Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

51.(30 Minutes) (Prepare Journal entries for company emerging from bankruptcy

using fresh start accounting)

Holmes Corporation must use fresh start accounting because the

reorganization value of $225,000 is less than the company's allowed debts and

the original owners hold less than 50 percent of the voting stock after the

reorganization.

BOOK VALUES AFTER EMERGING FROM REORGANIZATION

— Total assets = $248,200 ($225,000 reorganization value plus proceeds from

sale of stock of $36,000 less $12,800 payment made to settle unsecured

liabilities [20 percent of $64,000])

JOURNAL ENTRIES

— Goodwill ...................................................................... 15,000

Additional Paid-In Capital .................................... 15,000

To adjust to total reorganization value as part of fresh

start accounting ($225,000 – $210,000).

— Salary Payable ............................................................ 18,000

Note Payable—1 year ........................................... 18,000

To record note issued for accrued salaries.

Gain on Discharge of Debt ................................... 51,200

To record payment of unsecured debts—20% payment

made.

— Gain on Debt Discharge ............................................. 130,200

Additional Paid-In Capital ($27,000 – $25,200) ........ 1,800

Develop Your Skills

Research Case 1

This case allows the student to review the official information provided by the

Securities and Exchange Commission in connection with bankrupt organizations,

as well as gain information about reporting requirements for organizations in

bankruptcies. In addition, this assignment allows the student to see how the SEC

attempts to educate the public on matters pertaining to financial investing.

This site includes a significant amount of general information including the

following:

The differences between a Chapter 7 and a Chapter 11 bankruptcy.

The risks incurred by the various parties.

A description of a prepackaged bankruptcy plan.

Research Case 2

This assignment provides the student with the chance to work with actual data

from a real company. Thus, students get a feel for the process of retrieving

information of interest about a company that is going through bankruptcy. In

require slow and meticulous study.

Here is the actual note – parts (a) and (b) -- as supplied by the company. This

information can serve as the basis for considerable class discussion.

(a) Plan of Reorganization

On April 30, 2010 (the ‘‘Effective Date’’), the Bankruptcy Court entered an order

confirming the Debtors’ Modified Fourth Amended Joint Plan of Reorganization

(the ‘‘Plan’’) and the Debtors emerged from Chapter 11 by consummating their

restructuring through a series of transactions contemplated by the Plan including

the following:

• Name Change. On the Effective Date, but after the Plan became effective and

prior to the distribution of securities under the Plan, SFI changed its corporate

name to Six Flags Entertainment Corporation. As used herein, unless the context

• Common Stock. Pursuant to the Plan, all of SFI’s common stock, preferred stock

purchase rights, preferred income equity redeemable shares (‘‘PIERS’’) and any

On the Effective Date, Holdings issued an aggregate of 54,777,778 shares of

common stock at $0.025 par value as follows: (i) 5,203,888 shares of common

stock to the holders of unsecured claims against SFI, (ii) 4,724,618 shares of

6,798,012 shares of common stock in an offering to certain purchasers for an

aggregate purchase price of $75.0 million, (v) 3,399,006 shares of common stock

in an offering to certain purchasers for an aggregate purchase price of $50.0

On June 21, 2010, the common stock commenced trading on the New York Stock

Exchange under the symbol ‘‘SIX.’’

• Prepetition Indebtedness. Pursuant to the Plan and on the Effective Date, all

outstanding obligations under notes issued by SFI and SFO (collectively, the

‘‘Prepetition Notes’’) were cancelled and the indentures governing such

obligations were cancelled, except to the extent to allow the Debtors,

Pursuant to the Plan and on the Effective Date, the Second Amended and

Restated Credit Agreement, dated as of May 25, 2007 (as amended, modified or

otherwise supplemented from time to time, the ‘‘Prepetition Credit Agreement’’),

allowing the Administrative Agent to exercise certain rights).

• Financing at Emergence. On the Effective Date, we entered into two exit

financing facilities: (i) an $890.0 million senior secured first lien credit facility

comprised of a $120.0 million revolving loan facility, which could have been

See Note 8 for a discussion of the terms and conditions of these facilities and

subsequent amendments, early repayments, and terminations from debt

extinguishment transactions.

• Fresh Start Accounting. As required by accounting principles generally

accepted in the United States (‘‘GAAP’’), we adopted fresh start accounting

effective May 1, 2010 following the guidance of Financial Accounting Standards

The implementation of the Plan and the application of fresh start accounting

results in financial statements that are not comparable to financial statements in

As used herein, ‘‘Successor’’ refers to the Company as of the Effective Date and

‘‘Predecessor’’ refers to SFI together with its consolidated subsidiaries prior to

the Effective Date.

(b) Fresh Start Accounting and the Effects of the Plan

Fresh start accounting results in a new basis of accounting and reflects the

allocation of the Company’s estimated fair value to its underlying assets and

liabilities. The Company’s estimates of fair value are inherently subject to

Fresh start accounting provides, among other things, for a determination of the

value to be assigned to the equity of the emerging company as of a date selected

for financial reporting purposes, which for the Company is April 30, 2010, the date

that the Debtors emerged from Chapter 11. The Plan required the contribution of

equity from the creditors representing the unsecured senior noteholders of SFI,

of which $555.5 million was raised at a price of $14.71 per share, as adjusted to

reflect the June 2011 two-for-one stock split described in Note 12. Holdings also

capital expenditures and the discount rate utilized.

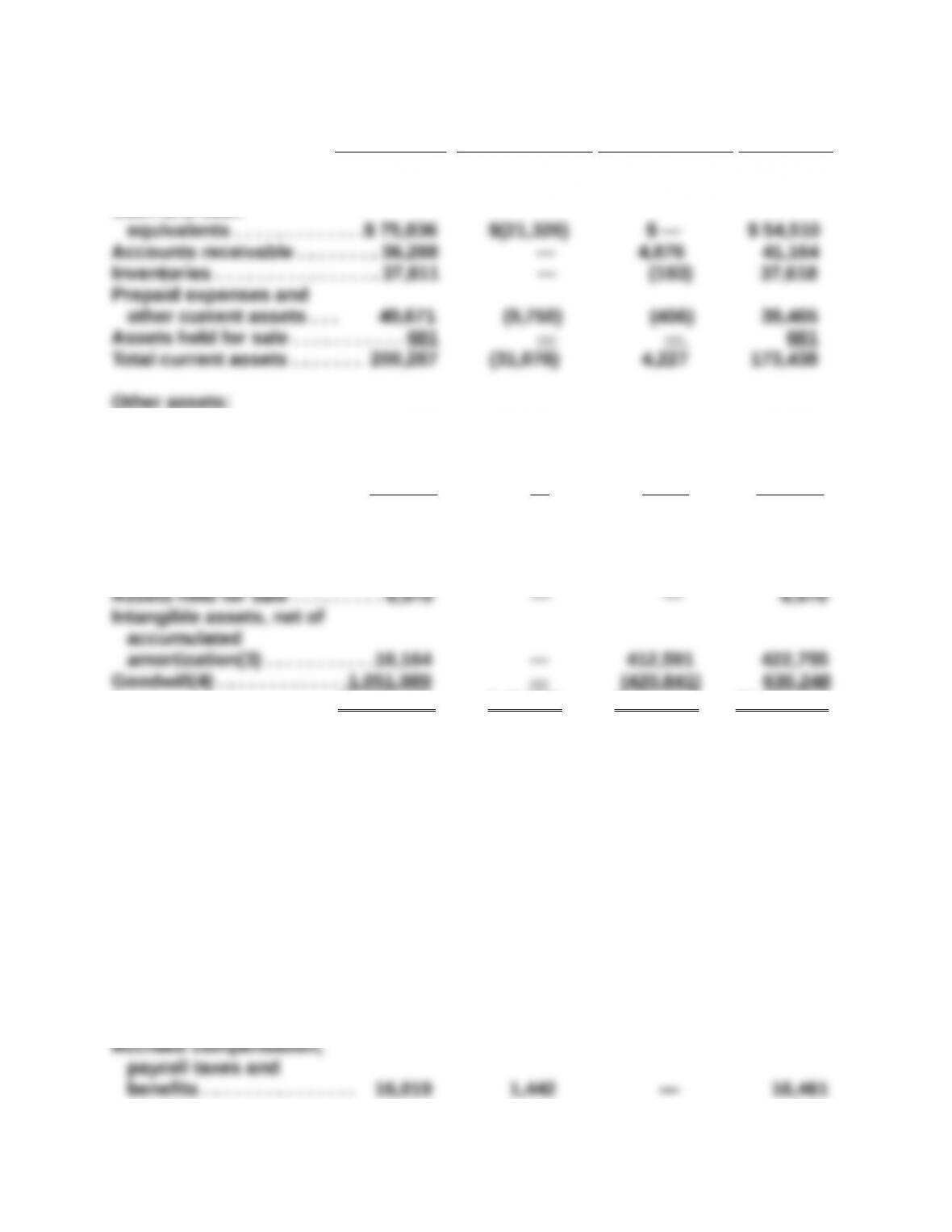

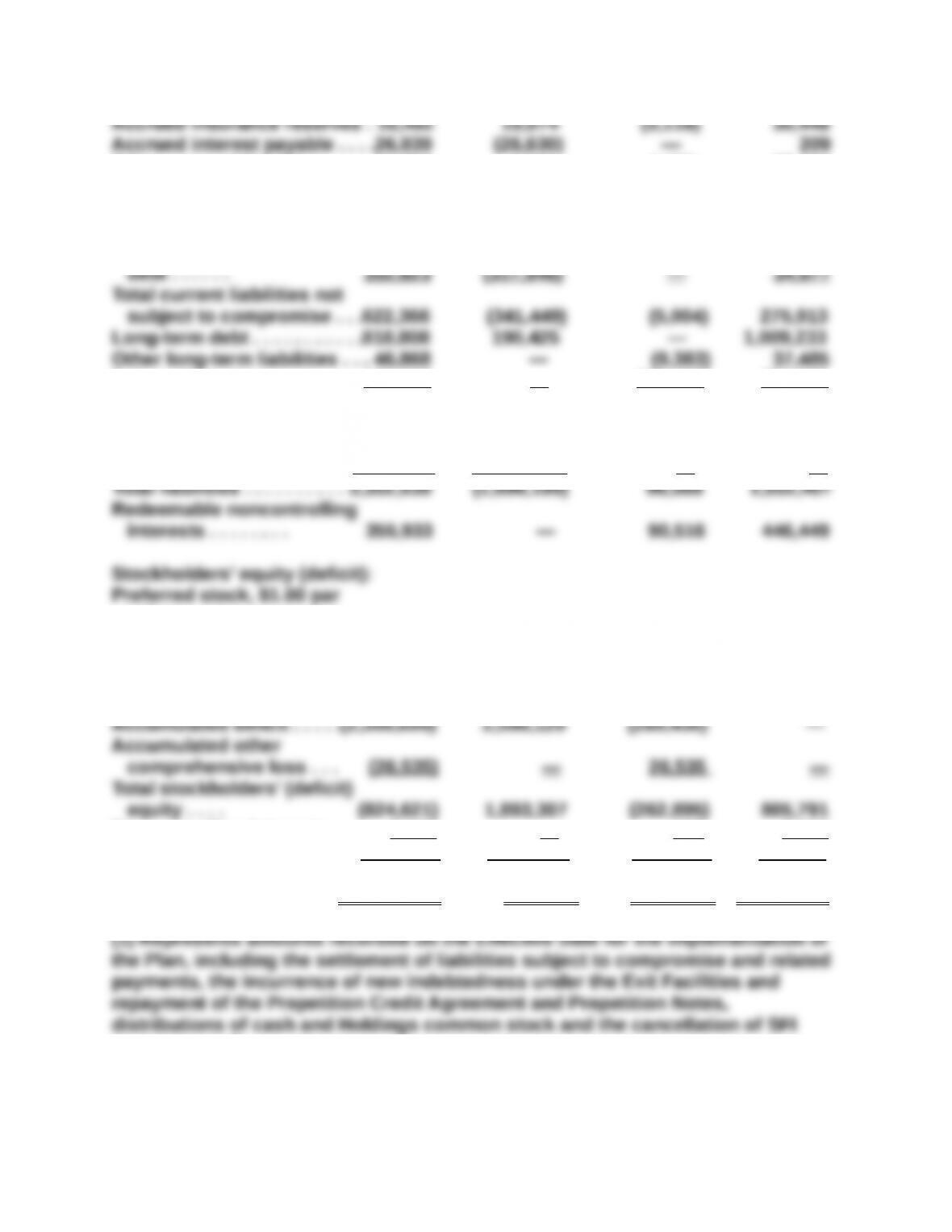

The four-column consolidated statement of financial position as of April 30, 2010

(see below) reflects the implementation of the Plan. Reorganization adjustments

have been recorded within the condensed consolidated balance sheets as of April

30, 2010 to reflect effects of the Plan, including discharge of liabilities subject to

compromise and the adoption of fresh start accounting in accordance with FASB

ASC 852. The reorganization value of the Company of approximately $2.3 billion

was based on the equity value of equity raised plus new indebtedness and fair

value of Partnership Parks ‘‘put’’obligations as follows (in thousands):

Equity value based on equity raised(1) . . . . . . . . . . . . . . . . . . . . . . . . . $ 805,791

Add: Redeemable noncontrolling interests(2) . . . . . . . . . . . . . . . . . . 446,449

Add: Exit First Lien Facility . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 770,000

Add: Exit Second Lien Facility . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 250,000

_______________________

(1) Equity balance is calculated based on 54,777,778 shares of Holdings common

stock at the price of $14.71 per share pursuant to the Plan, as adjusted to reflect

the June 2011 two-for-one stock split described in Note 12.

the annual guaranteed minimum distributions to the holders of the ‘‘put’’ rights

and a discount rate of 7%.

_______________________

Under fresh start accounting, the total Company value is adjusted to

reorganization value and is allocated to our assets and liabilities based on their

respective fair values in conformity with the purchase method of accounting for

business combinations in FASB ASC Topic 805, Business Combination (‘‘FASB

ASC 805’’). The excess of reorganization value over the fair value of tangible and

comprehensive loss were eliminated.

The valuations required to determine the fair value of the Company’s assets as

presented below represent the results of valuation procedures performed by

SIX FLAGS ENTERTAINMENT CORPORATION

CONDENSED CONSOLIDATED BALANCE SHEET

(in thousands)

April 30, 2010

Reorganization Fresh Start

Predecessor Adjustments(1) Adjustments(2) Successor

ASSETS

Current assets:

Cash and cash

Debt issuance costs . . . . . . . . 11,817 28,184 — 40,001

Restricted-use

investment securities . . . . . . .2,753 — — 2,753

Deposits and other assets . . . 97,677 — 6,643 104,320

Total other assets . . . . . . . . . 112,247 28,184 6,643 147,074

Property and equipment,

at cost, net . . . . . 1,507,677 — (78,304) 1,429,373

Total assets . . . . . . . . . . . $2,888,442 $ (2,892) $ (75,684) $2,809,866

LIABILITIES and EQUITY (DEFICIT)

Liabilities not subject to compromise:

Current liabilities:

Accounts payable . . . . . . . $ 92,198 $ (20,272) $ — $71,926

Other accrued liabilities . . . . .52,753 2,883 1,438 57,074

Deferred income . . . . . . . . . . .61,033 — (1,324) 59,709

Liabilities from discontinued

operations . . 5,409 — — 5,409

Current portion of long-term

Deferred income taxes . . . . .118,821 — 110,955 229,776

Total liabilities not subject

to compromise . . . . . . . . 1,606,863 (151,024) 96,568 1,552,407

Liabilities subject to

compromise . . . . . . . . . . 1,745,175 (1,745,175) — —

value . . . . . . . . — — — —

New common stock . . . . . . . . . . . — 685 — 685

Old common stock . . . . . . . . . 2,458 (2,458) — —

Capital in excess of

par value . . . . . . . . . 1,508,155 (703,049) — 805,106

Noncontrolling interests . . . . . 5,092 — 127 5,219

Total (deficit) equity . . . . . . .(819,529) 1,893,307 (262,768) 811,010

Total liabilities and

equity (deficit) . . . . $ 2,888,442 $ (2,892) $ (75,684) $2,809,866

_________________

common stock.

The Plan’s impact resulted in a net decrease of $21.3 million in cash and cash

equivalents. The significant sources and uses of cash were as follows (in

thousands):

Sources:

Net amount borrowed under the Exit First Lien Term Loan . . . . . . . . . $ 762,300

Net amount borrowed under the Exit Second Lien Loan Facility . . . . . . 246,250

Uses:

Repayments of amounts owed:

Prepetition Credit Agreement—long term portion of term loan . . . . . 818,125

2016 Notes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 330,500

Prepetition Credit Agreement—revolving portion . . . . . . . . . . . . . . . . 270,269

Payments:

Exit Facilities’ debt issuance costs . . . . . . . . . . . . . . . . . . . . . . . . . . . 29,700

Accrued interest . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 96,950

The gain on the cancellation of liabilities subject to compromise, before income

taxes, was calculated as follows:

Extinguishment of the 2010 Notes, 2013 Notes, 2014 Notes and 2015

Notes (collectively, the ‘‘SFI Senior Notes’’) . . . . . . . . . . . . . . . . . . .$ 868,305

Extinguishment of the PIERS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 306,650

Write-off of the accrued interest on the SFI Senior Notes . . . . . . . . . . . 29,868

Write-off debt issuance costs on the Prepetition Credit Agreement

compromise, before income taxes . . . . . . . . . . . . . . . . . . . . . .$1,087,516