Archives: Solution Manual

Chapter 22 Excel File Solution Note to instructor

Continuing Case Solution 32 Chapter 22 Excel File Solution Note to instructor As an extension to the chapter 22 exercise, you could add the following requirement: Prepare the correcting entries to be made in 2013, and record the information on […]

Chapter 21 The Lease Accounted For Properly Capital Lease

Extensive detail and information is contained within the help function of Microsoft Excel and in the provided text. You should enter your name, date, instructor’s name, and course into the cells at the top of the page. This information will […]

Chapter 21 One The First Areas Studied Is What

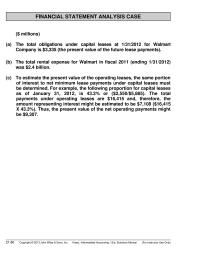

FINANCIAL STATEMENT ANALYSIS CASE ($ millions) (a) The total obligations under capital leases at 1/31/2012 for Walmart Company is $3,335 (the present value of the future lease payments). (b) The total rental expense for Walmart in fiscal 2011 (ending 1/31/2012) […]

Chapter 21 The Cost The Lease Matched With Revenue

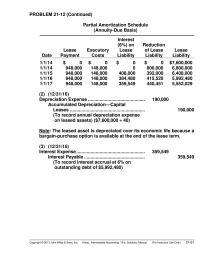

PROBLEM 21-12 (Continued) Partial Amortization Schedule (Annuity-Due Basis) Date Lease Payment Executory Costs Interest (6%) on Lease Liability Reduction of Lease Liability Lease Liability 1/1/14 $ 0 $ 0 $ 0 $ 0 $7,600,000 1/1/14 948,000 148,000 0 800,000 6,800,000 […]

Chapter 21 The Amount Capitalized Represents The Completed Service

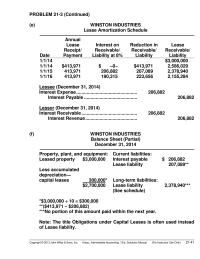

PROBLEM 21-3 (Continued) (e) WINSTON INDUSTRIES Lease Amortization Schedule Date Annual Lease Receipt/ Payment Interest on Receivable/ Liability at 8% Reduction in Receivable/ Liability Lease Receivable/ Liability 1/1/14 $3,000,000 1/1/14 $413,971 $ –0– $413,971 2,586,029 1/1/15 413,971 206,882 207,089 2,378,940 […]

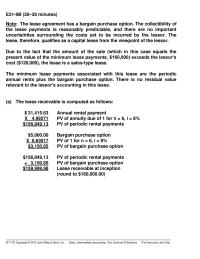

Chapter 21 The lease agreement has a bargain-purchase option

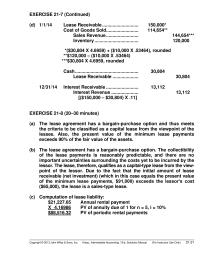

EXERCISE 21-7 (Continued) (d) 1/1/14 Lease Receivable ………………………. 150,000* Cost of Goods Sold……………………. 114,654** Sales Revenue ……………………. 144,654*** Inventory ……………………………. 120,000 * *($30,804 X 4.6959) + ($10,000 X .53464), rounded **$120,000 – ($10,000 X .53464) ***$30,804 X 4.6959, rounded Cash […]

Chapter 21 Walker Company Can Use The Sales type Lease

CHAPTER 21 Accounting for Leases ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis *1. Rationale for leasing. 1, 2, 4 1, 2 *2. Lessees; classification of leases; accounting by lessees. 3, 5, 7, 8, […]

Chapter 21 Depreciation is recorded for one month of the use

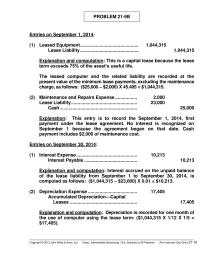

PROBLEM 21-9B Entries on September 1, 2014: (1) Leased Equipment ……………………………………… 1,044,315 Lease Liability ……………………………………… 1,044,315 Explanation and computation: This is a capital lease because the lease term exceeds 75% of the asset’s useful life. The leased computer and the […]

Chapter 21 Current Liabilities Lease Liability Interest Payable

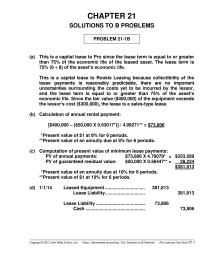

CHAPTER 21 SOLUTIONS TO B PROBLEMS PROBLEM 21-1B (a) This is a capital lease to Pro since the lease term is equal to or greater than 75% of the economic life of the leased asset. The lease term is 75% […]

Chapter 21 The lease agreement has a bargain purchase option

E21-9B (20–30 minutes) Note: The lease agreement has a bargain purchase option. The collectibility of the lease payments is reasonably predictable, and there are no important uncertainties surrounding the costs yet to be incurred by the lessor. The lease, therefore, […]

Chapter 21 Cost Fair Market Value Leased Asset

CHAPTER 21 SOLUTIONS TO B EXERCISES E21-1B (15–20 minutes) (a) This is a capital lease to Manor since the lease term (6 years) is greater than 75% of the economic life (6 years) of the leased asset. The lease term […]

Chapter 21 The Same Time There Increase Liabilities

Continuing Case Solution 29 Chapter 21 (a) Memorandum To: Eric Conner and Phil Martin, CM2 From: L. Harbach Re: Leases Date: February 13, 2013 According to FASB ASC 840-10-25-1, the lease proposal offered by Tyler Leasing Company meets at least […]

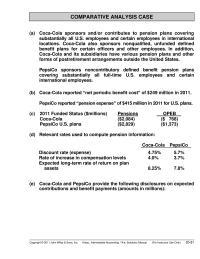

Chapter 20 Coca-Cola sponsors and/or contributes to pension

COMPARATIVE ANALYSIS CASE (a) Coca-Cola sponsors and/or contributes to pension plans covering substantially all U.S. employees and certain employees in international locations. Coca-Cola also sponsors nonqualified, unfunded defined benefit plans for certain officers and other employees. In addition, Coca-Cola and […]

Chapter 20 Accumulated other comprehensive loss

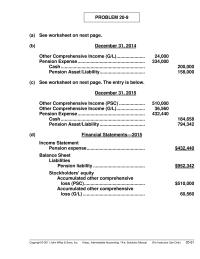

PROBLEM 20-9 (a) See worksheet on next page. (b) December 31, 2014 Other Comprehensive Income (G/L) …………………. 24,000 Pension Expense ……………………………………………. 334,000 Cash ……………………………………………………….. 200,000 Pension Asset /Liability …………………………….. 158,000 (c) See worksheet on next page. The entry is below. […]

Chapter 20 Expected Future Years Service Average Remaining Service

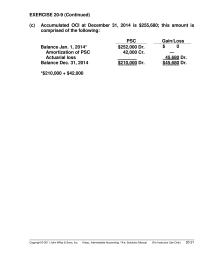

EXERCISE 20-9 (Continued) (c) Accumulated OCI at December 31, 2014 is $255,680; this amount is comprised of the following: PSC Gain/Loss Balance Jan. 1, 2014* $252,000 Dr. $ 0 Amortization of PSC 42,000 Cr. — Actuarial loss 45,680 Dr. Balance […]

Chapter 20 Unexpected Gain Amortization Contributions Benefits Increase

PROBLEM 20-7B MANGROVE CORP. Pension Worksheet—2014 General Journal Entries Memo Record Items Annual Pension Expense Cash OCI—Prior Service Cost OCI— Gain/Loss Pension Asset / Liability Projected Benefit Obligation Plan Assets Balance, Jan. 1, 2014 160,000 Cr. 520,000 Cr. 360,000 Dr. […]

Chapter 20 Because the amount of net gain or loss does not exceed

Time and Purpose of Problems (Continued) Problem 20-12 (Time 35–45 minutes) Purpose—to provide a problem that requires preparation of a worksheet, journal entries, and indicates financial statement presentation. *Problem 20-13 (Time 30–35 minutes) Purpose—to provide a problem that requires preparation […]

Chapter 20 The excess of the cumulative net gain or loss

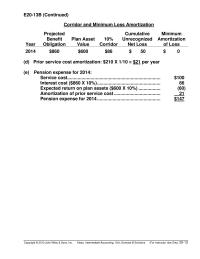

E20-13B (Continued) Corridor and Minimum Loss Amortization Year Projected Benefit Obligation Plan Asset Value 10% Corridor Cumulative Unrecognized Net Loss Minimum Amortization of Loss 2014 $860 $600 $86 $ 50 $ 0 (d) Prior service cost amortization: $210 X 1/10 […]

Chapter 20 Note to financial statements disclosing components

CHAPTER 20 SOLUTIONS TO B EXERCISES E20-1B (5–10 minutes) (a) Computation of pension expense: Service cost ………………………………………………… $250,000 Interest cost ($2,600,000 X 0.08) …………………… 208,000 Actual (expected) return on plan assets ……….. (65,000) Prior service cost amortization …………………….. 40,000 Pension […]

Chapter 20 Continuing Case Solution B Memorandum To Eric

Continuing Case Solution 25 Chapter 20 (a) Memorandum To: Eric Conner and Phil Martin, CM2 From: L. Harbach Re: Postretirement Pension Benefits Date: February 10, 2013 Defined benefit pension plans are so-named because the benefit provided to the employee is […]

Chapter 19 Significant components of P&G’s deferred tax assets

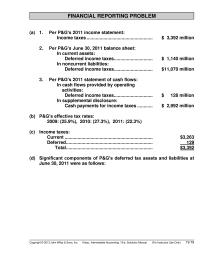

FINANCIAL REPORTING PROBLEM (a) 1. Per P&G’s 2011 income statement: Income taxes …………………………………………… $ 3,392 million 2. Per P&G’s June 30, 2011 balance sheet: In current assets: Deferred income taxes ………………………… $ 1,140 million In noncurrent liabilities: Deferred income taxes […]

Chapter 19 Reduce The Deferred Tax Asset Valuation Allowance

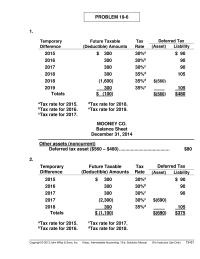

PROBLEM 19-6 1. Temporary Difference Future Taxable (Deductible) Amounts Tax Rate Deferred Tax (Asset) Liability 2015 $ 300 30%a $ 90 2016 300 30%b 90 2017 300 30%c 90 2018 300 35%d 105 2018 (1,600) 35%d $(560) 2019 300 35%e […]

Chapter 19 Pretax Financial Income Nondeductible Expense Subtotal Taxable

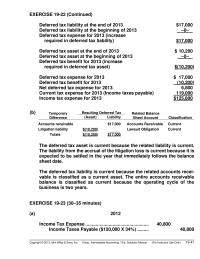

EXERCISE 19-22 (Continued) Deferred tax liability at the end of 2013 $17,000 Deferred tax liability at the beginning of 2013 –0– Deferred tax expense for 2013 (increase required in deferred tax liability) $17,000 Deferred tax asset at the end of […]

Chapter 19 Deferred Tax Liability The Beginning 2013 Deferred

EXERCISE 19-8 (10–15 minutes) (a) 2014 Income Tax Expense ………………………………………. 336,000 Deferred Tax Asset ($20,000 X 40%) ………………… 8,000 Deferred Tax Liability ($30,000 X 40%) ……… 12,000 Income Taxes Payable ($830,000 X 40%) …… 332,000 2015 Income Tax Expense ………………………………………. […]

Chapter 19 Reconcile pretax financial income with taxable income

CHAPTER 19 Accounting for Income Taxes ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Reconcile pretax financial income with taxable income. 1, 13 1, 2, 3, 4, 5, 12, 18, 20, 21 1, […]

Chapter 19 the amount of cumulative temporary difference existing

PROBLEM 19-5B (Continued) (c) 2014 Income Statement Operating loss before income taxes …………… $(140,000) Income tax benefit Benefit due to loss carryback ……………… $21,000 Benefit due to loss carryforward …………. 25,500 46,500 Net loss ……………………………………………………. $(93,500) (d) 2016 Income Statement […]

Chapter 19 Income Tax Expense Current Deferred Adjustment

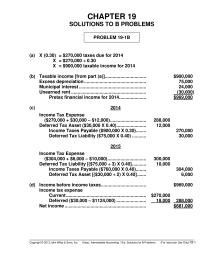

CHAPTER 19 SOLUTIONS TO B PROBLEMS PROBLEM 19-1B (a) X (0.30) = $270,000 taxes due for 2014 X = $270,000 ÷ 0.30 X = $900,000 taxable income for 2014 (b) Taxable income [from part (a)]………………………….. $900,000 Excess depreciation ………………………………………… 75,000 […]

Chapter 19 Pretax financial income is equal to the taxable

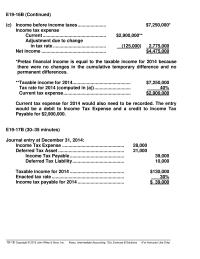

E19-16B (Continued) (c) Income before income taxes …………………. $7,250,000* Income tax expense Current …………………………………………. $2,900,000** Adjustment due to change in tax rate ………………………………….. (125,000) 2,775,000 Net income ………………………………………….. $4,475,000 *Pretax financial income is equal to the taxable income for 2014 […]

Chapter 19 Temporary difference resulting in future deductible

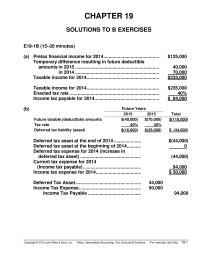

CHAPTER 19 SOLUTIONS TO B EXERCISES E19-1B (15–20 minutes) (a) Pretax financial income for 2014 ……………………………………. $125,000 Temporary difference resulting in future deductible amounts in 2015 ……………………………………………………….. 40,000 in 2014 ……………………………………………………….. 70,000 Taxable income for 2014 ……………………………………………….. $235,000 Taxable income […]

Chapter 19 Existing Contracts Firm Sales Backlog That Will

Continuing Case Solution Chapter 19 (a) Memorandum To: Eric Conner and Phil Martin, CM2 From: L. Harbach Re: Income Taxes Date: February 4, 2013 According to GAAP (see FASB ASC 740-10-05-05), the framework for the accounting for taxes is comprised […]

Chapter 18 This Represents More Conservative Policy Light The

ACCOUNTING, ANALYSIS, AND PRINCIPLES (Continued) Principles Both methods attempt to report revenues that faithfully represent the operations of the company so that future earnings and cash flows can be predicted (relevance). With the percentage-of–completion method, companies use subjective estimates (based […]

Chapter 18 Unearned Franchise Fee Revenue From Franchise

CA 18-4 (Continued) a premium, the types of customers who receive credits, and the ease of exchanging credits for premiums will all affect the proportion of credits actually redeemed in relation to the potential redemptions. The difference between the five […]

Chapter 18 An alternative valuation of the repossessed

PROBLEM 18-13 (Continued) Balance at repossession ………….. $360* Gross profit (40% X $360) ………… (144) Book value ……………………………… 216 Value of repossessed merchandise ……………………….. (100) Loss on repossession ……………… $116 *$30 X (20 payments – 8 payments) = $360 Copyright […]

Chapter 18 The actual freight costs are expenses made by

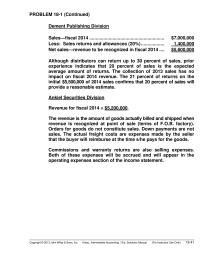

PROBLEM 18-1 (Continued) Dement Publishing Division Sales—fiscal 2014 …………………………………………………. $7,000,000 Less: Sales returns and allowances (20%) ……………… 1,400,000 Net sales—revenue to be recognized in fiscal 2014 …. $5,600,000 Although distributors can return up to 30 percent of sales, prior experience […]

Chapter 18 Installment Accounts Receivables That Are Normally Treated

EXERCISE 18-7 (Continued) 2. 6/3 Accounts Receivable (Ann Mount) ………… 7,840 Sales Revenue [$8,000 – (2% X $8,000)] ………………. 7,840 6/5 Sales Returns and Allowances ……………… 588 Accounts Receivable (Ann Mount) [$600 – (2% X $600)] ……………………. 588 6/7 Delivery […]

Chapter 18 Billings Construction Process Accounts Reported The Balance

Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only) 18-1 CHAPTER 18 Revenue Recognition ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis sales transactions; high […]

Chapter 18 Deduct Contract Costs Incurred Loss Contract

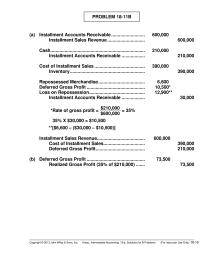

PROBLEM 18-11B (a) Installment Accounts Receivable …………………….. 600,000 Installment Sales Revenue ……………………….. 600,000 Cash ………………………………………………………………. 210,000 Installment Accounts Receivable ……………… 210,000 Cost of Installment Sales ………………………………… 390,000 Inventory …………………………………………………. 390,000 Repossessed Merchandise ……………………………… 6,600 Deferred Gross Profit ……………………………………… 10,500* Loss […]

Chapter 18 The disadvantage is that when the contract extends

CHAPTER 18 SOLUTIONS TO B PROBLEMS PROBLEM 18-1B (a) 1. The point of sale method recognizes revenue when the earnings process is complete and an exchange transaction has taken place. This can be the date goods are delivered, when title […]

Chapter 18 When Gross Profit Expressed Percentage Cost Must

E18–17B (15–25 minutes) (a) Computation of gross profit to be recognized under completed-contract method: No computation necessary. No gross profit to be recognized prior to completion of contract. Computation of billings on uncompleted contract in excess of related costs, under […]

Chapter 18 Gee would recognize revenue by discounting

CHAPTER 18 SOLUTIONS TO B EXERCISES E18-1B (5-10 minutes) (a) Notes Receivable …………………………………… 445,000 Sales Revenue ($450,000 – $5,000) ……. 445,000 (b) Sales revenue ………………………………………… $ 445,000 Interest revenue ($550,000 – $445,000) …….. 105,000 Total revenue …………………………………………. $ 550,000 E18-2B […]

Chapter 18 Revenue from disposing of assets other than products

Continuing Case Solution Chapter 18 (a) Memorandum To: Eric Conner and Phil Martin, CM2 From: L. Harbach Re: Revenue Recognition Date: February 2, 2013 The revenue recognition principle states that revenue should be recognized when the earnings process is complete, […]

Chapter 17 Compute the unrealized gains or losses and prepare

Name: Date: Instructor: Course: Cost Fair Value Unrealized Gain (Loss) Amount Amount Formula Amount Amount Formula Amount Amount Formula Formula Formula Formula Amount Formula Amount Amount Securities Total of portfolio (c) Compute the unrealized gains or losses and prepare the […]

Chapter 17 The Circumstances Leading The Decision Sell Transfer

COMPARATIVE ANALYSIS CASE THE COCA-COLA COMPANY and PEPSICO, INC. (a) Coca-Cola PepsiCo (1) Cash used in investing activities $(2,524) $(5,618) (2) Cash used for acquisitions and investments $ (977) $(3,193) (3) Total investment in unconsolidated affiliates at 12/31/11 $ 1,141 […]

Chapter 17 The Unrealized Holding Loss The Difference Between

Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only) 17–61 *PROBLEM 17-15 (a) January 7, 2014 Put Option ……………………………………………………… 360 Cash ………………………………………………………… 360 (b) March 31, 2014 Put Option ……………………………………………………… 2,000 […]

Chapter 17 Any Change The Net Unrealized Holding Gain

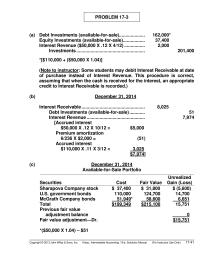

Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only) 17–41 PROBLEM 17-3 (a) Debt Investments (available-for-sale)……………….. 162,000* Equity Investments (available-for-sale) …………….. 37,400 Interest Revenue ($50,000 X .12 X 4/12) ……………. 2,000 […]

Chapter 17 Variable rate Debt Variable Rate Debt Payment Debt

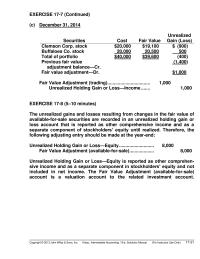

EXERCISE 17-7 (Continued) (c) December 31, 2014 Securities Cost Fair Value Unrealized Gain (Loss) Clemson Corp. stock $20,000 $19,100 ($ (900) Buffaloes Co. stock 20,000 20,500 ( 500) Total of portfolio $40,000 $39,600 ( (400) Previous fair value adjustment balance—Cr. […]

Chapter 17 The 20 Rule That Investment Direct Indirect

CHAPTER 17 Investments ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Debt securities. 1, 2, 3, 13 1 6 (a) Held-to-maturity. 4, 5, 7, 8, 10, 13, 21 1, 3 2, 3, 5 […]

Chapter 17 reported as a separate component of stockholders’

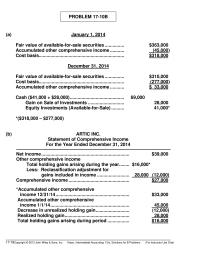

PROBLEM 17-10B (a) January 1, 2014 Fair value of available-for-sale securities …………… $363,000 Accumulated other comprehensive income ……….. (45,000) Cost basis………………………………………………………… $318,000 December 31, 2014 Fair value of available-for-sale securities …………… $310,000 Cost basis………………………………………………………… (277,000) Accumulated other comprehensive income ……….. […]

Chapter 17 The Entries Would The Same Except That

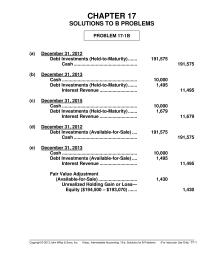

CHAPTER 17 SOLUTIONS TO B PROBLEMS PROBLEM 17-1B (a) December 31, 2012 Debt Investments (Held-to-Maturity) ……. 191,575 Cash …………………………………………. 191,575 (b) December 31, 2013 Cash …………………………………………………. 10,000 Debt Investments (Held-to-Maturity) ……. 1,495 Interest Revenue ……………………….. 11,495 (c) December 31, 2015 […]

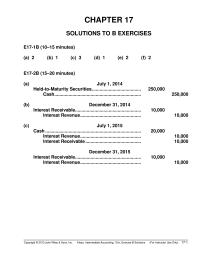

Chapter 17 Schedule of Interest Revenue and Bond Discount

Interest Receivable…………………………………………… 10,000 Interest Revenue ……………………………………….. 10,000 (c) July 1, 2015 Cash ……………………………………………………………….. 20,000 Interest Revenue ……………………………………….. 10,000 Interest Receivable ……………………………………. 10,000 December 31, 2015 Interest Receivable…………………………………………… 10,000 Interest Revenue ……………………………………….. 10,000 CHAPTER 17 SOLUTIONS TO B EXERCISES E17-1B (10–15 […]