27. (30 minutes) (Conversion to equity method, sale of investment, and

unrealized gross profit)

Part a

Allocation and annual amortization—first purchase

Purchase price of 10 percent interest……………..………..…………. $92,000

Net book value ($800,000 × 10%)…………….…………………..………. (80 ,000)

Annual Amortization…..………..…………………..………..………………….... $ 750

27. Part a (continued)

Allocation and annual amortization—second purchase

Purchase price of 20 percent interest……………..………..…………. $210,000

Net book value ($800,000 is increased by $180,000

income but decreased by $80,000 in dividends)

($900,000 × 20%) ………..………..…………………..………….…..…... (180 ,000)

Annual amortization…………..………..…………………..……………..…..….. $ 2 ,000

Equity income—2013 (after conversion to establish comparability)

2013 basic equity income accrual ($180,000 × 10%)..…..…..…....... $18,000

2013 amortization on first purchase (above)……………..……………... (750)

Equity income—2013……………………..………..………………….…..…. $17 ,250

Equity income 2014

2014 basic equity income accrual ($210,000 × 30%)…….…..….. $63,000

Part b

Investment in Barringer

Purchase price—January 1, 2013…………………………………..…..….... $92,000

Purchase price January 1, 2014…………..…………………..…………….... 210,000

2015 amortization on second purchase (above).…..…..…......... (2,000)

2015 dividends ($100,000 × 30%)……………..…..…..…..…..…..…... (30 ,000)

Investment in Barringer—12/31/15……………..……………..…..…..….... $377 ,750

27. Part b (continued)

Gain on sale of investment in Barringer

Sales price (given)…………..………..………..………….…..…..…..…..… $400,000

Gain on sale of investment……………..…………………..…………. $ 22 ,250

Part c

Deferral of 2014 unrealized gross profit into 2015

Ending inventory…………….………..………..…………………..………….. $20,000

Gross profit percentage ($15,000 ÷ $50,000)….………..…………… × 30%

Deferral of 2015 unrealized gross profit into 2016

Ending inventory…………….………..………..…………………..………….. $40,000

Gross profit percentage ($27,000 ÷ $60,000)….………..…………… × 45%

Unrealized gross profit………….………..…………..…..…..…..…... $18,000

Equity Income—2015

2015 equity income accrual ($230,000 × 30%)……..…..…..…..…. $69,000

2015 amortization on first purchase (above)….…..…..…..…..….. (750)

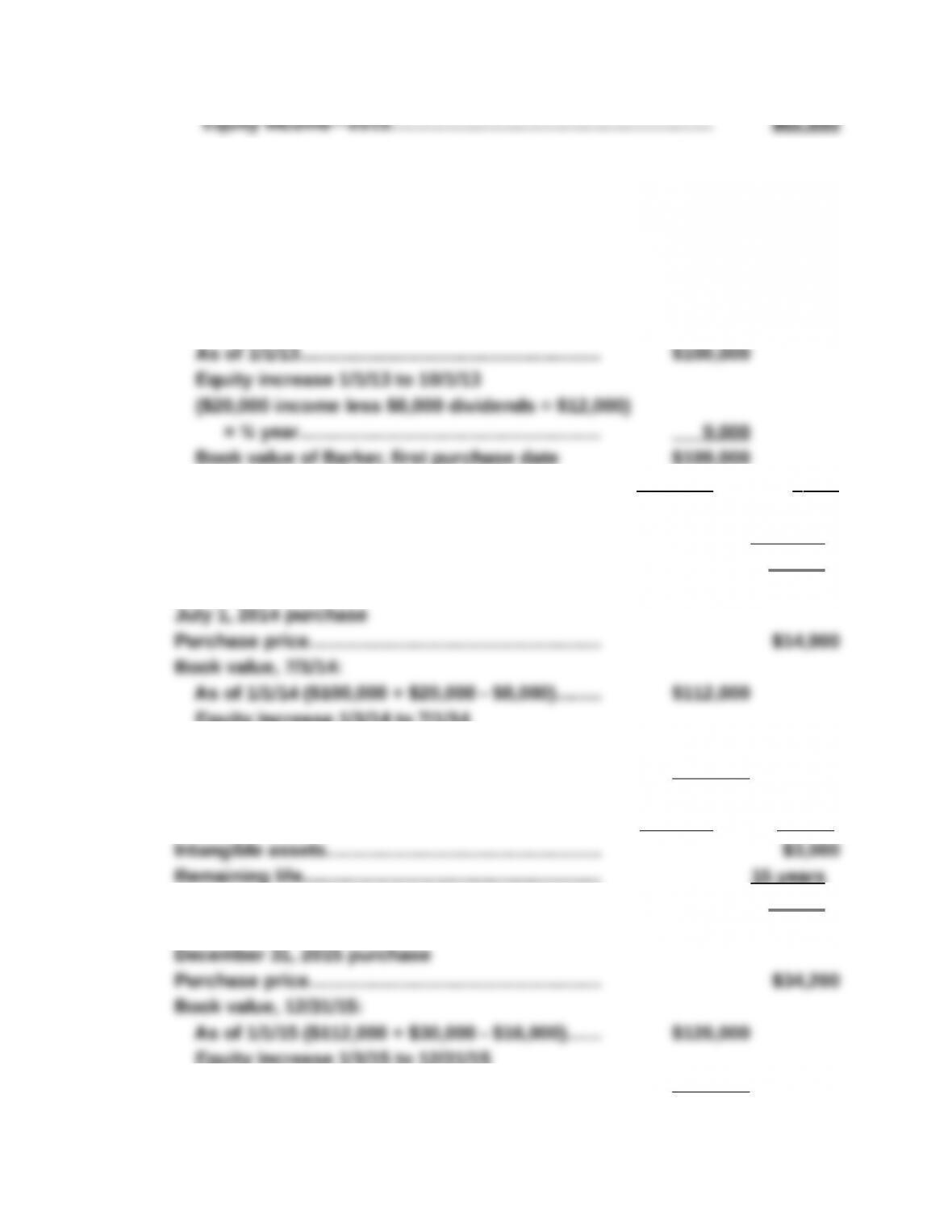

28. (40 Minutes) (Conversion to equity method and equity reporting after several

years)

a. Annual Amortization

October 1, 2013 purchase

Purchase price……………………………..………..….…..…..…..…..…..… $7,475

Book value, 10/1/13:

Acquired percentage……………………………..………... × 5% 5 ,450

Intangible assets…………………..…………..…..…..…... $2,025

Remaining life…………..………..………………………..…. 15 years

Annual amortization—first purchase……..…..….... $ 135

Equity increase 1/1/14 to 7/1/14

($30,000 income less $16,000 dividends = $14,000)

× ½ year………….………..….…..…..…..…..…..…. 7 ,000

Book value of Barker, second purchase date $119,000

Acquired percentage……………………………..………... × 10% 11 ,900

Annual amortization—second purchase..…......... $ 200

Equity increase 1/1/15 to 12/31/15

($24,000 income less $9,000 dividends)........... 15 ,000

Book value of Barker, third purchase $141,000

Acquired percentage……………………………..………... × 20% 28,200

28.a (continued)

Intangible assets…………..………..………..…..…..….... $6,000

Equity Income Reported by Smith

Reported for 2013 (3 months) after conversion

to equity method:

Accrual ($20,000 × ¼ year × 5%)………..…... $250.00

Reported for 2014 (5% for entire year and an additional 10%

for last 6 months) (after conversion to equity method):

Accrual—first purchase ($30,000 entire year × 5%)....... 1,500

Equity income—2014……………………..………..…………… $2 ,765

Reported for 2015 (15% for entire year; because final acquisition occurred

at year end, neither income nor amortization is recognized):

Basic equity accrual ($24,000 × 15%)……..…..…..…..….... $3,600

b. Investment in Barker

Cost—first purchase………….………..…………………..………..…….…. $ 7,475.00

Cost—second purchase……………………………..………..……….….... 14,900.00

2015…….…………………..………..…………………..…..…..…..…..…..… 3,265.00

28. b (continued)

Less: investee dividends

2013 ($8,000 × ¼ × 5%)……….…………………..……….…..…..…..… (100.00)

2015 ($9,000 × 15%)………….…………………..………..…..…..…..…. (1 ,350.00)

Balance………..………..…………………..………..…………………..………… $59 ,771.25

29. (25 Minutes) (Preparation of journal entries for two years, includes losses and

intra-entity transfers of inventory)

Journal Entries for Harper Co.

1/1/14 Investment in Kinman Co….......... 210,000

Cash….……………………………….. 210,000

(To record initial investment)

12/31/14 Equity in Kinman Income—Loss. 16,000

Other Comprehensive Loss of Kinman 8,000

Investment in Kinman Co…..… 24,000

of Kinman—see Schedule 1 below)

29. (continued)

12/31/14 Equity in Kinman Income-Loss.... 2,000

Investment in Kinman Co…..… 2,000

(To defer unrealized gross profit on intra-entity

sale see Schedule 2 below)

During Dividends Receivable….…............ 4,800

equity investee)

12/31/15 Equity in Kinman Income............. 3,300

Investment in Kinman Co…..… 3,300

(To record amortization relating to acquisition

of Kinman)

12/31/15 Investment in Kinman Co….......... 2,000

29. (continued)

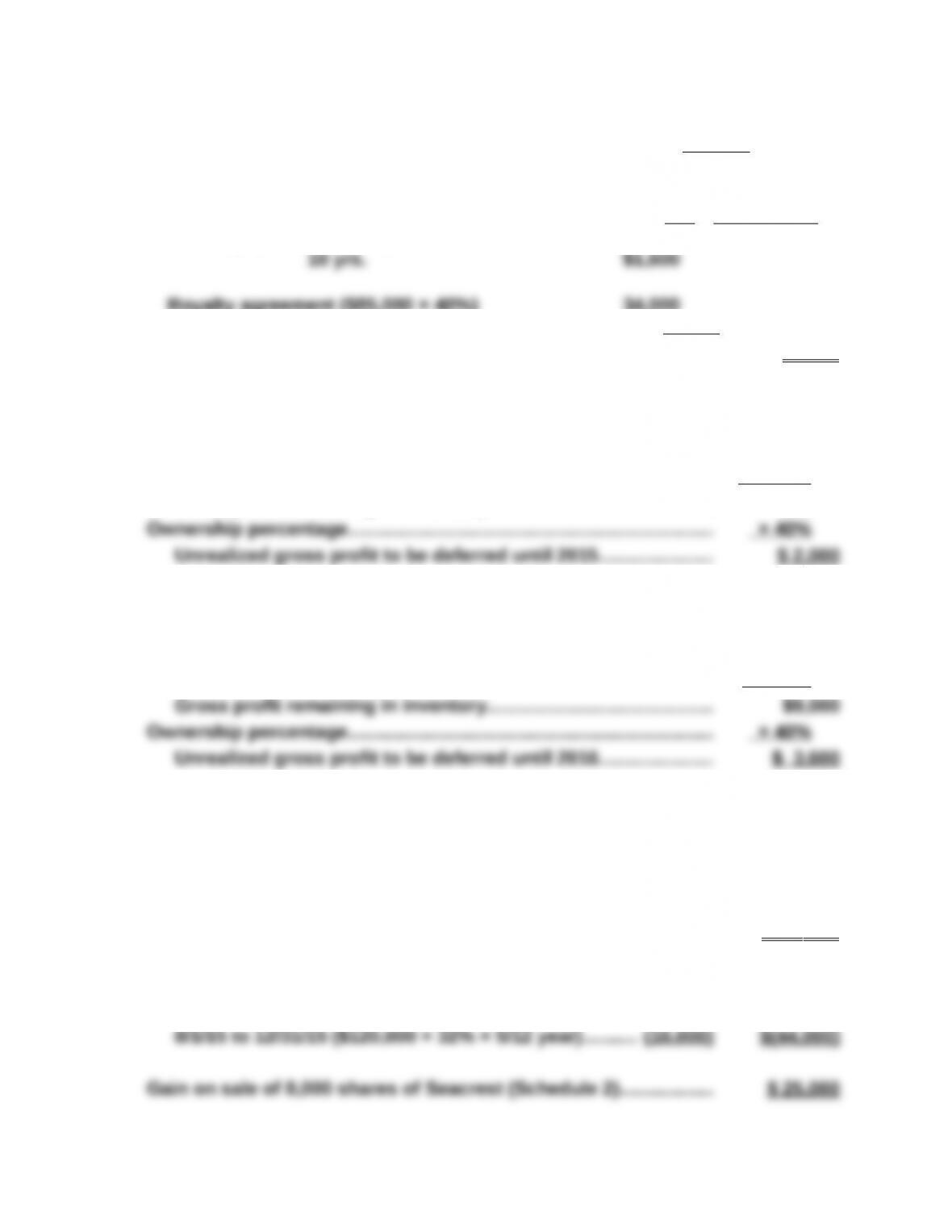

Schedule 1—Allocation of Purchase Price and Related Amortization

Purchase price ……….………..………..……………………. $210,000

Percentage of book value acquired

($400,000 × 40%)…………………..…………………..…….. (160 ,000)

Payment in excess of book value…………….…..…..….. $50,000

Remaining Annual

Excess payment identified with specific assets: Life Amortization

Building ($40,000 × 40%) $16,000

Royalty agreement ($85,000 × 40%) 34,000

20 yrs. 1,700

Total annual amortization $3 ,300

Schedule 2—Deferral of Unrealized Gross Profit—2014

Inventory remaining at end of year……………..………..………………….. $15,000

Gross profit percentage ($30,000 ÷ $90,000)……………..………..….... × 33 ⅓ %

Gross profit remaining in inventory………………..…………………… $5,000

Schedule 3—Deferral of Unrealized Gross Profit—2015

Inventory remaining at end of year (30%)………………..…………….…. $24,000

Gross profit percentage ($30,000 ÷ $80,000)……………..………..….... × 37 ½ %

30. (35 Minutes) (Investment sale with equity method applied both before and

after. Includes other comprehensive loss and intra-entity inventory

transfer)

Income effects for year ending December 31, 2015

Equity income in Seacrest, Inc. (Schedule 1)…..…..…..…..…..… $116 ,000

Other comprehensive loss—Seacrest, Inc.

1/1/15 to 8/1/15 ($120,000 × 40% × 7/12 year)..….......... (28,000)

Schedule 1—Equity Income in Seacrest, Inc.

Investee income accrual—operations

$342,000 × 40% × 7/12 year………….…..…..…..…..… $79,800

$342,000 × 32% × 5/12 year………….…..…..…..…..… 45 ,600 $125,400

Amortization

shares): $12,000 × 80% × 5/12 year………….….. 4 ,000 (11,000)

Recognition of unrealized gross profit

Remaining inventory—12/31/14………………….….... $10,000

Gross profit percentage on original sale

($20,000 ÷ $50,000)……….………..………..…………. × 40%

30. (continued)

Schedule 2—Gain on Sale of Investment in Seacrest, Inc.

Book value—investment in Seacrest, Inc.—1/1/15 (given)………. $293,600

Investee income accrual—1/1/15 – 8/1/15 (Schedule 1)…………... 79,800

Recognition of deferred profit (Schedule 1)……….…..…..…..…..… 1 ,600

Investment in Seacrest book value 8/1/15…………..………..…….…. $340,000

Percentage of investment sold (8,000 ÷ 40,000 shares)…..…...... × 20 %

Gain on sale of 8,000 shares of Seacrest……………..…..…..….. $ 25 ,000

31. (30 Minutes) (Compute equity balances for three years. Includes

intra-entity inventory transfer)

Part a.

Equity Income 2013

Basic equity accrual ($598,000 × ½ year × 25%)…………………… $74,750

Amortization (½ year—see Schedule 1)……….…..…..…..…..….... (30 ,800)

Equity Income—2013……………………..…………..…..…..…..….... $43 ,950

Equity Income 2014

Basic equity accrual ($639,600 × 25%)……………..……………..…. $159,900

Equity Income—2014……………………..………..…………..…..….. $92 ,300

Equity Income 2015

Basic equity accrual ($692,400 × 25%)……………..……………..…. $173,100

Amortization (see Schedule 1)…………..…………………..…..…..…. (61,600)

31. (continued)

Schedule 1—Acquisition Price Allocation and Amortization

Acquisition price (88,000 shares × $13) $1,144,000

Remaining Annual

Excess payment identified with specific assets: Life Amortization

Equipment ($364,000 × 25%) $91,000 7 yrs. $13,000

Goodwill 78,600indefinite

-0-

Total annual amortization (full year) $61,600

Schedule 2—Deferral of Unrealized Intra-entity Gross Profit

Intra-entity Gross Profit Percentage:

Sales $152,000

Gross profit percentage: $60,800 ÷ $152,000 = 40%

Investor ownership percentage…………..………….…..…..…..…..…... × 25%

Unrealized intra-entity gross profit deferred from

2014 until 2015………..………..………..…………………..………….….... $ 6,000

Part b.

Investment in Shaun—December 31, 2015 balance

Acquisition price…………..………..………..…………………..………………. $1,144,000

2013 Equity income (above)……………………..………..…..…..…..….... 43,950

2013 Dividends declared during half year (88,000 shares × $1.00) (88,000)

2015 Dividends declared (88,000 shares × $1.00 × 2)…..…..…..... (176 ,000)

Investment in Shaun—12/31/15……………………..…..…..…..… $957 ,750