32. (65 Minutes) (Journal entries for several years. Includes conversion to

equity method and a sale of a portion of the investment)

1/1/13 Investment in Sumter…………..……… 192,000

Cash……….……….…….…..….….….. 192,000

(To record cost of 16,000 shares of Sumter

Company.)

day, a dividend receivable account is unnecessary.)

9/15/14 Cash……………..………..……….…………. 8,000

Dividend Income…………….….….. 8,000

(Annual dividends declared and received from Sumter

Company.)

Adjustment—Equity in Investee Income 36,800

(Retrospective adjustment necessitated by change

to equity method. Change in figures previously

reported for 2013 and 2014 are calculated as

follows.)

32. (continued)

2013 as reported

Income (dividends)….…...$8,000

Balance………..………..…………..- 0 –

2013—equity method (as restated)

Income (8% of $300,000

2014 as reported

Income (dividends)….…...$8,000

2014—equity method (as restated)

Income (8% of $360,000

reported income)……….…………………$28,800

2013 increase in reported income ($24,000 – $8,000)……..….…... $16,000

2014 increase in reported income ($28,800 – $8,000)……..….…... 20,800

Retrospective adjustment—income (above)..….…..….….…..….…. $36,800

Retrospective adjustment—Investment in Sumter (above)... $36,800

9/15/15 Cash……………..………..……….………..……….... 40,000

Investment in Sumter……………….….….. 40,000

(Annual dividend declared and received from Sumter

[40% × $100,000])

12/31/15 Investment in Sumter….….….…..….….….…. 160,000

Equity in Investee Income……..…......... 160,000

[indicated in problem] over 15 years)

32. (continued)

(To accrue ½ year income of 40% owner-

ship = $380,000 × ½ × 40%)

7/1/16 Equity in Investee Income…………..………… 1,685

Investment in Sumter……………….….….. 1,685

(To record ½ year amortization of patent

to establish correct book value for invest-

ment as of 7/1/16)

7/1/16 Cash ……………….………..………..……….………. 425,000

Investment in Sumter (rounded)…....... 346,374

Investment in Sumter and cost of shares sold:

1/1/13 Acquisition …….………..………..……….………..………….….… $ 192,000

1/1/15 Acquisition….………..………..……….………..……………….….. 965,750

1/1/15 Retrospective adjustment……………..…………….….…..…. 36,800

9/15/15 Dividends…………..………..………..………………….….….….. (40,000)

7/1/16 Amortization….……….………..………..……….………..………… (1,685)

Investment in Sumter—7/1/16 balance……………….….….…. $1,385,495

Because 20,000 of 80,000, or ¼, of shares are sold, the percentage retained is

¾ of 40% = 30%.

9/15/16 Cash……………..………..………………….….…... 30,000

(To record annual dividend declared and received)

32. (continued)

12/31/16 Equity in Sumter…………….………..……….….. 57,000

12/31/16 Equity in Investee Income……………..…..…. 1,264 (rounded)

Investment in Sumter……………….….….. 1,264

(To record ½ year of patent amortization—

computation presented below)

Annual patent amortization—original computation………..………. $3,370

Percentage of shares retained (60,000 ÷ 80,000)…………….………. × 75%

33. (25 Minutes) (Equity income balances for two years, includes intra-entity

transfers)

Equity Income 2014

Basic equity accrual ($250,000 × 30%)……………..………..……… $75,000

Deferral of unrealized gross profit (see Schedule 2)………….. (9 ,000)

Equity Income—2014…………………….………..………..……….... $48 ,000

Equity Income (Loss—2015)

Basic equity accrual ($100,000 [loss] × 30%)…………………….. $(30,000)

Amortization (see Schedule 1)…………..………..………..……..…... (18,000)

33. (continued)

Schedule 1

Purchase price…………………..…..….….…..….….…$770,000

Book value acquired ($1,200,000 × 30%)..….…. 360,000

Payment in excess of book value…….…...........$410,000

Remaining Annual

Excess payment identified with specific assets: Life Amortization

Schedule 2

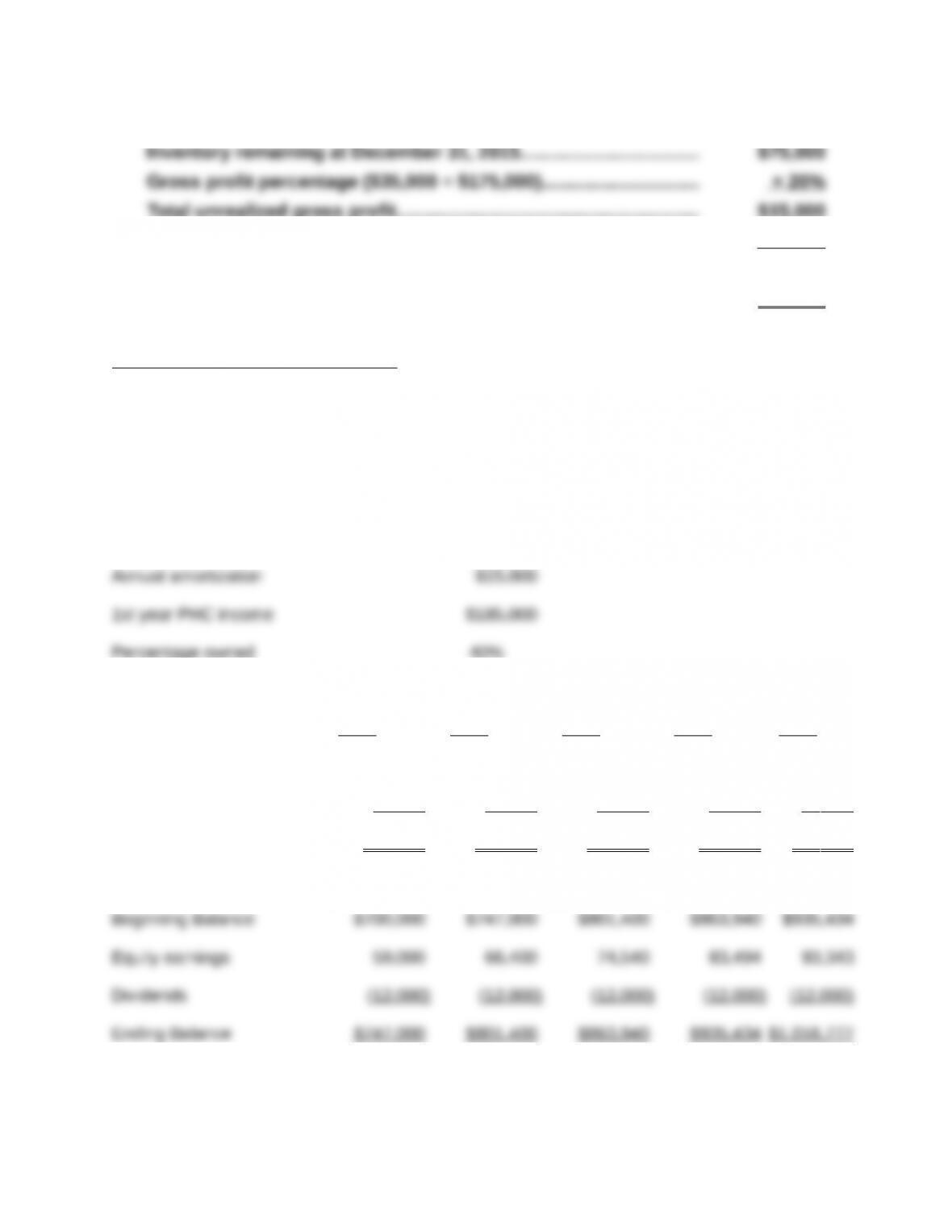

Inventory remaining at December 31, 2014…….….…..….….….…... $80,000

Gross profit percentage ($60,000 ÷ $160,000)……..….….….…..….. × 37 ½ %

Total unrealized gross profit………….……….………..………..……….…. $30,000

Schedule 3

Total unrealized gross profit………….……….………..………..……….…. $15,000

Investor ownership percentage…………..………….….…..….….….….. × 30%

Unrealized intra-entity gross profit —12/31/15

(To be deferred until realized in 2016)…………………….…………. $ 4,500

Solutions to Develop Your Skills

Excel Assignment No. 1 (less difficult)—see textbook Website for the Excel file solution

Parts 1, 2 and 3

Growth rate in income 10%

Dividends $30,000

Cost $700,000 (given in problem)

Percentage owned 40%

2015 2016 2017 2018 2019

PHC reported income $74,000 $81,400 $89,540 $98,494 $108,343

Amortization 15 ,000 15 ,000 15 ,000 15 ,000 15 ,000

Equity earnings $59 ,000 $66 ,400 $74 ,540 $83 ,494 $93 ,343

ROI 8.43% 8.89% 9.30% 9.66% 9.98%

Average 9.25%

Part 3

Growth rate in income 10%

Dividends $30,000

Cost $639,794

(Determined through Solver

under Tools command)

PHC reported income $74,000 $81,400 $89,540 $98,494 $108,343

Amortization 15 ,000 15 ,000 15 ,000 15 ,000 15 ,000

Equity earnings $59 ,000 $66 ,400 $74 ,540 $83 ,494 $93 ,343

Beginning Balance $639,794 $686,794 $741,194 $803,734 $875,228

Equity earnings 59,000 66,400 74,540 83,494 93,343

Excel Assignment No. 2 (more difficult)—see textbook Website for the Excel file solution

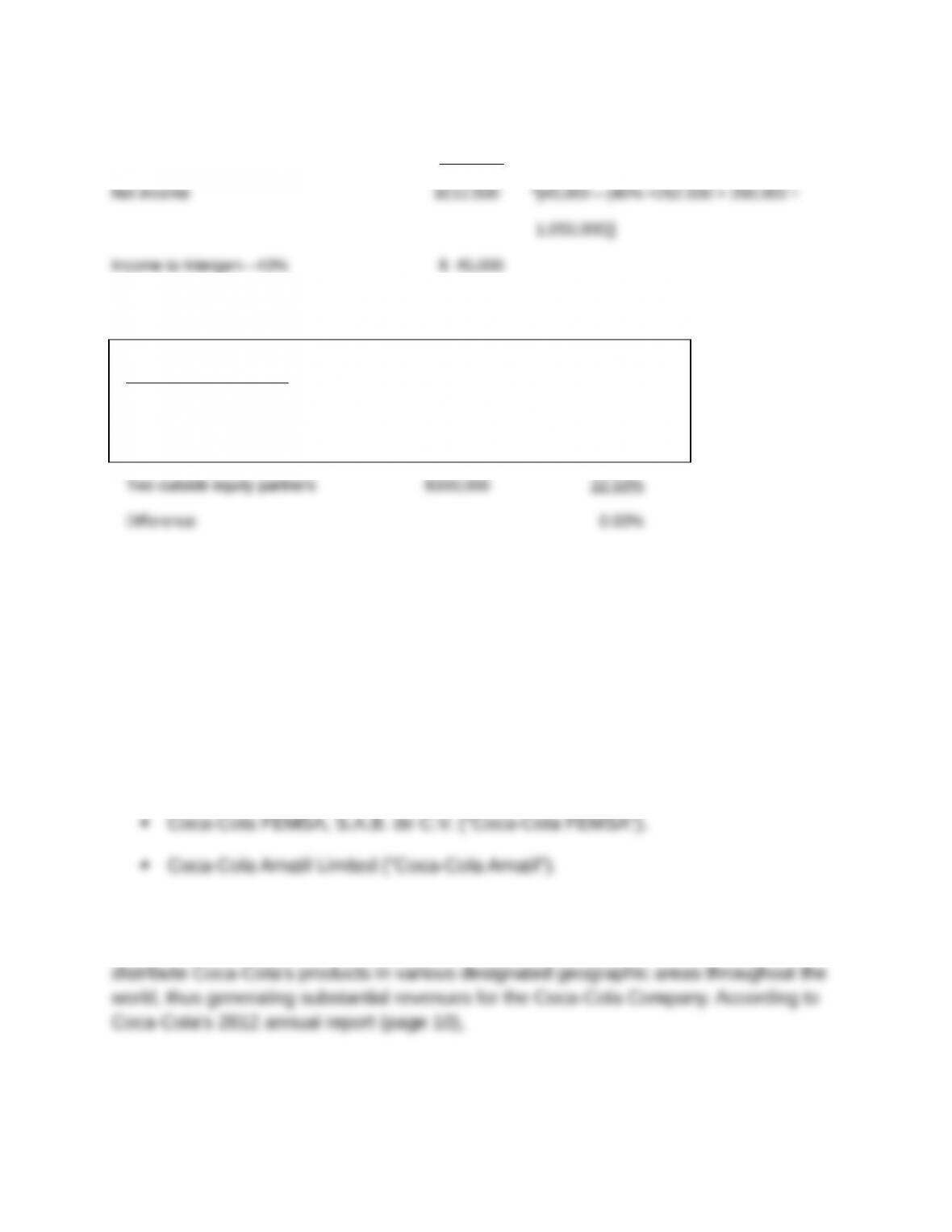

Intergen’s ownership percentage of Ryan 40% Intra-entity Transfer Price = $1,025,000

Cell F4

Ryan’s Income Statement Intergen’s Income Statement

Sales $900,000 Sales $1,025,000

Beginning inventory $ -0- Cost of goods sold $ 850 ,000

Cost of goods sold $768,750

Net income $131,250 *(52,500 – (40% × 256,250 ×

175,000/1,025,000))

Income to Intergen—40% $ 52,500

Income to two equity partners—60% $ 78,750

Rate of Return Analysis

Investment Base Rate of Return

Intergen’s ownership percentage of Ryan = 40% Intra-entity Transfer Price = 1,050,000

Ryan’s Income Statement Intergen’s Income Statement

Inventory 25% Equity in Ryan’s earnings $ 25 ,000*

Use Goal Seek or

Solver under the

Tools command to

set Cell D20 to zero

by changing Cell F4

Ending inventory $ 262,500 Net income $ 225,000

Cost of goods sold $787,500

Income to two equity partners—60% $ 67,500

Rate of Return Analysis

Investment Base Rate of Return

Intergen $1,000,000 22.50%

Solution to Coca-Cola Company Analysis Case

1. In its 2012 10-K, Coca-Cola lists the following companies as significant equity

method investees:

Coca-Cola Hellenic Bottling Company S.A. (“Coca-Cola Hellenic”).

As part of strategic business alliances, each of these companies bottle, market, and

We make equity investments in selected bottling operations with the intention of

maximizing the strength and efficiency of the Coca-Cola system’s production,

2. From the Coca-Cola Company’s 2012 10-K report (page 85),

We use the equity method to account for investments in companies, if our

3. 2012 equity income = $819 million.

4. In general, the equity method provides cost-based values while fair values provide

exit-based values. The relevance of the equity method valuation derives from the

investment’s nature as a productive asset for the investor. Because of their business

of investee revenues and expenses as they are earned by the investor.

When possible, fair values are measured using market prices for the investor’s

shares of the investee. Although exit prices represent a “hypothetical” sale

RESEARCH AND ANALYSIS CASE—IMPAIRMENT

1. Paragraph 323-10-35-32 of the FASB ASC states that

A loss in value of an investment which is other than a temporary decline

shall be recognized. Evidence of a loss in value might include, but would

not necessarily be limited to, absence of an ability to recover the carrying

2. Given the facts in the case, a very good case can be made that the decline in value

3. No, according to FASB ASC para. 350-20-35-59, the equity method investment as a

Research Case Solution — Noncontrolling Shareholder Rights

1. Protective Rights (ASC Topic 810, Consolidation 810-10-25-10)

Noncontrolling rights (whether granted by contract or by law) that would allow the

noncontrolling shareholder to block corporate actions would be considered

protective rights and would not overcome the presumption of consolidation by the

investor with a majority voting interest in its investee. The following list is illustrative

of the protective rights that often are provided to the noncontrolling shareholder but

is not all-inclusive:

a. Amendments to articles of incorporation of the investee

e. Issuance or repurchase of equity interests.

2. Substantive Participating Rights (ASC Topic 810, Consolidation 810-10-25-11)

Noncontrolling rights (whether granted by contract or by law) that would allow the

noncontrolling shareholder to participate in determining certain financial and

in Clearwire.

3. (FASB ASC Topic 810, Consolidation 810-10-25-11)

Substantive participating rights would overcome the presumption that the investor

with a majority voting interest shall consolidate its investee. The following list is

illustrative of substantive participating rights, but is not necessarily all-inclusive:

4. Assessing Individual Noncontrolling Rights (FASB ASC Topic 810, Consolidation

810-10-55-1 b and c)

b. Existing facts and circumstances should be considered in assessing whether

the rights of the noncontrolling shareholder relating to an investee’s incurring

c. The rights of the noncontrolling shareholder relating to dividends or other

distributions may be protective or participating and should be assessed in light