42. (continued)

Part c. Forward Contract Fair Value Hedge of a Foreign Currency Firm

Commitment (Purchase)

9/15 There is no formal entry for the forward contract or the purchase order.

9/30 Forward Contract $5,940.60

Gain on Forward Contract $5,940.60

Foreign Currency (euro) $220,000

Cash $212,000

Forward Contract 8,000

42. (continued)

Part d. Option Cash Flow Hedge of a Foreign Currency Liability

The following schedule summarizes the changes in the components of the fair

value of the euro call option with a strike price of $1.00 for October 31.

Change Change

Spot Option Fair in Fair Intrinsic Time in Time

Date Rate Premium Value Value Value Value Value

09/15 $1.00 $.035 $7,000 – $0 $7,0001–

1 Because the strike price and spot rate are the same, the option has no intrinsic

value. Fair value is attributable solely to the time value of the option.

2 With a spot rate of $1.05 and a strike price of $1.00, the option has an intrinsic

value of $10,000. The remaining $4,000 of fair value is attributable to time

value.

3 The time value of the option at maturity is zero.

9/15 Inventory $200,000

Accounts Payable (euro) $200,000

AOCI $7,000

AOCI $10,000

Gain on Foreign Currency Option $10,000

Accounts Payable (euro) $10,000

Foreign Currency Option $6,000

AOCI $6,000

AOCI $10,000

Gain on Foreign Currency Option $10,000

Option Expense $4,000

AOCI $4,000

42. (continued)

Part e. Option Fair Value Hedge of a Foreign Currency Firm Commitment

(Purchase)

Firm Commitment Option Foreign Currency Option

Spot Change in Premium Change in

Date Rate Fair Value Fair Value for 10/31 Fair Value Fair Value

9/15 $1.00 $0 – $.035 $ 7,000 –

1 ($200,000 – $210,000) x .9901 = $(9,901), where .9901 is the present value factor for one

month at an annual interest rate of 12% (1% per month) calculated as 1/1.01.

9/15 Foreign Currency Option $7,000

Cash $7,000

9/30 Foreign Currency Option $7,000

Gain on Foreign Currency Option $7,000

Firm Commitment $10,099

Foreign Currency (euro) $220,000

Cash $200,000

Foreign Currency Option 20,000

Inventory $220,000

Chapter 9 Develop Your Skills

Research Case—International Flavors and Fragrances

The responses to this assignment might change over time as the company

changes its use of foreign currency derivatives or changes the manner in

which it discloses its foreign currency hedging activities in the annual report.

The following responses are based on IFF’s 2012 annual report.

1. In 2012, IFF provided information in the annual report related to its

management of foreign exchange risk in the following locations:

2. Note 14 indicates that IFF uses foreign currency forward contracts to

reduce exposure to cash flow volatility arising from foreign currency

fluctuations associated with intercompany loans, foreign currency

3. Toward the end of Note 14, the company indicates that “the ineffective

Accounting Standards Case—Forecasted Transactions

Questions asked in the case are:

Is management’s intent sufficient to assess that a forecasted transaction is

likely to occur?

If not, what additional evidence must be considered?

Source of guidance: FASB ASC 815-20-55-24 Derivatives and Hedging; Hedging-

ASC 815-20-55-24 states: “An assessment of the likelihood that a forecasted

transaction will take place should not be based solely on management’s intent

a. The frequency of similar past transactions

d. The extent of loss or disruption of operations that could result if the

transaction does not occur

e. The likelihood that transactions with substantially different characteristics

The answers to the specific questions asked in the case are:

Management’s intent is not sufficient to assess whether a forecasted

transaction is likely to occur.

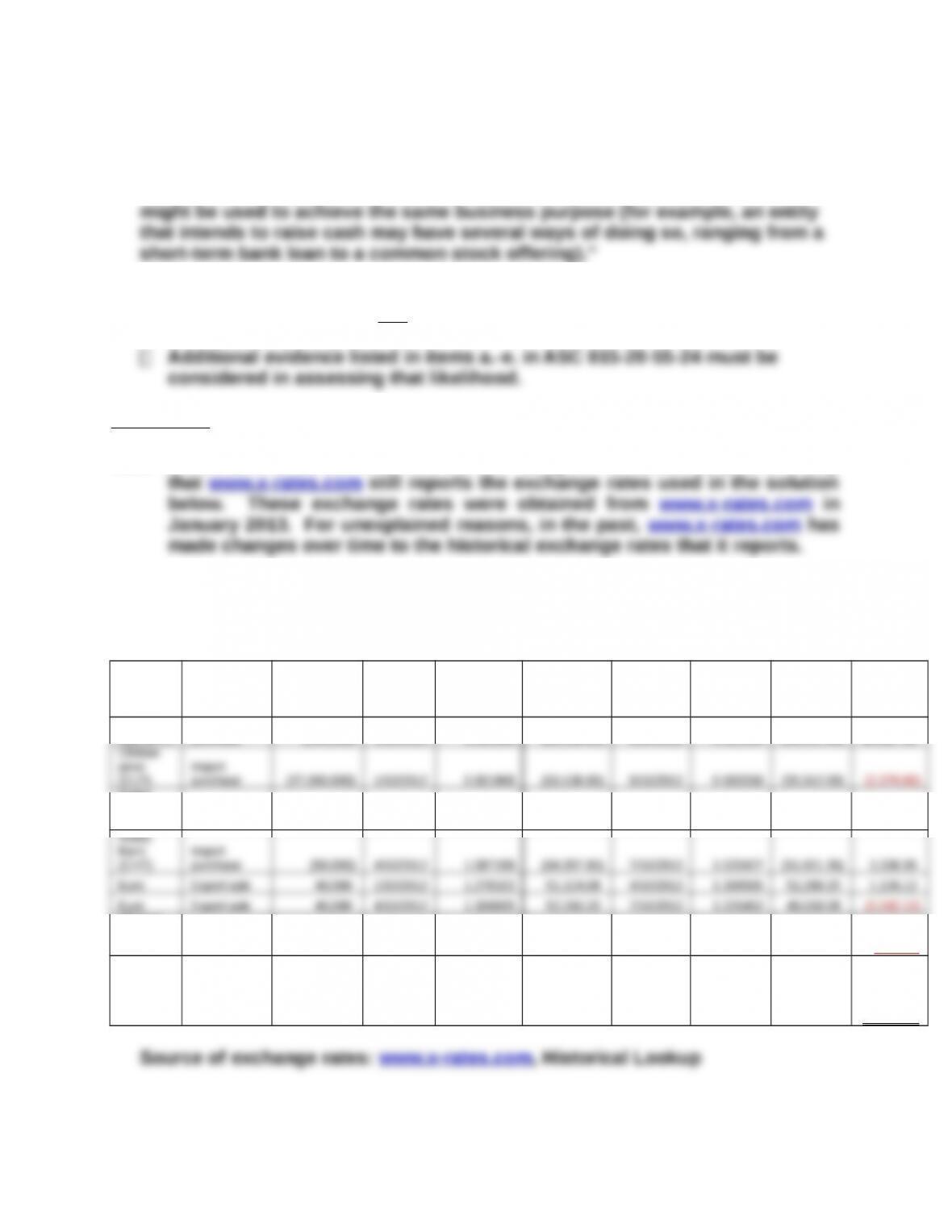

Excel Case—Determine Foreign Exchange Gains and Losses

Note to Instructors: At the time this case is assigned to students, please verify

1., 2. and 3. Spreadsheet for the calculation of the foreign exchange gains

(losses) related to Import/Export Company’s foreign currency

transactions for the year 2012.

Foreign

Currency

Type of

Transaction

Amount in

Foreign

Currency

Trans–

action

Date

Exchange

Rate at

Transaction

Date

$ Value on

Transaction

Date

Settle–

ment Date

Exchange

Rate at

Settlement

Date

$ Value on

Settlement

Date

Foreign

Exchange

Gain

(Loss)

Brazilian

real (BRL)

Import

purchase (100,000) 1/10/2012 0.553189 (55,318.90) 5/10/2012 0.511316 (51,131.60) $4,187.30

Swiss

franc

(CHF) Export sale 50,000 1/10/2012 1.05384 52,692.00 4/10/2012 1.087158 54,357.90 1,665.90

Chinese

yuan

(CNY)

Import

purchase (340,000) 1/10/2012 0.158353 (53,840.02) 10/10/2012 0.158893 (54,023.62) (183.60)

Total Net

Foreign

Exchange

Gain

(Loss) $4,524.15

Import/Export Company reported a net foreign exchange gain of $4,524.15 in

2012 income.

Possible discussion points for instructors: Note that all transactions had a $

value on transaction date of approximately $53,000. The size of the foreign

exchange gains and losses reported in the last column differs substantially

Excel Case (continued)

On the other hand, the large appreciation in the value of the CLP over the

same time period resulted in a foreign exchange loss on a foreign currency

payable.

Analysis Case—Cash Flow Hedge

1. Given the $6,000 total Premium Expense, the forward rate on 2/1/15 must

have been $1.06 [($1.06 – $1.00 spot) x 100,000 euros = $6,000].

2. Given that the forward contract is reported as a liability of $1,980 ($2,000 x

3. Given that the cost of goods sold is $103,000, the spot rate on 5/1/15 must

have been $1.03. Linber must pay $1.06 per euro under the forward

4. The Premium Expense of $6,000 reflects the increase in cost for the parts

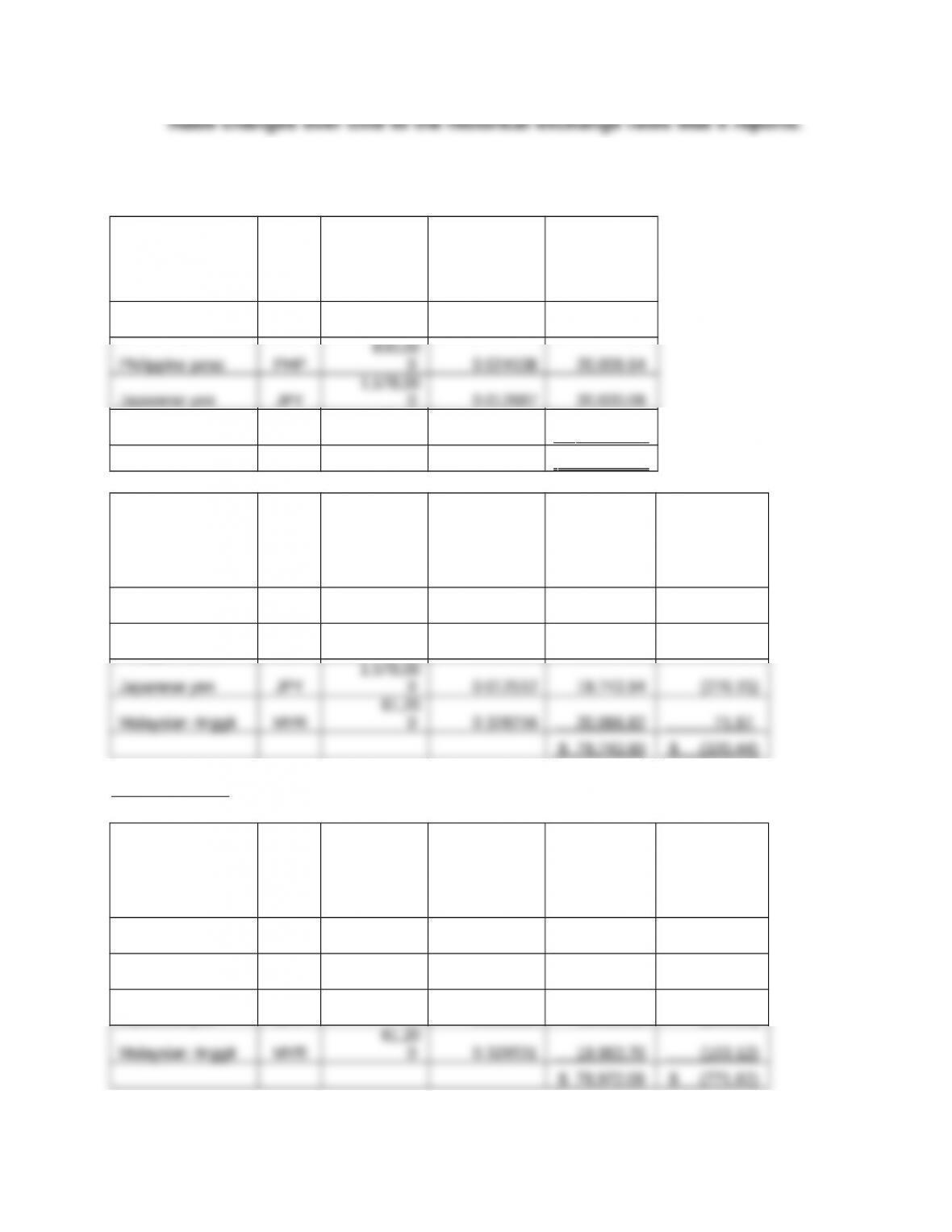

Internet Case—Historical Exchange Rates

Note to Instructors: At the time this case is assigned to students, please verify

1. Spreadsheets for the calculation of the foreign exchange gains (losses)

related to Pier Ten Company’s foreign currency account receivables.

Currency Code

Foreign

Currency

Account

Receivable

Exchange

Rate on

10/15/12

U.S. Dollar

Value on

10/15/12

Indian rupee INR

1,062,00

0 0.018851 $ 20,019.76

830,00

Malaysian ringgit MYR

61,20

0 0.32704 20,014.85

$ 80,064.34

Currency Code

Foreign

Currency

Account

Receivable

Exchange

Rate on

10/31/12

U.S. Dollar

Value on

10/31/12

Foreign

Exchange

Gain (Loss)

on 10/31/12

Indian rupee INR

1,062,00

0 0.018586 $ 19,738.33 $ (281.43)

Philippine peso PHP

830,00

0 0.024307 20,174.81 165.17

1,578,00

Internet Case (continued)

Currency Code

Foreign

Currency

Account

Receivable

Exchange

Rate on

11/15/12

U.S. Dollar

Value on

11/15/12

Foreign

Exchange

Gain (Loss)

on 11/15/12

Indian rupee INR

1,062,00

0 0.018265 $ 19,397.43 $ (340.90)

Philippine peso PHP

830,00

0 0.024279 20,151.57 (23.24)

Japanese yen JPY

1,578,00

0 0.012319 19,439.38 (304.55)

61,20

Currency Code

Foreign

Currency

Account

Receivable

U.S. Dollar

Value on

10/15/12

U.S. Dollar

Value on

11/15/12

Net Foreign

Exchange

Gain (Loss)

1,062,00

Japanese yen JPY

1,578,00

0 20,020.09 19,439.38 (580.70)

Malaysian ringgit MYR

61,20

0 20,014.85 19,983.70 (31.15)

2. Pier Ten would have reported a net foreign exchange loss of $320.44 in the

fiscal year ended October 31, 2012 and a net foreign exchange loss of

3. Assuming a strike price equal to the October 15, 2012 spot rate, the only

foreign currency transactions for which the purchase of a put option

Internet Case (continued)

put option in INR had been acquired, and the net cash flow from the JPY

receivable would have been $480.70 greater ($580.70 FX loss avoided less

$100.00 cost of the option) if a put option in JPY had been acquired.

$100.00 (the cost of the option).

Communication Case—Forward Contracts and Options

To: Mr. Dewey Nukem, CEO, Palmetto Bug Extermination Company (PBEC)

The primary advantage of using forward contracts to hedge foreign exchange

risk is that there is no cost to enter into them. The disadvantage is that the

company is obligated to exchange foreign currency for dollars at the

contracted forward rate. Depending upon the future spot rate, this may or

Exporters sometimes use forward contracts to hedge export sales (import

purchases) when the foreign currency is selling at a forward premium

(discount) as this locks in premium revenue (discount revenue). The risk

associated with this strategy is that the customer may or may not pay on

Since PBEC is making import purchases, it has more control over the timing

of when it will need foreign currency. In that case, it should be safe to enter

The bottom line is that there is no right or wrong answer to the question