Archives

Chapter 1 The Sec Coordinates With The Fas

CHAPTER 1: THE DEMAND FOR AND SUPPLY OF FINANCIAL ACCOUNTING INFORMATION 1. A problem arising from equal information is called information asymmetry. a. True b. False ANSWER: False POINTS: 1 DIFFICULTY: Easy LEARNING OBJECTIVES: ACCT.WHAL.16.1.1 – LO: 1.1 NATIONAL STANDARDS: […]

Chapter 1 Which statement measures and reports the financial results

Chapter 1: The Demand for and Supply of Financial Accounting Information 53. Notes to financial statements provide a. discussions that further explain items shown in the financial statements. b. comparative financial information with the previous year. c. management’s discussions about […]

Chapter 10 If an exchange lacks commercial substance and results in a gain

CHAPTER 10: PROPERTY, PLANT, AND EQUIPMENT: ACQUISITION AND SUBSEQUENT INVESTMENTS 1. One advantage of recording property, plant, and equipment at historical costs is that historical cost is equal to the fair value on the purchase date. a. True b. False […]

Chapter 10 Reba Company received $60,000 in cash

Chapter 10: Property, Plant, and Equipment: Acquisition and Subsequent Investments 50. When exchanging nonmonetary assets a. boot must be associated with the transaction in order to recognize a gain or loss. b. recognized gain or loss can occur depending on […]

Chapter 10 The appraised value of the computer is$15,000, and the appraised

Chapter 10: Property, Plant, and Equipment: Acquisition and Subsequent Investments 85. A farmer donated a large tract of land and a building to a community group for use as a recreation center. The agreement provided that the recreation center employ […]

Chapter 11 Assets sold on or before the 15th are

CHAPTER 11: DEPRECIATION, DEPLETION, IMPAIRMENT AND DISPOSAL 1. The service life of an asset can only be measured in units of activity or output. a. True b. False ANSWER: False POINTS: 1 DIFFICULTY: Easy LEARNING OBJECTIVES: ACCT.WHAL.16.11.1 – LO: 11.1 […]

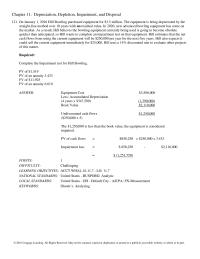

Chapter 11 No depreciation has been recorded in 2016

Chapter 11: Depreciation, Depletion, Impairment, and Disposal 121. On January 1, 2016 Hill Bowling purchased equipment for $3.5 million. The equipment is being depreciated by the straight-line method over 10 years with no residual value. In 2020, new advanced bowling […]

Chapter 11 Record The Journal Entry For The Disposal

Chapter 11: Depreciation, Depletion, Impairment, and Disposal Exhibit 11-05 Wilson is preparing his tax returns using the MACRS convention. The following information relates to the purchase of an asset on January 1, Year 1. MACRS Depreciation as a Percentage of […]

Chapter 11 The Change Should Accounted For With Adjustment

Chapter 11: Depreciation, Depletion, Impairment, and Disposal 55. Willis Limo Service purchased three used assets with the following characteristics: Residual Asset Cost Value Life Limo $12,000 $2,000 10 years Van 6,800 1,200 4 years Photocopier 1,500 250 5 years Assuming […]

Chapter 12 May not be scanned, copied or duplicated, or posted to a publicly

© 2016 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part. Chapter 12: Intangibles Costs $10,000 Book value of trade name, 12/31/15 $10,000 b. 2016 […]

Chapter 12 Purchased materials exclusively for use in R&D projects

Chapter 12: Intangibles 100. The determination of impairment losses differs under IFRS versus GAAP in that a. only GAAP permits a value–in-use estimate b. only IFRS employs a disposal approach as a measure of fair value c. only GAAP compares […]

Chapter 12 Riveria Should Report Which The Following Its

Chapter 12: Intangibles 55. For financial reporting purposes, GAAP requires organization costs to be a. expensed in the period in which they are incurred. b. capitalized and amortized over 20 years. c. capitalized and amortized over the first five years […]

Chapter 12 Technological feasibility of software products is established

CHAPTER 12: INTANGIBLES 1. Purchased intangible assets are generally expensed at their acquisition costs because the future economic benefits associate with them are difficult to measure. a. True b. False ANSWER: False POINTS: 1 DIFFICULTY: Easy LEARNING OBJECTIVES: ACCT.WHAL.16.12.1 – […]

Chapter 13 December 31 How Would Sun Record The

CHAPTER 13: INVESTMENTS AND LONG TERM RECEIVABLES 1. Significant influence of another company generally occurs when the investor owns between 25% and 45%. Due to this relationship the investor is required to issue consolidated financial statements. a. True b. False […]

Chapter 13 Declared and paid a cash dividend, $175,000

Chapter 13 – Investments and Long–Term Receivables 118. Fish Galore Corp. bought 25% of Fin Chaser Corporation’s stock for $70,000 on January 1, 2017. During 2017, Fin Chaser earned $25,000 of net income , and Fin Chaser distributed $15,000 of […]

Chapter 13 June 30 2017 The Company Still Has

Chapter 13 – Investments and Long–Term Receivables 100. On January 1, 2017, Lightner bought 20,000 shares (5% ownership) of Winter Corp. common stock for $360,000. On May 3, 2017, Winter declared and distributed a 50% stock dividend. On September 1, […]

Chapter 13 Smith Company The wise Company Should Account For

Chapter 13 – Investments and Long–Term Receivables 55. Wright Company has available-for-sale debt and equity securities that on December 31, 2017, had a cost of $110,000 and a market value of $108,000. The market value rose to $123,000 by December […]

Chapter 14 bonds that the company has the right to retire before

Chapter 14: Financing Liabilities: Bonds and Notes Payable 154. Which of the following is true for accounting for a troubled debt restructuring by a modification of terms by the debtor? a. If undiscounted cash flows after restructuring are greater than […]

Chapter 14 Discount Bonds Pay abled Sum The Cash Payment

Chapter 14: Financing Liabilities: Bonds and Notes Payable 60. Refer to Exhibit 14-1. At date of issuance cash received would be a. $280,747. b. $287,765. c. $292,998. d. $299,998. ANSWER: a POINTS: 1 DIFFICULTY: Moderate LEARNING OBJECTIVES: ACCT.WHAL.16.14.3 – LO: […]

Chapter 14 Financing Liabilities Bonds And Notes Payable183 What

Chapter 14: Financing Liabilities: Bonds and Notes Payable 171. On January 1, 2016, Darth Corp. issued 50,000 of five-year, $1,000 bonds payable at 104. These bonds were each convertible into 100 shares of $10 par common stock. On January 1, […]

Chapter 14 The entry to record the retirement in May

Chapter 14: Financing Liabilities: Bonds and Notes Payable 108. On July 1, 2016, Rio Corporation issued bonds with a face value of $100,000 and 12% interest payable semiannually. The bonds mature on June 30, 2021. The market rate of interest […]

Chapter 14 The effective rate is less than the contract rate when

CHAPTER 14: FINANCING LIABILITIES: BONDS AND NOTES PAYABLE 1. A company looking to issue debt instead of equity may want to consider debt due to favorable tax benefits. a. True b. False ANSWER: True POINTS: 1 DIFFICULTY: Easy LEARNING OBJECTIVES: […]

Chapter 15 Average Increase Sales greater Than 5 greater

Chapter 15: Contributed Capital 54. Assume common stock is issued to employees as a result of exercising stock purchase rights issued under a noncompensatory share purchase plan. Which of the following accurately describes the effect on the company‘s income, paid-in […]

Chapter 15 Listed Below Are Various Classifications Corporations

Chapter 15: Contributed Capital 100. If a company does not maintain its treasury stock records on a specific identification basis, which of the following approaches may be used to record a reduction in the treasury stock account when the stock […]

Chapter 15 May not be scanned, copied or duplicated, or posted to a

CHAPTER 15: CONTRIBUTED CAPITAL 1. Accumulated other comprehensive income is not reported with shareholder’s equity. a. True b. False ANSWER: False POINTS: 1 DIFFICULTY: Easy LEARNING OBJECTIVES: ACCT.WHAL.16.15.1 – LO: 15.1 NATIONAL STANDARDS: United States – BUSPROG: Reflective Thinking – […]

Chapter 15 May not be scanned, copied or duplicated, or posted to a publicly

Chapter 15: Contributed Capital © 2016 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part. 137. Below is the partial trial balance dated December 31, […]

Chapter 15 Record The January 15 2018 Convert The

Chapter 15: Contributed Capital 125. On January 1, 2016, Asquith Company adopts a performance-based stock option plan with a four-year vesting and service period, a $35 exercise price, and a $6 per option fair value. The plan grants a maximum […]

Chapter 16 Michael Declared 10 Stock Dividend Distributed February15

CHAPTER 16: RETAINED EARNINGS AND EARNINGS PER SHARE 1. When a property dividend is declared, fair value is determined on the ex-dividend date. a. True b. False ANSWER: False POINTS: 1 DIFFICULTY: Easy LEARNING OBJECTIVES: ACCT.WHAL.16.16.1 – LO: 16.1 NATIONAL […]

Chapter 16 Retained Earnings And Earnings Per

Chapter 16: Retained Earnings and Earnings Per Share 46. On January 1, a corporation had 15,380 shares of common stock outstanding. On August 1, it sold an additional 5,000 shares. During the year, dividends of $4,800 and $56,000 were declared […]

Chapter 16 Retained Earnings And Earnings Per Share 105 What

Chapter 16: Retained Earnings and Earnings Per Share 93. Daniel Company had 30,000 shares of common stock outstanding on January 1 and issued an additional 9,000 on August 1 of 2016. The company also has $100,000 of 8% convertible bonds […]

Chapter 16 The Company Subject 35 Tax Rate required prepare The

Chapter 16: Retained Earnings and Earnings Per Share 80. As of December 31, 2017, the Russell Corporation has 10,000 shares of 10% preferred stock issued and outstanding with a total par value of $250,000. In addition, as of this date, […]

Chapter 17 Advanced Issues Revenue Recognition 33 Company Must Account

CHAPTER 17: ADVANCED ISSUES IN REVENUE RECOGNITION 1. The core principle of revenue recognition is that a company should recognize revenue when it has been earned. a. True b. False ANSWER: False POINTS: 1 DIFFICULTY: Easy LEARNING OBJECTIVES: ACCT.WHAL.16.17.1 – […]

Chapter 17 Refer Exhibit 172 Assuming The Performance Obligation

Chapter 17: Advanced Issues in Revenue Recognition 53. On January 1, 2017, Oldham Company sold goods to Windall Company in exchange for a 3-year, non-interest-bearing note with a face value of $10,000. If Oldham entered into a separate financing transaction […]

Chapter 17 Thompson Construction began a construction project in 2016

Chapter 17: Advanced Issues in Revenue Recognition 86. On January 1, 2017, BT&T Company enters into a 2-year contract with a customer for an unlimited talk and 10 GB data wireless plan for $70 per month. The contract includes a […]

Chapter 18 Accounting For Income Taxes 31 The Amount Owed

CHAPTER 18: ACCOUNTING FOR INCOME TAXES 1. The amount of income tax expense as determined by GAAP differs from amount determined under the Internal Revenue Code due to measurement and timing. a. True b. False ANSWER: True POINTS: 1 DIFFICULTY: […]

Chapter 18 Accounting For Income Taxes 91 Rice Inc Began

Chapter 18: Accounting for Income Taxes 86. Fairfax Company had a balance in Deferred Tax Liability of $840 on December 31, 2016, resulting from depreciation timing differences. Differences in tax and accounting depreciation for assets purchased on January 1, 2016, […]

Chapter 18 For Each Item Listed Below Indicate

Chapter 18: Accounting for Income Taxes 48. On January 1, 2016, Bedrock Company began recognizing revenues from all sales under the accrual method for financial reporting purposes and under the installment sales method for income tax purposes. Bedrock reported the […]

Chapter 18 The Beginning 2016 Jasper Company Had

Chapter 18: Accounting for Income Taxes 96. At the beginning of 2016, Jasper Company had a deferred tax asset of $7,000 related to the warranty liability on its balance sheet. At the end of 2016, the company estimates that its […]

Chapter 19 Clemson Had Pension Plan Assets Totaling 990000

Chapter 19: Accounting for Postretirement Benefits 48. On January 1, 2015, a company had $84,000 of unrecognized prior service cost. The years-of-future-service method of amortization is used. The company has seven employees, as indicated below: Expected Years of Employee Future […]

Chapter 19 In 2016, the Electrician Company decided to amend

Chapter 19: Accounting for Postretirement Benefits 75. Joan, Inc. started a pension plan on January 1, 2016. At that date, prior service cost of $1,100,000 was recognized as a result of prior service credit granted to existing employees. At December […]

Chapter 19 In deciding how to recognize prior period cost

CHAPTER 19: ACCOUNTING FOR POSTRETIREMENT BENEFITS 1. Under contributory plans the employees bear the majority of the risks of the plan and contribute towards the plan with deductions from their salaries. a. True b. False ANSWER: True POINTS: 1 DIFFICULTY: […]

Chapter 2 Financial Reporting Its Conceptual Framework 31 Order Relevant

CHAPTER 2: FINANCIAL REPORTING: ITS CONCEPTUAL FRAMEWORK 1. Accounting principles are theories, truths, and propositions that service as the basis for financial accounting and reporting. a. True b. False ANSWER: True POINTS: 1 DIFFICULTY: Easy LEARNING OBJECTIVES: ACCT.WHAL.16.2.1 – LO: […]

Chapter 2 The ability of a company to use its financial resources to

Chapter 2: Financial Reporting: Its Conceptual Framework 60. Which of the following is a phase of the joint FASB and IASB conceptual framework project? a. going-concern assumption b. mixed attribute measurement c. elements and recognition d. period of time assumption […]

Chapter 20 May not be scanned, copied or duplicated, or posted to a publicly accessible

CHAPTER 20: ACCOUNTING FOR LEASES 1. The lessor is the party in the lease agreement who acquires the right to use the leased asset in exchange for making future lease payments. a. True b. False ANSWER: False POINTS: 1 DIFFICULTY: […]

Chapter 20 Merchant Company found themselves in need of cash

Chapter 20: Accounting for Leases * Rounded $1.50 d. 1/1/2016 Cost of Goods Sold 70,000 Inventory 70,000 Lease Receivable [($30,764 × 4) + $4,000] 127,056 Sales Revenue 110,000 Unearned Interest: Leases 17,056 Cash 30,764 Lease Receivable 30,764 12/31/2016 Unearned Interest: […]

Chapter 20 Shown Below List Key Terms Aj

Chapter 20: Accounting for Leases 99. Any initial direct costs incurred by the lessor for a sales-type lease should be a. expensed in the same period that the lease receivable is recognized. b. recorded as a prepaid asset and allocated […]

Chapter 20 Stacie Signed Lease Agreement With Amy

Chapter 20: Accounting for Leases 54. On January 1, 2016, Rhyme Co. leased equipment by signing a six-year lease that required six payments of $30,000 due on January 1 of each year with the first payment due January 1, 2016. […]

Chapter 20 The present Value The Minimum Lease Payments Equal

Chapter 20: Accounting for Leases 128. Addison Company signs a lease agreement dated January 1, 2016 for equipment from Luke Rental Company beginning January 1, 2016. The following information relates to the capital lease: 1) The lease term is 5 […]

Chapter 21 Cash dividends of $12,000 were declared and paid in

Chapter 21: The Statement of Cash Flows 51. The Red Blast Company uses the visual inspection method for completing the statement of cash flows. The following information relates to the Red Blast Company: Increase in accounts receivable $ 80 Increase […]

Chapter 21 Prepare the Net Cash Flow from Operating Activities section

Chapter 21: The Statement of Cash Flows 89. Your friend is in business and wants your advice on preparing and interpreting the statement of cash flows for 2016. Information regarding the business is as follows: Cash received from customers $ […]

Chapter 21 The following are several transactions and events that

Chapter 21: The Statement of Cash Flows 79. The following information relates to the Maxwell Company for 2016: Gain on sale of land $ 800 Bond payable premium amortization 300 Decrease in accounts payable 700 Increase in prepaid expenses 100 […]

Chapter 21 Under the spreadsheet method of preparing the cash flow statement

CHAPTER 21: THE STATEMENT OF CASH FLOWS 1. Receipts of dividends from investments in equity securities would be reported in the financing activities section of the cash flow statement. a. True b. False ANSWER: False POINTS: 1 DIFFICULTY: Easy LEARNING […]

Chapter 22 Fifo Inventory Costing Effective January 2018 The

Chapter 22: Accounting for Changes and Errors 99. When a company has a counterbalancing error, the company should a. not take any action if the financial statements are no longer being presented on a comparative basis. b. restate the financial […]

Chapter 22 Meagan Co Has The Following Errors

Chapter 22: Accounting for Changes and Errors POINTS: 1 DIFFICULTY: Challenging LEARNING OBJECTIVES: ACCT.WHAL.16.22.3 – LO: 22.3 ACCT.WHAL.16.22.5 – LO: 22.5 NATIONAL STANDARDS: United States – BUSPORG: Analytic LOCAL STANDARDS: United States – OH – Default City – AICPA: FN-Measurement […]

Chapter 22 Sometimes a change in estimate and a change in accounting

CHAPTER 22: ACCOUNTING FOR CHANGES AND ERRORS 1. An advantage of retrospective adjustment method is that it achieves comparability and consistency between accounting periods. a. True b. False ANSWER: True POINTS: 1 DIFFICULTY: Easy LEARNING OBJECTIVES: ACCT.WHAL.16.22.1 – LO: 22.1 […]

Chapter 22 What is the appropriateaction that Lilly should do now?

Chapter 22: Accounting for Changes and Errors Exhibit 22-2 On January 1, 2017, Nathan, Inc. purchased a machine for $56,000. Eight-year, straight-line depreciation with no salvage value was used through December 31, 2018. On January 1, 2019, it was estimated […]

Chapter 3 Do not prepare the heading

Chapter 3: Review of a Company’s Accounting System © 2016 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part. Income Taxes Payable 5,499 0.3 x […]

Chapter 3 If the trial balance does not balance

CHAPTER 3: REVIEW OF A COMPANY’S ACCOUNTING SYSTEM 1. The primary purpose of an accounting system is to record, organize. summarize, and report useful information to external financial statement users and stakeholders, as well as to company management, who make […]

Chapter 3 Neither The Wages The salaries Had Been Previously

Chapter 3: Review of a Company’s Accounting System 103. An organization will typically utilize a subsidiary ledger to a. make sure all debits equal credits. b. make it easier to handle cash received from customers. c. keep customer accounts up […]

Chapter 3 Review Companys Accounting System 81 Which The Following

Chapter 3: Review of a Company’s Accounting System 55. On June 1, 2015, Little Corporation received $5,320 in advance for a two-year rental of some land and properly credited Unearned Rent. In the adjusting entry at December 31, 2015, there […]

Chapter 3 Review Companys Accounting System Review

Chapter 3: Review of a Company’s Accounting System © 2016 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part. Chapter 3: Review of a Company’s […]

Chapter 4 Adjusted present value is based on the present-day fair

CHAPTER 4: THE BALANCE SHEET AND THE STATEMENT OF SHAREHOLDER’S EQUITY 1. The balance sheet reports the financial position of a company at a specific date in time whereas all other financial statements report changes in the financial position of […]

Chapter 4 Below List Common Ratios Necessary For

Chapter 4: The Balance Sheet and the Statement of Shareholders’ Equity 119. A list of statements follows: a. A balance sheet summarizes the ____________________ ____________________ of a company. b. ____________________ are the probable future economic benefits obtained or controlled by […]

Chapter 4 Listed Below Are Ten Terms Followed

Chapter 4: The Balance Sheet and the Statement of Shareholders’ Equity 61. Current liabilities includes all of the following except a. income tax payable. b. mortgage due to be paid this year. c. notes receivable. d. advance payments from customers. […]

Chapter 4 May not be scanned, copied or duplicated, or posted to

Chapter 4: The Balance Sheet and the Statement of Shareholders’ Equity 109. Gerald Company’s balance sheet information at the end of 2016 and 2017 is as follows: 2016 2017 Total shareholders’ equity $ (n) $ 145,600 Accumulated other comprehensive income […]

Chapter 5 Interperiod tax allocation involves apportioning a

CHAPTER 5: THE INCOME STATEMENT AND THE STATEMENT OF CASH FLOWS 1. Together with the cash flow statement, the income statement enables the investors to determine the rate of return the company is generating relative to the amount of capital […]

Chapter 5 Prepare a 2016 income statement for Rummer Company

Chapter 5: The Income Statement and the Statement of Cash Flows 105. The following income statement information for 2014 and 2015 was obtained from the accounting records of Upperco Company. 2014 2015 Sales $200,000 $150,000 Beginning inventory (a) ______ (e) […]

Chapter 5 The following are accounting items taken from

Chapter 5: The Income Statement and the Statement of Cash Flows 120. Below is a list of financial statement components with a corresponding letter code. a. Sales revenue (net) b. Cost of goods sold c. Selling expenses d. General and […]

Chapter 5 The Income Statement and the Statement of Cash Flows

Chapter 5: The Income Statement and the Statement of Cash Flows 55. When an entity reports on a sale of a component of the business a. any income or loss from operations of the component should be reported in the […]

Chapter 6 In general, GAAP requires receivables to be recorded

CHAPTER 6: CASH AND RECEIVABLES 1. A compensating balance used to secure a short term loan should be recorded against its short term borrowing in current assets separate from cash. a. True b. False ANSWER: True POINTS: 1 DIFFICULTY: Easy […]

Chapter 6 Joan Bell, Inc. uses the bank reconciliation form that arrives at a

Chapter 6: Cash and Receivables 104. On October 1, Robins’s Online Sales sold goods for $50,000 and accepted a six-month noninterest-bearing note. Current interest rates were 10%. The December 31 adjusting entry should be a. Interest Receivable 2,500 Interest Revenue […]

Chapter 6 June 30 required prepare The Receivables Portion Davidsons First

Chapter 6: Cash and Receivables 134. Prior to recording the recovery and collection of a $2,200 account receivable previously written off and the adjusting entry for bad debt expense for the year, the general ledger reflected the following information: Sales […]

Chapter 6 Objectives national Standards local Standards keywords they Are Negotiable Instruments Which

Chapter 6: Cash and Receivables 151. The following information for the month of March is available from Butters Cookies, Inc.’s accounting records: . Balance per bank statement, March 31, 2014 $12,100 . Cash balance per books, March 31, 2014 15,295 […]

Chapter 6 What The Amount Bad Debt Expense for The

Chapter 6: Cash and Receivables 58. Theoretically, the amount of estimated future returns and allowances on credit sales should be recorded during the period of the sale so as not to overstate sales and ending accounts receivable. In practice, these […]

Chapter 7 The costs of operating a purchasing department are necessary to the

CHAPTER 7: INVENTORIES: COST MEASUREMENT AND FLOW ASSUMPTIONS 1. The following relationship is only true for a merchandising firm: Beginning Inventory + Purchases (net) or Production costs for the period = Cost of Goods Available for Sale a. True b. […]

Chapter 7 The Ending inventory The Lowest Because Contains The

Chapter 7: Inventories: Cost Measurement and Flow Assumptions 105. Cabinets for Less uses FIFO for internal reporting purposes and LIFO for financial and income tax purposes. At the end of 2016, the following information was obtained from the inventory records: […]

Chapter 7 Trooper Company has provided the following inventory data

Chapter 7: Inventories: Cost Measurement and Flow Assumptions 94. The list below provides several terms connected with inventory valuation. Following the list is a series of descriptive statements. a. consignee f. gross price method b. consignor g. merchandise inventory c. […]

Chapter 7 Which of the following cannot be used as the current cost

Chapter 7: Inventories: Cost Measurement and Flow Assumptions Exhibit 7-3 Davis Co. had the following inventory activity during April: Unit Units Cost Beginning inventory 100 $ 8 Purchase (April 3) 60 12 Sale (April 10) 80 Purchase (April 18) 50 […]

Chapter 8 The accountant for Lee Company made the following errors related

Chapter 8: Inventories: Special Valuation Issues 89. The correct net income for Sarah Corp. was $53,500. However, the company reported incorrect net income because beginning inventory was understated by $2,500, purchases were overstated by $2,000, and ending inventory was overstated […]

Chapter 8 The accounting records for the current year contain the

Chapter 8: Inventories: Special Valuation Issues 116. The Baby Super Store uses the average cost retail inventory method to determine its ending inventory. The accounting records for the current year for the Baby Super Store contained the following information: Cost […]

Chapter 8 The declining value could potentially mislead decision makers

Chapter 8: Inventories: Special Valuation Issues 127. Walker Towel & Linen Shop uses the lower of cost or market method and has a periodic inventory system. Additional information follows: Inventory Date Cost Market January 1, 2016 $4,600 $4,000 December 31, […]

Chapter 8 The gross profit method is more sensitive to price changes

CHAPTER 8: INVENTORIES: SPECIAL VALUATION ISSUES 1. Reporting inventory at the lower of cost or market provides a representationally faithful value of inventory; therefore, the application of the lower of cost or market rule is consistent with the materiality principle. […]

Chapter 8 The gross profit method results in a less accurate inventor

Chapter 8: Inventories: Special Valuation Issues 49. As a result of taking a physical inventory count on December 31, 20106 the Cookie Company inventory was determined to be $425,000. The auditors for Cookie suspected an inventory shortage and used the […]

Chapter 9 Examples Amounts Determined Operating Activities Would Accrued

Chapter 9: Current Liabilities and Contingencies 107. The Captain Company began operations on January 1, 2016. In 2016, Captain’s sales were $400,000, and payments arising out of warranty obligations were $18,000. Required: a. Assume that this is an assurance-type warranty […]

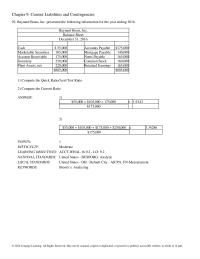

Chapter 9 For the prior fiscal year, the Radar Company paid

Chapter 9: Current Liabilities and Contingencies 92. Baynard Boats, Inc. presented the following information for the year ending 2016. Baynard Boats, Inc. Balance Sheet December 31, 2016 Cash $ 55,000 Accounts Payable $175,000 Marketable Securities 105,000 Mortgage Payable 140,000 Account […]

Chapter 9 GAAP requires the company to recognize a liability

CHAPTER 9: CURRENT LIABILITIES AND CONTINGENCIES 1. Liabilities are defined as probable future sacrifices of economic benefits arising from present obligations of a company to provide services or assets in the future as defined by the FASB. a. True b. […]

Chapter 9 Salty Chip 150 Each Past Experience Indicates

Chapter 9: Current Liabilities and Contingencies 52. Jennifer Cakes places a coupon in each box of its product. Customers may send in five coupons and $3, and the company will send them a recipe book. Sufficient books were purchased at […]

Tvm Module 4 Samos Excavating is considering purchasing some new equipment for

TVM Module: Time Value of Money Module ACCT.WHAL.TVM.6 – LO: TVM.7 ACCT.WHAL.TVM.7 – LO: TVM.7 ACCT.WHAL.TVM.8 – LO: TVM.8 NATIONAL STANDARDS: United States – BUSPROG: Reflective Thinking – BUSPROG: Analytic LOCAL STANDARDS: United States – OH – Default City – […]

Tvm Module ow much money will Georgia have on December 31, 2020

TVM Module: Time Value of Money Module KEYWORDS: Bloom’s: Analyzing 56. Table factors for present values a. decrease as the interest rate decreases b. decrease as the number of periods increases c. increase as the interest rate increases d. increase […]

Tvm Module The formula to compute the present value of a dollar is

TVM MODULE: TIME VALUE OF MONEY MODULE 1. One type of compensation provided by the time value of money is compensation for expected consumption. a. True b. False ANSWER: False POINTS: 1 DIFFICULTY: Easy LEARNING OBJECTIVES: ACCT.WHAL.TVM.1 – LO: TVM.1 […]

Tvm Module Using the compound interest tables, answer the following questions

TVM Module: Time Value of Money Module 99. Suppose you borrow money from your parents for college tuition on January 1, 2013. Your parents require four annual payments of $1,000 each, with the first payment due on January 1, 2017. […]