Archives: Solution Manual

Chapter 17 Continuing Case Solution Judgment Necessary Assess The

Continuing Case Solution 7 Chapter 17 (a) 1. Stock investment in Infrared of 10% of the outstanding voting stock: DR CR Cash ($24,000 x 10%) 2,400 2. Stock investment in Infrared of 30% of the outstanding voting stock: DR CR […]

Chapter 16 FASB allows companies to rebut the presumption that contracts

PROFESSIONAL SIMULATION (Continued) Schedule A *Computation of weighted-average number of shares adjusted for dilutive securities Average number of shares under options outstanding …………. 140,000 Option price per share ……………………………………………………….. X $10 Proceeds upon exercise of options …………………………………….. $1,400,000 Market price […]

Chapter 16 Eps Standards Are Important Analysts Who Rely

CA 16-6 (Continued) 36,000 [(30,000 X $30) ÷ $25] shares of treasury stock at $25 with the proceeds. Therefore, if you add the 30,000 exercised warrants to the common stock outstanding and then subtract the 36,000 shares presumably purchased, the […]

Chapter 16 That Portion The Proceeds Assigned The Warrants

PROBLEM 16-1 (Continued) Calculations: Common Stock Paid-in Capital in Excess of Par At beginning of year ………………….. 300,000 shares $ 600,000 From stock rights (entry #3) ………. 9,500 shares 209,000 From stock warrants (entry #4) ….. 1,600 shares 44,800 From […]

Chapter 16 Income Before Income Taxes Income Taxes 40

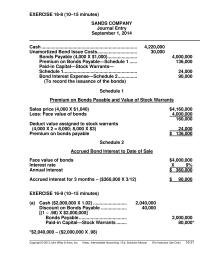

EXERCISE 16-8 (10–15 minutes) SANDS COMPANY Journal Entry September 1, 2014 Cash ……………………………………………………………….. 4,220,000 Unamortized Bond Issue Costs…………………………. 30,000 Bonds Payable (4,000 X $1,000) ………………….. 4,000,000 Premium on Bonds Payable—Schedule 1 …… 136,000 Paid-in Capital—Stock Warrants— Schedule 1 ………………………………………………… 24,000 […]

Chapter 16 Fair Value Estimated Using Acceptable Option Pricing

CHAPTER 16 Dilutive Securities and Earnings Per Share ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Convertible debt and preferred stock. 1, 2, 3, 4, 5, 6, 7 1, 2, 3 1, 2, […]

Chapter 16 memo entry made to indicate the number of rights

CHAPTER 16 Dilutive Securities and Earnings Per Share SOLUTIONS TO B PROBLEMS PROBLEM 16-1B **Allocated to Bonds: $97 X $1,060,000 = $970,000; $97 + $9 Discount = $1,000,000 – $970,000 = $30,000 **Allocated to Warrants: $9 X $1,060,000 = $90,000 […]

Chapter 16 Weighted-average number of shares outstanding

E16-16B (Continued) (d) Income from continuing operationsa $1.06 Loss from discontinued operationsb (0.08) Net income $0.98 a Net income available for common $6,552,000 Add: Loss from discontinued operations 500,000 Income from continuing operations $7,052,000 $7,052,000 = $1.06 6,660,000 b $(500,000) […]

Chapter 16 When The Warrants Are Nondetachable Separate Recognition

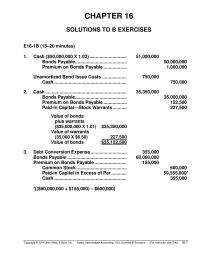

CHAPTER 16 SOLUTIONS TO B EXERCISES E16-1B (15–20 minutes) 1. Cash ($50,000,000 X 1.02) ……………………….. 51,000,000 Bonds Payable …………………………………. 50,000,000 Premium on Bonds Payable ……………… 1,000,000 Unamortized Bond Issue Costs ………………. 750,000 Cash ……………………………………………….. 750,000 2. Cash ……………………………………………………… 35,350,000 Bonds […]

Chapter 16 Diluted Earnings Per Share Deps Of calculation Deps

Continuing Case Solution Chapter 16 Memorandum To: Eric Conner and Phil Martin, CM2 From: L. Harbach Re: Basic and Diluted Earnings Per Share Date: January 28, 2013 If CM2 decided to issue 5% cumulative, convertible preferred stock and complex. This […]

Chapter 15 Major Differences Relate Terminology Used Introduction Items

FINANCIAL STATEMENT ANALYSIS CASES CASE 1 (a) Management might purchase treasury stock to provide to stockholders a tax-efficient method for receiving cash from the corporation. In addition, it might have to repurchase shares to have them available to issue to […]

Chapter 15 The Stock Dividend Results Increase The Amount

PROBLEM 15–12 PENN COMPANY Stockholders’ Equity June 30, 2015 Capital stock 8% preferred stock, $25 par value, cumulative and nonparticipating, 100,000 shares authorized, 40,000 shares issued and outstanding—Note A ……………. $1,000,000 Common stock, $10 par value, 300,000 shares authorized, 115,400 […]

Chapter 15 Emporia Plastics Inc Trading The Equity Successfully

EXERCISE 15-6 (25–30 minutes) (a) Cash [(5,000 X $45) – $7,000] ……………………………… 218,000 Common Stock (5,000 X $5) ………………………… 25,000 Paid-in Capital in Excess of Par— Common Stock …………………………..……………. 193,000 (b) Land (1,000 X $46) …………………………………………….. 46,000 Common Stock (1,000 […]

Chapter 15 Paid-in capital in excess of par no effect

PROBLEM 15-8B (Continued) Note: The journal entries made for the previous transaction are: Equity Investments ($3.50 – $3.10) X 10,250 …………… 4,100 Unrealized Holding Gain or Loss—Income ………. 4,100 (To record increase in value of securities to be issued) Retained […]

Chapter 15 Wellington declares and issues a 15% stock dividend

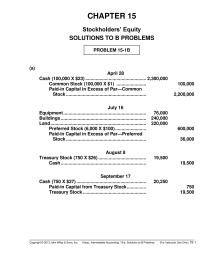

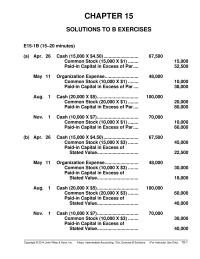

CHAPTER 15 Stockholders’ Equity SOLUTIONS TO B PROBLEMS PROBLEM 15-1B (a) April 28 Cash (100,000 X $23) ……………………………………….. 2,300,000 Common Stock (100,000 X $1) ………………….. 100,000 Paid-in Capital in Excess of Par—Common Stock …………………………………………………….. 2,200,000 July 16 Equipment ………………………………………………………. 76,000 […]

Chapter 15 One might use the cost of treasury stock

May 11 Organization Expense …………………….. 48,000 Common Stock (10,000 X $1) …….. 10,000 Paid-in Capital in Excess of Par …. 38,000 Aug. 1 Cash (20,000 X $5) ………………………….. 100,000 Common Stock (20,000 X $1) …….. 20,000 Paid-in Capital in Excess […]

Chapter 15 Equity Has Indefinite Life With Maturity Date

Continuing Case Solution 1 Chapter 15 (a) [Note to the instructor: You could require the students to show the journal entry for issuing each type of debt or equity instrument and the related interest or dividend payments.] Memorandum To: Eric […]

Chapter 14 Interest Expense Or Bond Issue Expense Would

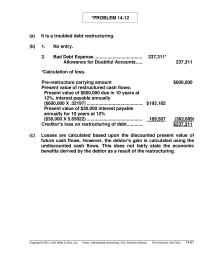

*PROBLEM 14-12 (a) It is a troubled debt restructuring. (b) 1. No entry. 2. Bad Debt Expense …………………………………………. 237,311* Allowance for Doubtful Accounts …………….. 237,311 *Calculation of loss. Pre-restructure carrying amount $600,000 Present value of restructured cash flows: Present value […]

Chapter 14 American Bank Under The Debt Restructuring Agreement

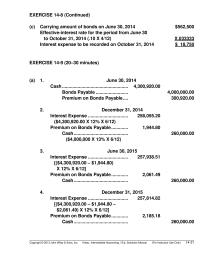

EXERCISE 14-8 (Continued) (c) Carrying amount of bonds on June 30, 2014 $562,500 Effective-interest rate for the period from June 30 to October 31, 2014 (.10 X 4/12) X.033333 Interest expense to be recorded on October 31, 2014 $ 18,750 […]

Chapter 14 Longterm Liabilities Assignment Classification Table By

CHAPTER 14 Long-Term Liabilities ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Long-term liability; classification; definitions. 1, 10, 14, 22 1, 2 10, 11 1, 2 2. Issuance of bonds; types of bonds. […]

Chapter 14 Cash Interest Carrying Paid Expense Premium Amount

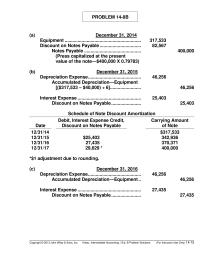

PROBLEM 14-8B (a) December 31, 2014 Equipment ………………………………………………………. 317,533 Discount on Notes Payable ………………………….. 82,567 Notes Payable ……………………………………………….. 400,000 (Press capitalized at the present value of the note—$400,000 X 0.79783) (b) December 31, 2015 Depreciation Expense …………………………………………….. 46,256 Accumulated Depreciation—Equipment […]

Chapter 14 Proceeds From Sale Bonds Premium Bonds

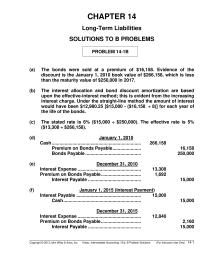

CHAPTER 14 Long-Term Liabilities SOLUTIONS TO B PROBLEMS PROBLEM 14-1B (a) The bonds were sold at a premium of $16,158. Evidence of the discount is the January 1, 2010 book value of $266,158, which is less than the maturity value […]

Chapter 14 Maturities and sinking fund requirements on long-term

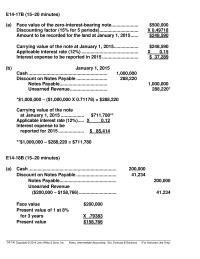

E14-17B (15–20 minutes) (a) Face value of the zero-interest-bearing note………………… $500,000 Discounting factor (15% for 5 periods) ………………………… X 0.49718 Amount to be recorded for the land at January 1, 2015 …… $248,590 Carrying value of the note at January […]

Chapter 14 Interest Expense For The Period From January

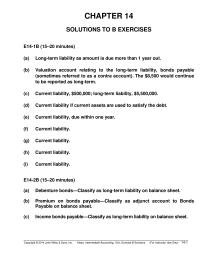

CHAPTER 14 SOLUTIONS TO B EXERCISES E14-1B (15–20 minutes) (a) Long-term liability as amount is due more than 1 year out. (b) Valuation account relating to the long-term liability, bonds payable (sometimes referred to as a contra account). The $8,500 […]

Chapter 13 The warranty payable and the interest payable

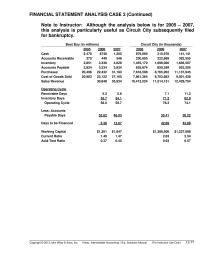

FINANCIAL STATEMENT ANALYSIS CASE 3 (Continued) Note to Instructor: Although the analysis below is for 2005 – 2007, this analysis is particularly useful as Circuit City subsequently filed for bankruptcy. Best Buy (in millions) Circuit City (in thousands) 2005 2006 […]

Chapter 13 These Audits May Result The Assessment Additional

FINANCIAL REPORTING PROBLEM (Continued) (c) P&G provided the following discussion related to commitments and contingencies: Note 10: Commitments and Contingencies Guarantees In conjunction with certain transactions, primarily divestitures, we may provide routine indemnifications (e.g., indemnification for representa– tions and warranties […]

Chapter 13 Windsor Airlines need not establish a liability

PROBLEM 13-7 (a) (1) Cash ………………………………………………………. 4,440,000 Sales Revenue (600 X $7,400) ………………………….. 4,440,000 (2) Warranty Expense ([600 X $390] / 2) …………………………. 117,000 Inventory ($170 X 600 X 1/2) ………………………….. 51,000 Salaries and Wages Payable ($220 X 600 X […]

Chapter 13 The Student Must Compute Income Tax Withheld

EXERCISE 13-6 (Continued) (b) Accrued liability at year-end: 2013 2014 Jan. 1 balance $ 0 $7,740 + accrued 7,740 8,352 – paid ( 0) (6,966) Dec. 31 balance $7,740 (1) $9,126 (2) (1) 9 employees X $10.75/hr. X 8 hrs./day […]

Chapter 13 Financial statement impact of liability transactions

CHAPTER 13 Current Liabilities and Contingencies ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Concept of liabilities; definition and classification of current liabilities. 1, 2, 3, 4, 6, 8 1, 16 1, 2 […]

Chapter 13 Because the cause for litigation occurred before

PROBLEM 13-9B (Continued) 2015 Inventory of Premiums …………………………………………… 400,000 Cash ……………………………………………………………… 400,000 (To record the purchase of 500,000 download codes at $0.80 each) Cash ……………………………………………………………………… 1,520,000 Sales Revenue ……………………………………………….. 1,520,000 (To record the sale of 7,600,000 candy bars at 20 […]

Chapter 13 Current Liabilities Warranty Liability 189750 Longterm

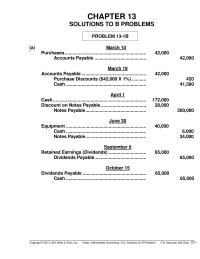

CHAPTER 13 SOLUTIONS TO B PROBLEMS PROBLEM 13-1B (a) March 10 Purchases ……………………………………………………… 42,000 Accounts Payable …………………………………. 42,000 March 19 Accounts Payable ………………………………………….. 42,000 Purchase Discounts ($42,000 X 1%) ……….. 420 Cash …………………………………………………….. 41,580 April 1 Cash ……………………………………………………………… 172,000 Discount […]

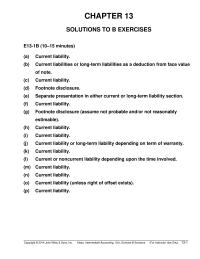

Chapter 13 Separate presentation in either current or long-term

(c) Current liability. (d) Footnote disclosure. (e) Separate presentation in either current or long-term liability section. (f) Current liability. (g) Footnote disclosure (assume not probable and/or not reasonably estimable). (l) Current or noncurrent liability depending upon the time involved. (m) […]

Chapter 13 Unearned Revenue Account Make Sure That The

Continuing Case Solution Chapter 13 Part I Memorandum To: Eric Conner and Phil Martin, CM2 From: L. Harbach Re: Unearned Revenue and Contingencies Date: January 24, 2013 Here are the answers to your questions for the year ended December 31, […]

Chapter 12 Assets Gt 350 Intangibles Goodwill And

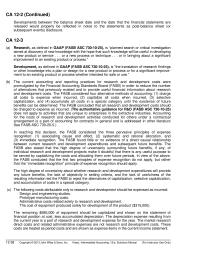

CA 12-2 (Continued) Developments between the balance sheet date and the date that the financial statements are released would properly be reflected in notes to the statements as post-balance sheet (or subsequent events) disclosure. CA 12-3 (a) Research, as defined […]

Chapter 12 Fair Value Conchita Division Carrying Value

EXERCISE 12-11 (Continued) (b) Analysis of 2014 transactions 1. The $245,700 incurred for research and development should be expensed. 2. The book value of Patent B is $11,250 and its estimated future cash flows are $6,000: (3 X $2,000); therefore […]

Chapter 12 The Impairment Loss Measured The Amount Which

CHAPTER 12 Intangible Assets ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Intangible assets; concepts, definitions; items comprising intangible assets. 1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12, 13, […]

Chapter 12 Research and development expense in the income statement

CHAPTER 12 SOLUTIONS TO B PROBLEMS PROBLEM 12-1B Franchises …………………………………………………………… 60,000 Prepaid Rent ………………………………………………………… 24,000 Retained Earnings (Net loss + R&D) ………………………. 108,000 Patents ($80,000 + $13,500) …………………………………… 93,500 Research and Development Expense …………………….. 265,000 Intangible Assets …………………………………………. 550,500 Amortization […]

Chapter 12 Events such as an expectation of selling assets

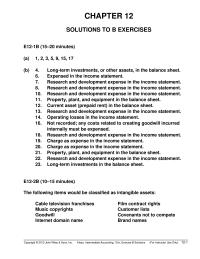

Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Exercise B Solutions (For Instructor Use Only) 12-1 Music copyrights Customer lists Goodwill Covenants not to compete Internet domain name Brand names CHAPTER 12 SOLUTIONS TO B EXERCISES […]

Chapter 12 The goodwill is considered impaired because the fair

Continuing Case Solution Chapter 12 Part I Memorandum To: Eric Conner and Phil Martin, CM2 From: L. Harbach Re: Goodwill and R&D Costs Date: January 20, 2013 Goodwill: Goodwill is defined as the excess cost over the fair value of […]

Chapter 11 Encino Athletic Equipment Company are calculated

Name: Date: Instructor: Course: for $315,000 10 $15,000 240,000 25,000 2,650 25,500 Amount Amount Formula Number Formula Number Formula Depreciable value: Life units expected: Depreciation per unit: Period units: Period depreciation: Amount Amount Formula Number Formula Number Formula Formula Formula […]

Chapter 11 Depreciation Not Taken Assets Intended Sold

PROFESSIONAL RESEARCH (Continued) 35–30 For example, valuation techniques consistent with the market approach often use market multiples derived from a set of comparables. Multiples might lie in ranges with a different multiple for each comparable. The selection of where within […]

Chapter 11 You Also Mentioned That Using Straightline Depreciation

SOLUTIONS TO CONCEPTS FOR ANALYSIS CA 11-1 (a) The purpose of depreciation is to distribute the cost (or other book value) of tangible plant assets, less salvage, over their useful lives in a systematic and rational manner. Under generally accepted […]

Chapter 11 Homework Sons Inc 150 115 10 Cost Rate

PROBLEM 11-2 Depreciation Expense 2014 2015 (a) Straight-line: ($89,000 – $5,000) ÷ 7 = $12,000/yr. 2014: $12,000 X 7/12 $7,000 2015: $12,000 $12,000 (b) Units-of-output: ($89,000 – $5,000) ÷ 525,000 units = $.16/unit 2014: $.16 X 55,000 8,800 2015: $.16 […]

Chapter 11 Machine C—Using the double-declining balance method

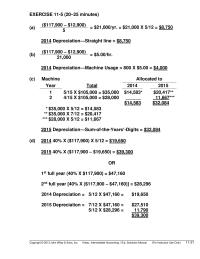

EXERCISE 11-5 (20–25 minutes) (a) ($117,900 – $12,900) = $21,000/yr. = $21,000 X 5/12 = $8,750 5 2014 Depreciation—Straight line = $8,750 (b) ($117,900 – $12,900) = $5.00/hr. 21,000 2014 Depreciation—Machine Usage = 800 X $5.00 = $4,000 (c) Machine […]

Chapter 11 The Principal Disadvantage That After Period Time

CHAPTER 11 Depreciation, Impairments, and Depletion ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Depreciation methods; meaning of depreciation; choice of depreciation methods. 1, 2, 3, 4, 5, 6, 10, 14, 20, 21, […]

Chapter 11 The amounts to be recorded on the books of Darby

CHAPTER 11 Depreciation, Impairments, and Depletion SOLUTIONS TO B PROBLEMS PROBLEM 11-1 (a) 1. Depreciable Base Computation: Purchase price ………………………… $85,000 Less: Purchase discount (2%) ….. 1,700 Freight-in ………………………………… 800 Installation ………………………………. 3,800 87,900 Less: Salvage value ………………… 1,500 Depreciation […]

Chapter 11 The Year Which There Are Remaining Years

CHAPTER 11 SOLUTIONS TO B EXERCISES E11-1B (15–20 minutes) (a) Straight-line method depreciation for each of Years 1 through 3 = $500,000 – $50,000 = $45,000 10 (b) Sum-of-the-years’-digits = 10 X 11 = 55 2 10/55 X ($500,000 – […]

Chapter 11 Continuing Case Solution A Memorandum To

Continuing Case Solution Chapter 11 (a) Memorandum To: Eric Conner and Phil Martin, CM2 From: L. Harbach Re: Depreciation and Impairment Date: January 18, 2013 According to FASB ASC 360-10-35-4: The cost of a productive facility is one of the […]

Chapter 10 This illustrates the exception to no gain or loss recognition

PROBLEM 10-9 (Continued) Wiggins, Inc.’s Books Cash ……………………………………………………………… 15,000 Machienry (A) ………………………………………………… 50,400** Accumulated Depreciation—Machinery (B) ……… 47,000 Machinery (B) …………………………………………. 110,000 Gain on Disposal of Machinery ………………… 2,400* Computation of total gain: Fair value of Asset B $75,000 Less: […]

Chapter 10 Typical transactions involve allocation of the cost

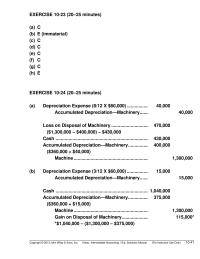

EXERCISE 10-23 (20–25 minutes) (a) C (b) E (immaterial) (c) C (d) C (e) C (f) C (g) C (h) E EXERCISE 10-24 (20–25 minutes) (a) Depreciation Expense (8/12 X $60,000) …………………….. 40,000 Accumulated Depreciation—Machinery ……………. 40,000 Loss on Disposal […]