CHAPTER 15

PARTNERSHIPS: TERMINATION AND LIQUIDATION

Chapter Outline

I. The termination of a partnership and liquidation of its property may take place for a number

of reasons.

A. The death, withdrawal, or retirement of a partner can lead to cessation of business

activity.

B. The bankruptcy of either an individual partner or the partnership as a whole can

necessitate termination and liquidation.

II. Because of the importance of liquidating and distributing assets fairly, all parties look to the

accountant to play an important role in the process.

A. The accountant provides timely financial information.

B. The accountant works to ensure an equitable settlement of all claims.

III. The statement of liquidation

A. The liquidation process usually involves the disposal of noncash assets, payment of

liabilities and liquidation expenses, and distribution of any remaining cash to the partners

based on their final capital balances.

B. A statement of liquidation should be produced periodically by the accountant to disclose

losses and gains that have been incurred, remaining assets and liabilities, and current

capital balances.

IV. Deficit capital balances

A. By the end of, or even during, the liquidation process, one or more partners may have a

negative (or deficit) capital balance often as a result of losses incurred in disposing of

assets.

B. The Uniform Partnership Act indicates that any deficit capital balance should be

eliminated by having that partner contribute enough additional assets to offset the

negative balance.

C. If this contribution is not immediately received, the remaining partners may request a

preliminary distribution of any partnership cash that is available.

1. Safe payments of cash to individual partners are determined based on safe capital

balances, the amounts that will remain in the individual capital accounts even if all

deficits and other assets prove to be complete losses that must be absorbed by the

remaining partners.

2. If a portion (or all) of a deficit is subsequently recovered from a partner, a further

distribution to the other partners is made based on newly computed safe capital

balances.

3. Any deficit that is not recovered from a partner must be charged to the remaining

partners based on their relative profit and loss ratio.

V. Treatment of partner’s loan to partnership

A. The Uniform Partnership Act states that, in a liquidation, partnership assets should be

used to first settle claims of partnership creditors, including claims of partners who are

creditors.

1. This implies that the partnership would first repay partners’ loans before distributing

any cash to partners based on their capital balances.

B. However, in practice, to avoid making a cash distribution to a partner who subsequently

develops a deficit capital balance, partners’ loan accounts typically are combined with

partners’ capital accounts and funds are distributed accordingly. This text uses this

practice.

Vl. Preliminary distribution of assets to the partners

A. The liquidation process can extend over a lengthy period of time as business activities

wind down and property is sold.

B. When the partnership terminates activity, or during the course of the liquidation, more

cash may be available than the amount needed to extinguish all potential liabilities and

liquidation expenses.

C. If possible, the distribution of excess cash amounts should be made as quickly as

possible to enable the partners to make use of their funds.

1. The accountant may choose to produce a proposed schedule of liquidation at such

times to determine the equitable distribution of cash amounts that become available.

2. The proposed schedule of liquidation is developed based upon simulating the

accounting recognition that would be required by a possible series of transactions:

assets are sold, expenses are paid, etc.

a. These events are simulated with the anticipation of maximum losses in each

case.

b. Noncash assets are assumed to have no resale value; maximum possible

liquidation expenses are included; all partners are considered personally

insolvent; etc.

3. Ending potential capital balances that remain on a proposed schedule of liquidation

are safe capital balances, the amounts that could be immediately paid to each

partner without jeopardizing future payments. Safe capital balances indicate that the

partner will still have a sufficient interest in the partnership to absorb all potential

losses even after a preliminary distribution.

Vll. Predistribution plan

A. The proposed schedule of liquidation (described above) can be used to determine safe

payments based on safe capital balances but a newly revised schedule must be

prepared each time a distribution of cash to partners is contemplated.

B. Accountants often prefer to produce a single predistribution plan at the start of a

liquidation to provide guidance for all payments made to the partners throughout this

process.

C. Information for the predistribution plan is generated by assuming the occurrence of a

series of losses, each just large enough to eliminate one partner’s claim to any

partnership property.

D. Once a series of losses has been simulated that would eliminate the capital balances of

all partners, the actual plan is developed by measuring the effects that occur if the

losses do not materialize.

E. By working backwards through this series of possible losses, a predistribution plan can

be produced that serves as a guide for all payments made during the liquidation.

Answer to Discussion Question: What Happens if a Partner Becomes Insolvent?

This case demonstrates one of the nightmares of a partnership: the apparent insolvency of a

partner is threatening the future of a successful business. The problem is especially acute to

Wilkinson and Walker since this partnership was created solely for convenience; the partners

share the facilities but do not actually work together. Therefore, the presence of Rogers is not

essential to the other partners except that he pays a portion of the business’s expenses.

However, the claim that has been filed could lead to the actual liquidation of the entire business.

Obviously, the partners should take no immediate action until they have spoken with Rogers.

The entire issue may prove to be a mistake. Conversely, numerous other claims against Rogers

may also be outstanding with the initial claim simply being the first to be filed. Because of the

Walker would have a building that was apparently larger than their needs. Unless they could

utilize the space in some manner, they might have no way of recouping their additional

investment.

As a second possibility, a new dentist could be brought in to acquire Rogers’ interest in the

partnership. Again, the money is conveyed to Rogers but now the original partners are not

forced to make the payment. The building would continue to be fully utilized so that the partners’

expenses would not escalate. In this case, though, a new partner may have to be identified in a

Although Wilkinson and Walker have several possible actions that can be taken, none of these

is without problems. Therefore, partners should always include agreements within their Articles

of Partnership to specify actions that will be taken in such cases. The insolvency of a partner is

not a particularly unusual event. Hence, the partners (or their attorneys and accountants) should

have the forethought to arrange the resolution of the business if insolvency of a partner does

occur.

Answers to Questions

1. A dissolution refers to the cessation of a partnership. In many cases, this process is simply a

preliminary step in the transfer of business property to a newly formed partnership.

2. Many reasons can exist that would lead to the termination and liquidation of a partnership.

The business might simply have failed to generate sufficient profits or the partners may elect

3. During the liquidation process, monitoring the balance of the partners’ capital accounts

becomes of paramount importance. That amount will eventually indicate either the cash to

4. Final distributions made to the various partners are based solely on their ending capital

account balances unless the partners have agreed otherwise. If any partner has a deficit

balance, that partner should make an additional contribution to the partnership to offset the

5. A statement of liquidation summarizes the financial effect of the liquidation process as it has

progressed to date. Information to be presented includes the balances of all remaining

6. From a legal viewpoint, any partner who incurs a negative (or deficit) capital balance is

obligated to make an additional contribution to offset that amount.

7. A safe capital balance is the amount of a partner’s capital account that exceeds all possible

needs of a partnership as it goes through liquidation. A partner should, therefore, be able to

receive this balance immediately without endangering the future amount to be received by

8. Although the Uniform Partnership Act states that loans from partners rank ahead of the

partners’ capital balances in the distribution of partnership assets, in practice a partner’s

9. A proposed schedule of liquidation is prepared by the accountant to determine the allocation

of any cash available in the early stages of a liquidation that exceeds the amount needed to

pay all liabilities and estimated liquidation expenses. The schedule is based on anticipating

10. A predistribution plan is produced based on an assumed series of losses. Each loss is

calculated to eliminate in turn the capital balance of one of the partners. In this manner, the

accountant can determine the vulnerability to losses exhibited by each capital account.

Answers to Problems

4. B (Partner with deficit capital balance)

Angela, Capital Woodrow, Capital Cassidy, Capital

Reported balances $19,000 $18,000 $(12,000)

Potential loss from

5. B (Insolvent partner)

Bell Hardy Dennard Suddath

Reported balances $50,000 $56,000 $14,000 $80,000

Adjusted balances $ 6,000 $23,000 $(8,000)$69,000

Potential loss from Dennard

6. A (Predistribution plan)

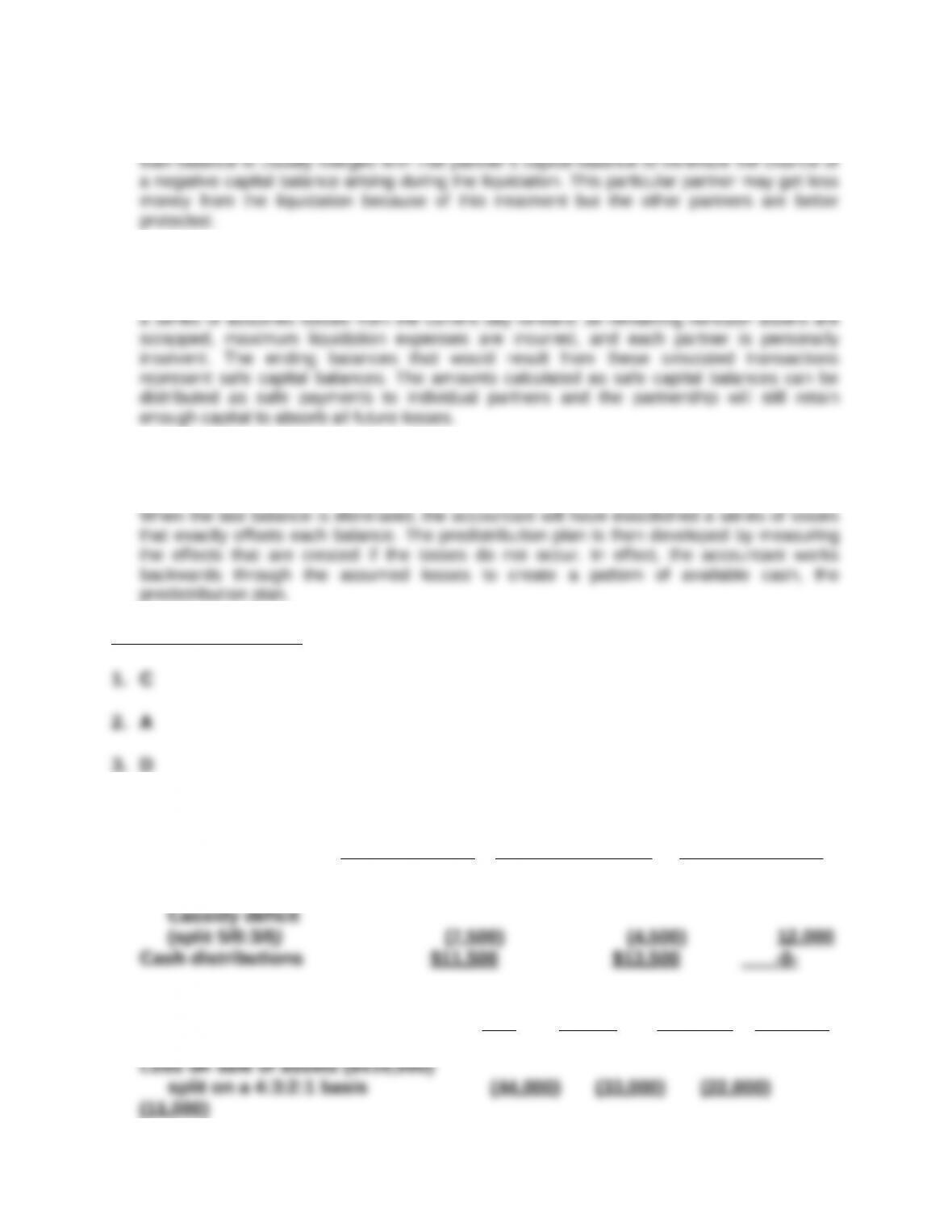

7. A (Proposed schedule of liquidation to determine safe payments before the

liquidation begins; partner has deficit)

Art Raymond Darby

Reported balances ………………………….…... $18,000 $25,000 $26,000

Loss on sale of assets ($22,000) split

on a 4:3:3 basis …………..……….…..….….… (8 ,800) (6 ,600) (6 ,600)

Adjusted balances ……………….…..….….….. $ 9,200 $18,400 $19,400

Anticipated liquidation expenses ($12,000)

Since the partnership currently has total capital of $400,000, the $30,000

that is available would indicate maximum potential losses of $370,000.

A B C

Reported balances $100,000 $120,000 $180,000

Anticipated loss ($370,000) split on

Potential loss from C’s deficit (split 2:3) (2 ,000) (3 ,000) 5 ,000

Current cash distribution $ 24 ,000 $ 6 ,000 $ -0-

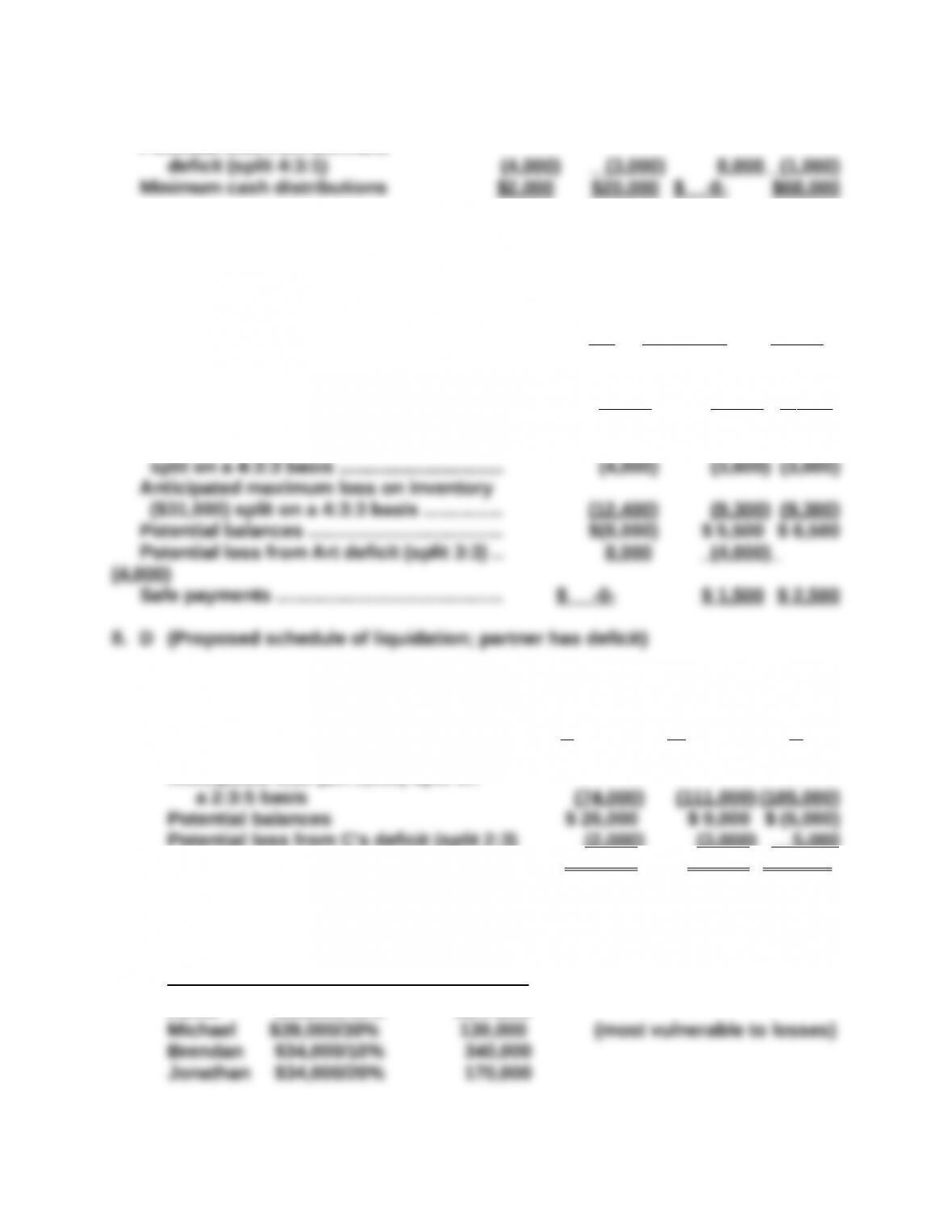

9. C (Predistribution plan)

To solve this problem a predistribution plan should be created.

Maximum Losses That Can Be Absorbed

Kevin $59,000/40% $147,500

The assumption is made that a $130,000 loss occurs:

Kevin Michael Brendan Jonathan

Reported balances …………….….….….$59,000 $39,000 $34,000 $34,000

Assumed loss ($130,000) split

Maximum Losses That Now Can Be Absorbed

Kevin $7,000 / 4/7 $12,250 (most vulnerable to losses)

The assumption is made that a $12,250 loss occurs:

Kevin Brendan Jonathan

Reported balances ………………………….….…...$7,000 $21,000 $8,000

Assumed loss ($12,250) split

Maximum Losses That Now Can Be Absorbed

Brendan $19,250/1/3 $57,750

Jonathan $4,500/2/3 6,750 (most vulnerable to losses)

The assumption is made that a $6,750 loss occurs:

Brendan Jonathan

Reported balances……………………..…..….….….… $19,250 $4,500

Brendan will receive a $17,000 distribution from the partnership before any

of the other partners collect any cash.

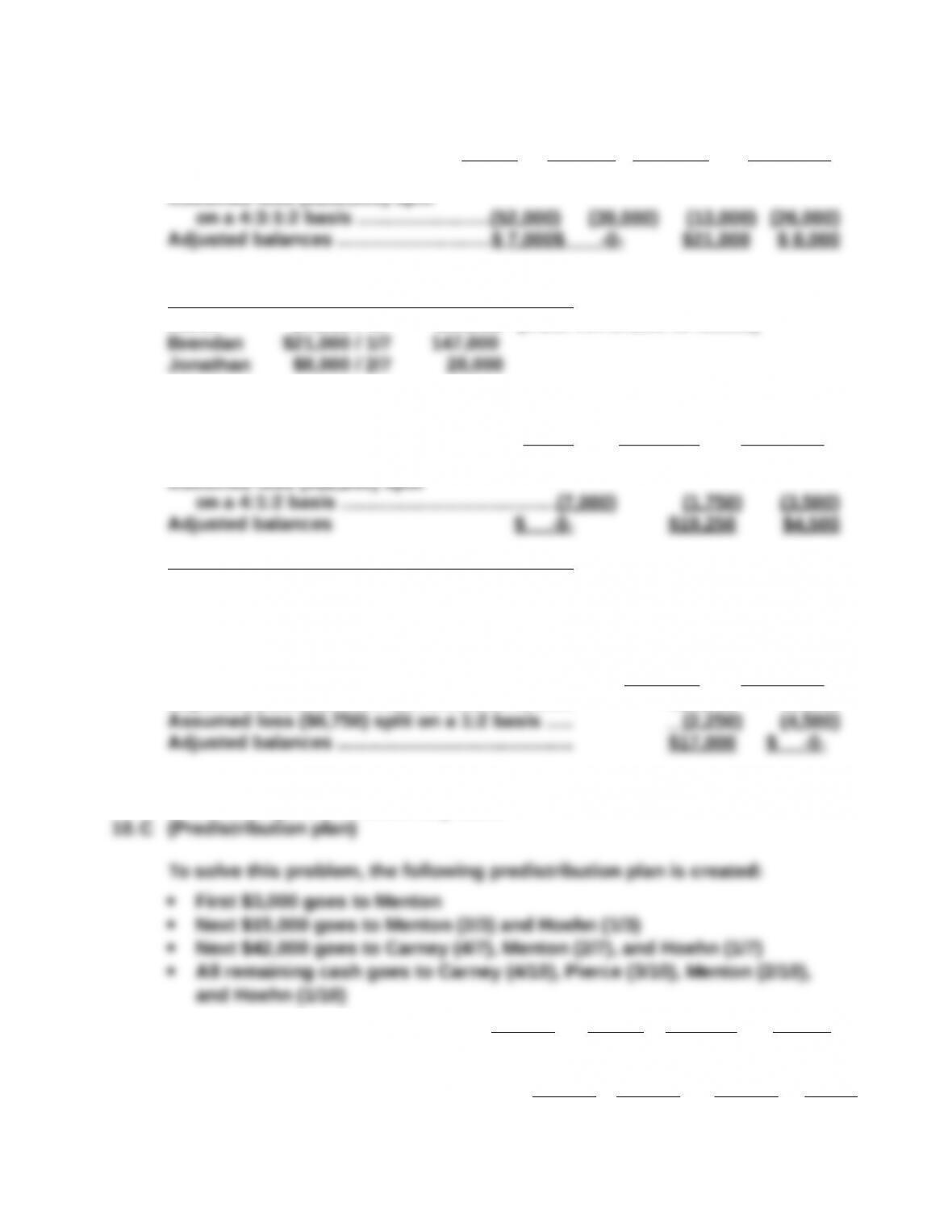

Carney Pierce Menton Hoehn

Beginning balances $60,000 $27,000 $43,000 $20,000

Assumed loss of $90,000 (see

Schedule 1) (4:3:2:1 basis) (36 ,000) (27 ,000) (18 ,000) (9 ,000)

Schedule 1

Maximum Loss

Capital Balance/ That Can

Partner Loss Allocation Be Absorbed

Carney $60,000/40% $150,000

Schedule 2

Maximum Loss

Capital Balance/ That Can

Partner Loss Allocation Be Absorbed

Carney $24,000/(4/7) $ 42,000 (most vulnerable)

Schedule 3

Maximum Loss

Capital Balance/ That Can

Partner Loss Allocation Be Absorbed

11.C (Partners with deficit capital balances; proposed schedule of liquidation;

safe capital balances)

The $16,000 available cash can be distributed but should be done under the

assumption that all deficit balances will be total losses. After offsetting

can be immediately distributed.

Wayman Jones Fuller Rogers

(30%) (20%) (30%) (20%)

Reported balances $(2,000) $(2,000) $13,000 $7,000

Potential losses from Wayman

12.(8 minutes) (Determine safe payments; partner has deficit)

Nixon Cleveland Pierce

Reported balances …………………..….… $170,000 $110,000 $70,000

Anticipated loss ($342,000) split

13. (20 minutes) (Final settlement of a partnership being liquidated; various

amounts of loss on sale of assets)

Part a. Brown gets $21,000, Fish gets $12,000, and Stone gets $2,000.

Brown Fish Stone

Reported balances …………………….…..….…. $25,000 $15,000 $5,000

Part b. Brown gets $16,429 and Fish gets $8,571

Brown Fish Stone

Reported balances …………………….…..….…. $25,000 $15,000 $5,000

Loss on sale of land ($20,000) split on

Part c. Brown gets $10,714 and Fish gets $4,286

Brown Fish Stone

Reported balances …………………….…..….…. $25,000 $15,000 $5,000

Loss on sale of land ($30,000) split on

a 4:3:3 basis…………………..….….….…..…. (12 ,000) (9 ,000) (9 ,000)

14.(10 minutes) (Distribute cash contributed by partner with deficit balance)

The entire $20,000 goes to Atkinson.

Atkinson Kaporale Dennsmore Rasputin

Reported balances $70,000 $30,000 $(42,000) $(58,000)

Capital contribution -0- -0- -0- 20 ,000

Adjusted balances $70,000 $30,000 $(42,000) $(38,000)

Potential loss from Dennsmore

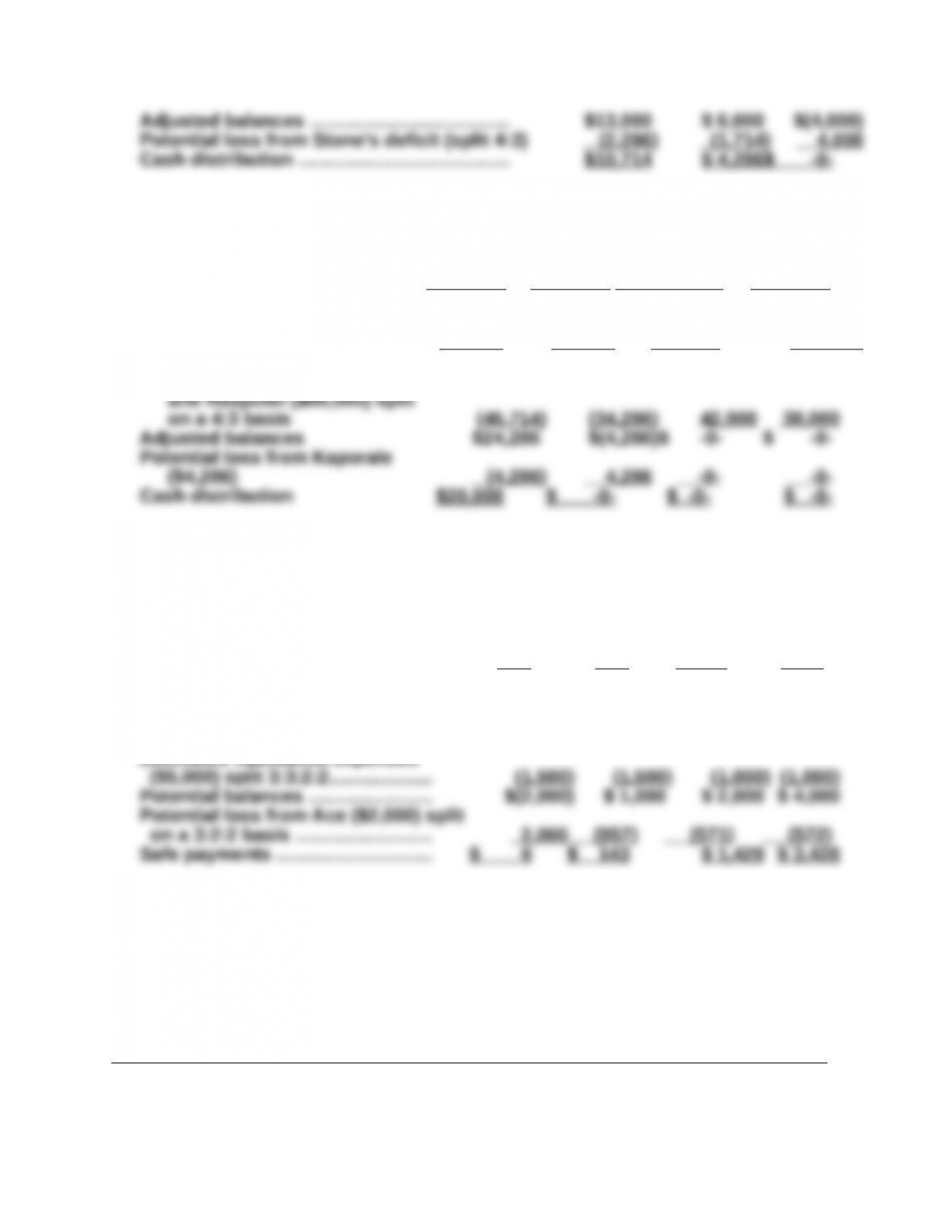

15. (8 minutes) (Determine safe payments)

Ball gets $143, Eaton gets $1,429, and Lake gets $3,428.

Ace Ball Eaton Lake

Reported balances …….…..….….... $25,000 $28,000 $20,000 $22,000

Maximum losses on land and building

($85,000) split on a 3:3:2:2 basis (25,500) (25,500) (17,000)

(17,000)

Estimated liquidation expenses

16. (15 minutes) (Prepare a proposed schedule of liquidation)

HARDWICK, SAUNDERS, AND FERRIS

Proposed Schedule of Liquidation

Hardwick, Ferris,

Other Accounts Loan and Saunders, Loan &

Cash Assets Payable Capital Capital Capital

Beginning

balances 90,000 820,000 (210,000) (270,000) (200,000)

(230,000)

(44,000)

Of the available $80,000 in cash, $22,000 can be paid safely to Hardwick, $14,000

to Saunders, and $44,000 to Ferris.

17.(7 minutes) (Determine amount of cash needed to assure payments to all

partners)

Watson is the partner most vulnerable to a loss. A loss of only $100,000 would

completely eliminate Watson’s capital balance:

18.(5 minutes) (Determine safe capital balances and safe payments)

Maximum potential losses are $128,000: $8,000 in liquidation expenses and a

complete $120,000 loss on the noncash assets. Such a loss would reduce the