35. (60 Minutes) (Consolidation worksheet for combination with upstream inventory

transfers and downstream transfer of land. Also asks about transfer of a building.

Parent uses partial equity method.)

Consideration transferred …………….……..….…. $570,000

Noncontrolling interest fair value…………………. 380 ,000

to customer list………………………………..….…. 100 ,000

20 yrs…..…..…..………………………………$5,000

-0-

a. CONSOLIDATION ENTRIES

Entry *TL

Entry *G

Retained earnings, 1/1/15 (Keller) ……………… 10,000

Entry *C

Retained earnings, 1/1/15 (Gibson) ..….......... 9,000

Investment in Keller ………….…………….…... 9,000

Parent is applying the partial equity method as can be seen by the amount

in the Equity in earnings of Keller Company account (60 percent of the

reported balance). Thus, the parent’s share of amortization of $3,000

35. (continued)

Entry S

Common stock (Keller) ……………….…..….….... 320,000

Additional paid-in capital ……………….…………. 90,000

Entry A

Customer list……….……………….…………………… 95,000

Entry I

Equity in earnings of Keller …………………….… 84,000

Investment in Keller ………….…………….…... 84,000

To eliminate intra-entity income accrual.

Entry P

Liabilities………………………….…………….…..….… 40,000

Accounts receivable ………….……….…..…... 40,000

To eliminate intra-entity debt.

Entry Tl

35. (continued)

Entry G

Cost of goods sold ……………..…………….….….. 12,000

Net income attributable to noncontrolling interest

Keller reported net income …………..…………………..….…..….….... $140,000

Excess fair value amortization ……………..………….….…..….…..… (5,000)

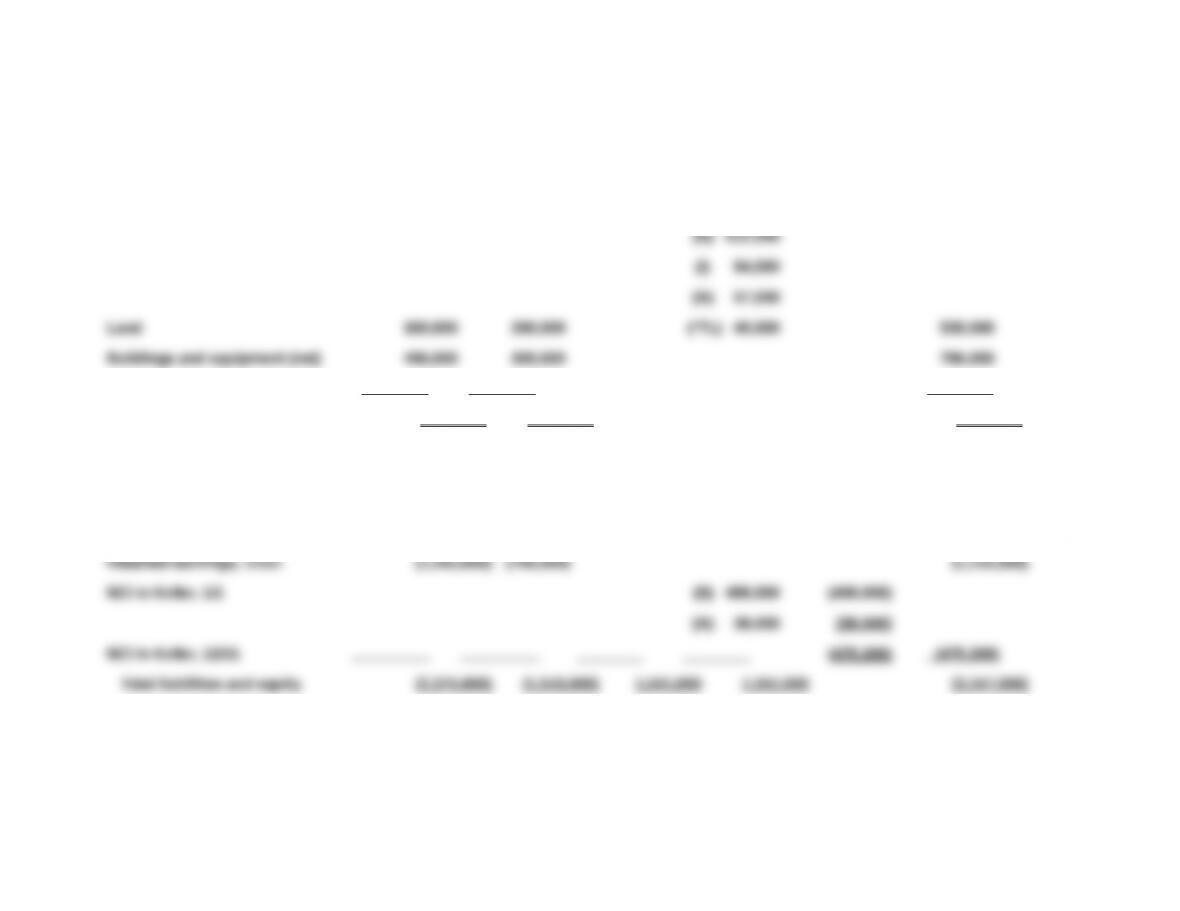

35. a. (continued) GIBSON AND KELLER

Consolidation Worksheet

Year Ending December 31, 2015

Consolidation Entries Noncontrolling Consolidated

Accounts Gibson Keller Debit Credit Interest Totals

Sales (800,000) (500,000) (TI) 200,000 (1,100,000)

Cost of goods sold 500,000 300,000 (G) 12,000 (*G) 10,000 602,000

(TI) 200,000

Operating expenses 100,000 60,000 (E) 5,000 165,000

RE, 1/1—Keller (620,000) (*G) 10,000

(S) 610,000

Net income (above) (284,000) (140,000) (279,800)

Dividends declared 115 ,000 60 ,000 (D) 36,000 24,000 115 ,000

Retained earnings, 12/31 (1 ,285,000) (700 ,000) (1 ,231,800)

Cash 177,000 90,000 267,000

Accounts receivable 356,000 410,000 (P) 40,000 726,000

Inventory 440,000 320,000 (G) 12,000 748,000

Investment in Keller 726,000 (D) 36,000 (*C) 9,000 -0-

Customer list -0- -0- (A) 95,000 (E) 5,000 90 ,000

Total assets 2 ,375,000 1 ,510,000 3 ,157,000

Liabilities (480,000) (400,000) (P) 40,000 (840,000)

Common stock (610,000) (320,000) (S) 320,000 (610,000)

Additional paid-in capital (90,000) (S) 90,000

35. (continued)

b. If the intra-entity transfer had been a building rather than land, two

adjustments to the consolidation entries would be needed. Entry *TL

Entry *TA

Retained earnings, 1/1/15 (Gibson) ..….......... 36,000

To defer unrealized gain ($40,000 original amount less one year of

excess depreciation at $4,000 per year) as of beginning of year. Entry

also returns Buildings account to historical cost (from $100,000 to

$140,000) and Accumulated Depreciation account to historical cost

(original $80,000 less one year of excess depreciation at $4,000).

Because the Buildings account is shown at net value in the

information given in this problem, the above entry would probably be

made as follows:

Entry *TA (Alternative)

Retained earnings, 1/1/15 (Gibson) ..….......... 36,000

Buildings (net) …………..……………………..…. 36,000

Entry ED

To remove excess depreciation for current year created by transfer

36. (40 Minutes) (Prepare consolidation worksheet with intra-entity transfer of

inventory and land. No outside ownership exists)

a. Skyline reported net income……………..………….….…..….…..…... $(88,000)

Patented technology amortization……………….…………………….. 15,000

b. Acquisition-Date Fair Value Allocation

Consideration transferred (fair value of shares issued) ........ $450,000

Book value of subsidiary …………………………………….….…..….… 300 ,000

Fair value in excess of book value ………………….…..….…..….… $150,000

Excess fair over book value assigned to:

Unrealized Upstream Inventory Gross Profit, 1/1

Inventory being held ($50,000 × 72%) ……….……………………….. $36,000

Gross profit rate ($20,000 ÷ $50,000) …………………………..…..… 40%

Unrealized gross profit, 1/1 ……………………….….…..….…..….….. $14 ,400

Unrealized Upstream Inventory Gross Profit, 12/31

CONSOLIDATION ENTRIES

Entry *G

computed above.

Entry S

Common stock (Skyline) …………..……………..….... 120,000

Additional paid-in capital (Skyline) ………..…..….. 30,000

36. (continued)

Entry A

Trademarks ……………..……………….…………….….…. 30,000

Patented technology …………..……………….………… 105,000

Entry I

Investment income …………..……….…..….…..….….. 55,400

Investment in Skyline ……………………………….. 55,400

To remove intra-entity income accrued by parent using the equity

method.

Entry D

Entry Tl

Revenues ………..……………….……………..…..….….… 80,000

Cost of goods sold ……………..…………….….….. 80,000

To eliminate intra-entity inventory transfer for current year.

Entry G

Entry TL

Gain on sale of land …………………………….………... 18,000

Land ……………………………………………….…..…... 18,000

To remove gain from intra-entity transfer of land during current year.

Entry P

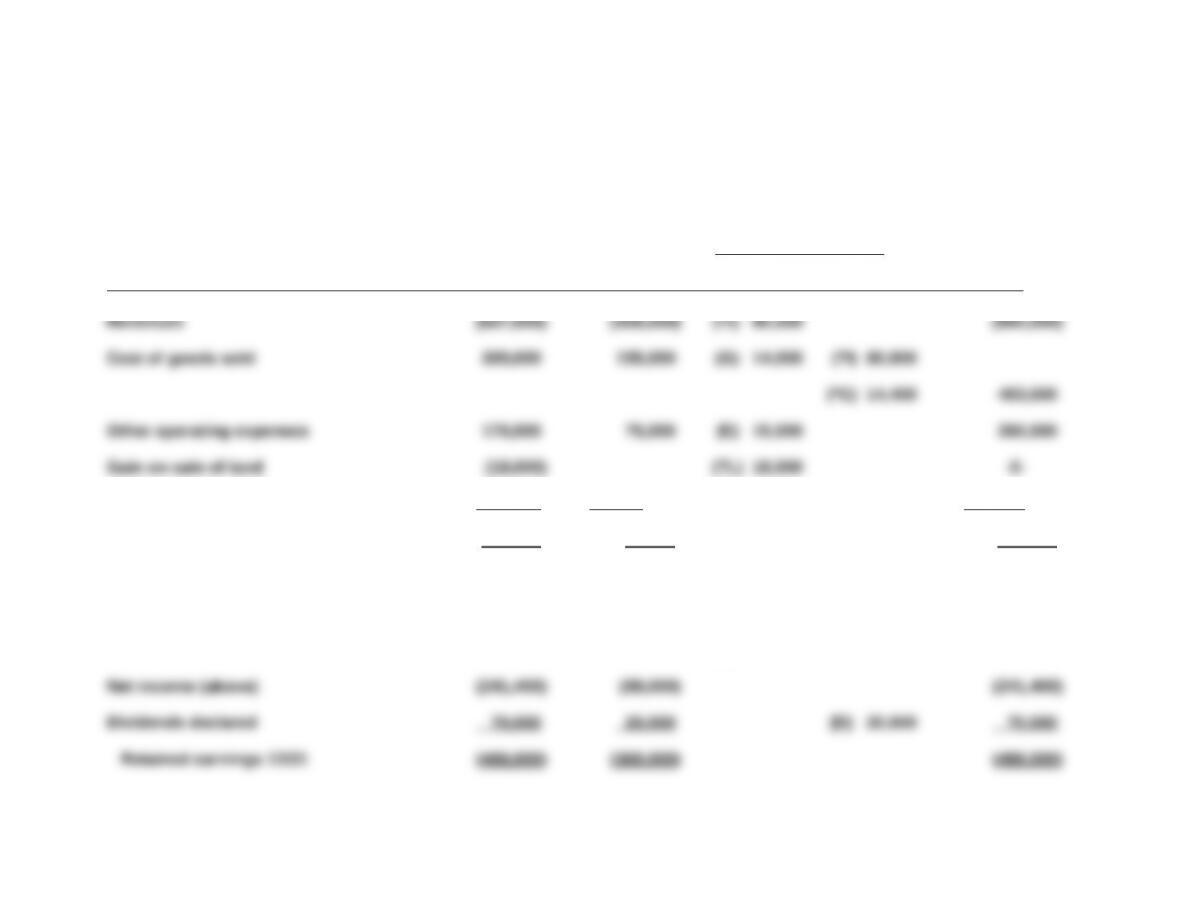

36. (continued) PARKWAY AND SKYLINE

Consolidation Worksheet

Year Ending December 31, 2015

Consolidation Entries Consolidated

Accounts Parkway Skyline Debit Credit Totals

Investment income (55 ,400) (I) 55,400 -0-

Net income (241 ,400) (88 ,000) (241 ,400)

Retained earnings 1/1 (314,600) (292,000) (*G) 14,400 (314,600)

(S) 277,600 -0-

(A) 135,000 -0-

(I) 55,400

Trademarks 50,000 (A) 30,000 80,000

Patented technology 130,000 (A) 105,000 (E) 15,000 220,000

Land, buildings, and equipment (net) 637 ,000 283 ,000 (TL) 18,000 902 ,000

Total liabilities & stockholders’ equity (1 ,650,000) (725 ,000) 844 ,400 844 ,400 (1 ,800,000)

Chapter 5 Excel Case Solution

Excel Case Equity in Shawn Co. Earnings

2014 78,000

Fair Value Allocation Schedule 1/1/2014El profit (34,200)

Consideration transferred 1,000,000 Amortization (12 ,600)

C.S. 500,000 Equity earnings 31 ,200

Inventory El profit (37,800)

Shawn sells GPR remaining Amortization (12 ,600)

to Patrick 60% 30% Equity earnings 68 ,800

Intra-entity Inventory Transfers (upstream) Shawn Co. dividends

Sales Inventory Intra. profit 2014 25,000

Consolidation Adjustments

Investment account *G RE-Shawn 34,200

Cost 1,000,000

COGS 34,200

2014 Equity earnings 31,200

dividends (25 ,000)

2015 Equity earnings 68,800

dividends (27 ,000)

A Tradename 302,400

12/31/15 1 ,048,000

Investment in Shawn 302,400

27,000

E Amortization expense 12,600

Tradename

12,600

IT Sales 210,000

COGS

Analysis and Research—Accounting Information and Salary Negotiations

a. With common control over related enterprises, a consolidated income statement better

portrays economic reality. For example, it is likely that the Stadium’s concession and parking

Searching the FASB ASC for “separate statements” and then “intra-entity” yields the following

relevant support:

There is a presumption that consolidated financial statements are more meaningful than

As consolidated financial statements are based on the assumption that they represent the

Granger Eagles Team and Stadium

Consolidated Income Statement

Ticket revenues $2,000,000

Concession revenue 800,000

COGS 250,000

Depreciation 80,000

b. Other pertinent factors include

Any available comparisons for the market values for the players