33.(15 Minutes) (The effect that various events have on a consolidated statement of

cash flows.)

Sale of building. The $44,000 in cash received from the sale is listed as a

cash inflow within the company’s investing activities. If the company is

using the direct method in presenting cash flows from operating activities,

the $12,000 gain is not presented. However, if the indirect method is used,

the gain (a positive) must be eliminated from net income by a subtraction.

Decrease in accounts payable. Cash payments have reduced this liability

balance during the period. If the direct method is used to present cash flows

from operating activities, the change is added to cost of goods sold as one

step in deriving the cash paid during the period for inventory (an outflow). If

the indirect method is applied, the decrease is subtracted from net income in

34.(20 Minutes) (Determine cash flows from operations for a consolidated entity.)

DIRECT METHOD

Cash revenues (add book values, eliminate intra-entity transfers,

and add decrease in accounts receivable) ……………………………… $648,000

Cash inventory purchases (add book values, eliminate

intra-entity transfers, eliminate unrealized gains, add increase in

INDIRECT METHOD

Consolidated net income (computed below) ……………………………….. $216,000

Adjustments:

Depreciation and amortization …………….……………………..…..… 61,000

Gain on sale of equipment …………….………………………………….. (30,000)

Consolidated Net Income = $206,200 + 9,800 = $216,000 or computation below:

Revenues (add book values and subtract intra-entity transfers) $640,000

Cost of goods sold (add book values, less intra-entity

transfers and beginning unrealized gain, plus ending

unrealized gain) ………………………………………….….…..…..…..…... (353,000)

Depreciation and amortization (add book values plus

35. (30 Minutes) (Compute basic and diluted earnings per share for a parent and its

100 percent owned subsidiary, both with convertible bonds.)

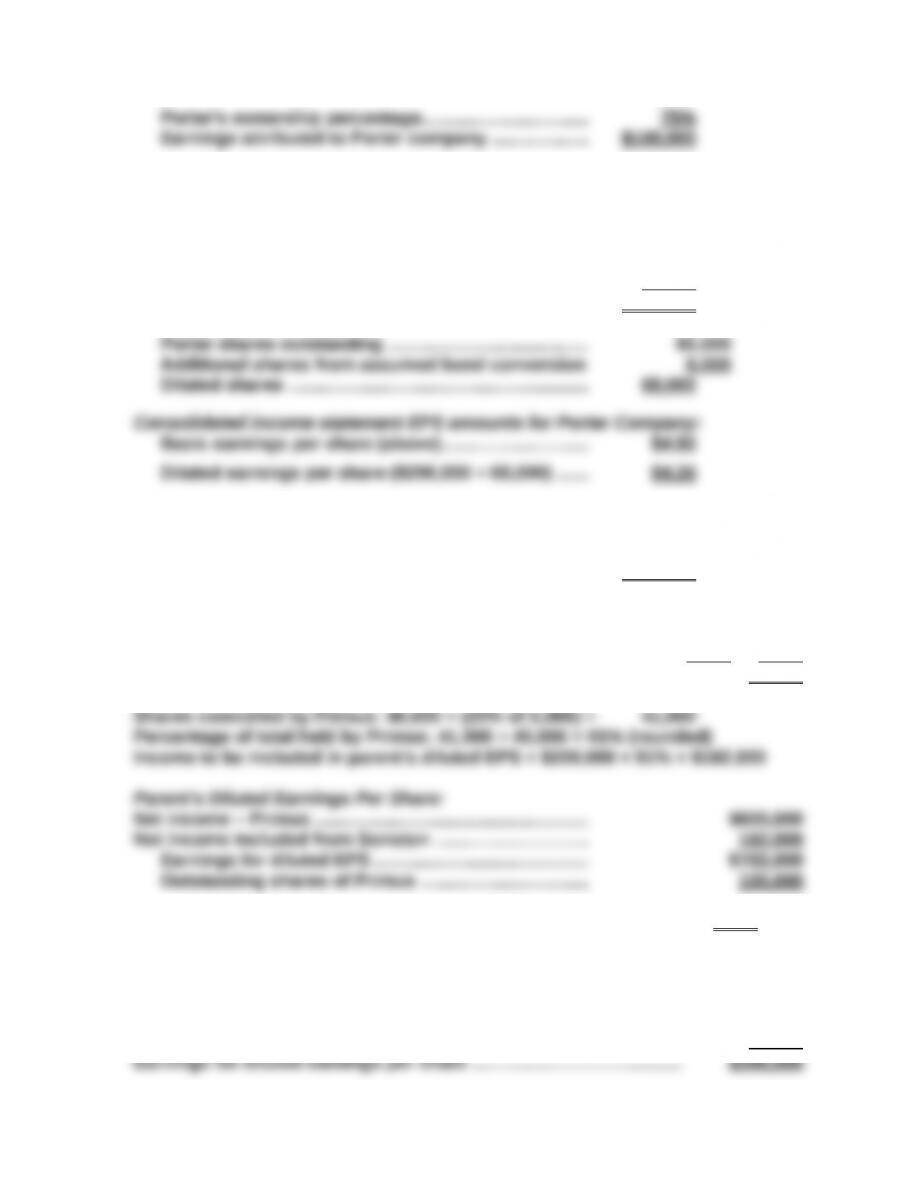

Basic EPS—Porter Company:

Porter’s reported net income ………………..…..…..…... $150,000

Street’s reported net income …………………………….... 130,000

Diluted EPS—Street Company

Street earnings after amortization…………..…………... $120,000

Shares outstanding …………..…………………………..…... 30,000

Basic earnings per share (120,000 ÷ 30,000) ……..… $4.00

Street’s earnings assuming conversion of its bonds

Porter’s share of Street’s diluted earnings:

Total shares assuming Street bond conversion ..... 40,000

Shares owned by Porter…………..……………….…..….... 30,000

Porter’s earnings and shares for diluted EPS:

Porter’s separate net income …………..…………..…..… $150,000

Street’s income applicable to Porter (above).….…... 108,000

Interest saved (net of tax) on assumed

………..…………………………….…..…..….…..…...conversion of Porter’s

bonds …………………………………….…..…..…..…..…... 32,000

Diluted earnings to Porter…………………….…..…..….... $290,000

36. (15 Minutes) (Compute diluted EPS. Subsidiary has stock warrants outstanding)

Figures For Sonston’s Diluted EPS

Net Income ………..…………………………….…..…..….…..…... $200,000

Shares outstanding …………..……………………..….…..…..… 40,000

Assumed conversion of stock warrants .…..…..…..….... 10,000

Repurchase of treasury stock with proceeds of stock

Warrants (10,000 × $10 = $100,000 ÷ $20) …….…........... (5 ,000) 5,000

Shares for diluted earnings per share computation..... 45,000

PARENT’S DILUTED EARNINGS PER SHARE = $782,000 ÷ 100,000 = $7.82

37. (15 Minutes) (Compute diluted EPS. Subsidiary has convertible bonds.)

Figures for Simon’s diluted EPS:

Net income ………..……………………………………………………………………. $290,000

Interest (net of tax) saved from assumed conversion ………..…..…. 56,000

Shares outstanding …………..…………………………………..…..…..….….... 80,000

Assumed conversion of bonds ……………….…………………..…..…..….. 30,000

Subsidiary shares for parent’s share of diluted earnings…….…..… 110,000

Shares controlled by Garfun = 80,000 ÷ 110,000 = 73% (rounded)

Income to be included in parent’s diluted EPS = $346,000 × 73% = $252,580

Earnings for parent’s diluted earnings per share:

PARENT’S DILUTED EARNINGS PER SHARE = $717,580 ÷ 80,000 = $8.97 (rounded)

38. (35 Minutes) (Compute basic and diluted earnings per share for parent

company. Subsidiary has stock warrants and convertible bonds.)

Basic EPS—Parent Company ( Burks ):

Reported net income (separate)—Burks ..…..….…..…...... $150,000

Foreman net income: 80% × ($120,000 – $40,000 amort.)……… 64,000

Diluted EPS—Parent Company ( Burks )

Subsidiary income for Burks’ EPS:

Net income after amortization ($120,000 – 40,000)…………. $80,000

Interest (net of tax) saved assuming bond conversion.. 45 ,000

Income applicable to diluted EPS …..…..…..…..…..…... $125 ,000

Shares applicable to diluted EPS …………………….….... 55 ,000

Shares controlled by parent:

(40,000 × 80%) plus (10% × 10,000) ……………..….…..… 33 ,000

Income used in diluted EPS computation …..…..….......... $125,000

Earnings applicable to Burks’ diluted EPS:

Because of assumed conversion, preferred stock

dividends would not be paid ……………………………….... -0 –

Earnings applicable to diluted EPS ………………...…..….…. $220 ,500

Burks’ outstanding shares …………….………..…..…..…..…... 65,000

38. (continued)

Alternative derivation of Burks’ diluted EPS:

Consolidated net income $150,000 + ($120,000 – $40,000) $(230,000)

Consolidated interest saved (net of 10% intra-entity interest) (40 ,500)

Consolidated net income assuming bond conversion (270,500)

Subsidiary net income $(120,000)

Excess fair value amortization 40,000

Subsidiary interest saved (100%) (45 ,000)

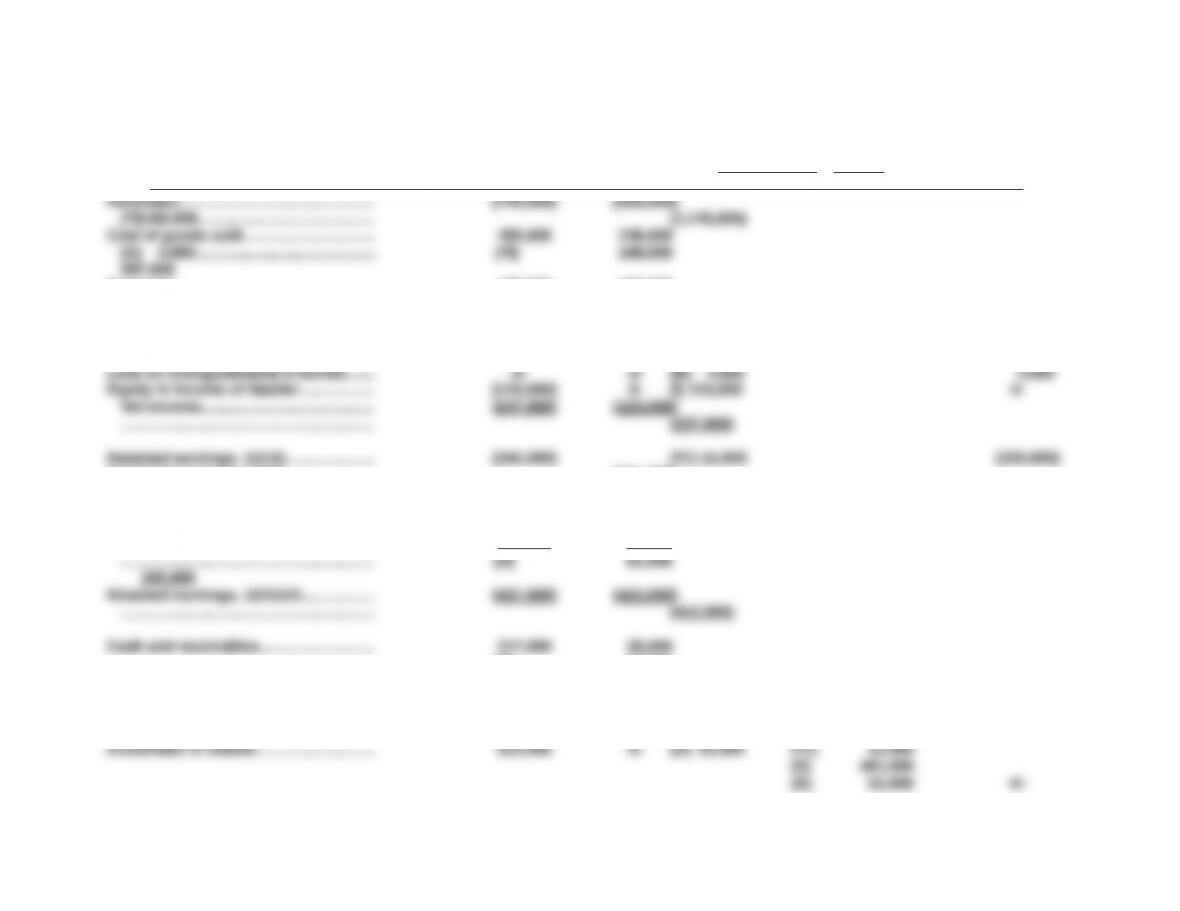

39. (8 Minutes) (Effect of subsidiary stock issuance to public at a price above

reported value per share)

Equity method investment prior to Ricardo share issue $490,000

Parent’s ownership percentage………….…..…..…..….…... 100%

Fair value ownership equivalency…………..…..…..….…... $490,000

Adjusted subsidiary fair value after new share issue

40. (20 Minutes) (Effects of two different stock issuances by subsidiary.)

a. Prior to the issuance of the new shares, Albuquerque owns an 80% interest in

Marmon (16,000 shares out of 20,000 shares). The adjusted acquisition-date fair

value is $840,000 ($600,000 + $150,000 + $90,000). After the stock issue, the

Investment in Marmon ………………………….….…..….... 16,000

Additional Paid-In Capital ……………..….…..…..….. 16,000

40.(continued)

b. Albuquerque’s adjusted acquisition-date fair value is $840,000 (see above) prior

to the issuance of the new shares. The 4,000 additional shares increase

subsidiary’s total value by $132,000 (the price of the stock) to $972,000.

41.(55 Minutes) (Prepare consolidation entries following a subsidiary stock issue to

outside parties.)

Initially, Aronsen owns 18,000 shares (or 90%) of Siedel’s outstanding shares

(the total number of shares can be determined by dividing the subsidiary’s

common stock account by the $10 per share par value). After issuing 4,000

Excess Acquisition-Date Fair Value Allocation and Amortization

Fair value (consideration transferred plus NCI fair value) .......... $649,000

Acquisition-date book value……………..…………………….…..…..…..… (480 ,000)

Fair value in excess of book value ……………….………………….…..… $169,000

Annual amortization ………….…………………………………………………… $ 5 ,000

Adjustment for Stock Transaction

Adjusted acquisition-date fair value of subsidiary

on new issue date ($649,000 + $90,000 + $152,000) ……………. $891,000

Adjusted parent ownership (18,000 shares ÷ 24,000 shares) …… 75%

Parent’s post-issue equity method value at 1/1/14 .…..…........ $668,250

Equity method balance before new subsidiary stock issue

41. (continued)

Consolidation worksheet entries:

Entry *C

Investment in Siedel …………..………………………………. 81,000

Retained Earnings, 1/1/14 (Aronsen) ..….…..….... 81,000

(To record adjustment for subsidiary stock

transaction; computation shown above.)

Entry S

Common Stock (Siedel) …………….………………..…..…. 240,000

Additional Paid-In Capital (Siedel) ……………….……… 112,000

(To eliminate subsidiary stockholders’ equity accounts

against Investment account and to recognize noncontrolling

interest. Stockholders’equity balances have been adjusted

for increase in book value during 2012–2013 and the issuance

by the subsidiary of 4,000 shares of stock on 1/1/14.)

Entry A

Land ………..……………………………………………………….. 89,000

2012–2013 amortization to arrive at 1/1/14 balance.

NCI now reflects 25% of the unamortized 1/1/14 balance.)

Entry I

Dividend Income ………….…………………………………….. 15,000

Dividends Declared ……………………………………….. 15,000

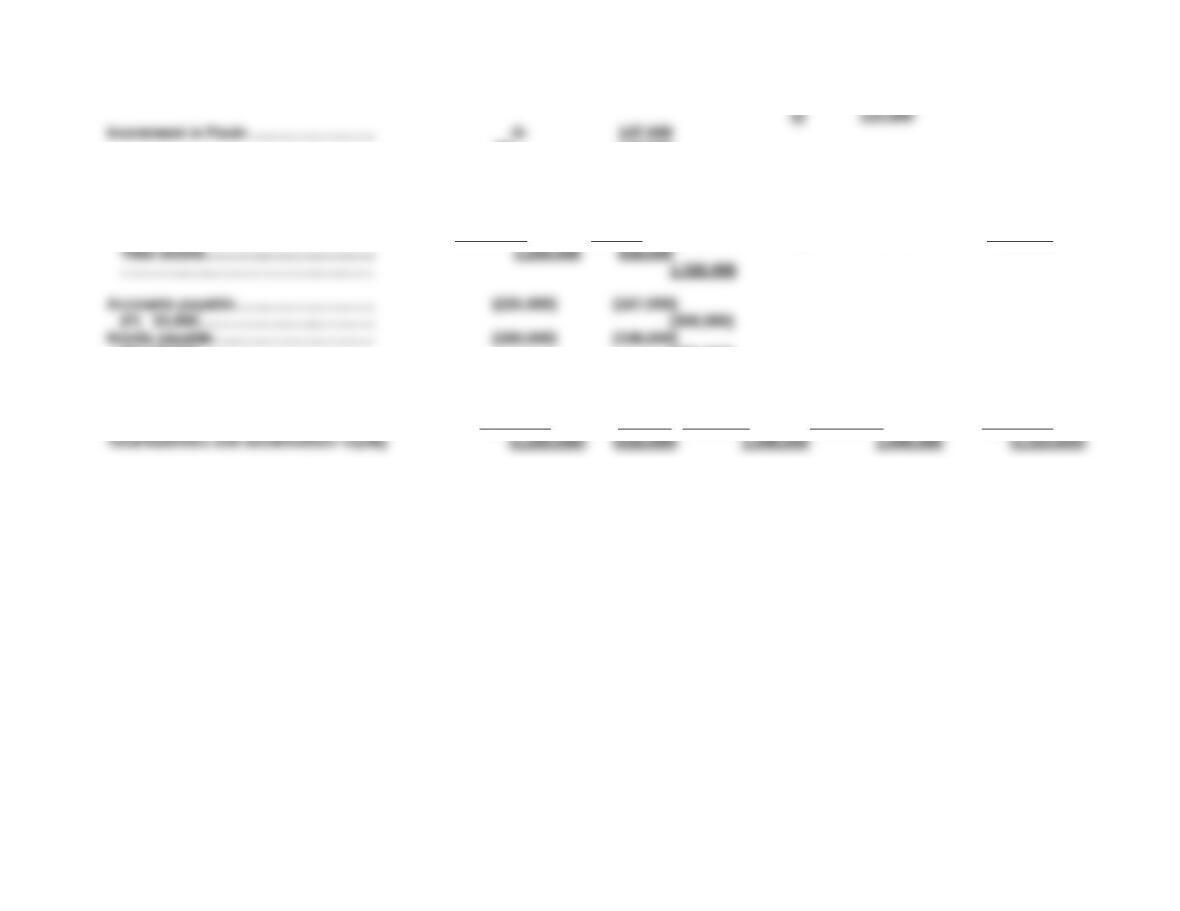

42. (50 Minutes) (Prepare consolidation worksheet for business combination. Intra-

entity bond acquisition is made during the current year.)

Acquisition-date fair-value allocation and amortization:

Equipment $30,000 10-year life $3,000 annual amortization

Trademarks $40,000 20-year life $2,000 annual amortization

As indicated in the problem, the parent is applying the partial equity method.

Hence an Entry *C must be recorded on the worksheet to convert the recorded

figures (amortization is needed for the three years prior to 2015) to equity

balances:

Amortization expense ($5,000 × 3 years) = ………….. $15,000 (Entry *C)

Unrealized gain in ending inventory (downstream):

Equivalent book value …………….…………………………….… $141,000

Amount paid ………………………………………………..…..…. 145,500

Loss on extinguishment of bonds ………………….…..…... $ 4,500 (Entry B)

Amortization during 2015 changed the carrying value of the bond payable from

$282,000 to $288,000 (found in the balance sheet) and the investment from

$145,500 to $147,000. This amortization also affects interest income and

expense accounts.

42.(continued) Pavin and Stabler

Consolidation Worksheet

Year Ending December 31, 2015

Consolidation Entries Consolidated

Accounts Pavin Stabler Debit Credit Totals

Expenses…………….…………....…....…..… 125,000 158,500

(E) 5,000…………………………..………… 288,500

Interest expense—bonds …....…..…..... 36,000 -0- (B) 18,000 18,000

Interest income—bond investment..... -0- (16,500)

(B) 16,500………………………………..….. -0-

Retained earnings, 1/1/15…………..….... (361,000)

(S) 361,000…………………………….…….. -0-

Net income (above)………..……….…..….. (247,000) (123,000)

……………………………………………………. (237,000)

Dividends declared………….…...…....….. 155 ,000 61 ,000

……………………………………………………. (P) 33,000

219,000

Inventory………………………………………... 175,000 87,000

……………………………………………………. (G) 2,000

260,000

……………………………………………………. (B) 147,000

-0-

Land, buildings, and equipment (net). 245,000 541,000

(A) 21,000………………………………..….. (E) 3,000

804,000

Trademarks…………………………………….. -0 – -0- (A) 34,000 (E) 2,000 32 ,000

(B) 150,000……………………………….….. (250,000)

Discount on bonds…......…..…..…....….. 12,000 -0- (B) 6,000 6,000

Common stock……………………..…..….... (300,000) (120,000)

(S) 120,000…………..………………..…..… (300,000)

Retained earnings (above)…..…....….... (437 ,000) (423 ,000) (412 ,000)