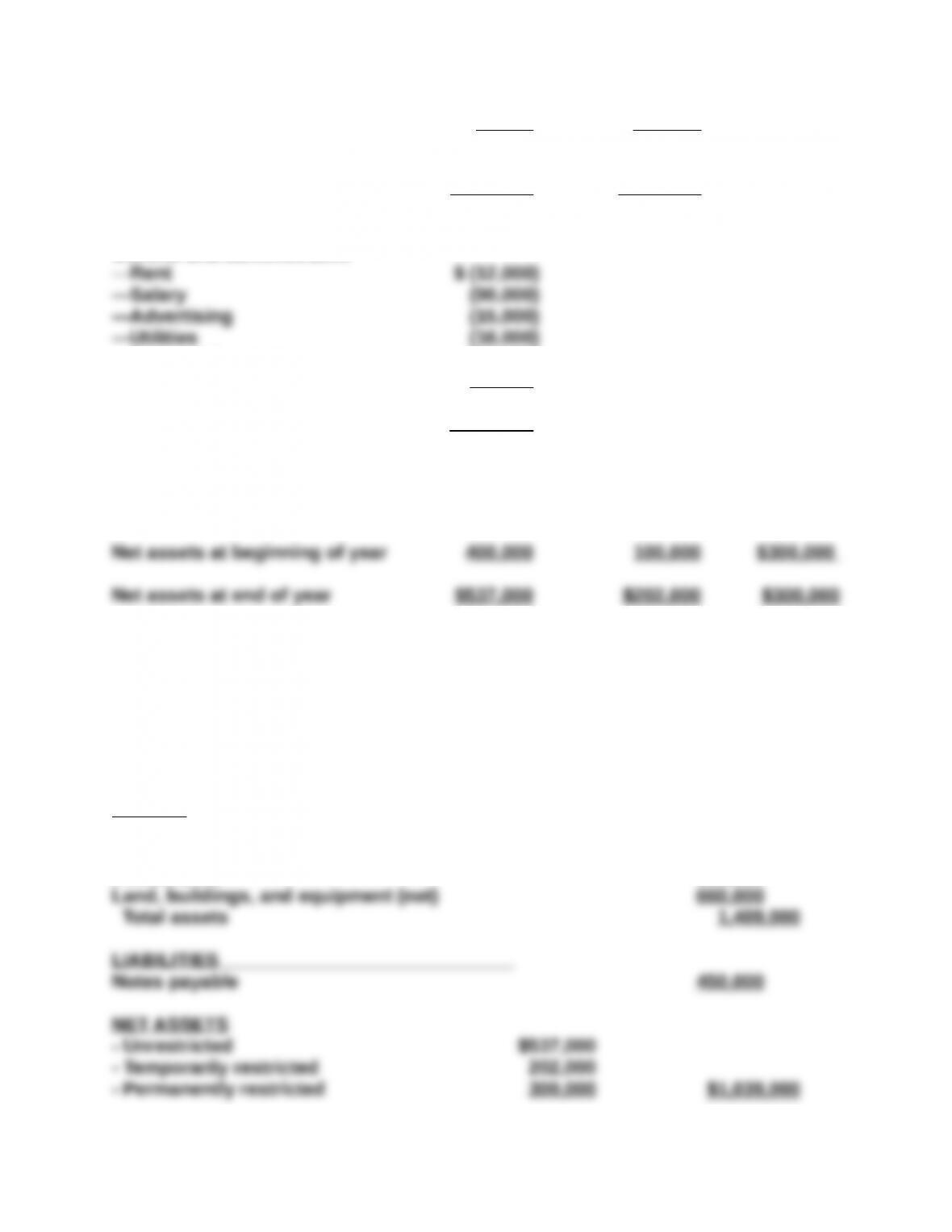

WATSON FOUNDATION

STATEMENT OF ACTIVITIES

For Year Ending December 31, 2015

Temporarily Permanently

Unrestricted Restricted Restricted

Net Assets Net Assets Net Assets

Contributed support $ 180,000 $ 161,000

Contributions — interest 20,000 6,000

restriction 65 ,000 ( 65 ,000) ________

Total support, revenues, and net

Assets released from restriction $ 325 ,000 $ 102 ,000 ________

Expenses:

General and administrative

—Depreciation (40,000)

—Interest (15 ,000)

Total expenses $(188 ,000)

Excess of total support, revenues

and net assets released from

restriction over expenses $137,000 $102,000 -0-

46. (continued)

b.

WATSON FOUNDATION

STATEMENT OF FINANCIAL POSITION

December 31, 2015

ASSETS

Cash $ 254,000

Contributions receivable (net) 275,000

Investments 300,000

47. (40 minutes) (Accounting for mergers and acquisitions)

a. In an acquisition, the assets and liabilities of the acquired entity are

included at fair value. Thus, the buildings and equipment reported by

Swim For Safety must be increased by $140,000 from $590,000 to

Cash held by Help & Save must be reduced by the $1 million payment as

must the balance shown for its unrestricted net assets.

47. (continued)

–Goodwill – $80,000 (above)

–Total assets – $3,360,000 (summation)

–Accounts payable and accrued liabilities – $180,000 ($110,000 plus $70,000)

–Notes payable – $1,720,000 ($1,100,000 plus $620,000)

–Total liabilities – $1,900,000 (summation)

b. In an acquisition, the assets and liabilities of the acquired entity are

included at fair value. Thus, the buildings and equipment reported by

Swim For Safety must be increased by $140,000 from $590,000 to

$730,000. Because the acquisition value ($990,000) exceeds the total fair

Cash held by Help & Save must be reduced by the $990,000 payment as must

the balance shown for its unrestricted net assets.

The increase in the buildings & equipment ($140,000) is reflected by an

increase in unrestricted net assets since no external restriction is in place

Balances To Be Reported:

–Cash – $1,110,000 ($1,600,000 less $990,000 plus $500,000)

–Contributions receivable (net) – $280,000 ($70,000 plus $210,000)

47. (continued)

–Accounts payable and accrued liabilities – $180,000 ($110,000 plus $70,000)

–Notes payable – $1,720,000 ($1,100,000 plus $620,000)

–Total liabilities and net assets – $3,290,000 ($1,900,000 plus $1,390,000)

c. This transaction is a merger: two not-for-profit entities are brought

together to form a new not-for-profit under a newly-formed governing

body.

As a merger, the carryover method is used. Book values are simply added

Balances To Be Reported:

–Cash – $2,100,000 ($1,600,000 plus $500,000)

–Accounts payable and accrued liabilities – $180,000 ($110,000 plus $70,000)

–Notes payable – $1,720,000 ($1,100,000 plus $620,000)

–Total liabilities – $1,900,000 (summation)

–Total liabilities and net assets – $4,140,000 ($1,900,000 plus $2,240,000)