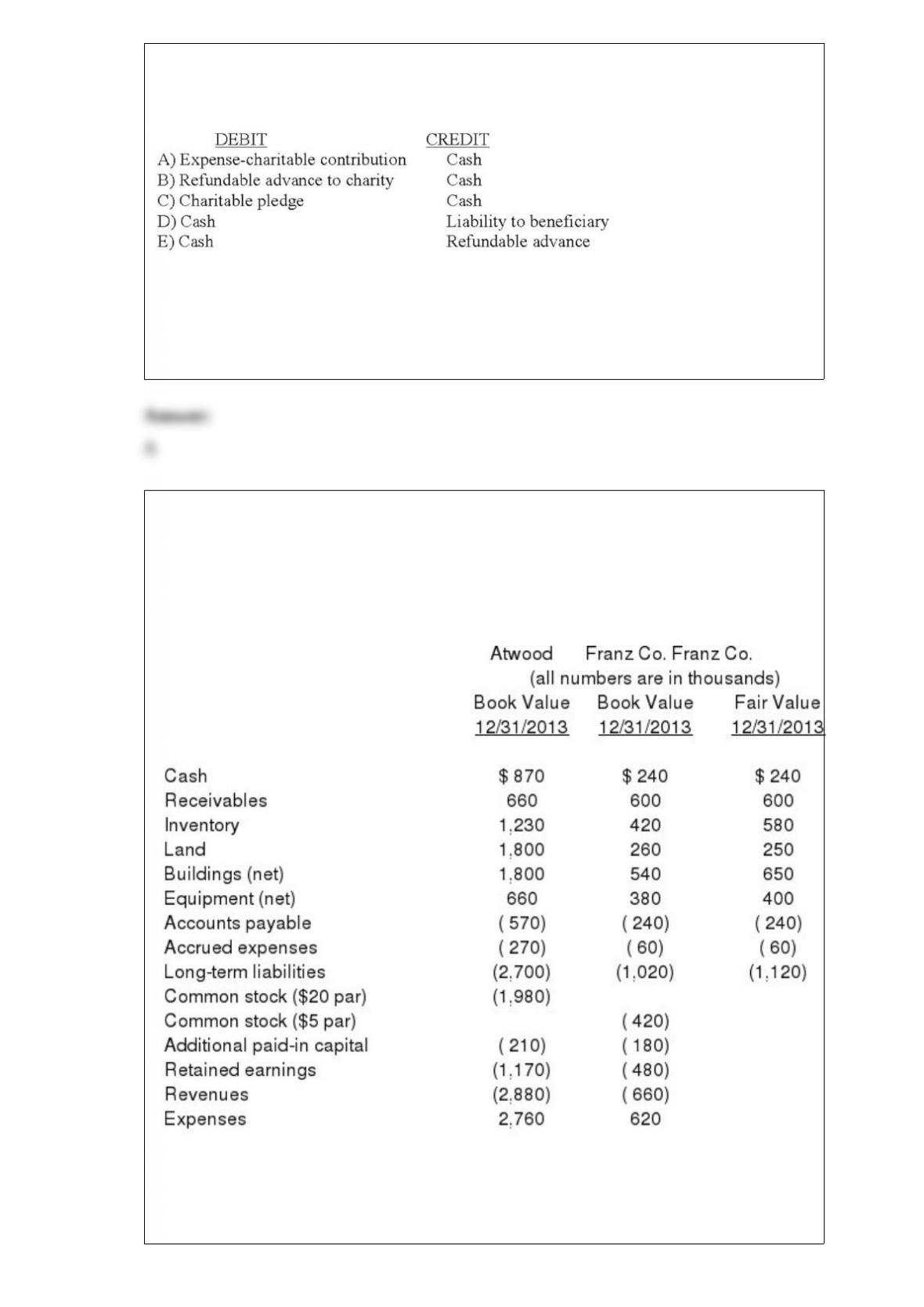

1) Which entry would be the correct entry on the donor’s books when the donor

relinquishes control of an asset that it contributes to a not-for-profit organization?

A.Option A

B.Option B

C.Option C

D.Option D

E.Option E

2) The financial balances for the Atwood Company and the Franz Company as of

December 31, 2013, are presented below. Also included are the fair values for Franz

Company’s net assets.

Note: Parenthesis indicate a credit balance

Assume an acquisition business combination took place at December 31, 2013. Atwood

issued 50 shares of its common stock with a fair value of $35 per share for all of the

outstanding common shares of Franz. Stock issuance costs of $15 (in thousands) and

direct costs of $10 (in thousands) were paid.

Compute consolidated goodwill at the date of the acquisition.

A) $360.

B) $450.

C) $460.

D) $440.

E) $475.

3) On January 1, 2013, Jackie Corp. purchased 30% of the voting common stock of Rob

Co., paying $2,000,000. Jackie properly accounts for this investment using the equity

method. At the time of the investment, Rob’s total stockholders’ equity was $3,000,000.

Jackie gathered the following information about Rob’s assets and liabilities whose book

values and fair values differed:

Any excess of cost over fair value was attributed to goodwill, which has not been

impaired. Rob Co. reported net income of $300,000 for 2013, and paid dividends of

$100,000 during that year.

What is the balance in Jackie Corp’s Investment in Rob Co. account at December 31,

2013?

A) $2,000,000.

B) $2,005,000.

C) $2,060,000.

D) $2,090,000.

E) $2,200,000.

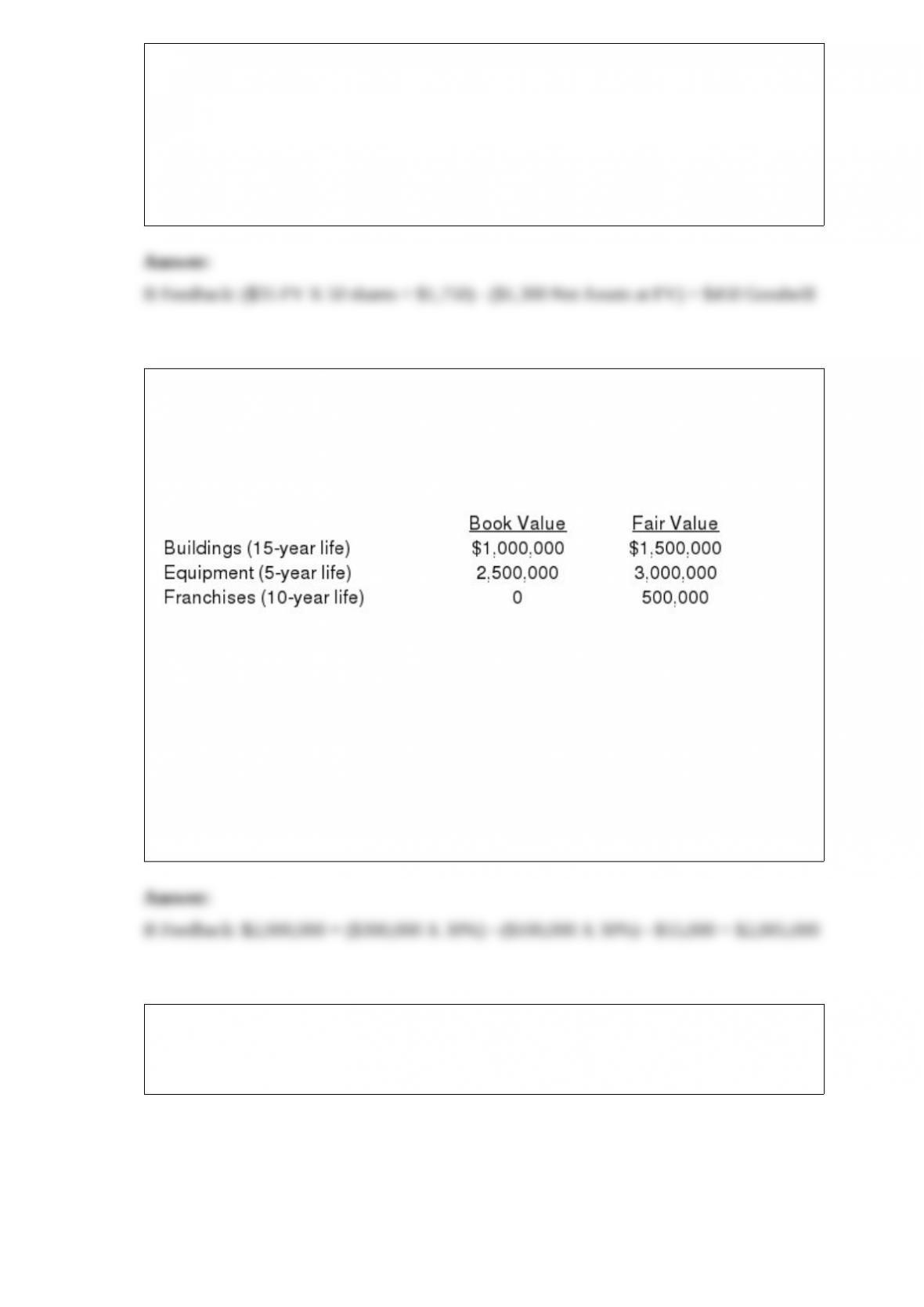

4) Presented below are the financial balances for the Atwood Company and the Franz

Company as of December 31, 2012, immediately before Atwood acquired Franz. Also

included are the fair values for Franz Company’s net assets at that date.

Note: Parenthesis indicate a credit balance

Assume a business combination took place at December 31, 2012. Atwood issued 50

shares of its common stock with a fair value of $35 per share for all of the outstanding

common shares of Franz. Stock issuance costs of $15 (in thousands) and direct costs of

$10 (in thousands) were paid to effect this acquisition transaction. To settle a difference

of opinion regarding Franz’s fair value, Atwood promises to pay an additional $5.2 (in

thousands) to the former owners if Franz’s earnings exceed a certain sum during the

next year. Given the probability of the required contingency payment and utilizing a 4%

discount rate, the expected present value of the contingency is $5 (in thousands).

Compute the consolidated cash upon completion of the acquisition.

A) $1,350.

B) $1,110.

C) $1,080.

D) $1,085.

E) $ 635.

5) A foreign subsidiary uses the first-in first-out inventory method. The following

inventory balances are given at December 31, 2013 in local currency units (LCU):

Compute the December 31, 2013, inventory balance using the lower of cost or market

method under the temporal method.

A.$429,000

B.$457,600

C.$596,400

D.$568,000

E.$426,000

6) A city starts a solid waste landfill during 2012. When the landfill was opened the city

estimated that it would fill to capacity within 5 years and that the cost to cover the

facility would be $1.5 million which will not be paid until the facility is closed. At the

end of 2012, the facility was 20% full, and at the end of 2013 the facility was 45% full.

On government-wide financial statements, which of the following are the appropriate

amounts to present in the financial statements for 2013?

A.Both expense and liability will be zero.

B.Expense will be $300,000 and liability will be $600,000.

C.Expense will be $600,000 and liability will be $600,000.

D.Expense will be $675,000 and liability will be $600,000.

E.Expense will be $375,000 and liability will be $675,000.

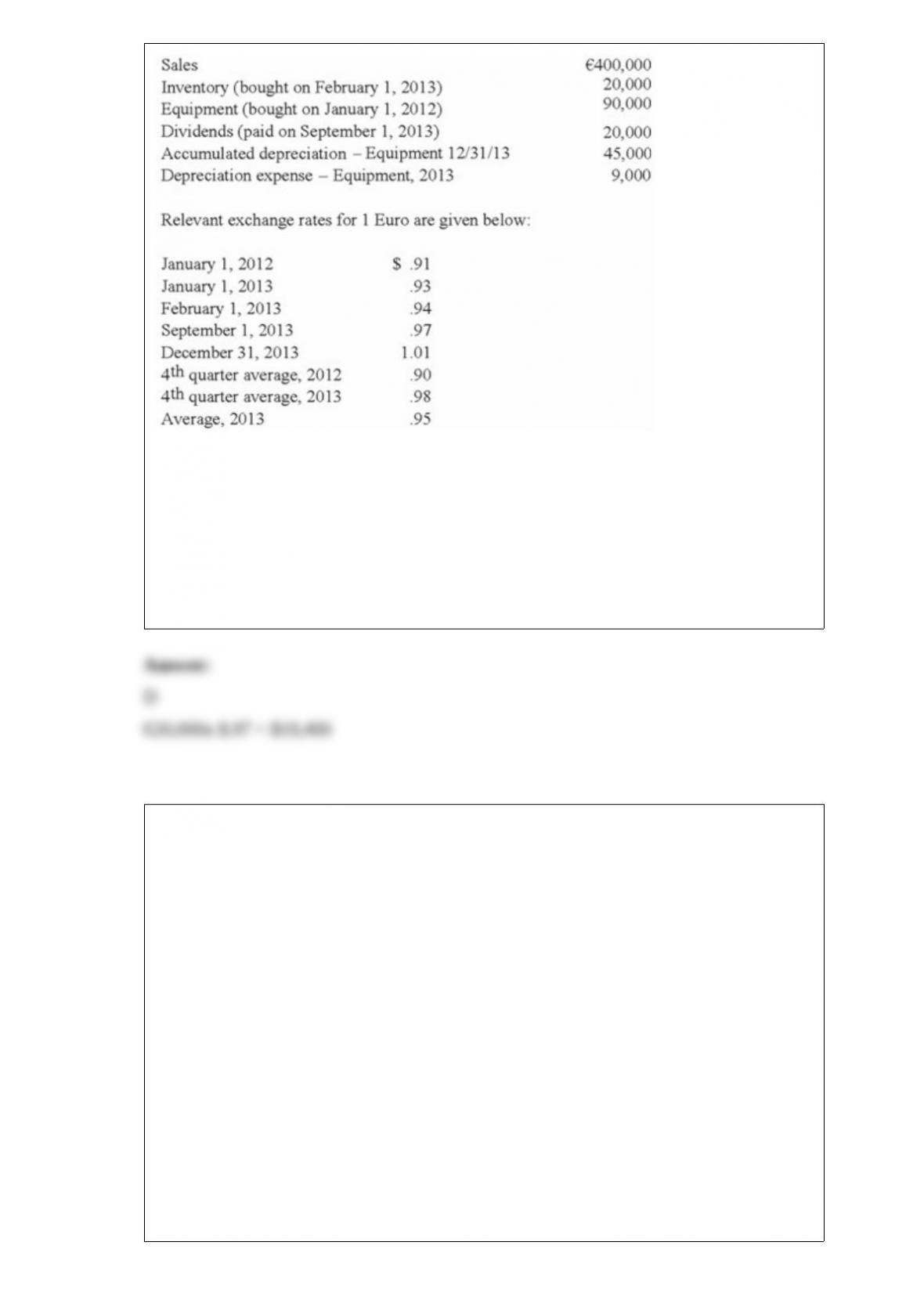

7) Quadros Inc., a Portuguese firm was acquired by a U.S. company on January 1,

2012. Selected account balances are available for the year ended December 31, 2013,

and are stated in Euro, the local currency.

Assume the functional currency is the Euro; compute the U.S. Statement of Retained

Earnings amount reported for Dividends in 2013.

A.$19,000

B.$20,200

C.$18,600

D.$19,400

E.$19,600

8) A partnership began its first year of operations with the following capital balances:

Young, Capital: $143,000

Eaton, Capital: $104,000

Thurman, Capital: $143,000

The Articles of Partnership stipulated that profits and losses be assigned in the

following manner:

Young was to be awarded an annual salary of $26,000 with $13,000 salary assigned to

Thurman.

Each partner was to be attributed with interest equal to 10% of the capital balance as of

the first day of the year.

The remainder was to be assigned on a 5:2:3 basis to Young, Eaton, and Thurman,

respectively.

Each partner withdrew $13,000 per year.

Assume that the net loss for the first year of operations was $26,000 with net income of

$52,000 in the second year.

What was the balance in Thurman’s Capital account at the end of the second year?

A.$133,380.

B.$84,760.

C.$105,690.

D.$132,860.

E.$71,760.

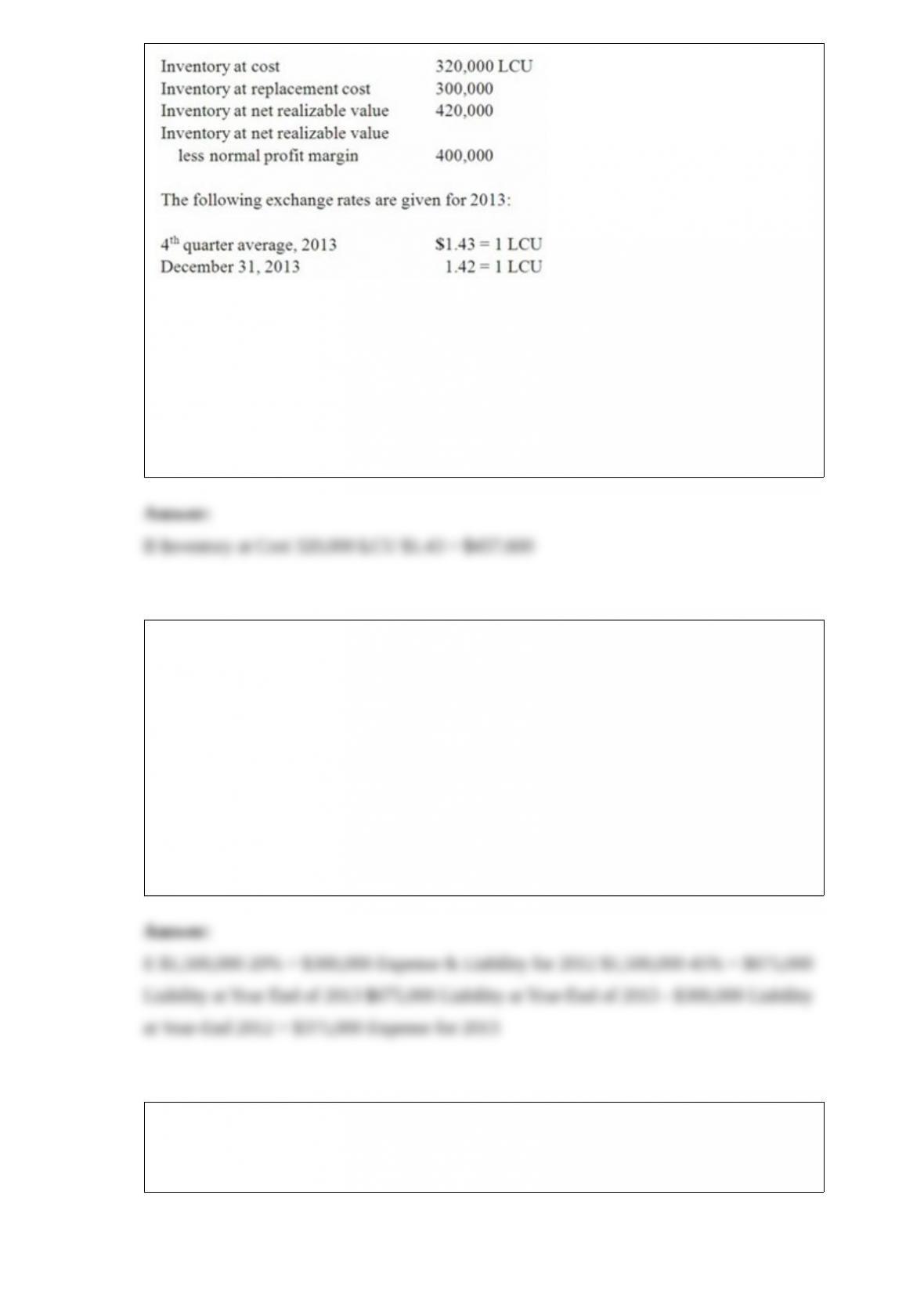

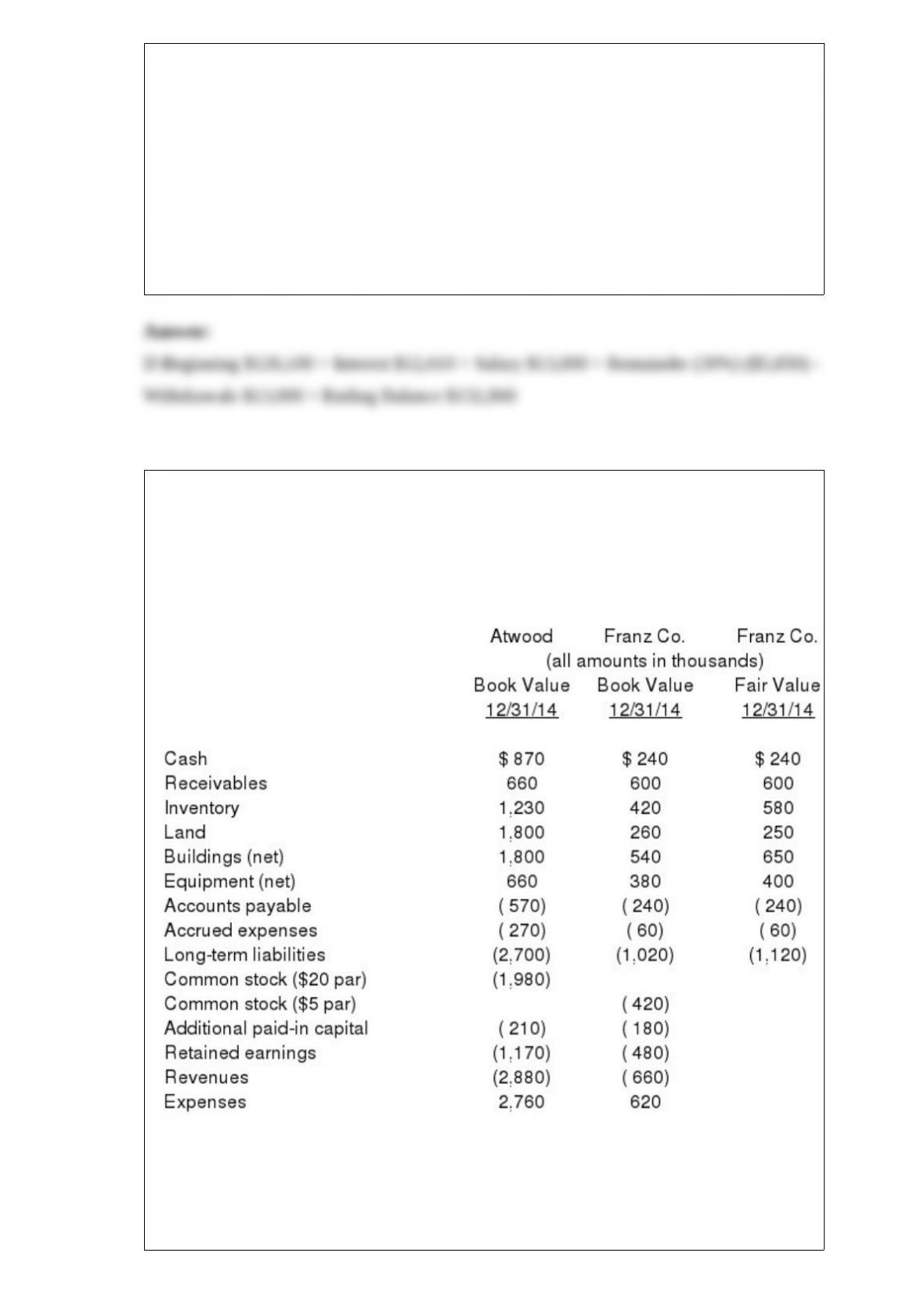

9) Presented below are the financial balances for the Atwood Company and the Franz

Company as of December 31, 2012, immediately before Atwood acquired Franz. Also

included are the fair values for Franz Company’s net assets at that date.

Note: Parenthesis indicate a credit balance

Assume a business combination took place at December 31, 2012. Atwood issued 50

shares of its common stock with a fair value of $35 per share for all of the outstanding

common shares of Franz. Stock issuance costs of $15 (in thousands) and direct costs of

$10 (in thousands) were paid to effect this acquisition transaction. To settle a difference

of opinion regarding Franz’s fair value, Atwood promises to pay an additional $5.2 (in

thousands) to the former owners if Franz’s earnings exceed a certain sum during the

next year. Given the probability of the required contingency payment and utilizing a 4%

discount rate, the expected present value of the contingency is $5 (in thousands).

Compute consolidated retained earnings as a result of this acquisition.

A) $1,160.

B) $1,170.

C) $1,265.

D) $1,280.

E) $1,650.

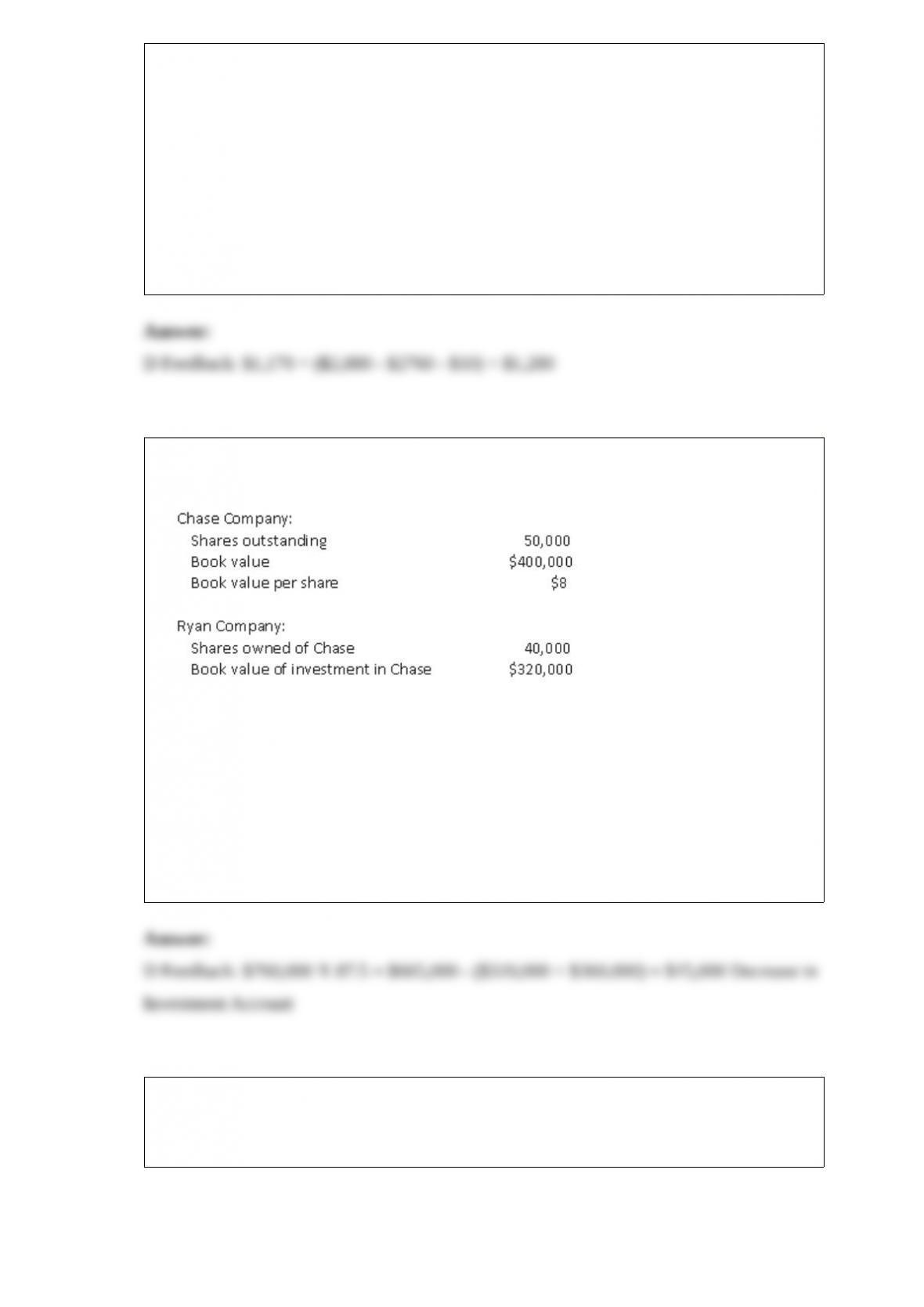

10) Ryan Company owns 80% of Chase Company. The original balances presented for

Ryan and Chase as of January 1, 2013, are as follows:

Assume Chase issues 30,000

additional shares common stock solely to Ryan for $12 per share.

After acquiring the additional shares, what adjustment is needed for Ryan’s investment

in Chase account?

A) $70,000 increase.

B) $70,000 decrease.

C) $15,000 increase.

D) $15,000 decrease.

E) No adjustment is necessary.

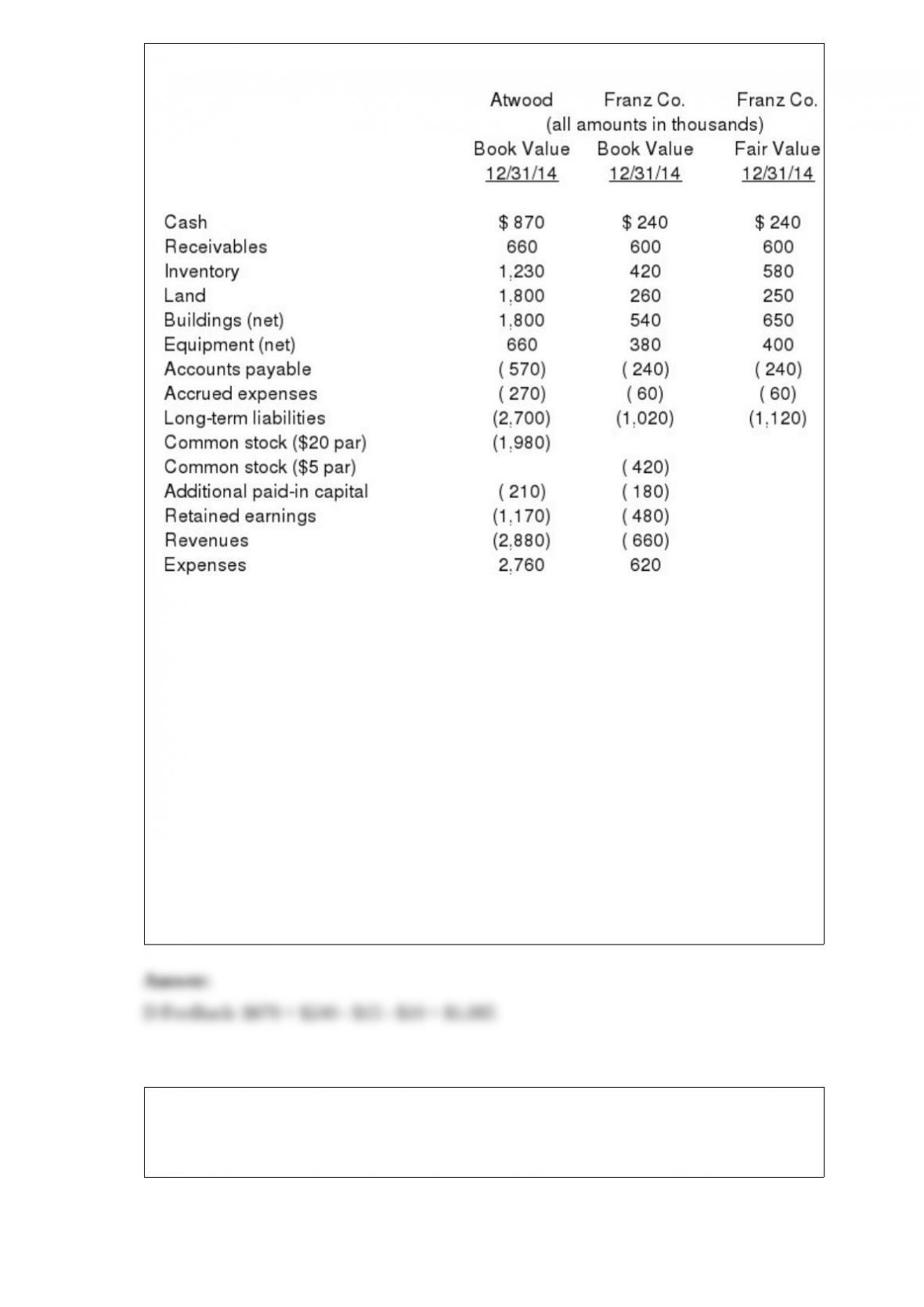

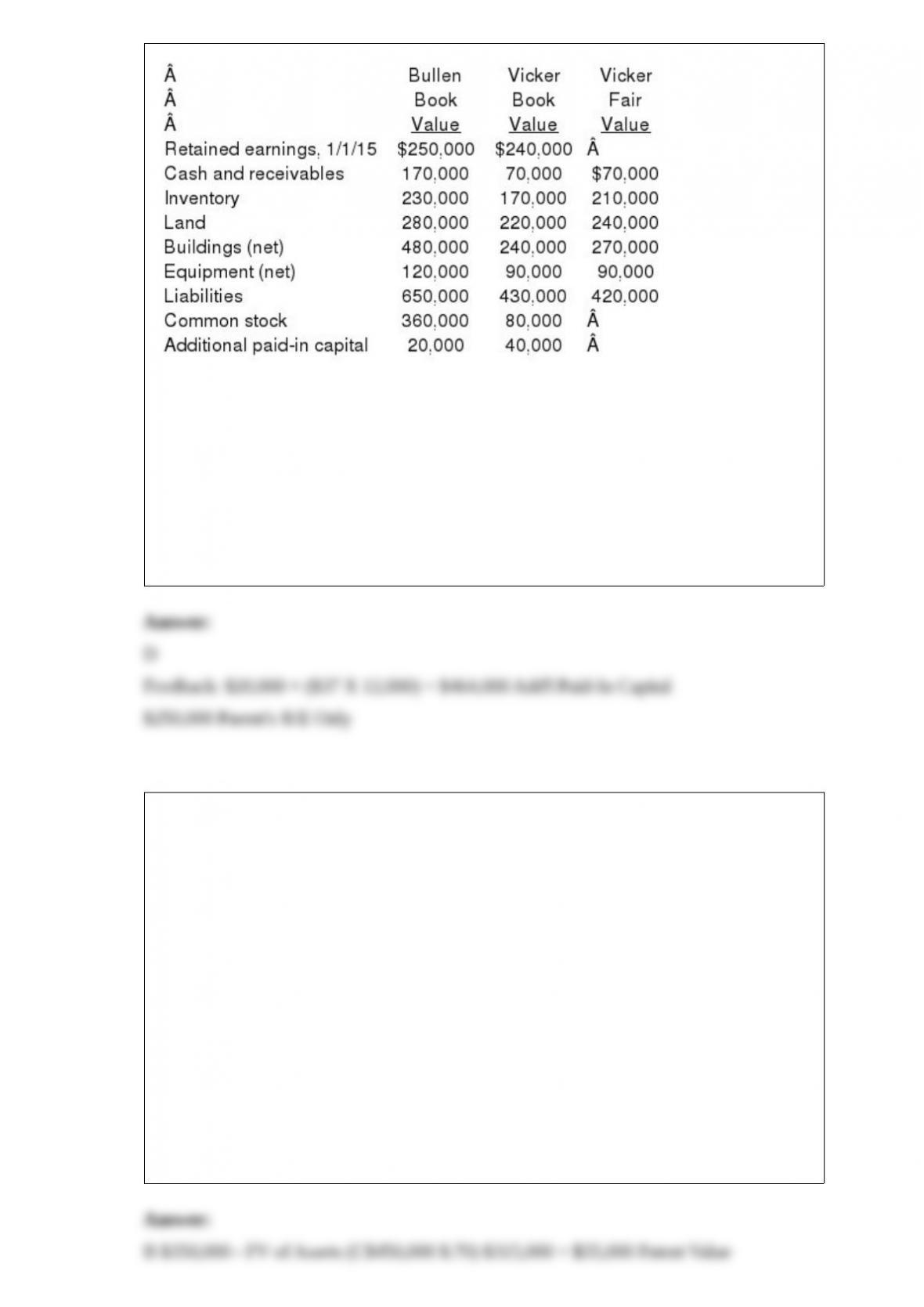

11) Bullen Inc. acquired 100% of the voting common stock of Vicker Inc. on January 1,

2013. The book value and fair value of Vicker’s accounts on that date (prior to creating

the combination) follow, along with the book value of Bullen’s accounts:

Assume that Bullen issued 12,000 shares of common stock with a $5 par value and a

$42 fair value for all of the outstanding shares of Vicker. What will be the consolidated

Additional Paid-In Capital and Retained Earnings (January 1, 2013 balances) as a result

of this acquisition transaction?

A) $60,000 and $490,000.

B) $60,000 and $250,000.

C) $380,000 and $250,000.

D) $464,000 and $250,000.

E) $464,000 and $420,000.

12) Kennedy Company acquired all of the outstanding common stock of Hastie

Company of Canada for U.S. $350,000 on January 1, 2013, when the exchange rate for

the Canadian dollar (CAD) was U.S. $.70. The fair value of the net assets of Hastie was

equal to their book value of CAD 450,000 on the date of acquisition. Any acquisition

consideration excess over fair value was attributed to an unrecorded patent with a

remaining life of five years. The functional currency of Hastie is the Canadian dollar.

For the year ended December 31, 2013, Hastie’s trial balance net income was translated

at U.S. $25,000. The average exchange rate for the Canadian dollar during 2013 was

U.S. $.68, and the 2013 year-end exchange rate was U.S. $.65

Calculate the U.S. dollar amount allocated to the patent at January 1, 2013

A.$50,000

B.$35,000

C.$34,000

D.$32,500

E.$28,200

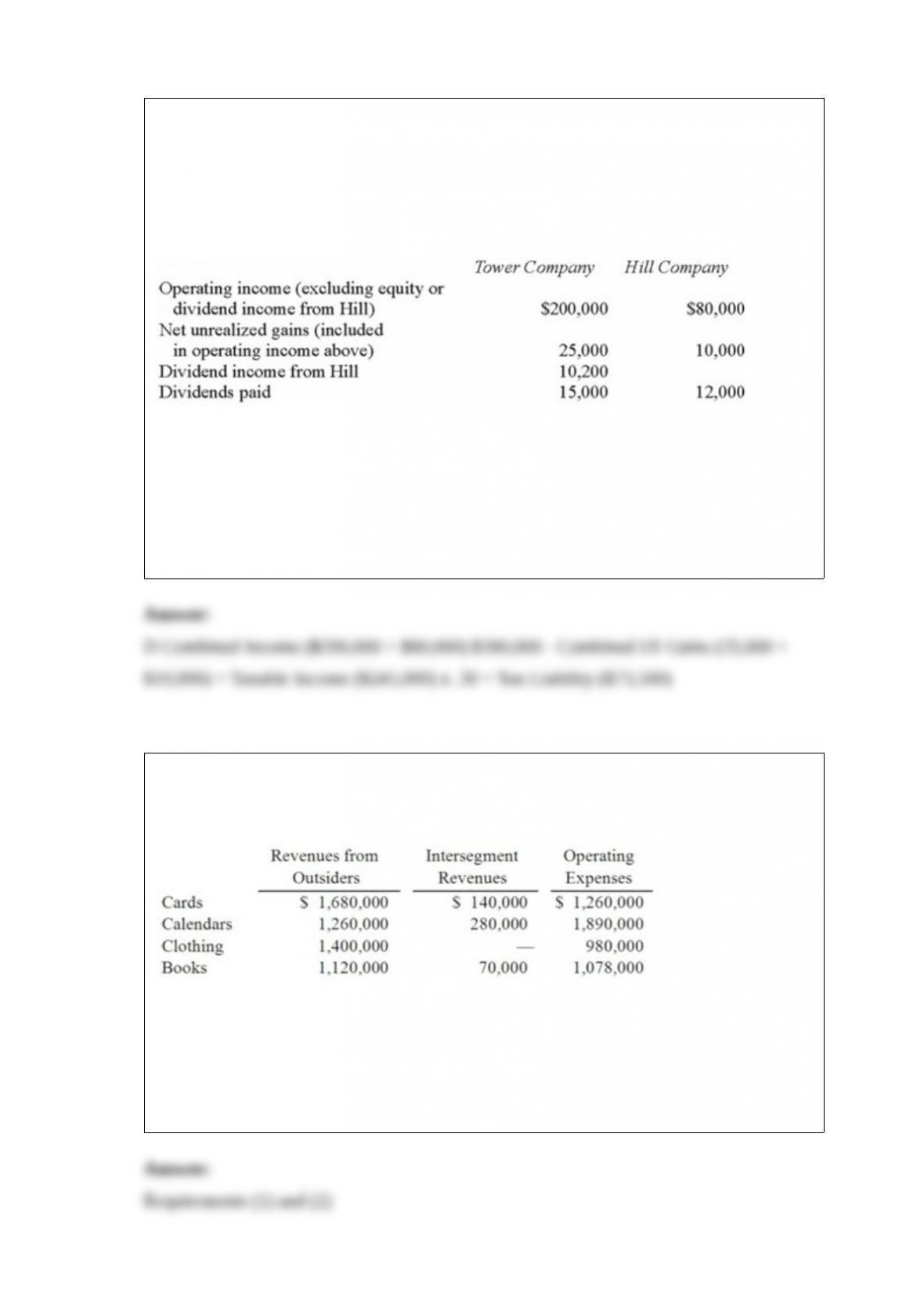

13) Tower Company owns 85% of Hill Company. The two companies engaged in

several intra-entity transactions. Each company’s operating and dividend income for the

current time period follow, as well as the effects of unrealized gains. No income tax

accruals have been recognized within these totals. The tax rate for each company is

30%.

What is the tax liability for the current year if consolidated tax returns are prepared?

A.$55,560.

B.$70,350.

C.$60,000.

D.$73,500.

E.$84,000.

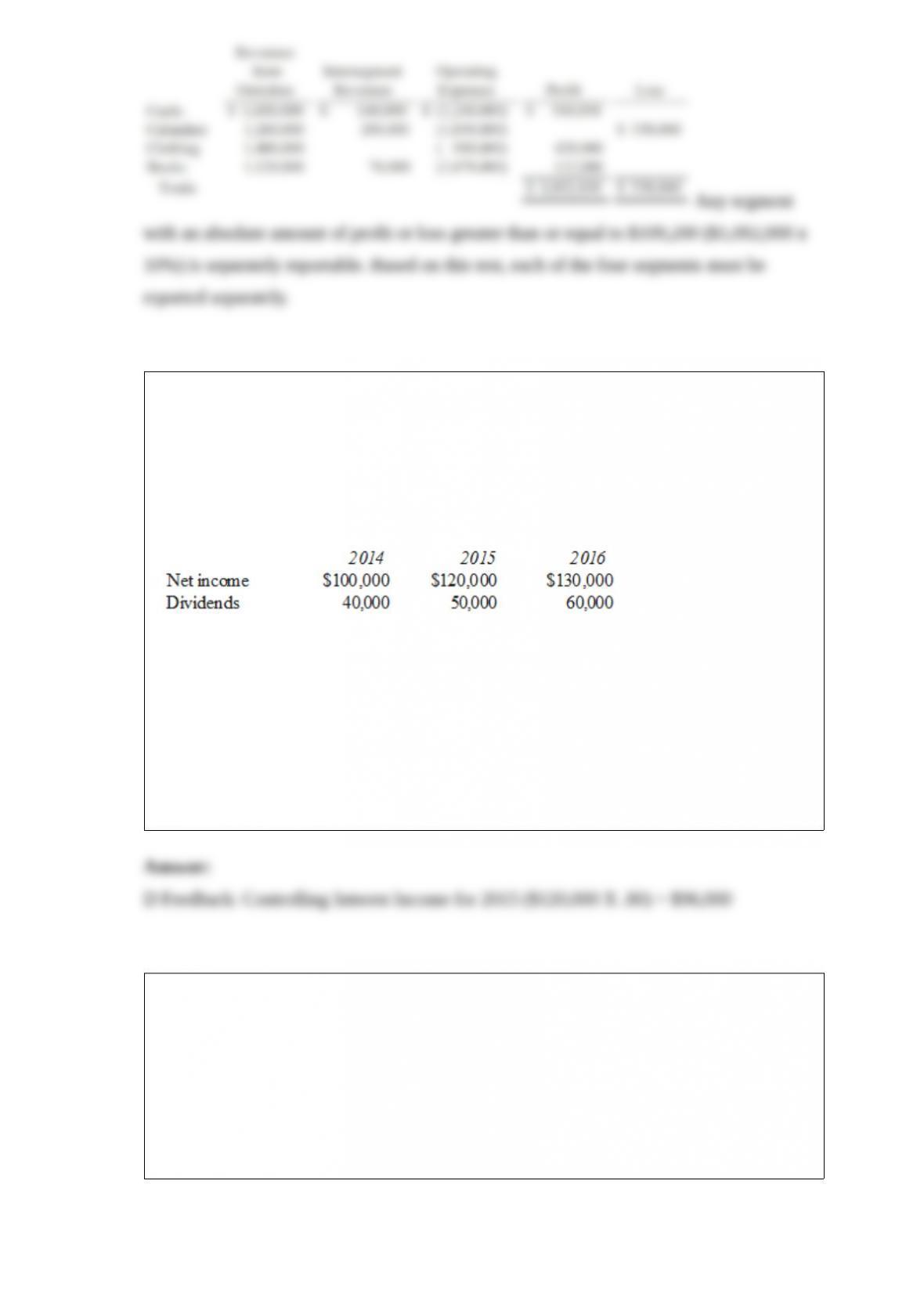

14) Burnside Corp. is organized into four operating segments. The following segment

information was generated by the internal reporting system in 2013:

Required:

1) What was the profit or loss of each of these segments?

2) Prepare the profit or loss test to determine which of these segments was separately

reportable.

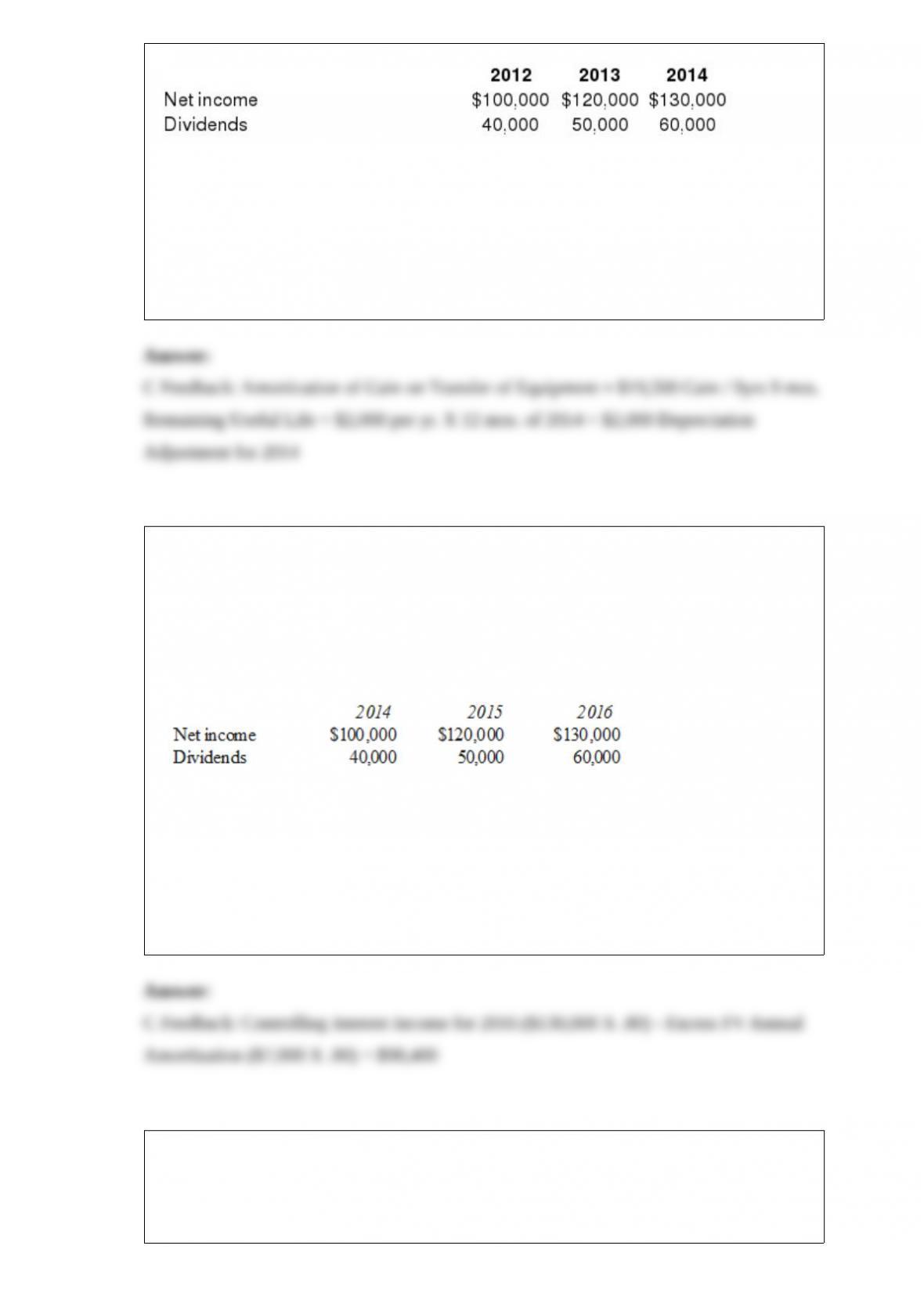

15) Pell Company acquires 80% of Demers Company for $500,000 on January 1, 2014.

Demers reported common stock of $300,000 and retained earnings of $210,000 on that

date. Equipment was undervalued by $30,000 and buildings were undervalued by

$40,000, each having a 10-year remaining life. Any excess consideration transferred

over fair value was attributed to goodwill with an indefinite life. Based on an annual

review, goodwill has not been impaired.

Demers earns income and pays dividends as follows:

Assume the PARTIAL EQUITY method is applied.

How much does Pell record as income from Demers for the year ended December 31,

2015?

A) $90,400.

B) $89,000.

C) $50,400.

D) $96,000.

E) $56,000.

16) Wilson owned equipment with an estimated life of 10 years when it was acquired

for an original cost of $80,000. The equipment had a book value of $50,000 at January

1, 2012. On January 1, 2012, Wilson realized that the useful life of the equipment was

longer than originally anticipated, at ten remaining years.

On April 1, 2012 Simon Company, a 90% owned subsidiary of Wilson Company,

bought the equipment from Wilson for $68,250 and for depreciation purposes used the

estimated remaining life as of that date. The following data are available pertaining to

Simon’s income and dividends:

Compute the amortization of gain through a depreciation adjustment for 2014 for

consolidation purposes.

A) $1,925.

B) $1,825.

C) $2,000.

D) $1,500.

E) $7,000.

17) Pell Company acquires 80% of Demers Company for $500,000 on January 1, 2014.

Demers reported common stock of $300,000 and retained earnings of $210,000 on that

date. Equipment was undervalued by $30,000 and buildings were undervalued by

$40,000, each having a 10-year remaining life. Any excess consideration transferred

over fair value was attributed to goodwill with an indefinite life. Based on an annual

review, goodwill has not been impaired.

Demers earns income and pays dividends as follows:

Assume the EQUITY METHOD is applied.

Compute Pell’s income from Demers for the year ended December 31, 2016.

A) $50,400.

B) $56,000.

C) $98,400.

D) $97,000.

E) $104,000.

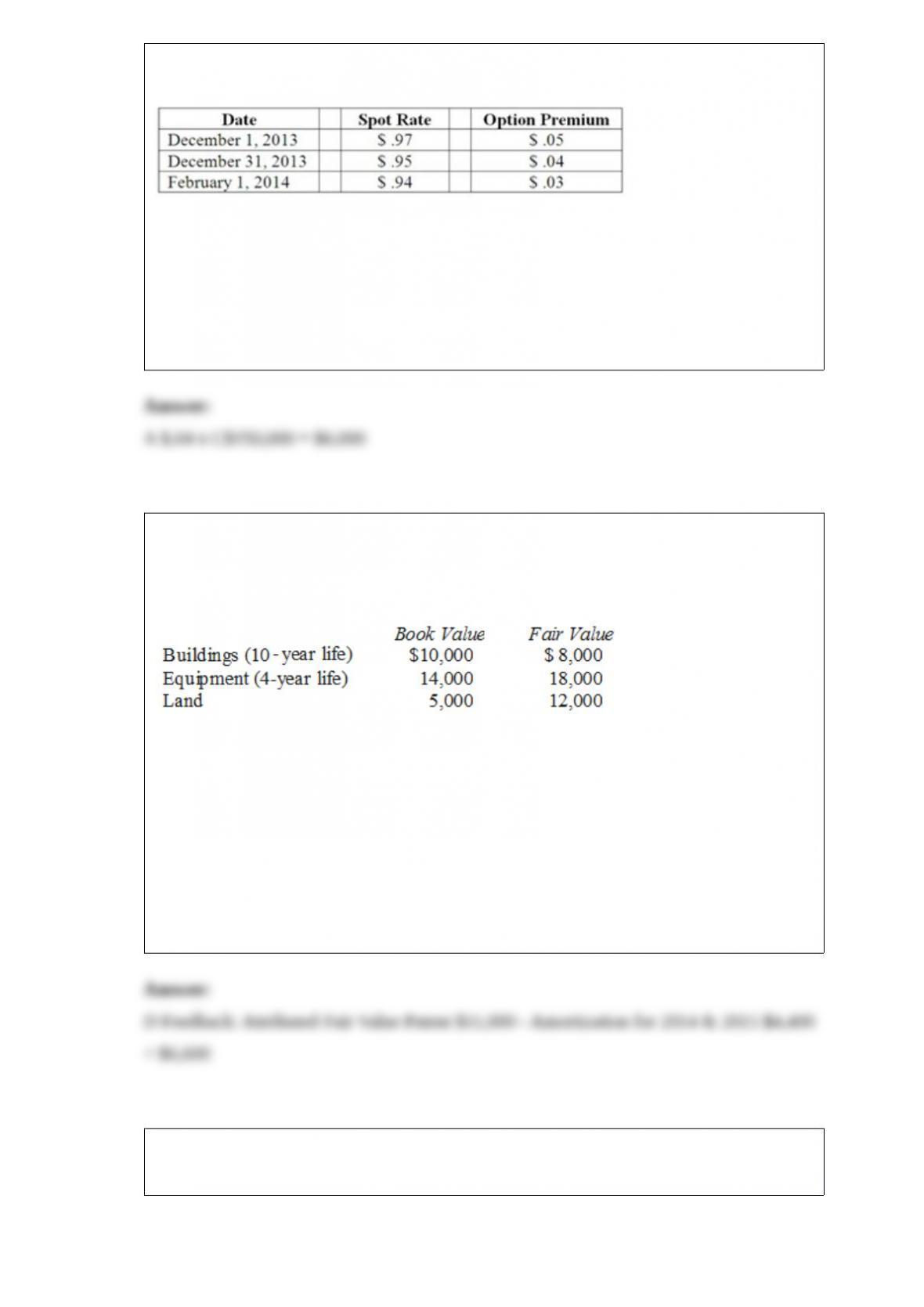

18) On December 1, 2013, Keenan Company, a U.S. firm, sold merchandise to Velez

Company of Canada for 150,000 Canadian dollars (CAD). Collection of the receivable

is due on February 1, 2014. Keenan purchased a foreign currency put option with a

strike price of $.97 (U.S.) on December 1, 2013. This foreign currency option is

designated as a cash flow hedge. Relevant exchange rates follow:

Compute the fair value of the foreign currency option at December 31, 2013

A.$6,000

B.$4,500

C.$3,000

D.$7,500

E.$1,500

19) McGuire Company acquired 90 percent of Hogan Company on January 1, 2014, for

$234,000 cash. This amount is reflective of Hogan’s total fair value. Hogan’s

stockholders’ equity consisted of common stock of $160,000 and retained earnings of

$80,000. An analysis of Hogan’s net assets revealed the following:

Any excess consideration transferred over fair value is attributable to an unamortized

patent with a useful life of 5 years.

In consolidation at December 31, 2015, what net adjustment is necessary for Hogan’s

Patent account?

A) $4,200.

B) $5,500.

C) $8,000.

D) $6,600.

E) No adjustment is necessary.

20) How are direct and indirect costs accounted for when applying the acquisition

method for a business combination?

21) Steven Company owns 40% of the outstanding voting common stock of Nicole

Corp. and has the ability to significantly influence the investee’s operations. On January

3, 2013, the balance in the Investment in Nicole Corp. account was $503,000.

Amortization associated with this acquisition is $12,000 per year. During 2013, Nicole

earned net income of $120,000 and paid cash dividends of $40,000. Previously in 2012,

Nicole had sold inventory costing $35,000 to Steven for $50,000. All but 25% of that

inventory had been sold to outsiders by Steven during 2012. Additional sales were

made to Steven in 2013 at a transfer price of $75,000 that had cost Nicole $54,000.

Only 10% of the 2013 purchases had not been sold to outsiders by the end of 2013.

What amount of equity income would Steven have recognized in 2013 from its

ownership interest in Nicole?

22) Steven Company owns 40% of the outstanding voting common stock of Nicole

Corp. and has the ability to significantly influence the investee’s operations. On January

3, 2013, the balance in the Investment in Nicole Corp. account was $503,000.

Amortization associated with this acquisition is $12,000 per year. During 2013, Nicole

earned net income of $120,000 and paid cash dividends of $40,000. Previously in 2012,

Nicole had sold inventory costing $35,000 to Steven for $50,000. All but 25% of that

inventory had been sold to outsiders by Steven during 2012. Additional sales were

made to Steven in 2013 at a transfer price of $75,000 that had cost Nicole $54,000.

Only 10% of the 2013 purchases had not been sold to outsiders by the end of 2013.

What amount of unrealized intra-entity inventory profit should be deferred by Steven at

December 31, 2012?

23) A partnership held three assets: Cash, $13,000; Land, $45,000; and a Building,

$65,000. There were no recorded liabilities. The partners anticipated that expenses

required to liquidate their partnership would amount to $6,000. Capital balances were

as follows:

King, Capital: $32,700

Murphy, Capital: 36,400

Madison, Capital: 26,000

Pond, Capital: 27,900

The partners shared profits and losses 30:30:20:20, respectively.

Required:

Prepare a proposed schedule of liquidation, showing how cash could be safely

distributed to the partners at this time.

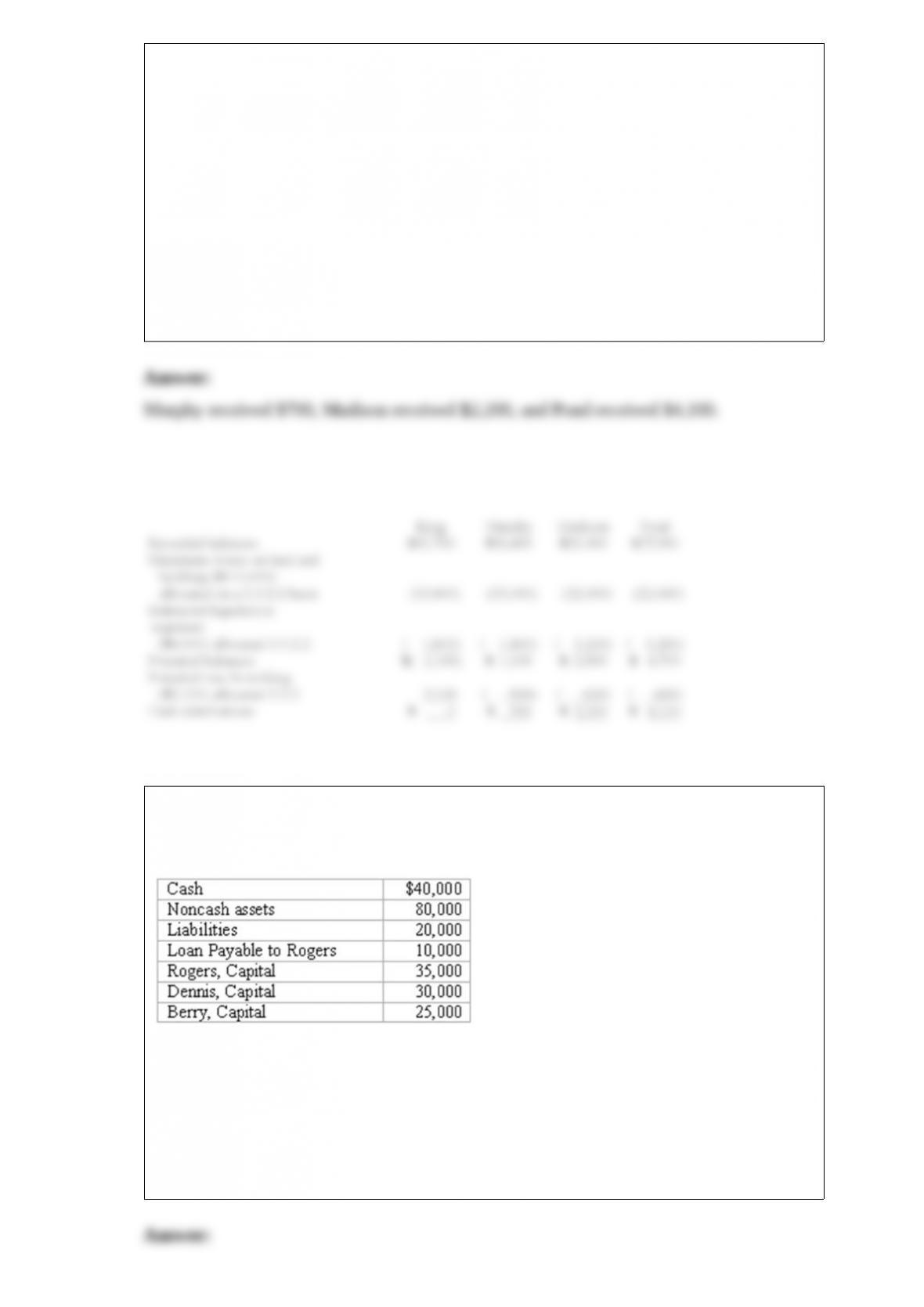

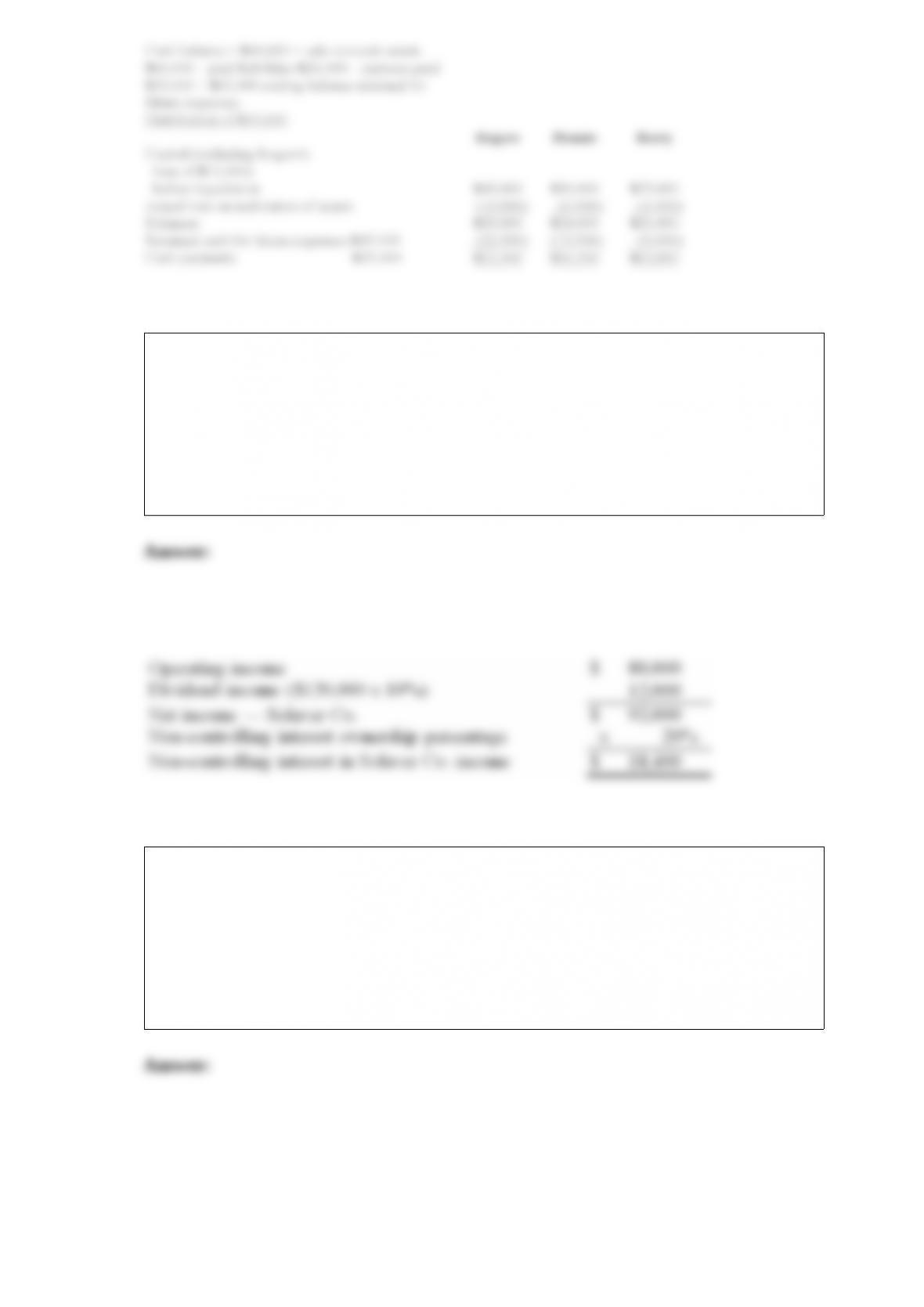

24) The balance sheet of Rogers, Dennis & Berry LLP prior to liquidation included the

following:

The three partners shared net income and losses in a 5:3:2 ratio, respectively. Noncash

assets were sold for $60,000. Creditors were paid in full, partners were paid $35,000,

and the balance of cash was retained pending future developments.

Determine the cash to be retained and prepare a schedule to distribute $35,000 cash to

the partners.

25) Jull Corp. owned 80% of Solaver Co. Solaver paid $250,000 for 10% of Jull’s

common stock. In 2013, Jull and Solaver reported operating income (not including

income from the investment) of $300,000 and $80,000, respectively. Jull and Solaver

paid dividends of $120,000 and $50,000, respectively.

Under the treasury stock approach, what is the non-controlling interest in Solaver Co.’s

net income?

26) On January 1, 2012, Jumper Co. acquired all of the common stock of Cable Corp.

for $540,000. Annual amortization associated with the purchase amounted to $1,800.

During 2012, Cable earned net income of $54,000 and paid dividends of $24,000.

Cable’s net income and dividends for 2013 were $86,000 and $24,000, respectively.

Required:

Assuming that Jumper decided to use the partial equity method, prepare a schedule to

show the balance in the investment account at the end of 2013.

27) Fesler Inc. acquired all of the outstanding common stock of Pickett Company on

January 1, 2012. Annual amortization of $22,000 resulted from this transaction. On the

date of the acquisition, Fesler reported retained earnings of $520,000 while Pickett

reported a $240,000 balance for retained earnings. Fesler reported net income of

$100,000 in 2012 and $68,000 in 2013, and paid dividends of $25,000 in dividends

each year. Pickett reported net income of $24,000 in 2012 and $36,000 in 2013, and

paid dividends of $10,000 in dividends each year.

Assume that Fesler’s reported net income includes Equity in Subsidiary Income.

If the parent’s net income reflected use of the equity method, what were the

consolidated retained earnings on December 31, 2013?

28) Carnes Co. decided to use the partial equity method to account for its investment in

Domino Corp. An unamortized trademark associated with the acquisition was $30,000,

and Carnes decided to amortize the trademark over ten years. For 2013, Carnes’ Equity

in Subsidiary Earnings was $78,000.

Required:

What balance would have been in the Equity in Subsidiary Earnings account if Carnes

had used the equity method?