Archives

978-0078025549 Appendix C Appendix C Part 1

Interest is the cost of borrowing money. Simple interest is interest we earn on the initial investment only. Compound interest is the interest Present value tells us the value today of receiving some larger amount in the future. The discount […]

978-0078025549 Appendix C Appendix C Part 2

Exercise C-7 (LO C-3) Annuity payment Annual Rate Interest compounded Period invested Future value of annuity $2,000 13% Annually 30 years $586,398.43a Exercise C-8 (LO C-3) Annuity payment Annual Rate Interest compounded Period invested Present value of annuity Option 1 […]

978-0078025549 Appendix D Appendix D Part 1

Question D-1 (LO D-1) A company might invest in another company to (1) receive dividends, earn interest, and gain from the increase in the value of their investment, (2) temporarily invest excess cash created by Question D-2 (LO D-1) Companies […]

978-0078025549 Appendix D Appendix D Part 2

Exercise D-4 (LO D-2) Requirement 1 March 1 Debit Credit Investments (3,000 shares × $62) 186,000 July 1 Cash ($1.25 × 3,000 shares) 3,750 Dividend Revenue 3,750 (Receive cash dividends) October 1 Cash (750 shares × $70) 52,500 Investments (750 […]

978-0078025549 Appendix D Appendix D Part 3

Requirement 1 January 2 Debit Credit Investments 105,000 February 14 Investments 7,200 Cash 7,200 (Purchase preferred stock) May 15 Cash (300 shares × $62) 18,600 Loss (difference) 2,400 Investments (300 shares × $70) 21,000 (Sell investments below recorded amount) December […]

978-0078025549 Appendix E Appendix E

Differences in accounting standards cause problems for investors in comparing companies whose financial statements are prepared under different accounting rules. Investors unfamiliar with the accounting multinational corporations to comply with multiple sets of accounting rules. The IASB’s main objective is […]

978-0078025549 Chapter 1 Lecture Note

Learning Objectives LO1-1 Describe the two primary functions of financial accounting. LO1-2 Understand the business activities that financial accounting measures. LO1-3 Determine how financial accounting information is communicated through financial statements. LO1-4 Describe the role that […]

978-0078025549 Chapter 1 Solution Exercise B Part 1

Chapter 1 A Framework for Financial Accounting 1. a. 2. b. 3. a. 4. c. 5. b. 6. a. 7. c. EXERCISES Exercise 1-1 Transaction Account Activity 1. Falcon provides services to customers. Revenue Operating 2. Falcon pays salaries for […]

978-0078025549 Chapter 1 Solution Exercise B Part 2

Exercise 1-12 (LO 1-3) Requirement 1 Squirrel Tree Services Balance Sheet Assets Liabilities Cash $ 8,700 Accounts payable $ 9,600 Supplies 1,700 Salaries payable 4,500 Prepaid insurance 3,200 Notes payable 22,700 Building 75,000 Total liabilities 36,800 Stockholders’ Equity Common stock […]

978-0078025549 Chapter 1 Solution Manual Part 1

Question 1-1 (LO 1-1) Accounting is the language of business. Whereas a basic math class might involve adding, subtracting, and solving for unknown variables, accounting involves learning to measure Question 1-2 (LO 1-1) Those interested in making decisions about a […]

978-0078025549 Chapter 1 Solution Manual Part 2

Exercise 1-4 (LO 1-2) Requirement 1 Revenues − Expenses = Net Income Requirement 2 Assets = Liabilities + Stockholders’ equity $50,000 = $27,000 + $X $50,000 − $27,000 = $23,000 Exercise 1-5 (LO 1-2) Requirement 1 Revenues − Expenses = […]

978-0078025549 Chapter 1 Solution Manual Part 3

Exercise 1-17 (LO 1-3) ($ in billions) Total change in cash =Operating cash flows +Investing cash flows +Financing cash flows 1. Total change in cash =Operating cash flows +Investing cash flows +Financing cash flows 2. Total change in cash =Operating […]

978-0078025549 Chapter 1 Solution Manual Part 4

Problem 1-1B (LO 1-2) Type of business activity Transactions 1. Operating Pay for advertising 2. Financing Pay dividends to stockholders 3. Operating Collect cash from customer for previous sale 4. Investing Purchase a building to be used for operations 5. […]

978-0078025549 Chapter 1 Solution Manual Part 5

Assumption violated 1. Periodicity 2. Monetary unit 3. Going concern 4. Economic entity 1. h. 2. g. 3. f. 4. a. 5. d. 6. e. 7. i. 8. b. 9. c. The three primary forms of business organizations include sole […]

978-0078025549 Chapter 1 Solution Problem C

Type of business activity Transactions 1. Financing Issue common stock. 2. Financing Collect cash from a bank loan. 3. Operating Sell products to customers. 4. Operating Pay workers’ wages. Account classifications Account Names 1. Asset Accounts Receivable 2. Asset Land […]

978-0078025549 Chapter 10 Lecture Note Part 1

shares to the general public. The reporting of common stock, preferred stock, and treasury stock are illustrated using one example company, Canadian Falcon. Many competing texts develop a Chapter 10 Stockholders’ Equity INSTRUCTOR’S MANUAL Learning Objectives LO10-1 Identify the […]

978-0078025549 Chapter 10 Lecture Note Part 2

Forever Young has the following beginning balances in its stockholders’ equity accounts on and retained earnings, $10,000. Net income for the year ended December 31, 2015 is $16,000. Required: Solution: 1. Forever Young Balance Sheet (partial) December 31, 2015 Stockholders’ […]

978-0078025549 Chapter 10 Solution Exercise B

Terms __g___ 1. Limited liability company __e___ 2. Limited liability __d___ 3. Articles of Incorporation __h___ 4. Organization chart __a___ 5. S Corporation __b___ 6. Publicly held corporation __c___ 7. Initial public offering __f___ 8. Double taxation Definitions a. Allows […]

978-0078025549 Chapter 10 Solution Manual Part 1

<<PRODUCTION: Note that this chapter does not have continued lines for the review questions, as did all other chapters. Also, note that the running foot needs to be corrected on all but the first page, to show the correct edition […]

978-0078025549 Chapter 10 Solution Manual Part 2

Exercise 10-6 (LO 10-2, 10-3, 10-4) January 2, 2015 Debit Credit Cash (100,000 x $35) 3,500,000 Common Stock (100,000 x $1) 100,000 February 6, 2015 Cash (3,000 x $11) 33,000 Preferred Stock (3,000 x $10) 30,000 Additional Paid-in Capital (difference) […]

978-0078025549 Chapter 10 Solution Manual Part 3

Problem 10-6A (LO 10-2, 10-3, 10-4, 10-5, 10-7) Requirement 1 January 2, 2015 Debit Credit Cash (110,000 x $70) 7,700,000 Common Stock (110,000 x $1) 110,000 February 14, 2015 Cash (60,000 x $12) 720,000 Preferred Stock (60,000 x $10) 600,000 […]

978-0078025549 Chapter 10 Solution Manual Part 4

* $140,000 beginning balance in retained earnings + $150,000 net income – $115,000 in dividends Financial Analysis: American Eagle AP10-2 Requirement 1 $0.01 par value per share. The par value per share is listed in the stockholders’ Requirement 2 249,566,000 […]

978-0078025549 Chapter 10 Solution Problem C

Problem 10-1C Terms __h__ 1. 100% stock dividend __a__ 2. Statement of stockholders’ equity __e__ 3. Treasury stock __b__ 4. Value stocks __j__ 5. PE ratio __d__ 6. Stockholders’ equity section of the balance sheet __c__ 7. Return on equity […]

978-0078025549 Chapter 11 Lecture Note

INSTRUCTOR’S MANUAL Learning Objectives LO11-1 Classify cash transactions as operating, investing, or financing activities. LO11-2 Prepare the operating activities section of the statement of cash flows using the indirect method. LO11-3 Prepare the investing activities section and […]

978-0078025549 Chapter 11 Solution Exercise B

Items __e__ 1. Indirect method __d__ 2. Direct method __f__ 3. Depreciation expense __g__ 4. Cash return on assets __a__ 5. Operating activities __b__ 6. Investing activities __h__ 7. Financing activities __c__ 8. Noncash activities Descriptions a. Cash transactions involving […]

978-0078025549 Chapter 11 Solution Manual Part 1

Question 11-1 (LO 11-1) The three categories of cash flows are operating activities, investing activities, and financing activities. Operating activities include cash receipts and cash payments for transactions relating to revenue and expense activities, essentially the very same activities reported […]

978-0078025549 Chapter 11 Solution Manual Part 2

Exercise 11-7 (LO 11-2, 11-3) Technology Solutions Statement of Cash Flows For the Year Ended December 31, 2015 Cash Flows from Operating Activities Net income Adjustments to reconcile net income to net cash flows from operating activities: List of items […]

978-0078025549 Chapter 11 Solution Manual Part 3

Google and Yahoo’s cash flow to sales ratio is similar to Apple and much higher than Dell, while its asset turnover is lower than Apple or Dell. Google and Yahoo’s *Problem 11-6A (LO 11-5) Alliance Technologies Statement of Cash Flows […]

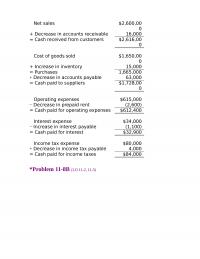

978-0078025549 Chapter 11 Solution Manual Part 4

Net sales $2,600,00 0 + Decrease in accounts receivable 16,000 0 Cost of goods sold $1,650,00 0 + Increase in inventory 15,000 = Purchases 1,665,000 + Decrease in accounts payable 63,000 = Cash paid to suppliers $1,728,00 0 Operating expenses […]

978-0078025549 Chapter 11 Solution Problem C

Type of Activity Cash Inflow or Outflow Transaction F CI 1. Issuance of common stock F CI 2. Issuance of bonds I CO 3. Investment in bonds I CI 4. Collection of a note receivable O CI 5. Sale of […]

978-0078025549 Chapter 12 Lecture Note

LO12-1 Perform vertical analysis. LO12-2 Perform horizontal analysis. LO12-3 Use ratios to analyze a company’s risk. LO12-4 Use ratios to analyze a company’s profitability. LO12-5 Distinguish persistent earnings from one-time items. LO12-6 Explain quality […]

978-0078025549 Chapter 12 Solution Exercise B

h1. Conservative accounting practices d2. Discontinued operation a3. Extraordinary item c4. Horizontal analysis g5. Liquidity b6. Quality of earnings f7. Solvency e8. Vertical analysis Descriptions a. A profit or loss unusual in nature and infrequent in occurrence. b. The ability […]

978-0078025549 Chapter 12 Solution Manual Part 1

Question 12-1 (LO 12.1, 12.2) The three types of comparisons commonly used in financial statement analysis are Question 12-2 (LO 12.1, 12.2) For vertical analysis, we express each item as a percentage of the same base amount, such as a […]

978-0078025549 Chapter 12 Solution Manual Part 2

Exercise 12-5 (LO12.3) Requirement 1 Risk Ratios Calculations Receivables turnover ratio $19,310,000 Average collection period 365 14.3 = 25.5 days Inventory turnover ratio $12,250,000 ($1,500,000 + $2,000,000) / 2 = 7.0 times Average days in inventory 365 7.0 = 52.1 […]

978-0078025549 Chapter 12 Solution Manual Part 3

Accounts payable $ 30,150 $ 46,800 $(16,650) (35.6) Long-term liabilities: Notes payable 138,150 127,600 10,550 8.3 Stockholders’ equity: Common stock 144,000 144,000 0 0 Retained earnings 118,350 68,000 50,350 74.0 Total liabilities and equity $450,000 $400,000 $50,000 12.5 Problem 12-4A […]

978-0078025549 Chapter 12 Solution Manual Part 4

($ in thousands) Increase (Decrease) 2013 2012 Amount % Net sales $ 3,475,802 $ 3,120,065 $ 355,737 11.4 Cost of sales 2,085,480 1,975,471 110,009 5.6 Gross profit 1,390,322 1,144,594 245,728 21.5 Selling, general, and admin. 834,601 718,123 116,478 16.2 Loss […]

978-0078025549 Chapter 12 Solution Problem C

The Sports Warehouse Income Statements For the Year Ended December 31, 2015 Equipment Apparel Amount % Amount % Sales $1,700,000 100.0 $2,850,000 100.0 Cost of goods sold 1,100,000 65.7 1,400,000 49.1 Gross profit 600,000 35.3 1,450,000 50.9 Operating expenses 250,000 […]

978-0078025549 Chapter 2 Lecture Note

Questions Learning Objective(s) Topic (Min.) 1 LO2-1 Understand the difference between external and internal transactions 5 2 LO2-1 List steps to measure external transactions 5 3 LO2-2 Explain dual effect of transactions 5 Chapter 2 The Accounting Cycle: During the […]

978-0078025549 Chapter 2 Solution Exercise B Part 1

1. d. 2. b. 3. a. 4. e. 5. c. Assets =Liabilities +Stockholders’ Equity 1. Increase =No effect +Increase 2. Decrease =No effect +Decrease 3. Increase =Increase +No effect Chapter 2 The Accounting Cycle: During the Period EXERCISES Exercise 2-1 […]

978-0078025549 Chapter 2 Solution Exercise B Part 2

Exercise 2-14 Cash (1) (4) 4,000 16,000 8,000 9,000 4,000 (2) (3) Transaction (8) is not posted to the Cash T-account because a purchase on account does not involve cash. (6) 3,000 1,000 7,000 (5) (7) 10,000 Exercise 2-15 Cash […]

978-0078025549 Chapter 2 Solution Manual Part 1

Question 2-1 (LO 2-1) External transactions are transactions between the company and a separate economic entity. Question 2-2 (LO 2-1) 1. Use source documents to identify accounts affected by external transactions. 2. Analyze the impact of the transaction on the […]

978-0078025549 Chapter 2 Solution Manual Part 2

Exercise 2-1 (LO 2-1) 1. d. 2. b. 3. a. 4. e. 5. c. Exercise 2-2 (LO 2-2) Assets =Liabilities +Stockholders’ Equity 1. Increase =No effect +Increase 2. Increase =Increase +No effect 3. Increase =No effect +Increase * One asset […]

978-0078025549 Chapter 2 Solution Manual Part 3

Exercise 2-14 (LO 2-5) Cash (1) (4) 5,000 15,000 8,000 9,000 3,000 (2) (3) Transaction (8) is not posted to the Cash T-account because a purchase on account does not involve cash. Exercise 2-15 (LO 2-5) Cash Accounts Receivable (3) […]

978-0078025549 Chapter 2 Solution Manual Part 4

Problem 2-2A (LO 2-2) Transaction Assets = Liabilities + Stockholders’ Equity 1. Provide services to $1,600. 2. Pay $400 for current month’s rent. −$400 =$0 +−$400 3. Hire a new employee, who will be paid $500 at the end $0 […]

978-0078025549 Chapter 2 Solution Manual Part 5

Problem 2-8A (connued) (10) Sep. 30 Salaries Expense 4,000 (11) Sep. 30 Dividends 1,100 Cash 1,100 (Pay dividends) Cash 4,000 (Pay salaries for current month) Problem 2-8A (connued) Requirements 2 and 3 Cash Accounts Receivable Supplies Bal. 6,500 (1) 4,700 […]

978-0078025549 Chapter 2 Solution Manual Part 6

Problem 2-4B (LO 2-4) Transactions for Eli’s Insurance Services May 2 Debit Credit Cash 300 May 5 Repairs and Maintenance Expense 425 Accounts Payable 425 (Receive maintenance services on account) May 7 Cash 500 Notes Payable 500 (Receive cash and […]

978-0078025549 Chapter 2 Solution Manual Part 7

Problem 2-8B (continued) Requirements 2 and 3 Cash Accounts Receivable Supplies Bal. 3,200 (1) 13,000 1,100 (5) 3,000 (6) Bal. 600 (4) 9,000 7,000 (9) Bal. 700 (3) 1,000 Equipment Accounts Payable Notes Payable Bal. 9,400 (2) 3,500 0 1,000 […]

978-0078025549 Chapter 2 Solution Manual Part 8

Great Adventures, Inc. Trial Balance July 31, 2015 Accounts Debit Credit Cash $ 9,000 Prepaid Insurance 4,800 Supplies 1,800 Equipment 12,000 Additional Perspective P2-1 (continued) Requirement 2 Additional Perspective 2-1 (concluded) Requirement 3 Cash (1) 10,000 (2) 10,000 (8) 2,000 […]

978-0078025549 Chapter 2 Solution Problem C Part 1

Transaction Assets = Liabilities + Stockholders’ Equity 1. Obtain a loan at the bank Increase = Increase + No effect 2. Issue common stock to stockholders for 3. Purchase equipment for cash. No effect* =No effect +No effect 4. Pay […]

978-0078025549 Chapter 2 Solution Problem C Part 2

Problem 2-7C Requirement 1 April 1 Debit Credit Cash 50,000 April 2 Cash 20,000 Common Stock 20,000 (Issue common stock) April 7 Equipment 40,000 Cash 40,000 (Purchase equipment) April 10 Supplies 4,000 Accounts Payable 4,000 (Purchase cleaning supplies on account) […]

978-0078025549 Chapter 3 Lecture Note Part 1

LO3-2 Distinguish between accrual-basis and cash-basis accounting. LO3-3 Demonstrate the purposes and recording of adjusting entries. LO3-4 Post adjusting entries and prepare an adjusted trial balance. LO3-5 Prepare financial statements using the adjusted trial balance. […]

978-0078025549 Chapter 3 Lecture Note Part 2

Customers receiving $700 of services from a company have not been billed as of the end of December. These customers will be billed on January 4 and are expected to pay the full amount owed on January 9. Solution Adjusting […]

978-0078025549 Chapter 3 Solution Exercise B Part 1

1. May 2. 2. Revenue would be recognized as each magazine is delivered. 3. November 21. 4. July 7. 1. May 2. 2. November 21. 3. November 4. 4. One month’s worth of rent expense is recorded each month. 1. […]

978-0078025549 Chapter 3 Solution Exercise B Part 2

Requirement 3 Blue Hens Corporation Balance Sheet December 31, 2015 Assets Liabilities Cash $ 15,700 Accounts payable $ 9,300 Accts. receivable 132,500 Salaries payable 12,500 Stockholders’ Equity Equipment 280,000 Common stock 126,200 Accum. depr. (156,900) Retained earnings 131,500 * Total […]

978-0078025549 Chapter 3 Solution Manual Part 1

Question 3-1 (LO 3-1) The revenue recognition principle states that we record revenue in the period in which we earn it. If a company sells products or provides services to a customer in the current year, then Question 3-2 (LO […]

978-0078025549 Chapter 3 Solution Manual Part 10

Additional Perspective 3-3 Requirement 1 Current assets equal $276,873 thousand. Current assets include cash and cash Requirement 2 Current liabilities equal $128,956 thousand. Current liabilities include accounts payable, accrued employee compensation, accrued store operating expenses, gift certificates redeemable, and income […]

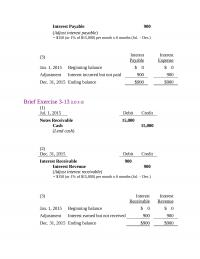

978-0078025549 Chapter 3 Solution Manual Part 2

Interest Payable 900 (Adjust interest payable) = $150 (or 1% of $15,000) per month x 6 months (Jul. – Dec.) (3) Interest Payable Interest Expense Jan. 1, 2015 Beginning balance $ 0 $ 0 Brief Exercise 3-13 (LO 3-3) (1) […]

978-0078025549 Chapter 3 Solution Manual Part 3

(e) Debit Credit Supplies Expense 3,900 Exercise 3-13 (LO 3-3) (a) Debit Credit Interest Receivable 270 Interest Revenue 270 (Adjust interest receivable) (b) Debit Credit Rent Expense 3,000 Prepaid Rent 3,000 (Adjust prepaid rent) (c) Debit Credit Unearned Revenue 5,500 […]

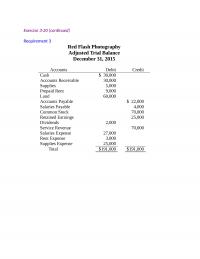

978-0078025549 Chapter 3 Solution Manual Part 4

Exercise 3-20 (connued) Requirement 3 Red Flash Photography Adjusted Trial Balance December 31, 2015 Accounts Debit Credit Cash $ 30,000 Accounts Receivable 30,000 Supplies 5,000 Prepaid Rent 9,000 Land 60,000 Accounts Payable $ 22,000 Salaries Payable 4,000 Common Stock 70,000 […]

978-0078025549 Chapter 3 Solution Manual Part 5

Problem 3-6A (LO 3-6, 3-7) Requirement 1 December 31 Debit Credit Service Revenue 77,500 Retained Earnings 62,100 Salaries Expense 46,000 Utilities Expense 8,200 Insurance Expense 5,800 Supplies Expense 2,100 (Close expense accounts) Retained Earnings 6,000 Dividends 6,000 (Close dividends account) […]

978-0078025549 Chapter 3 Solution Manual Part 6

Problem 3-8A (connued) Requirement 6 (adjusted entries posted in) Cash Accounts Receivable Supplies 20,000 39,000 26,000 13,000 8,000 21,000 18,000 4,000 Equipment Accumulated Depr. Salaries Payable 15,000 8,000 7,500 23,000 10,000 1,100 5,000 7,500 Common Stock Retained Earnings Service Revenue […]

978-0078025549 Chapter 3 Solution Manual Part 7

Problem 3-5B (LO 3-5) Orange Designs Income Statement For the year ended December 31, 2015 Service revenue $111,900 Expenses: Salaries 43,000 Rent 19,000 Depreciation 8,000 Problem 3-5B (concluded) Orange Designs Statement of Stockholders’ Equity For the year ended December 31, […]

978-0078025549 Chapter 3 Solution Manual Part 8

Problem 3-8B (connued) Requirement 2 (a) Debit Credit Accounts Receivable 65,000 Cash 20,000 (b) Debit Credit Cash 53,000 Accounts Receivable 53,000 (Collect on account) (c) Debit Credit Cash 11,000 Common Stock 11,000 (Issue common stock) (d) Debit Credit Salaries Expense […]

978-0078025549 Chapter 3 Solution Manual Part 9

Additional Perspective 3-1 (continued) Requirement 1 (concluded) Dec. 8, 2015 Miscellaneous Expense 1,200 Dec. 12, 2015 Supplies (Racing) 2,800 Accounts Payable 2,800 (Purchase racing supplies on account) Dec. 15, 2015 Cash 20,000 Service Revenue (Racing) 20,000 (Receive cash for adventure […]

978-0078025549 Chapter 3 Solution Problem C Part 1

Problem 3-1C Accrual-Basis Cash-Basis Transaction Revenue Expense Revenue Expense 1. Record employee salaries incurred 2. Pay advertising for the current month, $700. $0 $700 $0 $700 3. Pay utilities for the previous month, $750. $0 $0 $0 $750 4. Receive […]

978-0078025549 Chapter 3 Solution Problem C Part 2

Problem 3-7C (continued) David’s Services Balance Sheet December 31, 2015 Assets Liabilities Cash $18,100 Accounts payable $10,500 Accts. receivable 16,200 Salaries payable 4,200 Supplies 3,000 Utilities payable 1,900 Notes payable 40,000 Equipment 95,000 Accum. depr. (40,800) Stockholders’ Equity Common stock […]

978-0078025549 Chapter 3 Solution Problem C Part 3

Trial Balance Account Title Debit Credit Cash $ 34,500 Accounts Receivable 25,300 Supplies 3,700 Equipment 26,400 Debit Credit Depreciation Expense 2,900 Accumulated Depreciation 2,900 (Adjust accumulated depreciation) Supplies Expense 2,500 Supplies 2,500 (Adjust medical supplies) Unearned Revenue 4,000 Service Revenue […]

978-0078025549 Chapter 4 Lecture Note

LO4-3 Define cash and cash equivalents. LO4-4 Understand controls over cash receipts and cash disbursements. LO4-5 Reconcile a bank statement. LO4-6 Account for petty cash. LO4-7 Identify the major inflows and outflows of cash. Analysis […]

978-0078025549 Chapter 4 Solution Exercise B

Chapter 4 Cash and Internal Controls 1. True 2. False 3. True 4. True 5. False 6. False EXERCISES Exercise 4-1 1. False 2. True 3. True 4. False 5. True 6. True Exercise 4-2 1. True 2. False 3. […]

978-0078025549 Chapter 4 Solution Manual Part 1

Question 4-1 (LO 4-1) Occupational fraud is the use of one’s occupation for personal enrichment through the deliberate misuse or misapplication of the employing organization’s resources. Occupational Question 4-2 (LO 4-1) Internal control is a company’s plan to (1) safeguard […]

978-0078025549 Chapter 4 Solution Manual Part 2

Exercise 4-1 (LO 4-1) 1. False 2. True 3. True 4. False 5. True 6. True Exercise 4-2 (LO 4-1) 1. True 2. False 3. True 4. True 5. False 6. False Exercise 4-3 (LO 4-2) 1. True 2. False […]

978-0078025549 Chapter 4 Solution Manual Part 3

Requirement 2 Debit Credit Cash 6,450 Notes Receivable 6,000 Accounts Receivable 200 Advertising Expense 300 Rent Expense 1,100 Service Fee Expense 125 Cash 1,725 (Record NSF check, recording error, automatic payment, and bank service fee) Interest Revenue 450 (Record note […]

978-0078025549 Chapter 4 Solution Manual Part 4

June 2 Debit Credit Cash 19,000 June 3 Debit Credit Rent Expense 1,200 Cash 1,200 (Pay current month rent) June 7 Debit Credit Cash 5,200 Accounts Receivable 3,500 Service Revenue 8,700 (Provide services for cash and on account) June 11 […]

978-0078025549 Chapter 4 Solution Problem C

Weber Productions Bank Reconciliation February 28 Bank’s Cash Balance Company’s Cash Balance Per bank statement $ 4,576 Per general ledger $21,861 Deposits outstanding + 7,348 NSF check − 6,783 Checks outstanding − 541 Service fees − 195 PROBLEMS: SET C […]

978-0078025549 Chapter 5 Lecture Note Part 1

Chapter 5 Receivables and Sales INSTRUCTOR’S MANUAL Learning Objectives LO5-1 Recognize accounts receivable. LO5-2 Calculate net revenues using discounts, returns, and allowances. LO5-3 Record an allowance for future uncollectible accounts. LO5-4 Use the aging method to […]

978-0078025549 Chapter 5 Lecture Note Part 2

Problem #1 Mercy Care normally charges $200 for an annual physical exam. Currently, the company is offering a $50 discount to expectant mothers. In addition, Mercy offers terms 2/10, n/30 to all customers receiving services on account. The following events […]

978-0078025549 Chapter 5 Solution Exercise B Part 1

Chapter 5 Receivables and Sales May 7 Debit Credit Accounts Receivable 4,760 May 13 Cash 4,760 Accounts Receivable 4,760 (Collect cash on account) EXERCISES Exercise 5-1 Service Revenue 4,760 (Provide services on account) May 1 Debit Credit Cash 300 Exercise […]

978-0078025549 Chapter 5 Solution Exercise B Part 2

Exercise 5-11 Requirement 1 Age Group Amount Receivable Estimated Percent Uncollectible Estimated Amount Uncollectible Not yet due $ 69,500 10% $ 6,950 0-60 days past due 56,700 20% 11,340 61-120 days past due 32,400 45% 14,580 Requirement 2 December 31, […]

978-0078025549 Chapter 5 Solution Manual Part 1

Question 5-1 (LO 5-1) When recording a credit sale, we debit accounts receivable. Accounts receivable are reported Question 5-2 (LO 5-1) Trade receivables are amounts receivable from customers due to credit sales. Nontrade receivables are receivables from those other than […]

978-0078025549 Chapter 5 Solution Manual Part 2

Exercise 5-4 (LO 5-1, 5-2) March 12 Debit Credit Accounts Receivable 11,000 March 31 Cash 11,000 Accounts Receivable 11,000 (Receive cash on account) Exercise 5-5 (LO 5-1, 5-2) March 12 Debit Credit Service Fee Expense 11,000 Accounts Payable 11,000 (Receive […]

978-0078025549 Chapter 5 Solution Manual Part 3

Exercise 5-17 (LO 5-7) Requirement 1 April 1, 2015 Debit Credit Notes Receivable 600,000 Requirement 2 December 31, 2015 Debit Credit Interest Receivable 49,500 Interest Revenue 49,500 (Adjust interest receivable) (Interest revenue = $600,000 x 11% x 9/12) Requirement 3 […]

978-0078025549 Chapter 5 Solution Manual Part 4

Problem 5-6A (LO 5-3) Requirement 1 Debit Credit Bad Debt Expense 59,000 Requirement 2 Revised operating income = $260,000 − $59,000 (bad debt expense) = $201,000 Willie will not get his bonus because the revised operating income of $201,000 is […]

978-0078025549 Chapter 5 Solution Manual Part 5

Problem 5-4B (LO 5-4, 5-5) Requirement 1 Age group Amount receivable Estimated percent uncollectible Estimated amount uncollectible Not yet due $40,000 3% $1,200 0-30 days past due 11,000 4% 440 Requirement 2 December 31, 2015 Debit Credit Bad Debt Expense […]

978-0078025549 Chapter 5 Solution Manual Part 6

Jan. 24, 2016 Debit Credit Equipment 5,000 Feb. 25, 2016 Accounts Receivable 3,000 Service Revenue 3,000 (Provide TEAM event) Feb. 28, 2016 Cash 2,850 Sales Discounts 150 Accounts Receivable 3,000 (Receive cash on account less 5% discount) Mar. 19, 2016 […]

978-0078025549 Chapter 5 Solution Problem C

Revenue recognized in 2015 Scenario 1: $100,000 Scenario 2: $60 (= $75 x 80%) Scenario 3: $15,000 Scenario 4: $125,000 June 10 Debit Credit No entry June 12 No entry June 13 No entry June 16 Accounts Receivable 1,440 June […]

978-0078025549 Chapter 6 Lecture Note Part 1

Chapter 6 Inventory and Cost of Goods Sold INSTRUCTOR’S MANUAL Learning Objectives LO6-1 Trace the flow of inventory costs from manufacturing companies to merchandising companies. LO6-2 Understand how cost of goods sold is reported in a multiple-step income […]

978-0078025549 Chapter 6 Lecture Note Part 2

1. Calculate cost of goods sold and ending inventory using the LIFO method. Cost of goods available for sale = Cost of goods sold +Ending inventory Beginning inventory and purchases Number of units xUnit cost =Total Cost Jan. 1{50 $20 […]

978-0078025549 Chapter 6 Solution Exercise B Part 1

Exercise 6-1 Beginning inventory $ 63,800 Add: Purchases 925,500 Cost of goods available for sale 989,300 Less: Ending inventory (41,500) Chapter 6 Inventory and Cost of Goods SoldEXERCISES Cost of goods sold $947,800 Exercise 6-2 Wayman Corporation Multiple-step Income Statement […]

978-0078025549 Chapter 6 Solution Exercise B Part 2

Exercise 6-6 Debit Credit Inventory 320,000 Debit Credit Accounts Receivable 450,000 Sales Revenue 450,000 (Sell inventory on account) Cost of Goods Sold 340,000 Inventory 340,000 (Cost of inventory sold) Accounts Payable 320,000 (Purchase inventory on account) Exercise 6-7 June 5 […]

978-0078025549 Chapter 6 Solution Exercise B Part 3

Inventory Quantity Lower of Cost or Market Ending Inventory Shirts 52 $ 75 $ 3,900 MegaDriver 12 180 2,160 MegaDriver II 40 320 12,800 Debit Credit Cost of Goods Sold 840 Inventory 840 (Adjust inventory down to market) ($840 = […]

978-0078025549 Chapter 6 Solution Manual Part 1

Question 6-1 (LO 6-1) Inventory includes items a company intends for sale to customers. Inventory also includes items that are not yet finished products. The cost of inventory that has not been sold by the end of the Question 6-2 […]

978-0078025549 Chapter 6 Solution Manual Part 2

Brief Exercise 6-14 (LO 6-6) Inventory Quantity Lower-of-Cost -or-Market Ending Inventory Ski jackets 20 $ 95 $1,900 Skis 25 300 7,500 Brief Exercise 6-15 (LO 6-6) Inventory Quantity Lower-of-Cost -or-Market Ending Inventory Optima cameras 110 $45 $4,950 Inspire speakers 50 […]

978-0078025549 Chapter 6 Solution Manual Part 3

Exercise 6-4 (concluded) Requirement 3 Weighted average Date Transaction Number of units Unit cost Total cost Jan. 1 Beginning Inventory 50 $42 $ 2,100 Apr. 7 Purchase 130 44 5,720 Jul. 16 Purchase 200 47 9,400 Oct. 6 Purchase 110 […]

978-0078025549 Chapter 6 Solution Manual Part 4

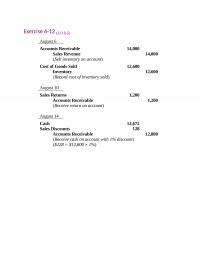

Exercise 6-12 (LO 6-5) August 6 Accounts Receivable 14,000 Cost of Goods Sold 12,600 Inventory 12,600 (Record cost of inventory sold) August 10 Sales Returns 1,200 Accounts Receivable 1,200 (Receive return on account) August 14 Cash 12,672 Sales Discounts 128 […]

978-0078025549 Chapter 6 Solution Manual Part 5

Problem 6-1A (concluded) Requirement 3 LIFO Date Transaction Number of units Unit Cost Ending Inventory Oct. 1 Beginning inventory 6 $900 $5,400 Date Transaction Number of units Unit Cost Cost of Goods Sold Oct. 10 Purchase 3 $910 $ 2,730 […]

978-0078025549 Chapter 6 Solution Manual Part 6

Problem 6-6A (continued) Requirement 1 (continued) October 20 Debit Credit Inventory 7,000 October 22 Cash 8,000 Sales Revenue 8,000 (Sell inventory for cash) Cost of Goods Sold 6,840 Inventory 6,840 (Record cost of inventory sold) ($6,840 = ($54 × 10 […]

978-0078025549 Chapter 6 Solution Manual Part 7

Problem 6-1B (concluded) Requirement 3 LIFO Date Transaction Number of units Unit cost Ending Inventory Date Transaction Number of units Unit cost Cost of Goods Sold Jun. 1 Beginning inventory 2 $350 $ 700 Jun. 12 Purchase 10 340 3,400 […]

978-0078025549 Chapter 6 Solution Manual Part 8

Problem 6-6B (continued) Requirement 1 (continued) November 21 Debit Credit Inventory 7,280 November 24 Cash 12,600 Sales Revenue 12,600 (Sell inventory for cash) Cost of Goods Sold 9,212 Inventory 9,212 (Record cost of inventory sold) [$9,160 = ($100 × 37 […]

978-0078025549 Chapter 6 Solution Manual Part 9

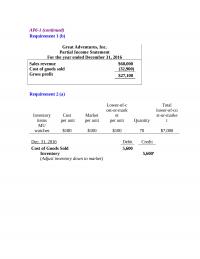

Great Adventures, Inc. Partial Income Statement For the year ended December 31, 2016 Sales revenue $60,000 Cost of goods sold (32,900) Gross profit $27,100 Inventory items Cost per unit Market per unit Lower-of-c ost-or-mark et per unit Quantity Total lower-of-co […]

978-0078025549 Chapter 6 Solution Problem C Part 1

Problem 6-1C Requirement 1 Date Transaction Number of units Unit cost Ending Inventory Jun. 1 Beginning Inventory 1 $ 240 $ 240 Jun. 12 Purchase 5 230 1,150 Jun. 24 Purchase 0 220 0 Jun. 29 Purchase 8 210 1,680 […]

978-0078025549 Chapter 6 Solution Problem C Part 2

November 2 Debit Credit Inventory 8,000 November 3 Inventory 210 Cash 210 (Pay freight-in) November 9 Accounts Payable 1,000 Inventory 1,000 (Return inventory on account) November 11 Accounts Payable 7,000 Inventory 140 Cash 6,860 (Pay on account less 2% discount) […]

978-0078025549 Chapter 7 Lecture Note

Chapter 7 Long-Term Assets INSTRUCTOR’S MANUAL Learning Objectives LO7-1 Identify the major types of property, plant, and equipment. LO7-2 Identify the major types of intangible assets. LO7-3 Describe the accounting treatment of expenditures after acquisition. LO7-4 […]

978-0078025549 Chapter 7 Solution Exercise B

Chapter 7 Long-Term Assets Purchase price of land (and building to be removed) $400,000 Title insurance 3,000 Back property taxes 4,000 Cost of removing the building 25,000 Less: Salvaged materials (2,000) Level the land 6,000 EXERCISES Exercise 7-1 Total cost […]

978-0078025549 Chapter 7 Solution Manual Part 1

Question 7-1 (LO 7-1) WorldCom recorded assets on the balance sheet that should have been recorded as expenses on the income statement. When WorldCom uses the telecommunication lines of another Question 7-2 (LO 7-1) The two major categories for long-term […]

978-0078025549 Chapter 7 Solution Manual Part 2

Exercise 7-4 (LO 7-1, 7-4) 1. Land is not depreciated. However, depreciation on the building is tax-deductible. If management allocates less of the purchase price to land 2. If the true allocation should have been 20% to land and 80% […]

978-0078025549 Chapter 7 Solution Manual Part 3

Requirement 2 Double-declining-balance University Car Wash Calculation End of Year Amounts Year Beginning Book Value XDepreciation Rate* =Depreciation Expense Accumulated Depreciation Book Value** 1 270,000 1/3 90,000 90,000 180,000 2 180,000 1/3 60,000 150,000 120,000 3 120,000 1/3 40,000 190,000 […]

978-0078025549 Chapter 7 Solution Manual Part 4

Requirement 2 Debit Credit Amortization Expense 25,000 * Requirement 3 Togo’s Sandwich Shop December 31, 2015 Cost Accumulated Depreciation Book Value Land $ 85,000 – $ 85,000 Building 560,000 ($273,280) 286,720 Equipment 145,000 (45,000) 100,000 Patent 125,000 (75,000) 50,000 $127,500 […]

978-0078025549 Chapter 7 Solution Problem C

Land Building Purchase price of land $140,00 0 Land clearing costs 5,000 Architect fees (for new building) $ 30,000 Requirement 1 The ovens should be recorded in the equipment account at $99,000 as detailed in the following schedule: Purchase price […]

978-0078025549 Chapter 8 Lecture Note Part 1

Chapter 8 Current Liabilities INSTRUCTOR’S MANUAL Learning Objectives LO8-1 Distinguish between current and long-term liabilities. LO8-2 Account for notes payable and interest expense. LO8-3 Account for employee and employer payroll liabilities. LO8-4 Explain the accounting for […]

978-0078025549 Chapter 8 Lecture Note Part 2

Alternate Let’s Review Problem #1 Assume Blue Sky Airlines borrows $1,000,000 from Midtown Bank on November 1, 2015 signing an 8%, six-month note payable. Required: 1. Record the issuance of the note. 2. Record the appropriate adjusting entry for the […]

978-0078025549 Chapter 8 Solution Exercise B

Reporting Method C. Current liability L. Long-term liability D. Disclosure note only N. Not reported Item __C__ 1. Accounts payable. __C__ 2. Customer advances. __C__ 3. Commercial paper. __D__ 4. Unused line of credit. __C__ 5. A loss contingency that […]

978-0078025549 Chapter 8 Solution Manual Part 1

Question 8-1 Liabilities have three essential characteristics. Liabilities are: (1) probable future sacrifices of economic benefits; (2) arising from present obligations to other entities; (3) resulting from past Question 8-2 In most cases, current liabilities are payable within one year […]

978-0078025549 Chapter 8 Solution Manual Part 2

Exercise 8-7 Requirement 1 Total Salary Expense (100 x 40 hours x $20) $80,000 Less: Withholdings Federal Income Taxes (80,000 x .15) 12,000 State Income Taxes (80,000 x .05) 4,000 FICA Taxes (80,000 x .0765) 6,120 Requirement 2 FICA Taxes […]

978-0078025549 Chapter 8 Solution Manual Part 3

Problem 8-6A Requirement 1 Cash 3,500 Requirement 2 Unearned Revenue 728 Sales Revenue ($728 / 1.04) 700 Sales Taxes Payable 28 (Redemption of gift certificates) Requirement 3 Unearned Revenue 728 3,500 2,772 Balance Problem 8-7A Requirement 1 The likelihood of […]

978-0078025549 Chapter 8 Solution Manual Part 4

Requirement 2 ($ in millions) Quick Assets ÷ Total Current Liabilities = Acid-Test Ratio Southwest $3,548 ÷ $4,650 = 0.76 United Airlines (0.86) also has the best acid-test ratio followed by Southwest (0.76). Requirement 3 The purchase of additional inventory […]

978-0078025549 Chapter 8 Solution Problem C

List A List B __g___ 1. Long-term debt maturing within a. FICA __j___ 2. Borrowing from another company with maturities up to 270 days. b. Acid-test ratio __f___ 3. Classifying liabilities as either current or long-term helps investors and creditors […]

978-0078025549 Chapter 9 Lecture Note Part 1

Chapter 9 Long-Term Liabilities INSTRUCTOR’S MANUAL Learning Objectives LO9-1 Explain financing alternatives. LO9-2 Identify the characteristics of bonds. LO9-3 Determine the price of a bond issue. LO9-4 Account for the issuance of bonds. LO9-5 Record […]

978-0078025549 Chapter 9 Lecture Note Part 2

2. If the market rate is 9%, the bonds will issue at a discount. The only change we make is that now I = 4.5% rather than 4%. Calculator Input Bond characteristics Key Amount 1. Face amount FV $500,000 2. […]

978-0078025549 Chapter 9 Solution Exercise B Part 1

Exercise 9-1 Requirement 1 Issue Bonds Issue Stock Operating income $12,000,000 $12,000,000 Interest expense (bonds only) 4,000,000 Income before tax 8,000,000 12,000,000 Requirement 2 Issuing bonds results in earnings per share of $2.60 compared with earnings per share of $1.95 […]

978-0078025549 Chapter 9 Solution Exercise B Part 2

Requirement 2 January 1, 2015 Cash 214,877 June 30, 2015 Interest Expense 6,446 Bonds Payable (difference) 554 Cash ($200,000 x 7% x ½) 7,000 (First semi-annual interest payment) December 31, 2015 Interest Expense 6,430 Bonds Payable (difference) 570 Cash ($200,000 […]

978-0078025549 Chapter 9 Solution Manual Part 1

Question 9-1 (LO 9-1) Capital structure is the mixture of liabilities and stockholders’ equity a business uses. Companies in the auto industry, like Ford, typically lean more toward liabilities for their financing, while companies in Question 9-2 (LO 9-1) One […]

978-0078025549 Chapter 9 Solution Manual Part 2

Exercise 9-1 (LO 9-1) Requirement 1 Issue Bonds Issue Stock Operating income $11,000,000 $11,000,000 Interest expense (bonds only) 2,450,000 Income before tax 8,550,000 11,000,000 Income tax expense (35%) 2,992,500 3,850,000 Net income $ 5,557,500 $ 7,150,000 Requirement 2 Issuing stock […]

978-0078025549 Chapter 9 Solution Manual Part 3

Requirement 2 January 1, 2015 Cash 644,161 December 31, 2015 Interest Expense 38,650 Bonds Payable (difference) 3,350 Cash ($600,000 x 7%) 42,000 (Pay annual interest) December 31, 2016 Interest Expense 38,449 Bonds Payable (difference) 3,551 Cash ($600,000 x 7%) 42,000 […]

978-0078025549 Chapter 9 Solution Manual Part 4

Problem 9-5A (LO 9-6) Requirement 1 January 1, 2015 Building 360,000 Cash 60,000 Requirement 2 (1) Date (2) Cash Paid (3) Interest Expense (4) Decrease in Carrying Value (5) Carrying Value Monthly Payment Carrying Value x 0.07 x 1/12 (2) […]

978-0078025549 Chapter 9 Solution Manual Part 5

Requirement 3 January 31, 2015 Interest Expense ($500,000 x 9% x 1/12) 3,750.00 Notes Payable (difference) 1,321.33 Requirement 4 Requirement 1 Assets = Liabilities + Stockholders’ Equity $201 million $91 + $61 = $152 million ? Total Liabilities ÷ Stockholders’ […]

978-0078025549 Chapter 9 Solution Problem C

Requirement 1 Face amount. The issue price is $600,000. Calculator Input Bond Characteristics Key Amount 1. Face amount FV $600,000 2. Interest payment PMT $18,000 = $600,000 x 6% x ½ year Calculator Output Issue price PV $600,000 (1) Date […]

AC 121 Quiz 1

1) We record gain contingencies when the gain is probable and can be reasonably estimated. 2) An S Corporation allows a company to enjoy limited liability as a corporation, but tax treatment as a partnership. Answer: True 3) FICA taxes […]

AC 209

1) The more frequent the rate of compounding, the more interest that is earned on previous interest, resulting in a higher future value. 2) Intangible assets with an indefinite useful life (goodwill and most trademarks) are not amortized. Answer: True […]

AC 627 Quiz

1) A $10,000 investment on the books of the company is sold for $11,000. How does this transaction affect operating, investing, and financing activities under the indirect method? 2) Match each account classification with its example. Answer: 1-b; 2-d; 3-f; […]

AC 707 Quiz 1

1) A sale on account for $1,000 offered with terms 2/10, n/30 means that the customers will get a $2 discount if payment is made within 10 days; otherwise, full payment is due within 30 days. 2) Under the allowance […]

AC 763 Test 1

1) We record dividends received as a financing activity. 2) Investing activities include cash investments in long-term assets and investment securities. Answer: True 3) We report interest paid on bonds or notes payable with operating activities rather than financing activities. […]

ACC 197 Test 1

1) In a classified balance sheet, we categorize all liabilities as current. 2) When bonds are issued at a premium (above face amount), the carrying value and the corresponding interest expense increase over time. Answer: False Feedback: When bonds are […]

ACC 289

1) In general, if a companys net income is increasing, so will its stock price. 2) Adjusting entries should be prepared after financial statements are prepared. Answer: False Feedback: Adjusting entries should be prepared before financial statements are prepared. 3) […]

ACC 313 Final

1) The CEO, as head of the company, is ultimately responsible for the firms accounting. 2) Treasury stock is a contra-equity account since treasury stock increases total stockholders equity. Answer: False Feedback: Treasury stock is a contra-equity account since treasury […]

ACC 486 Test

1) Financial statements are periodic reports published by the company for the purpose of providing information to managers. 2) Allowing the employee who authorizes purchases to also prepare the check is an example of good internal control. Answer: False Feedback: […]

ACC 490 1 An extremely high

1) An extremely high inventory turnover ratio may be a signal that the company is losing sales due to inventory shortages. 2) When preparing a statement of cash flows using the indirect method, a decrease in accounts payable is subtracted […]

ACC 547 Midterm 2

1) Unearned Revenue is a liability account. 2) A patent is an exclusive right to a published work such as a song, film, or painting. Answer: False Feedback: A patent is an exclusive right to manufacture a product or to […]

Acc 553

1) The Public Company Accounting Oversight Board (PCAOB) has the authority to establish standards dealing with auditing, quality control, ethics, independence, and other activities relating to the preparation of audited financial reports. 2) The gross profit ratio is calculated as […]

ACC 572 Midterm 2

1) Companies should set maximum purchase limits on debit cards and credit cards as part of internal controls. 2) Generally, a lower gross profit ratio reflects positively on a companys ability to manage its inventory. Answer: False Feedback: A higher […]

Acc 603 Quiz 3 1 Even though the

1) Even though the percentage-of-receivables method and the percentage-of-credit-sales method use different accounts to estimate future uncollectible accounts, the amount of bad debt expense reported in the income statement will always be the same under the two methods. 2) The […]

Acc 672 Quiz

1) The adjusting entry for a prepaid expense has the effect of reducing total assets and reducing net income. 2) Operating activities are both inflows and outflows of cash resulting from the external financing of a business. Answer: False Feedback: […]

Acc 676 Test 1

1) Under the indirect method, an increase in inventory is added to net income and a decrease in inventory is subtracted from net income to arrive at net cash flows from operating activities. 2) A copyright is an exclusive right […]

ACC 703 Quiz 1

1) Cost of goods sold is an asset reported in the balance sheet and inventory is an expense reported in the income statement. 2) In an activity-based depreciation method, we allocate an assets cost based on its use. Answer: True […]

Acc 806 Quiz 1

1) Define a contingent liability. Provide three common examples. Under what circumstances should a firm report a contingent liability? 2) A company received a utility bill of $600 but did not pay it. Indicate the amount of increases and decreases […]

ACC 836

1) The following data are taken from the cash-basis accounting records of Myerson Company for the year ended December 31, 2015: Calculate the amount of revenues and expenses for 2015 under cash-basis accounting. 2) A company maintains its records using […]

Accounting 329 Midterm 2

1) Retained earnings represent the earnings retained in the corporation earnings not paid out as dividends to stockholders. 2) A low inventory turnover ratio usually is a positive sign and indicates that inventory is selling quickly. Answer: False Feedback: A […]

Accounting 682 Quiz

1) During periods of rising costs, FIFO generally results in a higher cost of goods sold. 2) We expense internally generated intangible assets, such as research and development and advertising costs, as we incur them. Answer: True 3) Bonds issued […]

ACCT 120

1) Using a perpetual inventory system, the purchase of inventory is recorded with a debit to the Purchases account, which is a temporary account closed to cost of goods sold at the end of the period. 2) The debt to […]

ACCT 144 Final

1) The amount reported on the balance sheet for bonds payable is equal to the carrying value at the balance sheet date. 2) Convertible preferred stock allows the stockholder to exchange shares of preferred stock for common stock at a […]

ACCT 169

1) The Financial Accounting Standards Boards conceptual framework does not prescribe Generally Accepted Accounting Principles. It provides an underlying foundation for the development of accounting standards and interpretation of accounting information. 2) Bonds are the most common form of corporate […]

ACCT 178 Homework

1) We can calculate the issue price of a bond as the face amount plus the total periodic interest payments. 2) Financial accounting has an impact on everyday business decisions as well as wide-ranging economic consequences. Answer: True 3) Bond […]

ACCT 198 Quiz 1

1) A list of all account names used to record transactions of a company is referred to as a T-account. 2) Asset turnover is net sales divided by ending total assets. Answer: False Feedback: Asset turnover is net sales divided […]

Acct 225 Test 1

1) Accumulated Depreciation is a liability account that is increased by credits. 2) When customers pay for services with a debit card, the company should debit Cash and credit Service Revenue. Answer: True 3) Revenues have the effect of increasing […]

ACCT 312 Homework

1) We report extraordinary items separately, net of taxes, near the bottom of the income statement just below discontinued operations. 2) Financing activities include cash receipts and cash payments for transactions relating to revenue and expense activities. Answer: False Feedback: […]

Acct 344 Quiz 3

1) The Shoe Exchange issues 5,000 shares of its $1 par value common stock to provide funds for further expansion. If the issue price is $15 per share, what is the entry to record the issuance of the stock? 2) […]

Acct 392 Midterm 2

1) Given a choice, most companies would prefer to report a liability as current rather than long-term, because doing so may cause the firm to appear less risky. 2) The location where a loss is reported in the income statement […]

Acct 420

1) Notes receivable typically arise from sales to customers. 2) Airlines do not record revenue when a ticket is sold, but wait to record revenue until the actual flight occurs. Answer: True 3) The Sarbanes-Oxley Act is also known as […]

Acct 523 Midterm 2

1) A stock split has no effect on the total of any account in stockholders equity. 2) The closing entry for dividends includes a debit to the Dividends account and a credit to Retained Earnings. Answer: False Feedback: The closing […]

ACCT 626 Quiz 1

1) Prepaid expenses involve payment of cash (or an obligation to pay cash) for the purchase of an asset before the expense is incurred. 2) A credit balance in the Allowance for Uncollectible Accounts before adjustment indicates that last years […]

ACCT 686

1) The components of retained earnings include assets, expenses, and dividends. 2) Conservative accounting practices are those that result in reporting lower income, lower assets, and higher liabilities. Answer: True 3) Book value is equal to the original cost of […]

Acct 782 Test 1

1) The receivables turnover ratio measures how many times, on average, a company collects its receivables during the year. 2) The Supplies account is an example of an accrued expense. Answer: False Feedback: The Supplies account is an example of […]

ACCT 836 Test 2

1) An annuity is a series of equal cash payments over equal time intervals. 2) The Dividends account increases with a credit and decreases with a debit. Answer: False Feedback: The Dividends account increases with a debit and decreases with […]

Acct 860 1 Residual value also

1) Residual value, also referred to as salvage value, is the amount the company expects to receive from selling the asset at the end of its service life. 2) Some countries are more secretive (Brazil and Switzerland), leading to fewer […]

ACT 565 Quiz 2

1) Depreciation expense is not reported on the statement of cash flows under the direct method. 2) When accounts payable decrease, cash paid to suppliers must have been more than purchases. Answer: True 3) Only transactions involving cash affect a […]

ACT 892 Quiz 1

1) A corporation has limited liability and attracting outside investment is easier relative to sole-proprietorships and partnerships. 2) The inventory turnover ratio equals cost of goods sold divided by average inventory. Answer: True 3) Commonly, current liabilities are payable within […]

MET MG 225 Midterm 1 1 Consider

1) Consider the following transactions: 1> Pay employees salaries. 2> Repay borrowing to the bank. 3> Purchase equipment with note payable. 4> Provide services to customers on account. 5> Pay dividends to stockholders. 6> Collect cash from customers for services […]

MET MG 258 Quiz 2

1) Companies are free to choose FIFO, LIFO, or weighted-average cost to report inventory and cost of goods sold. 2) Purchasing equipment using cash causes assets to increase. Answer: False Feedback: One asset goes up; another asset goes down. There […]

MET MG 278 Quiz 3

1) Dobson Contractors is considering buying equipment at a cost of $75,000. The equipment is expected to generate cash flows of $15,000 per year for eight years and can be sold at the end of eight years for $5,000. The […]

MET MG 293

1) Gains/losses on the early extinguishment of debt are reported as part of operating income in the income statement. 2) During periods of rising costs, LIFO generally results in a higher ending inventory balance. Answer: False Feedback: During periods of […]

MET MG 480 Midterm 2

1) Match each qualitative characteristic with its definition. 2) Mobile Video Systems sold land, investments, and issued their own common stock for $10 million, $15 million, and $20 million, respectively. Mobile Video also purchased treasury stock, equipment, and a patent […]

MET MG 699

1) Interest is stated in terms of an annual percentage rate to be applied to the face value of the loan. 2) Interest revenue is calculated as the carrying value of the investment in bonds times the stated interest rate. […]

Par value has a direct relationship to the market value of the common stock.

1) Par value has a direct relationship to the market value of the common stock. 2) A company that has average inventory of $500 and cost of goods sold of $2,000 would have an inventory turnover ratio of 0.25. Answer: […]

SMG AC 544 Quiz 1

1) Separation of duties refers to auditors not being allowed to perform both audit and nonaudit services for the same client. 2) Accrued revenues involve the receipt of cash after the revenue has been earned and an asset has been […]

SMG AC 548 Midterm 1

1) A companys cash is reported in two financial statements income statement and statement of cash flows. 2) Sales returns and allowances occur when the buyer returns the goods or the seller reduces the customers balance owed. Answer: True 3) […]