35. (continued)

b. and c.

The following C$ financial statements are produced by combining the figures

from the main operation with the remeasured figures from the branch

remeasured in C$.

Income Statement c. Translation into U.S. dollars—

For the Year Ended December 31, 2015 Current Rate Method

Sales C$ 354,160 x .67 A =$ 237,287.20

Cost of goods sold (223 ,500)x .67 A = (149 ,745.00)

Gross profit 130,660 87,542.20

Depreciation expense (8,500)x .67 A = (5,695.00)

Salary expense (29,060)x .67 A = (19,470.20)

Statement of Retained Earnings

For the Year Ended December 31, 2015

Retained earnings, 1/1/15 C$ 135,530Given $ 70,421.00

Net income (above) 89,090Above 59,740.30

35. (continued)

b. and c.

Balance Sheet

December 31, 2015

Cash C$ 46,650x .65 C = $ 30,322.50

Receivables 75,350x .65 C = 48,977.50

Inventory 107,520x .65 C = 69,888.00

Accounts payable C$ 52,150x .65 C = $ 33,897.50

Notes payable 76,000x .65 C = 49,400.00

Cumulative translation adjustment Schedule Two 26 ,961.70

Total C$ 374 ,770 $ 243 ,600.50

Schedule Two—Translation Adjustment

Net assets, 1/1/15 C$ 185,530x .70 = $129,871.00

Changes in net assets

Net income 89,090 Above 59,740.30

Dividends (28 ,000)x .69 = (19 ,320.00)

Net assets, 12/31/15 C$ 246 ,620 $170,291.30

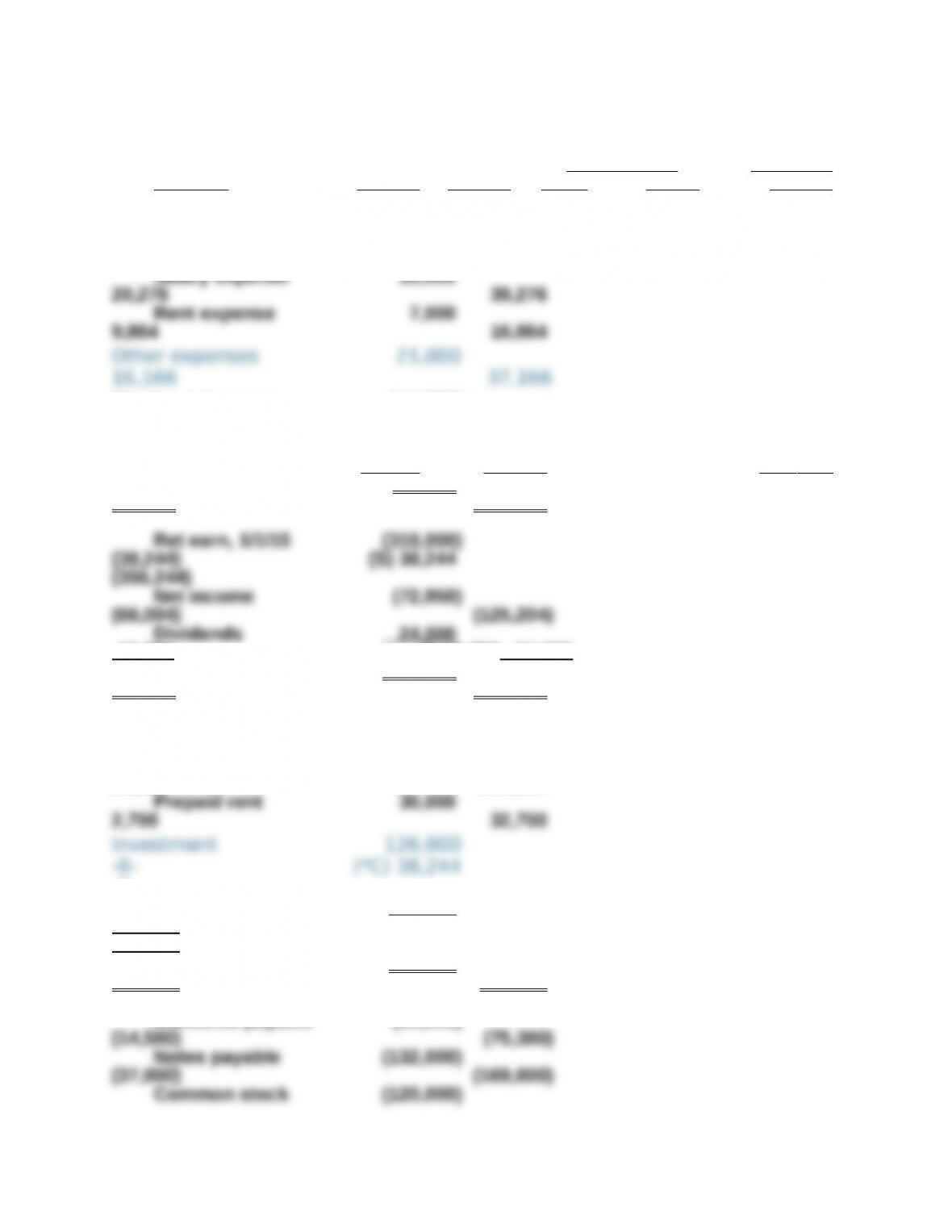

36. (90 minutes) (Translate foreign currency financial statements and prepare

consolidation worksheet)

Step One

Translation Worksheet

Exchange

Account Pounds Rate Dollars

Sales (800,000) 0.274 (219,200)

Cost of goods sold 420,0000.274 115,080

Salary expense 74,0000.274 20,276

Rent expense (adjusted) 36,0000.274 9,864

R/E, 1/1/15 (133,000) Schedule 1 (38,244)

Net income (241,000) Above (66,004)

Dividends 50 ,0000.275 13 ,750

R/E,12/31/15 (324 ,000) (90 ,498)

Accounts payable (54,000)0.270 (14,580)

Notes payable (140,000)0.270 (37,800)

Subtotal (259,878)

Cumulative translation

adjustment (negative) Schedule 2 14 ,718

Total (908 ,000) (245 ,160)

36. (continued)

Schedule 1—Translation of 1/1/15 Retained Earnings

Pounds Dollars

Retained earnings, 1/1/14 -0- -0-

Net income, 2014 (163,000)0.288 (46,944)

Schedule 2—Calculation of Cumulative Translation Adjustment at 12/31/15

Pounds Dollars

Net assets, 1/1/14 (390,000)0.300 (117,000)

Net income, 2014 (163,000)0.288 (46,944)

Net assets, 1/1/15(523,000) 0.280 (146,440)

Net income, 2015(241,000) Above (66,004)

Dividends, 6/1/15 50 ,000 0.275 13 ,750

Net assets, 12/31/15 (714 ,000) (198,694)

Net assets, 12/31/15 at

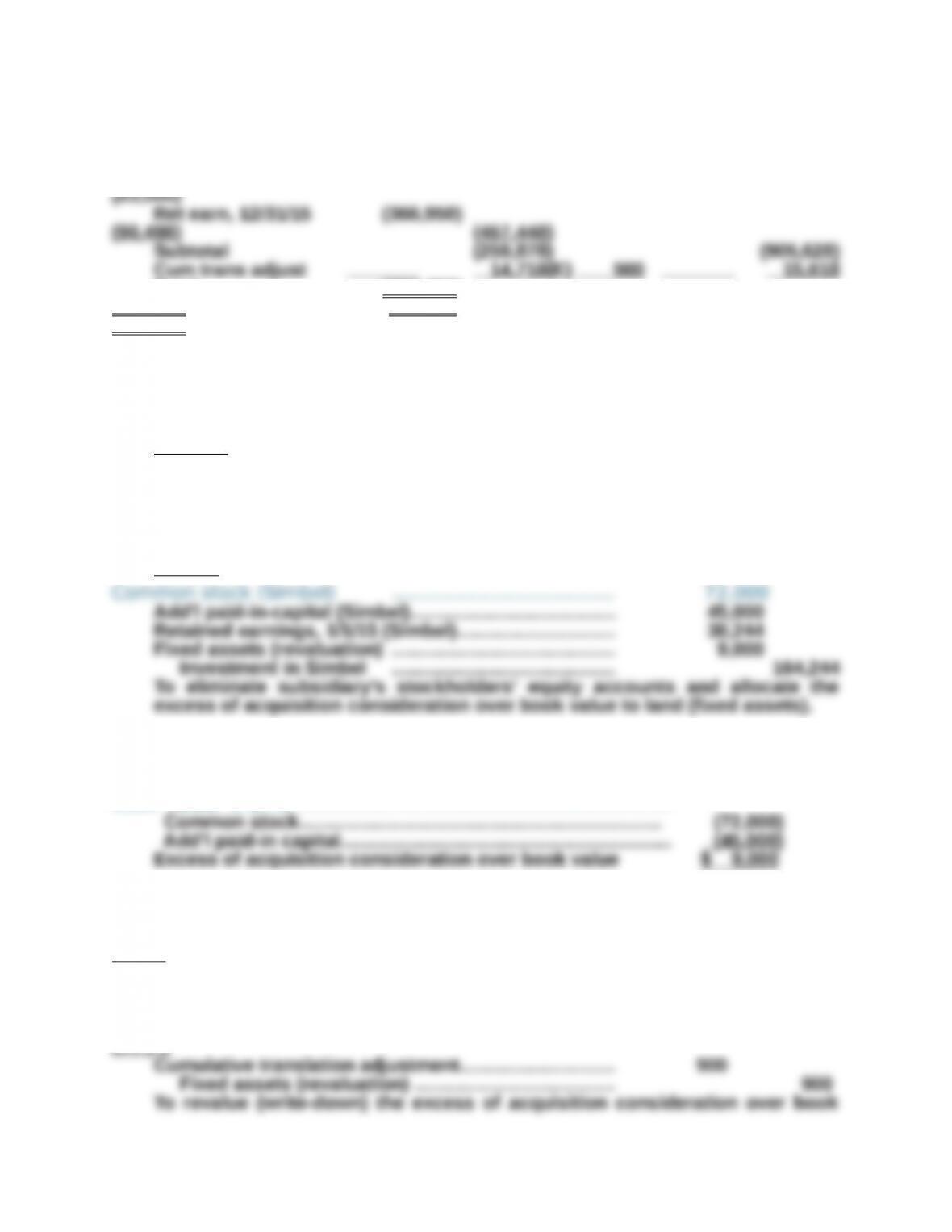

36. (continued)

Step Two

Cayce and Simbel’s U.S. dollar accounts are then consolidated. Necessary

adjustments and eliminations are made.

Consolidation Worksheet

Adjustments and

Consolidated

Cayce Simbel Eliminations Balances

Account Dollars Dollars Debit Credit Dollars

Sales (200,000)

(219,200) (419,200)

Cost of goods sold 93,800

115,080 208,880

Dividend income (13,750)

-0- (I) 13,750

-0-

Gain, 10/1/15 -0- (8 ,190) (8 ,190)

Net income (72 ,950)

(66,004) (125 ,204)

13,750 (I) 13,750 24 ,000

Ret earn, 12/31/15 (366 ,950)

(90,498) (457 ,448)

Cash and receivables 110,750

39,420 150,170

Inventory 98,000

80,190 178,190

-0-

Fixed assets 398 ,000

122,850 (S) 9,000

528,950

Total 762 ,750

245,160 890 ,010

Accounts payable (60,800)

(72,000) (S) 72,000

(120,000)

Additional PIC (83,000)

(45,000) (S) 45,000

Total (762 ,750)

(245,160) 217 ,138

(890,010)

36. (continued)

Explanation of Adjustment and Elimination Entries

Entry *C

Investment in Simbel……………………..………..…..….….... 38,244

Retained earnings, 1/1/15………………………..………... 38,244

To accrue 2015 increase in subsidiary book value (see Schedule 1). Entry is

needed because parent is using the cost method.

Entry S

The excess of acquisition consideration over book value is calculated as

follows:

Acquisition consideration…………….………..……………………….. $126,000

Book value, 1/1/15………………………………………………………..

The excess of acquisition consideration over book value is 30,000 pounds.

The U.S. dollar equivalent at 1/1/15, the date of acquisition, is $9,000

(£E30,000 x $.30).

Entry I

Dividend income…………………………….….………….……. 13,750

Dividends……………………..………………………..…..….… 13,750

To eliminate intra-entity dividend payments recorded by parent as income.

Entry E

value for the change in exchange rate since the date of acquisition with the

counterpart recognized in the consolidated cumulative translation

adjustment.

The revaluation of “excess” is calculated as follows:

Excess of acquisition consideration over book value

U.S. dollar equivalent at 12/31/15 £E30,000 x $.27 = $8,100

37. (90 minutes) Translate [remeasure] foreign currency financial statements

using U.S. GAAP and explain sign of translation adjustment [remeasurement

gain/loss])

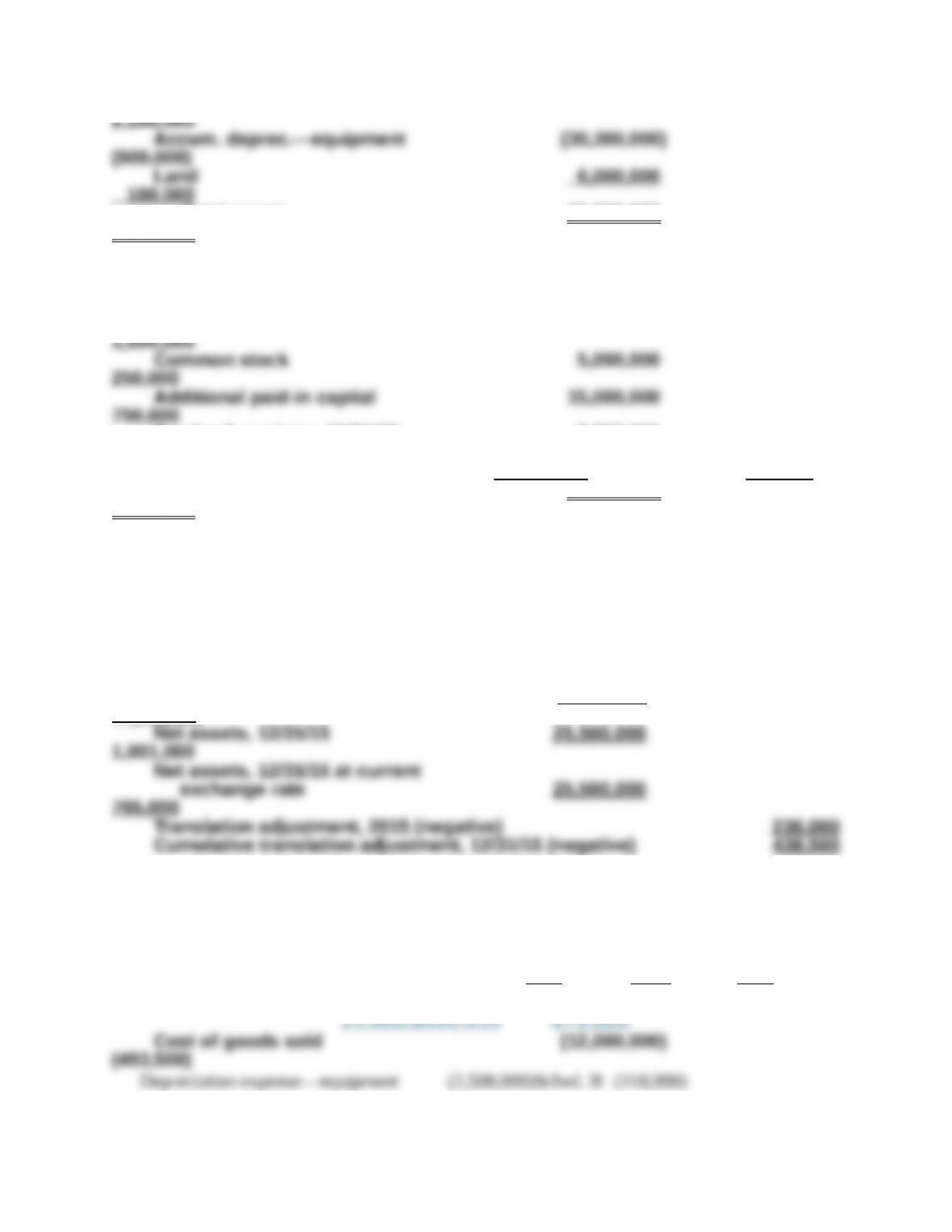

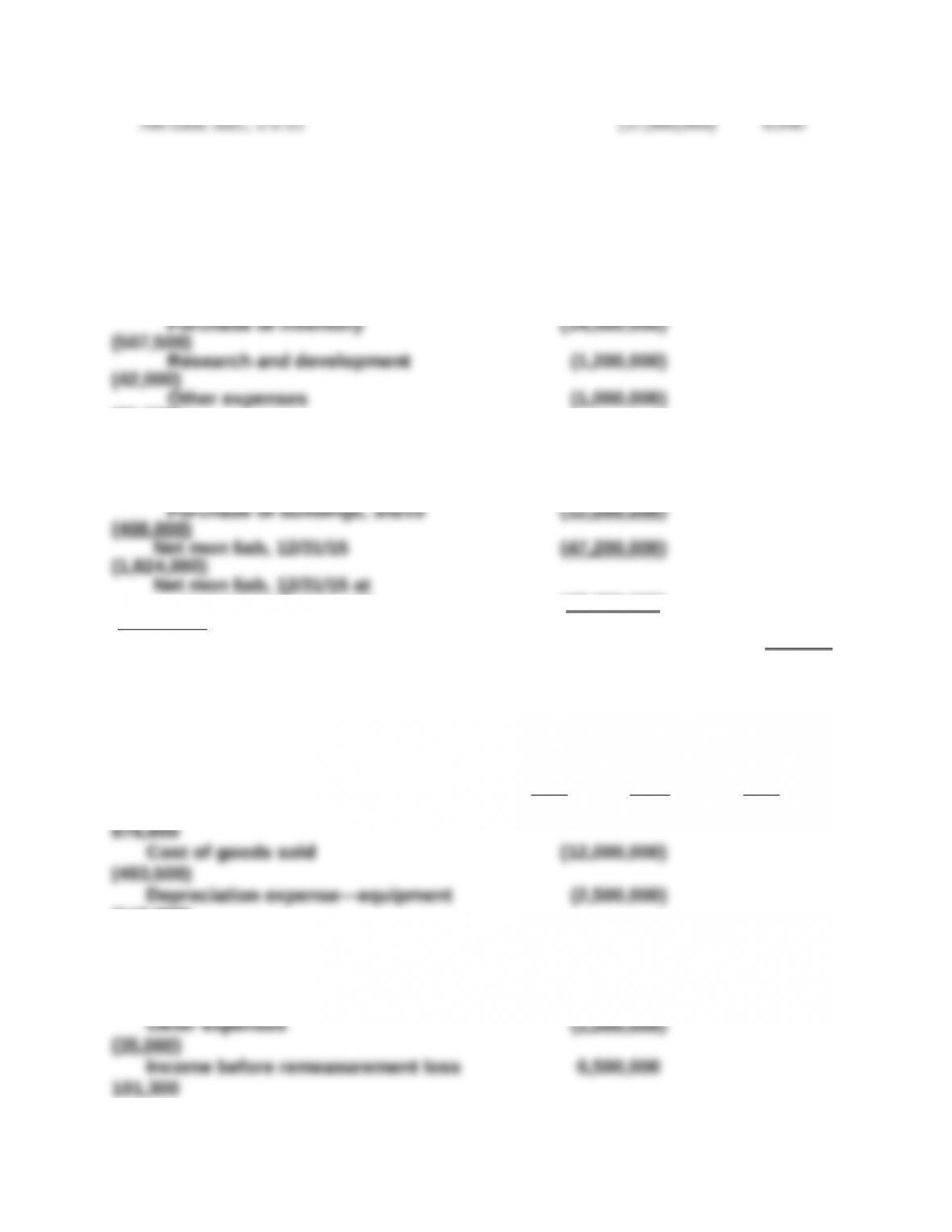

Part I (a). Czech koruna is the functional currency—current rate method

Exchange

K č S Rate US$

Sales 25,000,000 0.035 875,000

Cost of goods sold (12,000,000)

(420,000)

(63,000)

Research and development expense (1,200,000)

(42,000)

Other expenses (1 ,000,000)

(35,000)

(46,500)

Retained earnings, 12/31/15 5 ,500,000

203,500

Cash 2,000,000

60,000

Accounts receivable 3,300,000

750,000

Accum. deprec.—equipment (8,500,000)

(255,000)

Building 72,000,000

Total assets 78 ,000,000

2,340,000

Accounts payable 2,500,000

75,000

Long-term debt 50,000,000

Retained earnings, 12/31/15 5,500,000

above 203,500

Translation adjustment – to balance (438 ,500)

Total liabilities and equities 78 ,000,000

2,340,000

37. (continued)

Calculation of Translation Adjustment

Translation adjustment, 2015 (negative) 202,500

Net assets, 1/1/15 20,500,000

820,000

Net income, 2015 6,500,000

227,500

Dividends, 12/15/15 (1 ,500,000)

(46,500)

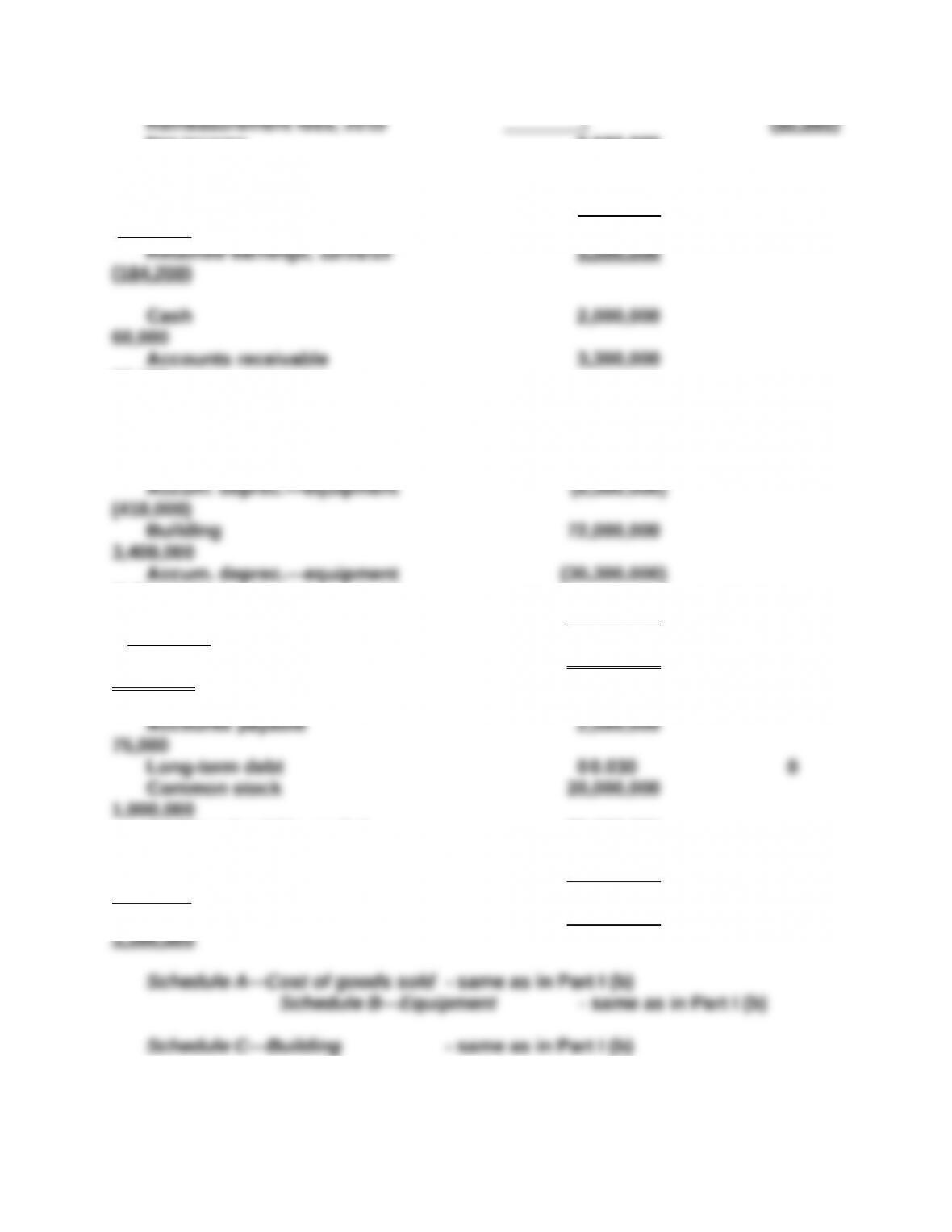

37. (continued)

Part I (b). U.S. dollar is the functional currency—temporal method

Exchange

K č S Rate US$

Sales

Net income 6,500,000

509,300

Retained earnings, 1/1/15 500,000 given 353,000

Dividends, 12/15/15 (1 ,500,000)

(46,500)

Retained earnings, 12/31/15 5 ,500,000

815,800

272,000

Equipment

25,000,000Sched.B 1,180,000

Accum. deprec.—equipment (8,500,000)

(418,000)

300,000

Total assets 78 ,000,000

3,390,800

Accounts payable 2,500,000

75,000

750,000

Retained earnings, 12/31/15 5 ,500,000

815,800

Total liabilities and equities 78 ,000,000

3,390,800

Schedule A—Cost of goods sold

K č S ER US$

Beginning inventory 6,000,000

0.043258,000

Purchases

37. (continued)

Schedule B—Equipment

K č S ER US$

Old Equipment—at 1/1/14 20,000,000 0.050

1,000,000

New Equipment—acquired 1/3/15 5 ,000,000

180,000

400,000

Accum. Depr.—New Equipment 500 ,0000.036 18 ,000

Total 8 ,500,000

418,000

118,000

Schedule C—Building

K č S ER US$

Old Building—at 1/1/14 60,000,000

3,000,000

New Building—acquired 3/5/15 12 ,000,000

Total 30 ,300,000

1,510,200

Deprec. expense—Old Building 1,500,000

75,000

85,200

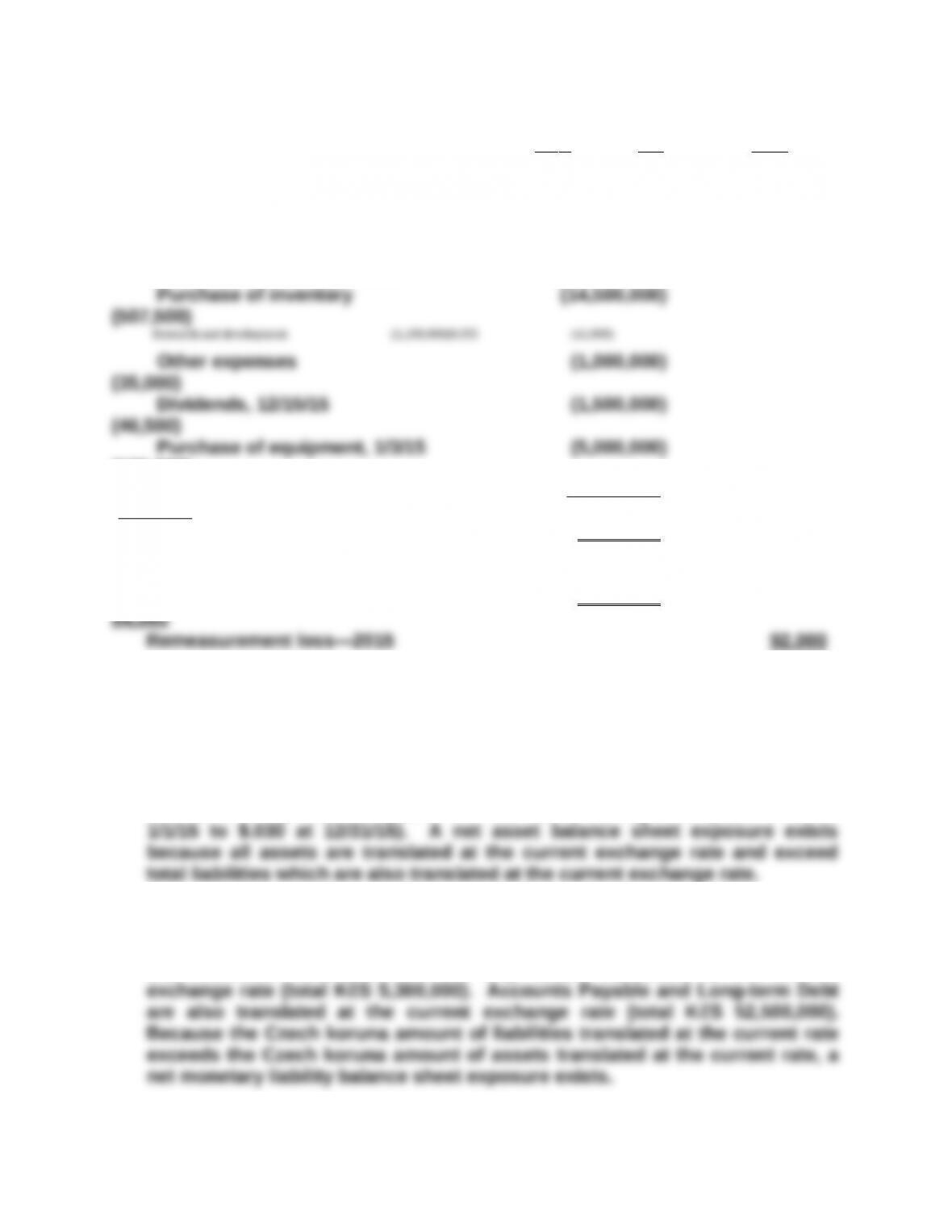

Calculation of Remeasurement Gain

K č S ER US$

(1,480,000)

Increase in mon. assets:

Sales 25,000,000

875,000

Decrease in mon. assets:

(35,000)

Dividends, 12/15/15 (1,500,000)

(46,500)

Purchase of equipment, 1/3/15 (5,000,000)

(180,000)

current exchange rate (47 ,200,000)

(1,416,000)

Remeasurement gain—2015 (408 ,000)

37. (continued)

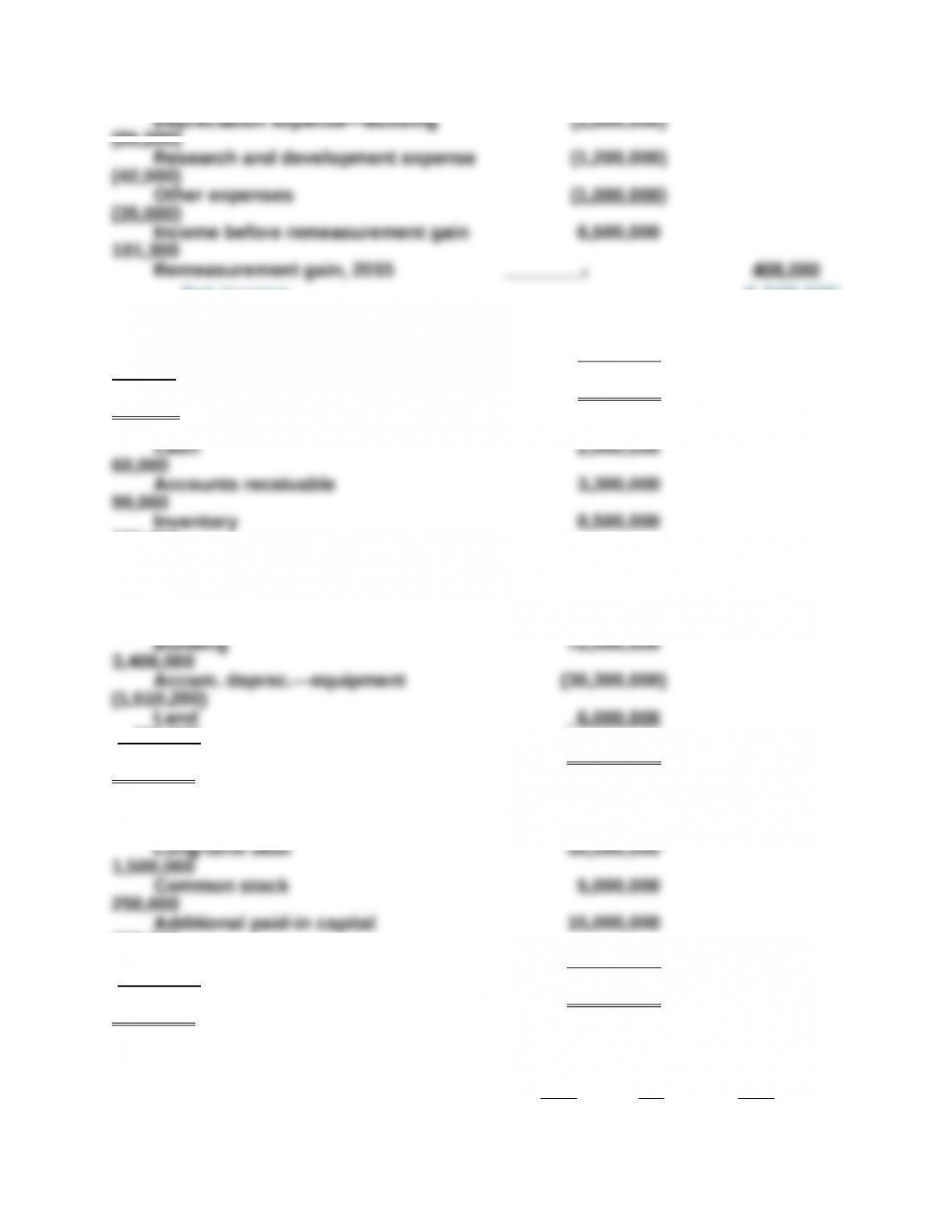

Part I (c). U.S. dollar is the functional currency—temporal method (no long-

term debt)

Exchange

K č S Rate US$

Sales 25,000,000

(118,000)

Depreciation expense—building (1,800,000)

(85,200)

Research and development expense (1,200,000)

(42,000)

Net income 6,500,000

9,300

Retained earnings, 1/1/15 500,000 given (147,000)

Dividends, 12/15/15 (1 ,500,000)

(46,500)

99,000

Inventory 8,500,000

272,000

Equipment 25,000,000

1,180,000

(1,510,200)

Land 6 ,000,000

300,000

Total assets 78 ,000,000

3,390,800

Additional paid in capital 50,000,000

2,500,000

Retained earnings, 12/31/15 5 ,500,000

(184,200)

Total liabilities and equities 78 ,000,000

37. (continued)

Calculation of Remeasurement Loss

K č S ER US$

Net monetary assets, 1/1/15 13,000,000

520,000

Increase in monetary assets:

Sales 25,000,000

875,000

Decrease in monetary assets:

(180,000)

Purchase of buildings, 3/5/15 (12 ,000,000)

(408,000)

Net monetary assets, 12/31/15 2 ,800,000

176,000

Net monetary assets, 12/31/15

at current exchange rate 2 ,800,000

37. (continued)

Part II. Explanation of the negative translation adjustment in Part I (a),

remeasurement gain in Part I (b), and remeasurement loss in Part I (c).

The negative translation adjustment in Part I (a) arises because of two

factors: (1) there is a net asset balance sheet exposure and (2) the Czech

koruna has depreciated against the U.S. dollar during 2015 (from $.040 at

The remeasurement gain in Part I (b) arises because of two factors: (1) there

is a net monetary liability balance sheet exposure and (2) the Czech koruna

has depreciated against the U.S. dollar. Under the temporal method, Cash

and Accounts Receivable are the only assets translated at the current

The remeasurement loss in Part I (c) arises because of two factors: (1) there

is a net monetary asset balance sheet exposure and (2) the Czech koruna has

depreciated against the U.S. dollar during 2015. Cash and Accounts

Receivable are the only assets translated at the current exchange rate (total