Part b — FUND FINANCIAL STATEMENTS

STATEMENT OF REVENUES, EXPENDITURES

AND CHANGES IN FUND BALANCE

For the Year Ended December 31, 2015

General Fund

Revenues

—Property Taxes $370,000

—Student Fees 3 ,000

Total Revenues $373,000

Expenditures

Change in Fund Balance $ 99,000

Fund Balance—Beginning of Year – 0 –

Fund Balance—End of Year $ 99 ,000

BALANCE SHEET

December 31, 2015

General Fund

Assets

—Cash $ 53,000

—Property Tax Receivable 80 ,000

Total Assets $133 ,000

Total Liabilities, Deferred Inflows of

Resources, and Fund Balance $133 ,000

45. (25 Minutes) (Assessing the impact of various government transactions.)

a. This statement is false. Internal service funds are included in

b. This statement is false because not enough information is available to

say that this fund “must be” reported as a major fund. The asset balance

($32,000) for this governmental fund is larger than 10 percent of the total assets

c. This statement is false. If (a) the user charge is the sole security for

the debts of the bus system or (b) the activity’s costs are required to be

recovered through the fee or (c) the fee is set to recover the activity’s costs, then

d. This statement is true. To record a budget so that the projected

e. This statement is false. To record a budget so that the projected

increase or decrease in fund balance will be obvious (a credit is an anticipated

f. This statement is true. In the purchases method, the total prepaid

expenses or supplies acquired is recorded as an expenditure. In the

g. This statement is true. Income taxes and sales taxes are both derived

tax revenues because the tax is assessed based on a specific event (the earning

of income or the making of a sale).

h. This statement is true. Accrual accounting is used for government-

i. This statement is false. The encumbrance (commitment) is removed

j. This statement is false. “Fund balance – committed” is used when

financial resources have been designated by the highest level of government

k. This statement is false. This is an intra-activity transaction between

46. (25 Minutes) (The handling of various government transactions.)

a. This statement is false. This transfer is an internal exchange

b. This statement is false. No increase in net position is recognized in

d. This statement is false. The $5,000 cannot be used at this time.

However, revenue recognition will occur after the passage of time. The

e. This statement is false. The $5,000,000 can never be spent so a fund

47. (25 Minutes) (Prepare a statement of revenues, expenditures, and other

changes in fund balance)

In this problem, the journal entries are prepared based on the rules for

creating fund financial statements for the General Fund.

a.

Cash 700,000

Property Taxes Receivable 100,000

b.

Expenditures—Police Cars 200,000

Cash 200,000

If previously recorded, an encumbrance would also have to be removed.

c.

Other Financing Uses—Transfers Out 90,000

d.

required in this period. Payment will not be until next June 30.

e.

Encumbrances – Computer 40,000

Encumbrances Outstanding 40,000

f.

h.

Expenditures—Supplies 10,000

Cash 10,000

i.

Supplies 2,000

Fund Balance—Nonspendable 2,000

FUND FINANCIAL STATEMENTS

CITY OF LOST ANGELS

STATEMENT OF REVENUES, EXPENDITURES AND OTHER CHANGES IN FUND

BALANCE

For the Year Ended December 31, 2015

General Fund

Revenues

—Property Taxes $750 ,000

Total Revenues $750 ,000

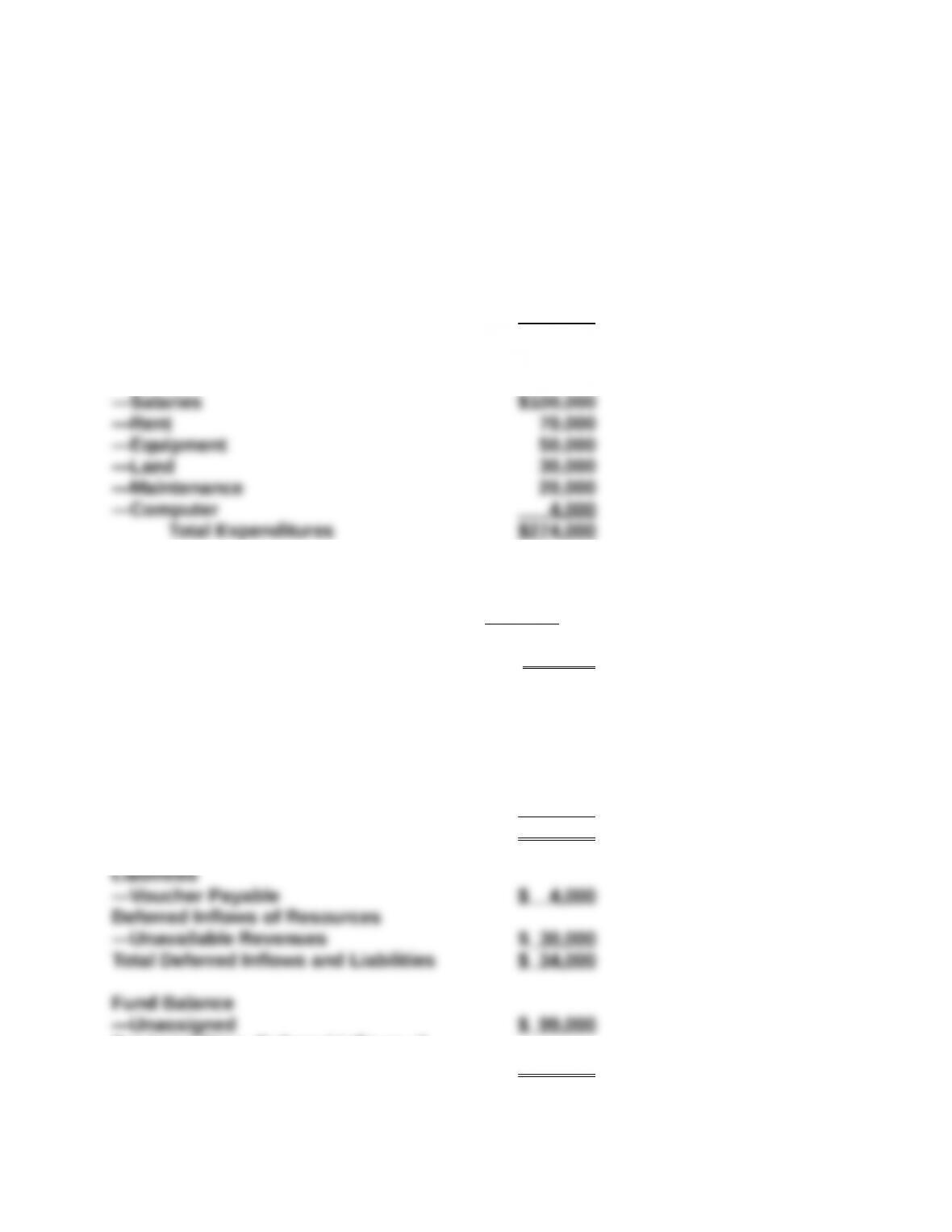

Expenditures

—Police cars $200,000

—Salaries 40,000

—Computer 41,000

Other Financing Sources (Uses)

—Transfer to Debt Service Fund $(90,000)

—Issued Long-Term Bond 200 ,000

Net Other Financing Sources $110 ,000

48. (25 Minutes) (Prepare a statement of net position for governmental

activities)

Here the journal entries are prepared based on the need to create

government-wide financial statements for the General Fund (a governmental

activity).

a.

Cash 700,000

Property Taxes Receivable 100,000

Property Tax Revenue 800,000

b.

d.

Cash 200,000

Bonds Payable 200,000

Interest Expense 10,000

Interest Payable 10,000

Interest is accrued here based on $200,000 x 10 percent x 1/2 year.

g.

Computer 41,000

Vouchers Payable 41,000

Depreciation Expense 4,100

Accumulated Depreciation 4,100

This problem indicates that the General Fund held $180,000 in cash at the start of

the year. The following account balances have been determined based on the

above journal entries.

GOVERNMENT-WIDE FINANCIAL STATEMENTS

CITY OF LOST ANGELS

STATEMENT OF NET POSITION

December 31, 2015 Governmental

Activities

Assets

—Cash $840,000

—Property Tax Receivable 100,000

Total Assets $1 ,168,900

Liabilities

—Vouchers Payable $41,000

—Salary Payable 10,000

—Interest Payable 10,000

The total net position figure of $907,900 can be found by taking the opening

balance of $180,000 and then adding the revenues for the period and

subtracting the expenses.

49. (10 Minutes) (The budgetary process)

A. True—The initial approval of spending was $380,000 and that amount

should be recorded immediately. The budgetary entry debits Estimated

Revenues and credits Appropriations.

E. False—Budgetary information only relates to fund financial statements

to show the inflows and outflows of current financial resources and has

no impact on the government-wide financial statements.

50. (10 Minutes) (The recording of grants)

A. False—This grant appears to be voluntary exchange transaction.

Revenue should be recognized when all eligibility requirements have

been met. Here, the eligibility requirements, if any, could have been met

during 2015. It is certainly possible that the eligibility requirements have

not been met but that is not necessarily the case.

D. True—Cash is recognized because it had been received but no revenue

is reported because all eligibility requirements have not yet been met.

Thus, unavailable revenue should be established for the amount

received.

51. (20 Minutes) (Impact of various government transactions)

a. Fund financial statements – the fund balance goes up by $6 million

because of the inflow of current financial resources.

Government-wide financial statements – the net position balance does

b. Fund financial statements – the fund balance goes down by $149,000

because of the outflow of current financial resources.

b. Fund financial statements – the fund balance is not affected because

the resources will not be collected quickly enough to be available in the

current period. An asset (receivable) is recognized along with a liability

(unearned revenue) so that the size of the fund balance is not affected.

d. Fund financial statements – the fund balance should go up by $500,000.

Sales took place in the current year but only half of the financial

resources will all be received within the 75 day period being used to

define available resources. The remainder will be unavailable revenue.

f. Fund financial statements – the fund balance for the General Fund goes

down by $18,000 because the transfer has been approved and will

remove current financial resources from this fund.

Government-wide financial statements – no impact occurs on the net

position balance of the governmental activities because this is an intra-

activity transfer from one Governmental Fund to another. There is no

net effect.